|

市场调查报告书

商品编码

1940777

欧洲智慧电錶:市场占有率分析、产业趋势与统计、成长预测(2026-2031 年)Europe Smart Meter - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

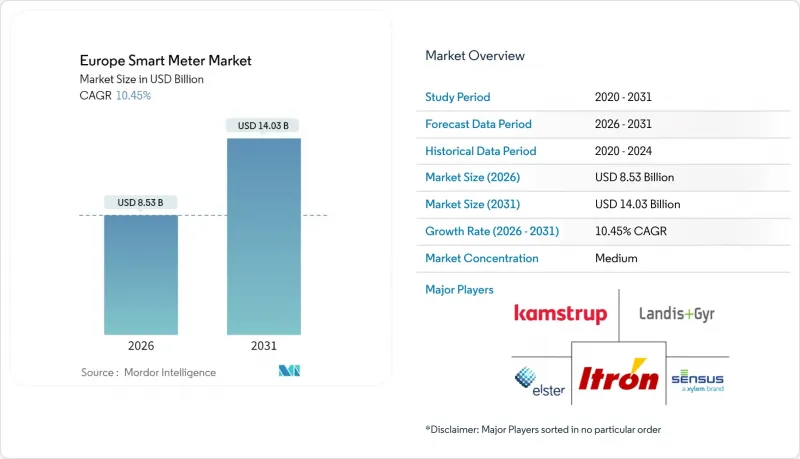

预计到 2026 年,欧洲智慧电錶市场规模将达到 85.3 亿美元,高于 2025 年的 77.2 亿美元。

预计到 2031 年将达到 140.3 亿美元,2026 年至 2031 年的复合年增长率为 10.45%。

严格的合规要求、电网现代化改造以及紧迫的数位化专案持续推动着这一成长趋势。欧盟指令2019/944强制要求所有成员国完成高阶计量系统的建设,即使短期成本效益看似有限,也能确保安装量的稳定成长。公共产业正在大规模部署可再生能源之前升级其计量基础设施,而新兴的交易型能源示范专案也为近即时资料交换的商业价值提供了支援。硬体商品化降低了计量表的初始成本,而随着公用事业公司将数据丰富的服务货币化,软体和分析服务的收入正在快速增长。随着差异化的通讯协定、网路安全安全功能和边缘分析能力成为决定性竞争优势,供应商之间的整合正在加速。

欧洲智慧电錶市场趋势与洞察

欧盟范围内的强制采用目标推动了合规速度的加快

根据2019/944号指令,安装义务确保了计量表供应商即使在成本敏感型市场也能获得销售量资讯。奥地利的目标是到2024年达到95%以上的普及率,而比利时已达到70%的覆盖率,拥有440万台设备。同时,政府也推出了产消者投资补贴,缩短了家庭用户的投资回收期。在德国,2032年这项法定完成日期已成为一个明确的里程碑,促进了现有公共产业和数位零售商之间的合作。围绕DLMS/COSEM通讯协定的整合消除了传统的互通性障碍,使供应商能够优化规模经济并进一步降低单位成本。

智慧电网和分散式能源(DER)的日益整合增加了数据需求。

屋顶光电发电和储能係统的快速普及,使得电网营运商必须在不到一小时内收集到负载曲线,以实现动态计费。荷兰一项针对1400个智慧水錶的试点研究表明,增加压力和洩漏分析功能可使电网效率提高89%,这充分证明了详细数据如何支持资产优化。在德国,动态计费系统依靠双向连接来引导灵活的需求,并使本地发电与用电量相符。由欧盟「地平线计画」资助的BeFlexible计画汇集了来自七个国家的21个合作伙伴,旨在建立互通性框架,该框架以先进的计量技术作为底层感测器层。

高昂的前期成本和网路安全风险限制了采用速度。

在德国,安装成本仍维持在 643 至 883 欧元之间,远超过法律规定的客户自付上限。围绕这些成本的法律挑战导致专案进度延误,并增加了公共产业的资金筹措需求。同时,NIS2 指令增加了加密和持续威胁监控的义务,从而增加了资本和营运成本。在英国,早期设备故障削弱了用户信心,迫使供应商拨出额外预算用于客户支援宣传活动和更换计画。儘管有证据显示长期来看可以节省成本,但这些摩擦正在减缓短期内的普及速度。

细分市场分析

智慧能源设备将在2025年继续推动营收成长,其中水务产业预计到2031年将以11.6%的复合年增长率领先。欧洲智慧水錶市场正在扩张,这主要得益于超音波技术,该技术可提供15-20年的电池寿命、声学洩漏检测和远端压力监测功能,这些功能已在比利时得到验证,目前已安装20.5万台。在义大利强制实施无线M-Bus连接政策的推动下,超音波燃气表近期获得了4.5万台的订单。日益严峻的水资源短缺问题凸显了洩漏分析的商业价值,公共产业即时进行升级改造。

