|

市场调查报告书

商品编码

1940785

英国IT服务:市场占有率分析、产业趋势与统计、成长预测(2026-2031年)United Kingdom IT Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

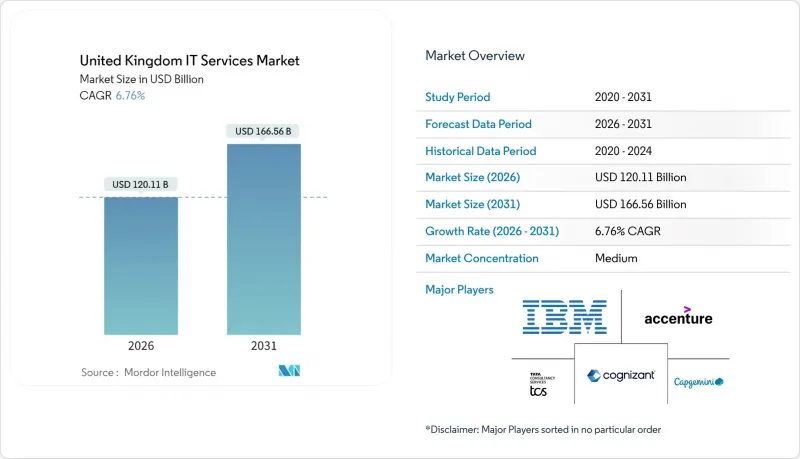

英国IT 服务市场在 2025 年的价值为 1,125 亿美元,预计到 2031 年将达到 1,665.6 亿美元,高于 2026 年的 1,201.1 亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 6.76%。

这一成长轨迹展现了英国IT服务市场的韧性,其驱动力来自公共和私营部门加速的数位转型、公共部门对人工智慧基础设施的持续投资以及网路安全领域日益严格的合规要求。公共部门云端框架和生成式人工智慧的合约订单屡创新高,区域科技中心的蓬勃发展也持续刺激着市场需求,但薪资上涨和宏观经济的谨慎态度仍然是限制因素。全球顾问公司正致力于加强在人工智慧领域的布局,以确保获得大规模多年合约。同时,中型服务供应商则专注于託管安全和工业4.0整合等领域。儘管由于本地人才供应紧张,近岸交付模式的采用率正在上升,但金融和政府等高度监管的行业仍然倾向于接近性考虑本地部署环境。

英国IT服务市场趋势与洞察

人工智慧主导的数位转型浪潮

英国目前是全球第三大人工智慧经济体,目标是透过人工智慧的应用实现每年1.5%的生产力成长。儘管热情高涨,但仅有16%的製造商表示拥有足够的人工智慧知识,这为服务供应商创造了咨询机会。 40亿美元的公共投资和140亿美元的私人承诺为以人工智慧为中心的各项措施提供了持续的资金支持。光是Accenture一家就已在2025财年第二季获得了14亿美元的人工智慧相关订单,这显示企业需求强劲。政府指定的AI成长区(位于剪切机卡勒姆)需要大规模的系统整合和云端容量。这些因素共同推动了英国IT服务市场的持续成长。

云端优先政府采购政策

由G-Cloud 14概述的「云端优先」方法正在改变公共部门的采购结构。 G-Cloud 14是一个包含4000家供应商提供的46000项服务的目录。自2012年以来,该框架已节省了23亿美元,这充分体现了其经济效益,并鼓励中小企业参与其中。即将启动的160亿美元「技术服务4」竞赛是供应商迄今为止最大的单一机会。在数位科技产业计画的指导下,云端技术的应用正在扩展到策略伙伴关係,模糊了采购和创新之间的界线。这种影响对私部门也显而易见,受监管产业纷纷效法公共部门的标准,推动英国IT服务市场平台服务持续保持两位数成长。

技术人才库薪资上涨

到2024年,科技业的薪资将上涨7%至10%,76%的雇主表示面临严重的技能短缺。国民保险费率将于2025年4月上调(从13.8%上升至15%),这将增加雇主的成本。英国脱欧后,30万欧盟专业人士的离境将造成60万个职缺,每年对英国经济造成630亿美元的损失。企业正透过近岸外包策略和提高自动化程度来填补这一缺口,但不断上涨的人事费用正在挤压利润空间,并限制英国IT服务市场的成长。

细分市场分析

到2025年,云端和平台服务将占英国IT服务市场份额的28.15%,凭藉G-Cloud 14产品目录的扩展以及传统资产持续向公有公共云端迁移,主导地位。预计在160亿美元的「技术服务4框架」(Technology Services 4 framework)的推动下,英国IT服务市场在该领域的规模将稳定成长。同时,受《网路安全与韧性法案》(Cybersecurity and Resilience Bill)强制合规要求的影响,资安管理服务预计到2031年将实现9.38%的复合年增长率。企业人工智慧专案的推进使IT咨询业务保持强劲成长,而IT外包和业务流程外包(BPO)则在自动化浪潮中实现了均衡成长。

