|

市场调查报告书

商品编码

1940790

二次包装:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Secondary Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

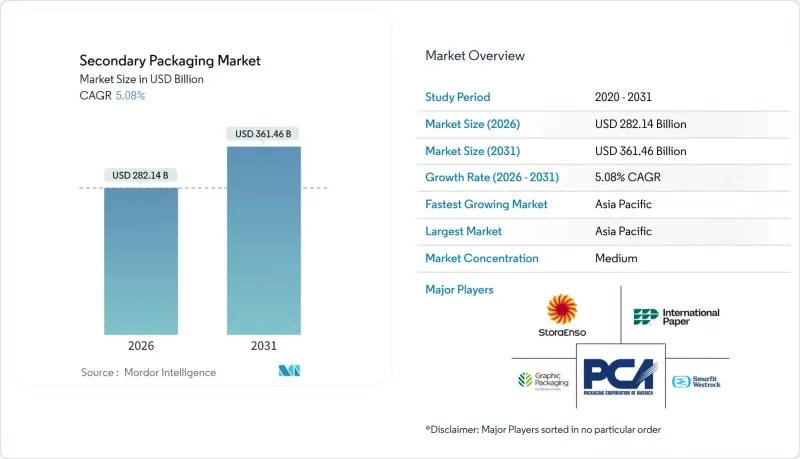

2025年,二级包装市场价值为2,685亿美元,预计到2031年将达到3,614.6亿美元,高于2026年的2,821.4亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 5.08%。

电子商务交易量的成长、零售商的零浪费政策以及品牌商对易于上架包装的需求,共同支撑着瓦楞纸解决方案的稳定需求。目前,瓦楞纸包装已占线上零售小包裹总量的80%。自动化设计的应用日益普及,84%的消费品製造商已在其二级生产线上部署机器人,预计2027年将达到93%。 2022年价值263亿美元的数位印刷市场预计到2032年将超过515亿美元,透过按需定制,有助于控制SKU的激增。亚太地区占据二级包装市场41%的份额,这主要得益于中国包装器材供应商的全球市场份额在五年内从20%增长到35%。全球领先的纸业和纸板企业之间的整合仍在继续,但由于欧洲产能过剩以及2023年消费量下降15.3%,利润率面临压力,限制了其定价能力。

全球二级包装市场趋势与洞察

电子商务的快速成长推动了对瓦楞纸包装的需求。

瓦楞纸箱已占线上配送小包裹的80%,预计到2024年将有27.1亿消费者进行线上购物,因此,纸箱正成为品牌宣传的重要管道。产品适配技术可减少填充材物和材料用量,同时降低承运商的体积重量费用。预计到2034年,全球瓦楞纸包装市场规模将超过8,000亿美元,加工商正在其产品组合中添加隔热内衬和防篡改封条,以应对生鲜产品和安全方面的挑战。数位印刷机可即时个人化,使品牌能够在纸箱内侧印製促销讯息,进而提升客户参与。与自动化相容的模切製程支援机器人组装和包装,可提高大批量加工点的生产效率。纸纤维的永续性正获得零售商的支持,他们承诺在二次包装市场中淘汰难以回收的塑胶。

向自动化包装过渡

劳动力短缺和生产线效率提升目标正推动对机器人拣选、装箱和码垛设备的投资,全球包装机器人市场预计将从2022年的38亿美元增长到2032年的75亿美元。标准化的二次包装尺寸、硬质瓦楞纸板等级和加固的角柱使末端执行器能够高速稳定地抓取纸箱。富邑葡萄酒集团(Treasury Wine Estates)的自动化酒桶仓库升级使产量提高了60%,证明了专为免人工操作而设计的包装的投资回报率。设备即服务(EaaS)合约透过将资本支出分摊到多年,降低了中型加工商的进入门槛。随着预测性维护软体的成熟,因装箱机卡纸和堆垛机错误造成的停机时间减少。运转率目标维持在95%以上。从长远来看,随着机器人成本曲线的下降,自动化概念将在二次包装行业中变得更加普遍。