物联网赋能的维修具有更大的交叉销售潜力,尤其是在LoRaWAN和NB-IoT回程传输无需电网站点配电的情况下。随着电錶规模的扩大,价格面临下行压力,而专用水和燃气设备由于内置压力、防篡改和声学特征感测器,仍能保持较高的利润率。随着网路洩漏检测技术在减少非收益用水方面展现出直接作用,即使在价格管制严格的地区,董事会也越来越倾向于核准相关投资。

儘管电力线通讯(PLC)仍保持着43.10%的市场份额,但欧洲智慧电錶市场正迅速采用蜂窝技术,因为营运商可以将网路维护外包给通讯业者。目前,NB-IoT和LTE-M模组的电池寿命已达10年,并具备远端韧体空中升级(FOTA)功能。英国正在进行基于4G的电錶回程传输试验,为计画中的2G/3G服务终止做准备。供水事业已订购了200万个蜂窝单元,并表示需要运营商级别的服务等级协定(SLA)。在PLC方面投入巨资的公用事业公司正在製定分阶段迁移计划,以防止资产閒置,但大多数新竞标都集中在混合或全蜂窝解决方案上。

蜂窝网路管理服务模式将资本支出 (CapEx) 转变为营运支出 (OpEx),并符合允许收取网路服务费用但限制消费者价格的法规结构。除了能源数据外,同一张 SIM 卡还可以承载可升级的应用程序,涵盖电能品质指标和变压器级分析,与一次性 PLC 链路相比,可提高生命週期投资回报率。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 欧盟内部强制实施目标(2019/944)

- 对智慧电网和分散式能源(DER)整合的需求日益增长

- 智慧城市数位化计划

- 交易能源试点项目

- 市场数据需要即时柔软性

- 包含物联网漏水侦测系统维修工程的套装出售

- 市场限制

- 高昂的初始成本和网路安全风险

- 旧有系统互通性差距

- 消费者隐私引发的强烈反弹以及资料片段化问题

- 半导体供应链瓶颈

- 产业价值链分析

- 监管环境

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 宏观经济趋势的影响

第五章 市场规模与成长预测

- 按计量类型

- 智慧电錶

- 智慧燃气表

- 智慧水錶

- 透过通讯技术

- 电力线路通讯(PLC)

- 射频(RF网状)

- 蜂窝通讯(2G/4G/NB-IoT)

- 有线乙太网路/光纤

- 按组件

- 硬体

- 软体和分析

- 服务(实施、AMI 管理)

- 最终用户

- 住宅

- 商业的

- 工业的

- 爱别

- 单相

- 三相

- 按国家/地区

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 比利时

- 荷兰

- 其他欧洲地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Landis+Gyr Group AG

- Itron, Inc.

- Kamstrup A/S

- Sensus USA Inc.(Xylem)

- Elster GmbH(Honeywell)

- Diehl Metering GmbH

- Apator SA

- Zenner International GmbH and Co. KG

- Arad Ltd.

- Aclara Technologies LLC

- Aidon Oy

- ADD GRUP SRL

- Networked Energy Services Corp.

- Iskraemeco dd

- Elgama-Elektronika UAB

- Holley Technology Ltd.

- ZIV Automation SL

- Wasion Group Holdings Ltd.

- Kaifa Technology(Europe)

- Secure Meters Europe Ltd.

- Sagemcom Energy and Telecom SAS

第七章 市场机会与未来展望

Europe smart meter market size in 2026 is estimated at USD 8.53 billion, growing from 2025 value of USD 7.72 billion with 2031 projections showing USD 14.03 billion, growing at 10.45% CAGR over 2026-2031.

Robust compliance mandates, grid-modernization efforts, and urgent digitalization programs continue to anchor this growth path. EU Directive 2019/944 obliges every member state to complete advanced metering rollouts, guaranteeing consistent installation volumes even when short-term cost-benefit arguments appear marginal. Utilities are upgrading measurement infrastructure ahead of large-scale renewable additions, while emerging transactive-energy pilots confirm the business case for near-real-time data exchange. Hardware commoditization is lowering upfront meter prices, but software and analytics revenues are rising fast as utilities monetize data-rich services. Consolidation among equipment vendors is intensifying because differentiated communication protocols, cybersecurity features, and edge analytics capabilities now define competitive advantage.

Europe Smart Meter Market Trends and Insights

EU-wide Mandatory Rollout Targets Drive Compliance Acceleration

Binding installation obligations under Directive 2019/944 guarantee volume visibility for metering suppliers even in cost-sensitive markets. Austria surpassed 95% penetration in 2024, and Belgium achieved 70% coverage with 4.4 million devices while offering prosumer investment premiums that ease household payback periods. Germany's legally enshrined completion deadline in 2032 imposes clear milestones, encouraging partnerships between incumbent utilities and digital retailers. Convergence around DLMS/COSEM protocols now removes the former interoperability barrier, letting vendors optimize economies of scale and lowering unit prices further.