云端迁移与安全增强的交叉整合正在帮助服务提供者提升收入。随着机构替换本地系统,託管安全合约被打包到平台协议中,从而扩大了市场份额。价值14亿美元的英国国家医疗服务体系(NHS)竞标表明,产业专用的框架正在推动生态系统供应商的发展。因此,能够将超大规模技术与零信任架构结合的供应商将在英国IT服务市场中获得竞争优势。

截至2025年,大型企业将占据英国IT服务市场规模的64.25%,并在多重云端部署、生成式人工智慧试点专案和监管现代化方面投入大量资金。随着其市场主导地位和转型蓝图的日趋成熟,其成长速度正在放缓。同时,在中小企业数位转型工作小组的十步行行动计画的推动下,预计到2031年,中小企业市场将以8.98%的复合年增长率成长。儘管中小企业在英国IT服务市场的份额仍然不大,但它们正在建立一个前景广阔的市场基础,预计人工智慧驱动的生产力提升将创造781亿美元的经济价值。

服务模式需要适应中小企业偏好的短销售週期和基于结果的定价模式。区域性人工智慧创新中心、税额扣抵和云端市场降低了准入门槛,使服务供应商能够开发可复製的服务包。因此,英国IT服务市场正在见证面向伦敦以外小规模企业的订阅式解决方案的兴起。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 人工智慧主导的数位转型浪潮

- 云端优先政府采购政策

- 严峻的网路威胁环境

- 英国製造业的OT-IT融合

- 绿色IT指令(永续性目标)进展

- 英国脱欧导致监管复杂化

- 市场限制

- 技术人才库薪资上涨

- 短期宏观经济放缓

- 与离岸服务相关的数据主权问题

- 伦敦以外中小企业采用情况分散

- 产业价值链分析

- 宏观经济因素的影响

- 关键法规结构评估

- 技术展望

- 波特五力分析

- 竞争对手之间的竞争

- 新进入者的威胁

- 供应商的议价能力

- 买方的议价能力

- 替代品的威胁

第五章 市场规模与成长预测

- 按服务类型

- IT咨询与实施

- IT外包(ITO)

- 业务流程外包(BPO)

- 资安管理服务

- 云端和平台服务

- 按最终用户公司规模划分

- 中小企业

- 大公司

- 按部署模式

- 陆上交付

- 近岸交付

- 离岸交付

- 按最终用户行业划分

- BFSI

- 製造业

- 政府/公共部门

- 医疗保健和生命科学

- 零售和消费品

- 通讯与媒体

- 物流/运输

- 能源与公共产业

- 其他终端用户产业

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Accenture plc

- IBM UK Ltd.

- Capgemini SE

- Tata Consultancy Services(TCS)UK

- Infosys Ltd. UK

- Cognizant Technology Solutions UK

- HCL Technologies UK

- Wipro Ltd. UK

- Fujitsu Services Ltd.

- DXC Technology UK

- CGI IT UK Ltd.

- Sopra Steria Ltd.

- Computacenter plc

- Softcat plc

- Kainos Group plc

- BJSS Ltd.

- Endava plc

- Version 1 Software UK Ltd.

- FDM Group plc

- PA Consulting Group

- Civica Ltd.

- NTT DATA UK Ltd.

- Capita IT Services

- Rackspace Technology UK

- Mastek(UK)Ltd.

第七章 市场机会与未来展望

The UK IT services market was valued at USD 112.5 billion in 2025 and estimated to grow from USD 120.11 billion in 2026 to reach USD 166.56 billion by 2031, at a CAGR of 6.76% during the forecast period (2026-2031).

This trajectory underscores the resilience of the UK IT services market, powered by accelerating digital transformation in both public and private sectors, sustained public investment in AI infrastructure, and expanding compliance mandates in cybersecurity. Public-sector cloud frameworks, record generative-AI contract bookings, and growing regional tech hubs continue to stimulate demand, while wage inflation and macro-economic caution remain moderating influences. Global consulting firms are reinforcing their AI credentials to secure large multi-year deals, whereas mid-tier providers are targeting specialized niches such as managed security and Industry 4.0 integration. Nearshore delivery adoption is rising in response to tight local talent supply, yet the UK IT services market still favors on-premises proximity for high-regulation verticals such as finance and government.