欧洲箱板纸产能过剩

受消费量下降15.3%的影响,欧洲造纸厂2023年的产量下降了12.8%,但供应过剩的局面依然存在,抑制了箱板纸价格,降低了盈利。不断上涨的电力成本迫使工厂暂时停产,而2024年第三季再生纸价格下跌了约25%,反映出市场对再生材料的需求放缓。生产商正寻求透过合併来精简产能,但反垄断审查延长了合併进程。短期价格疲软抑制了瓦楞纸板厂升级改造的意愿,也减缓了轻量高性能纸板的普及。因此,寻求扩大出口的欧洲加工商正有选择地投资于能够改变瓦楞形状并优化纤维利用率的柔性瓦楞纸板生产设备。

细分市场分析

瓦楞纸箱在2025年仍将维持41.35%的二级包装市场份额,主要得益于其在食品、电商和工业供应链中久经考验的结构性能和成本效益。高强度瓦楞和适用于潮湿仓库环境的涂层技术的持续改进巩固了瓦楞纸箱在该领域的主导地位,而数位印刷与製箱机的结合则缩短了前置作业时间并降低了最低订购量。零售商倾向于选择尺寸合适的运输纸箱,以减少空隙填充,而製箱厂也正在积极响应这一需求,推出新型高速雷射划线生产线,使SKU切换时间缩短至两分钟以内。易于自动化的RSC(平板瓦楞纸)和压锁式设计支援生产线末端的机器人操作,在降低人事费用的同时,还能维持每分钟35箱以上的生产效率。瓦楞纸加工商也正在部署针对特定产品的设备,以减少高达18%的纸板用量,进而助力食品杂货和一般商品分销管道实现零浪费目标。

随着大型零售商和汽车製造商寻求循环物流模式以消除一次性纺织品,可回收运输包装 (RTP) 预计将迎来最高的成长率,2026 年至 2031 年的复合年增长率 (CAGR) 将达到 8.41%。可折迭聚丙烯折迭式显着降低了农产品运输过程中的损坏率,并且可以重复使用 100 次以上,从而在总体拥有成本方面具有竞争优势。丰田物料输送欧洲公司报告称,透过过渡到 RTP 共享模式,固态废弃物减少了 74%,成本节省了 450 万欧元。欧洲塑胶包装废弃物减量 (PPWR) 目标要求到 2030 年所有运输包装都必须可重复使用或可回收,这为相关法规提供了推动。发泡包装、收缩套管和薄膜也在不断发展,其抗穿刺性能不断提高,以满足当日处理的需求。同时,凭藉其精美的图案和基于可再生资源的概念,高端折迭纸盒在化妆品和酒精饮料行业中保持着一定的市场需求。

区域分析

预计到2025年,亚太地区将占全球二级包装市场规模的40.55%,并在2031年之前以11.72%的复合年增长率增长,这主要得益于製造业规模的扩大和线上零售渗透率的提高。中国设备供应商的全球市占率已扩大至35%,使得区域加工商能够以极具吸引力的资本成本采用高速瓦楞纸生产设备。在对保质期长的折迭纸盒和重型运输箱的需求推动下,印度包装食品市场预计将从2020年的320亿美元增长到2025年的550亿美元。在越南,胡志明市週边聚集的900多家包装企业正受惠于国内电子商务订单每年15%至20%的成长。

在北美,小包裹量的强劲成长和消费品製造业的回流正推动新建和现有仓库升级为机器人装箱单元。沃尔玛等零售商已设定循环包装目标,鼓励供应商从发泡聚苯乙烯转向纸质缓衝材料。同时,欧洲面临纸板产能过剩的问题,预计2023年消费量将下降15.3%,但对折迭纸盒和牛皮纸袋的强劲需求正推动产量增加6.5%。

预计到2050年,东南亚将成为世界第四大经济体,税收优惠政策鼓励全球电子和服饰品牌将生产基地设于此。中东和非洲地区虽然尚未成熟,但潜力巨大,基础设施投资和日益增长的年轻消费群体(他们越来越多地选择网购)正在推动该地区的成长。监管差异显着。欧盟的《塑胶包装法规》(PPWR) 要求到2030年实现完全可回收,而美国各州的法规则各不相同,加州一次性塑胶减量25%的目标更使得合规环境变得复杂多变。跨国公司透过采用全球通用的设计方案来规避风险,这些方案可以根据区域标籤进行微调。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 电子商务的快速成长推动了对瓦楞纸包装的需求。