Growing Smart-Grid and DER Integration Amplifies Data Requirements

Surging rooftop PV and battery uptake oblige network operators to collect sub-hourly load profiles for dynamic-tariff settlement. Dutch pilots using 1,400 smart water meters delivered 89% network-efficiency gains after adding pressure and leak analytics, demonstrating how granular data supports asset optimization. In Germany, dynamic tariffs rely on bidirectional connectivity to nudge flexible demand and align local generation with consumption. Horizon-Europe-funded BeFlexible connects 21 partners across seven countries, establishing interoperability frameworks that require advanced metering as the foundational sensor layer.

High Upfront Costs and Cybersecurity Risks Constrain Deployment Velocity

Installation prices in Germany still range from EUR 643-883, well above the legally capped customer charge. Legal challenges over those costs delay schedules and inflate utility financing needs. Parallelly, the NIS2 directive adds encryption and continuous threat-monitoring mandates that raise equipment and operating expenditure. Earlier U.K. device malfunctions undermined user confidence, compelling suppliers to allocate extra budgets for customer-support campaigns and replacement programs. These frictions slow short-term uptake despite long-term cost-savings evidence.

Other drivers and restraints analyzed in the detailed report include:

- Smart-City Digitalization Programs Create Cross-Sector Synergies

- Transactive-Energy Pilots Establish New Revenue Models

- Semiconductor Supply-Chain Bottlenecks Extend Lead Times

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Smart electricity devices continued to dominate revenue in 2025, yet the water category is forecast to log the highest 11.6% CAGR through 2031. The Europe smart meter market size for water applications is expanding because ultrasonic technology offers 15-20 year battery life, acoustic leak detection, and remote pressure monitoring capabilities already validated through 205,000-unit deployments in Belgium. Ultrasonic gas meters benefit from Italian mandates requiring wireless M-Bus connectivity, with recent awards covering 45,000 units. Water scarcity concerns enhance the business case for leak analytics, pushing utilities toward immediate upgrades.

IoT-enabled retrofits increase cross-selling potential, especially when LoRaWAN or NB-IoT backhaul eliminates the need for grid-site power. Electricity meters face price compression as scale grows; meanwhile, specialized water and gas devices maintain higher margins because they include pressure, tamper, and acoustic-signature sensors. As networked leak-detection proves its direct non-revenue-water savings, boards authorize faster investments even in price-controlled regions.

While PLC retains a 43.10% share, the Europe smart meter market is witnessing rapid cellular uptake because operators can outsource network maintenance to telcos. NB-IoT and LTE-M modules now ship with 10-year battery life profiles and remote firmware-over-the-air features. U.K. trials using 4G for meter backhaul prepare the estate for planned 2G/3G sunsets, and water utilities have already ordered 2 million cellular units, citing carrier-grade SLAs. Utilities with deep PLC investments are mapping phased migrations to prevent stranded-asset losses, but most new tenders emphasize hybrid or full-cellular architectures.

Cellular's managed-service model shifts capex to opex, fitting regulatory frameworks that cap consumer charges yet allow network-service fees. Beyond energy data, the same SIM can host upgradeable applications covering power-quality metrics or transformer-level analytics, improving lifetime ROI compared with single-purpose PLC links.

The Europe Smart Meter Market Report is Segmented by Meter Type (Smart Electricity Meter, Smart Gas Meter, and Smart Water Meter), Communication Technology (Power-Line Communication, Radio Frequency, and More), Component (Hardware, Software and Analytics, and Services), End-User (Residential, Commercial, and Industrial), Phase (Single-Phase and Three-Phase), and Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Landis+Gyr Group AG

- Itron, Inc.

- Kamstrup A/S

- Sensus USA Inc. (Xylem)

- Elster GmbH (Honeywell)

- Diehl Metering GmbH

- Apator SA

- Zenner International GmbH and Co. KG

- Arad Ltd.

- Aclara Technologies LLC

- Aidon Oy

- ADD GRUP SRL

- Networked Energy Services Corp.

- Iskraemeco d.d.

- Elgama-Elektronika UAB

- Holley Technology Ltd.

- ZIV Automation S.L.

- Wasion Group Holdings Ltd.

- Kaifa Technology (Europe)

- Secure Meters Europe Ltd.