United Kingdom IT Services Market Trends and Insights

AI-led Digital Transformation Wave

The United Kingdom now ranks as the world's third-largest AI economy and is targeting annual productivity gains of 1.5% through AI deployment. Despite enthusiasm, only 16% of manufacturers report adequate AI knowledge, opening consultative opportunities for service providers. Public investment of USD 4 billion and USD 14 billion in private commitments form a durable pipeline for AI-centric engagements. Accenture alone secured USD 1.4 billion in generative-AI bookings during Q2 FY25, signaling robust enterprise appetite. Government-designated AI Growth Zones-beginning with Culham, Oxfordshire-will require extensive systems integration and cloud capacity. Together, these factors generate a sustained uplift in the UK IT services market.

Cloud-first Government Procurement Policies

The cloud-first mandate, highlighted by G-Cloud 14's catalog of 46,000 services from 4,000 suppliers, is reshaping public-sector procurement. Framework savings of USD 2.3 billion since 2012 validate economic benefits and stimulate SME participation. The forthcoming USD 16 billion Technology Services 4 competition represents the largest single opportunity for vendors. Cloud uptake extends into strategic partnerships under the Digital and Technologies Sector Plan, blurring lines between procurement and innovation. Private-sector spillovers are visible as regulated industries replicate public-sector standards, reinforcing double-digit growth in platform services across the UK IT services market.

High Wage Inflation in Tech Talent Pool

Tech salaries escalated 7-10% in 2024, with 76% of employers citing acute skill shortages. The April 2025 National Insurance hike from 13.8% to 15% inflate employer costs. Post-Brexit workforce attrition of 300,000 EU professionals leaves 600,000 vacancies that cost the economy USD 63 billion annually. Firms offset gaps by expanding nearshore and automation strategies, yet elevated labor costs compress margins and temper growth in the UK IT services market.

Other drivers and restraints analyzed in the detailed report include:

- Acute Cyber-threat Environment

- Convergence of OT-IT in UK Manufacturing

- Near-term Macroeconomic Slowdown

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud and platform services represented 28.15% of the UK IT services market share in 2025, a leadership position supported by G-Cloud 14's widened catalog and ongoing migration of legacy estates to the public cloud. The UK IT services market size for this segment is projected to compound steadily on the back of the USD 16 billion Technology Services 4 framework. Simultaneously, managed security services are forecast to post a 9.38% CAGR to 2031, reflecting mandatory compliance under the Cyber Security and Resilience Bill. IT consulting remains resilient thanks to enterprise AI programs, while IT outsourcing and BPO experience balanced growth amid automation.

Cross-pollination between cloud migration and security hardening underpins provider revenue expansion. As agencies replace on-premise systems, bundled managed-security contracts accompany platform deals, magnifying wallet share. NHS tenders worth USD 1.4 billion illustrate how sector-specific frameworks pull along ecosystem suppliers. The UK IT services market, therefore, rewards vendors that combine hyperscale know-how with zero-trust architectures.

Large enterprises controlled 64.25% of the UK IT services market size in 2025, leveraging substantial budgets for multi-cloud rollouts, generative-AI pilots, and regulatory modernization. Despite dominance, their growth rate moderates as transformation roadmaps mature. In contrast, the SME cohort is projected to expand at a 8.98% CAGR to 2031, propelled by the SME Digital Adoption Taskforce's 10-step action plan. UK IT services market share among SMEs remains modest, yet the economic value potential-USD 78.1 billion in AI-enabled productivity gains-creates a fertile addressable base.

Service models must adjust to shorter sales cycles and outcome-based pricing preferred by smaller firms. Regional AI innovation hubs, tax credits, and cloud marketplaces lower entry barriers, allowing providers to develop repeatable packages. Accordingly, the UK IT services market is witnessing a rise in subscription-oriented solutions tailored to micro-enterprises outside London.

The UK IT Services Market Report is Segmented by Service Type (IT Consulting and Implementation, IT Outsourcing, Business Process Outsourcing, and More), End-User Enterprise Size (Small and Medium Enterprises, and Large Enterprises), Deployment Model (Onshore Delivery, Nearshore Delivery, and More), and End-User Vertical (BFSI, Government and Public Sector, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Accenture plc

- IBM UK Ltd.

- Capgemini SE

- Tata Consultancy Services (TCS) UK

- Infosys Ltd. UK

- Cognizant Technology Solutions UK

- HCL Technologies UK

- Wipro Ltd. UK

- Fujitsu Services Ltd.

- DXC Technology UK

- CGI IT UK Ltd.

- Sopra Steria Ltd.

- Computacenter plc

- Softcat plc

- Kainos Group plc

- BJSS Ltd.

- Endava plc

- Version 1 Software UK Ltd.

- FDM Group plc

- PA Consulting Group

- Civica Ltd.

- NTT DATA UK Ltd.