- 过渡到便于自动化的包装形式

- 为品牌拥有者推广可直接上架的解决方案

- 零售商必须实现零浪费

- 亚太新兴市场线上杂货市场的成长

- 实施数位印刷以提高 SKU 灵活性

- 市场限制

- 欧洲纸板产能过剩

- 再生纤维成本波动性加剧

- 塑胶税的不确定性依然存在。

- 机器人维修领域资本投资的障碍

- 价值/供应链分析

- 监管环境

- 技术展望

- 波特五力模型

- 买方的议价能力

- 供应商的议价能力

- 新进入者的威胁

- 替代产品和服务的威胁

- 竞争对手之间的竞争

- 地缘政治局势如何影响市场

第五章 市场规模及成长预测(价值,十亿美元)

- 依产品类型

- 可折迭瓦楞纸箱

- 瓦楞纸箱

- 塑胶箱和手提袋

- 包装膜、薄膜、收缩套管

- 可回收运输包装(RTP)

- 按最终用户行业划分

- 食物

- 饮料

- 医疗和药品

- 家用电子电器

- 个人护理和家居用品

- 工业产品

- 电子商务与物流

- 按地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 东南亚

- 亚太其他地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 其他非洲地区

- 中东

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Smurfit Westrock

- Packaging Corporation of America(PCA)

- Stora Enso Oyj

- International Paper Company

- Graphic Packaging Holding Co.

- WestRock Company

- Sealed Air Corporation

- Reynolds Group Holdings

- Mondi Group

- Amcor plc

- DS Smith plc

- Sonoco Products Company

- Huhtamaki Oyj

- Crown Holdings Inc.

- Ball Corporation

- Tetra Pak

- Pratt Industries

- Nippon Paper Industries

- Rengo Co. Ltd.

第七章 市场机会与未来展望

The secondary packaging market was valued at USD 268.50 billion in 2025 and estimated to grow from USD 282.14 billion in 2026 to reach USD 361.46 billion by 2031, at a CAGR of 5.08% during the forecast period (2026-2031).

Rising e-commerce volumes, retailer zero-waste mandates, and brand-owner requests for shelf-ready packs underpin steady demand for corrugated solutions that already supply 80% of online-retail parcels. Automation-ready designs are gaining traction as 84% of consumer packaged-goods producers have deployed robotics on secondary lines, and the share is projected to reach 93% by 2027. Digital printing, valued at USD 26.3 billion in 2022, is on course to exceed USD 51.5 billion by 2032 and is helping converters manage SKU proliferation through on-demand customization. Asia-Pacific commands 41% of the secondary packaging market share, propelled by China's packaging-machinery suppliers whose global share rose from 20% to 35% in five years. Consolidation among global paper and board majors continues, yet European surplus capacity and a 15.3% drop in 2023 consumption create margin pressure that tempers pricing power.

Global Secondary Packaging Market Trends and Insights

E-commerce Boom Fueling Corrugated Demand

Corrugated cases already supply 80% of parcels shipped through online channels, and 2.71 billion consumers purchased goods digitally in 2024, turning the shipping box into a frontline branding asset. Fit-to-product technology is cutting void fill and material usage while lowering dimensional-weight charges for carriers. With the global corrugated segment projected to surpass USD 800 billion by 2034, converters are broadening portfolios to include insulated inserts and tamper-evident seals that address perishability and security concerns. Digital presses enable late-stage personalization so brands can deliver promotional messages inside the shipper, boosting unboxing engagement. Automation-friendly die cuts support robotic erecting and packing, accelerating throughput in high-volume fulfillment nodes. Sustainability credentials of paper fiber resonate with retailers that pledge to eliminate hard-to-recycle plastics from secondary packaging market offerings.

Shift to Automation-Ready Pack Formats

Labour scarcity and production-line efficiency goals spur investment in robotic pick-and-place, case packing, and palletizing equipment, pushing the global packaging-robot market from USD 3.8 billion in 2022 to an anticipated USD 7.5 billion by 2032. Standardized secondary pack footprints, stiffer board grades, and reinforced corner posts enable end-effectors to grasp boxes consistently at high speeds. Treasury Wine Estates' autonomous barrel-hall upgrade lifted throughput by 60%, illustrating the ROI available when packaging is engineered for hands-free handling. Equipment-as-a-Service contracts now spread capital outlays over multiyear terms, easing adoption for mid-sized converters. As predictive-maintenance software matures, downtime tied to case-erector jams or palletizer misfeeds falls, preserving uptime targets above 95%. Over the long term, automation-ready concepts will permeate the secondary packaging industry as robots move down the cost curve.