- Sagemcom Energy and Telecom SAS

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumption And Market Definition

- 1.2 Scope of the study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EU?wide mandatory rollout targets (2019/944)

- 4.2.2 Growing smart-grid and DER integration needs

- 4.2.3 Smart-city digitalisation programs

- 4.2.4 Transactive-energy pilot schemes

- 4.2.5 Real-time flexibility-market data demand

- 4.2.6 IoT leak-detection bundling with retrofits

- 4.3 Market Restraints

- 4.3.1 High upfront cost and cyber-security risk

- 4.3.2 Legacy-system interoperability gaps

- 4.3.3 Consumer privacy backlash vs data granularity

- 4.3.4 Semiconductor supply-chain bottlenecks

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Trends

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Meter Type

- 5.1.1 Smart Electricity Meter

- 5.1.2 Smart Gas Meter

- 5.1.3 Smart Water Meter

- 5.2 By Communication Technology

- 5.2.1 Power-Line Communication (PLC)

- 5.2.2 Radio Frequency (RF Mesh)

- 5.2.3 Cellular (2G/4G/NB-IoT)

- 5.2.4 Wired Ethernet/Fiber

- 5.3 By Component

- 5.3.1 Hardware

- 5.3.2 Software and Analytics

- 5.3.3 Services (Deployment, AMI-managed)

- 5.4 By End-User

- 5.4.1 Residential

- 5.4.2 Commercial

- 5.4.3 Industrial

- 5.5 By Phase

- 5.5.1 Single-Phase

- 5.5.2 Three-Phase

- 5.6 By Country

- 5.6.1 United Kingdom

- 5.6.2 Germany

- 5.6.3 France

- 5.6.4 Italy

- 5.6.5 Spain

- 5.6.6 Belgium

- 5.6.7 Netherlands

- 5.6.8 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Landis+Gyr Group AG

- 6.4.2 Itron, Inc.

- 6.4.3 Kamstrup A/S

- 6.4.4 Sensus USA Inc. (Xylem)

- 6.4.5 Elster GmbH (Honeywell)

- 6.4.6 Diehl Metering GmbH

- 6.4.7 Apator SA

- 6.4.8 Zenner International GmbH and Co. KG

- 6.4.9 Arad Ltd.

- 6.4.10 Aclara Technologies LLC

- 6.4.11 Aidon Oy

- 6.4.12 ADD GRUP SRL

- 6.4.13 Networked Energy Services Corp.

- 6.4.14 Iskraemeco d.d.

- 6.4.15 Elgama-Elektronika UAB

- 6.4.16 Holley Technology Ltd.

- 6.4.17 ZIV Automation S.L.

- 6.4.18 Wasion Group Holdings Ltd.

- 6.4.19 Kaifa Technology (Europe)

- 6.4.20 Secure Meters Europe Ltd.

- 6.4.21 Sagemcom Energy and Telecom SAS

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

物联网市场追踪:衡量

物联网市场追踪:衡量 2026年全球智慧电錶市场报告

2026年全球智慧电錶市场报告 多功能智慧电錶市场(按最终用户、应用、通讯技术、相型、部署模式和安装类型划分),全球预测,2026-2032年

多功能智慧电錶市场(按最终用户、应用、通讯技术、相型、部署模式和安装类型划分),全球预测,2026-2032年 美国智慧电錶:市场份额分析、产业趋势与统计、成长预测(2026-2031 年)

美国智慧电錶:市场份额分析、产业趋势与统计、成长预测(2026-2031 年) 全球电网现代化投资市场:预测(至2034年)-按输电基础设施、组件、资金来源、电网类型、技术、应用、最终用户和地区进行分析

全球电网现代化投资市场:预测(至2034年)-按输电基础设施、组件、资金来源、电网类型、技术、应用、最终用户和地区进行分析 智慧电錶市场规模、份额、趋势及预测(依产品、技术、应用及地区划分),2026-2034年

智慧电錶市场规模、份额、趋势及预测(依产品、技术、应用及地区划分),2026-2034年 智慧电錶市场-全球产业规模、份额、趋势、机会及预测(依技术、类型、应用、地区及竞争格局划分,2021-2031年)

智慧电錶市场-全球产业规模、份额、趋势、机会及预测(依技术、类型、应用、地区及竞争格局划分,2021-2031年) 智慧电錶市场规模、份额和趋势分析报告:按组件、类型、技术、最终用途、地区和细分市场预测(2026-2033 年)日本智慧电錶市场报告:按产品、技术、应用和地区划分(2026-2034年)

智慧电錶市场规模、份额和趋势分析报告:按组件、类型、技术、最终用途、地区和细分市场预测(2026-2033 年)日本智慧电錶市场报告:按产品、技术、应用和地区划分(2026-2034年) 智慧燃气计量系统市场规模、份额及成长分析(按技术、类型、组件和地区划分)-2026-2033年产业预测

智慧燃气计量系统市场规模、份额及成长分析(按技术、类型、组件和地区划分)-2026-2033年产业预测