- Capita IT Services

- Rackspace Technology UK

- Mastek (UK) Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 AI-led Digital Transformation Wave

- 4.2.2 Cloud-first Government Procurement Policies

- 4.2.3 Acute Cyber-threat Environment

- 4.2.4 Convergence of OT-IT in UK Manufacturing

- 4.2.5 Rise of Green-IT Mandates (Sustainability Targets)

- 4.2.6 Brexit-Driven Regulatory Complexity

- 4.3 Market Restraints

- 4.3.1 High Wage Inflation in Tech Talent Pool

- 4.3.2 Near-term Macroeconomic Slowdown

- 4.3.3 Data-Sovereignty Concerns with Offshore Delivery

- 4.3.4 Fragmented SME Adoption Outside London

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors

- 4.6 Evaluation of Critical Regulatory Framework

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Competitive Rivalry

- 4.8.2 Threat of New Entrants

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Bargaining Power of Buyers

- 4.8.5 Threat of Substitutes

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 IT Consulting and Implementation

- 5.1.2 IT Outsourcing (ITO)

- 5.1.3 Business Process Outsourcing (BPO)

- 5.1.4 Managed Security Services

- 5.1.5 Cloud and Platform Services

- 5.2 By End-User Enterprise Size

- 5.2.1 Small and Medium Enterprises (SMEs)

- 5.2.2 Large Enterprises

- 5.3 By Deployment Model

- 5.3.1 Onshore Delivery

- 5.3.2 Nearshore Delivery

- 5.3.3 Offshore Delivery

- 5.4 By End-user Vertical

- 5.4.1 BFSI

- 5.4.2 Manufacturing

- 5.4.3 Government and Public Sector

- 5.4.4 Healthcare and Life-Sciences

- 5.4.5 Retail and Consumer Goods

- 5.4.6 Telecom and Media

- 5.4.7 Logistics and Transport

- 5.4.8 Energy and Utilities

- 5.4.9 Other End-user Verticals

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Accenture plc

- 6.4.2 IBM UK Ltd.

- 6.4.3 Capgemini SE

- 6.4.4 Tata Consultancy Services (TCS) UK

- 6.4.5 Infosys Ltd. UK

- 6.4.6 Cognizant Technology Solutions UK

- 6.4.7 HCL Technologies UK

- 6.4.8 Wipro Ltd. UK

- 6.4.9 Fujitsu Services Ltd.

- 6.4.10 DXC Technology UK

- 6.4.11 CGI IT UK Ltd.

- 6.4.12 Sopra Steria Ltd.

- 6.4.13 Computacenter plc

- 6.4.14 Softcat plc

- 6.4.15 Kainos Group plc

- 6.4.16 BJSS Ltd.

- 6.4.17 Endava plc

- 6.4.18 Version 1 Software UK Ltd.

- 6.4.19 FDM Group plc

- 6.4.20 PA Consulting Group

- 6.4.21 Civica Ltd.

- 6.4.22 NTT DATA UK Ltd.

- 6.4.23 Capita IT Services

- 6.4.24 Rackspace Technology UK

- 6.4.25 Mastek (UK) Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

大型通讯业者业务与IT服务:全球市场预测(2025-2030)

大型通讯业者业务与IT服务:全球市场预测(2025-2030) 2026年全球网路部署服务市场报告

2026年全球网路部署服务市场报告 IT 服务市场:2026-2032 年全球市场预测(按服务类型、合约模式、最终用户、组织规模和部署方式划分)2026年全球5G网路部署服务市场报告2026年全球IT服务市场报告2026年全球硬体支援服务市场报告

IT 服务市场:2026-2032 年全球市场预测(按服务类型、合约模式、最终用户、组织规模和部署方式划分)2026年全球5G网路部署服务市场报告2026年全球IT服务市场报告2026年全球硬体支援服务市场报告 IT 服务市场规模、份额和趋势分析报告:按方法、类型、应用、技术、部署、企业规模、最终用途、地区和细分市场进行预测(2026-2033 年)

IT 服务市场规模、份额和趋势分析报告:按方法、类型、应用、技术、部署、企业规模、最终用途、地区和细分市场进行预测(2026-2033 年) IT 服务市场分析及预测(至 2035 年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户和解决方案划分Oracle服务市场分析及预测(至 2035 年):依类型、产品类型、服务、技术、元件、应用、部署类型、终端使用者、功能及解决方案划分

IT 服务市场分析及预测(至 2035 年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户和解决方案划分Oracle服务市场分析及预测(至 2035 年):依类型、产品类型、服务、技术、元件、应用、部署类型、终端使用者、功能及解决方案划分 美国IT服务:市场占有率分析、产业趋势与统计、成长预测(2026-2031年)

美国IT服务:市场占有率分析、产业趋势与统计、成长预测(2026-2031年)