Surplus Paperboard Capacity in Europe

European mills cut output 12.8% in 2023 after consumption fell 15.3%, yet oversupply persists, keeping linerboard prices subdued and eroding profitability. High electricity costs compel temporary shutdowns, while recovered-paper values dropped nearly 25% in Q3 2024, reflecting muted demand for recycled furnish. Producers pursue mergers to rationalize capacity, but antitrust scrutiny prolongs timelines. Short-term price weakness discourages capital upgrades in corrugating plants, delaying deployment of lightweight high-performance board grades. Consequently, European converters hunting for export growth selectively invest in flexible corrugators that can pivot between flute profiles and optimize fiber usage.

Other drivers and restraints analyzed in the detailed report include:

- Brand-Owner Push for Shelf-Ready Solutions

- Online Grocery Growth in Emerging APAC

- Rising Cost Volatility of Recycled Fibre

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Corrugated boxes retained 41.35% of the secondary packaging market share in 2025 on the back of their proven structural performance and cost-efficiency across food, e-commerce, and industrial supply chains. Steady upgrades to high-stack strength fluting and coatings that tolerate humid warehouses reinforce the segment's leadership, while digital print, in line with corrugators, shortens lead times and lowers minimum-order quantities. Retailers favor right-sized shippers that reduce void fill, and box plants answer with new high-speed laser-scoring lines able to switch SKUs in under two minutes. Automation-compatible RSC and crash-lock designs support end-of-line robotics, trimming manual labor and keeping throughput above 35 cases per minute. Corrugated converters also deploy fit-to-product equipment that cuts board usage by up to 18%, aligning with zero-waste scorecards in grocery and general merchandise channels.

Returnable transit packaging (RTP) clocks the fastest 2026-2031 growth at 8.41% CAGR as large retailers and automotive OEMs seek circular logistics models that eliminate single-use fiber. Polypropylene foldable crates slash damage rates in produce moves and can cycle more than 100 trips, delivering favorable total cost of ownership. Toyota Material Handling Europe reported 74% solid-waste reduction and EUR 4.5 million in savings after migrating to RTP pools. European PPWR targets that all transport packs be reusable or recyclable by 2030 add regulatory tailwinds. Foam wraps, shrink sleeves, and films continue to evolve with higher puncture resistance to cope with same-day delivery handling, while premium folding cartons sustain niche demand in cosmetics and spirits through upscale graphics and renewable sourcing narratives.

The Secondary Packaging Market Report is Segmented by Product Type (Folding Cartons, Corrugated Boxes, Plastic Crates and Totes, Wraps and Films, and More), End-User Industry (Food, Beverage, Healthcare and Pharma, Consumer Electronics, Personal Care and Household Care, and More), and Geography (North America, Europe, South America, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific captured 40.55% of the secondary packaging market size in 2025 and is forecast to post a 11.72% CAGR through 2031 as manufacturing output climbs and online retail penetration deepens. China's equipment suppliers raised their global share to 35%, enabling regional converters to install high-speed corrugators at attractive capital costs. India's packaged-food sector is moving from USD 32 billion in 2020 toward USD 55 billion by 2025, fueling demand for shelf-stable folding cartons and sturdy shipping cases. Vietnam's 900-plus packaging firms, clustered around Ho Chi Minh City, benefit from 15-20% annual growth in domestic e-commerce orders.

North America experiences robust parcel volumes and the reshoring of consumer-goods manufacturing, encouraging upgrades to robotic case-packing cells in both green- and brownfield warehouses. Retailers such as Walmart set circular-packaging targets that nudge suppliers to swap out polystyrene void fill for paper cushioning. In contrast, Europe grapples with over-capacity in paperboard that dragged consumption down 15.3% in 2023, although demand for folding cartons and sack-kraft showed resilience with 6.5% output growth.

Southeast Asia is projected to become the fourth-largest economic bloc by 2050, helped by tax incentives that draw global electronics and apparel brands to localize production. Middle East and Africa remain nascent yet promising, propelled by infrastructure investments and a youthful consumer base buying more online. Regulatory divergence is stark: the EU PPWR mandates full recyclability by 2030, whereas U.S. regulations vary by state and California's 25% single-use plastic reduction targets create a moving compliance landscape. Multinationals hedge risk by adopting globally compliant designs that can be fine-tuned with localized labeling.

- Smurfit Westrock

- Packaging Corporation of America (PCA)

- Stora Enso Oyj

- International Paper Company

- Graphic Packaging Holding Co.

- WestRock Company

- Sealed Air Corporation

- Reynolds Group Holdings

- Mondi Group

- Amcor plc

- DS Smith plc

- Sonoco Products Company

- Huhtamaki Oyj

- Crown Holdings Inc.

- Ball Corporation

- Tetra Pak

- Pratt Industries

- Nippon Paper Industries

- Rengo Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-commerce boom fueling corrugated demand

- 4.2.2 Shift to automation-ready pack formats

- 4.2.3 Brand-owner push for shelf-ready solutions

- 4.2.4 Retailer's zero-waste mandates

- 4.2.5 On-line grocery growth in emerging APAC

- 4.2.6 Adoption of digital printing for SKU agility

- 4.3 Market Restraints

- 4.3.1 Surplus paperboard capacity in Europe

- 4.3.2 Rising cost volatility of recycled fibre

- 4.3.3 Persistent plastics-tax uncertainty

- 4.3.4 Cap-ex hurdle for robotics retrofits

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Geo-Political Scenarios on the Market

5 MARKET SIZE & GROWTH FORECASTS (VALUE, USD BN)

- 5.1 By Product Type

- 5.1.1 Folding Cartons

- 5.1.2 Corrugated Boxes

- 5.1.3 Plastic Crates and Totes

- 5.1.4 Wraps, Films and Shrink Sleeves

- 5.1.5 Returnable Transit Packaging (RTP)

- 5.2 By End-user Industry

- 5.2.1 Food

- 5.2.2 Beverage

- 5.2.3 Healthcare and Pharma

- 5.2.4 Consumer Electronics

- 5.2.5 Personal and Household Care

- 5.2.6 Industrial Goods

- 5.2.7 E-commerce and Logistics

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 South America

- 5.3.2.1 Brazil

- 5.3.2.2 Argentina

- 5.3.2.3 Rest of South America

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 Rest of Europe

- 5.3.4 Asia-Pacific

- 5.3.4.1 China

- 5.3.4.2 Japan

- 5.3.4.3 India

- 5.3.4.4 South Korea

- 5.3.4.5 South-East Asia

- 5.3.4.6 Rest of APAC

- 5.3.5 Middle East and Africa

- 5.3.5.1 Middle East

- 5.3.5.1.1 Saudi Arabia

- 5.3.5.1.2 United Arab Emirates

- 5.3.5.1.3 Turkey

- 5.3.5.1.4 Rest of Middle East

- 5.3.5.2 Africa

- 5.3.5.2.1 South Africa

- 5.3.5.2.2 Nigeria

- 5.3.5.2.3 Rest of Africa

- 5.3.5.1 Middle East

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Smurfit Westrock

- 6.4.2 Packaging Corporation of America (PCA)

- 6.4.3 Stora Enso Oyj

- 6.4.4 International Paper Company

- 6.4.5 Graphic Packaging Holding Co.

- 6.4.6 WestRock Company

- 6.4.7 Sealed Air Corporation

- 6.4.8 Reynolds Group Holdings

- 6.4.9 Mondi Group

- 6.4.10 Amcor plc

- 6.4.11 DS Smith plc

- 6.4.12 Sonoco Products Company

- 6.4.13 Huhtamaki Oyj

- 6.4.14 Crown Holdings Inc.

- 6.4.15 Ball Corporation

- 6.4.16 Tetra Pak

- 6.4.17 Pratt Industries

- 6.4.18 Nippon Paper Industries

- 6.4.19 Rengo Co. Ltd.

7 MARKET OPPORTUNITIES & FUTURE OUTLOOK

- 7.1 White-space & Unmet-need Assessment

- 7.2 Investment Analysis