|

市场调查报告书

商品编码

1940798

东南亚数位户外(DOOH):市场占有率分析、产业趋势与统计、成长预测(2026-2031)South East Asia Digital Out-of-Home (DooH) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

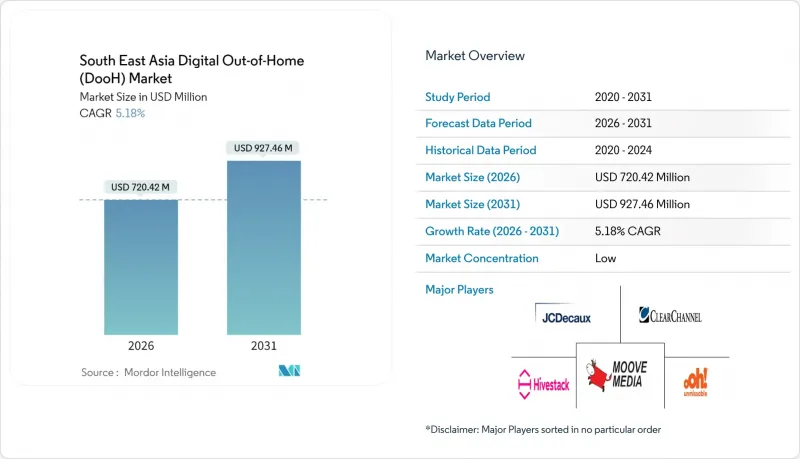

预计东南亚数位户外(DOOH) 市场将从 2025 年的 6.8493 亿美元成长到 2026 年的 7.2042 亿美元,到 2031 年将达到 9.2746 亿美元,2026 年至 2031 年的复合年增长率为 5.18%。

这一增长反映了随着快速都市化、政府智慧城市预算和超级应用广告生态系统在全部区域的融合,广告形式正从静态展示广告稳步转向数据驱动的程序化广告。公共交通走廊沿线通勤客流量的增加,加上购物中心数位化计划和零售媒体网路的推广,正在扩大优质萤幕的覆盖范围,并推动单一萤幕平均收入的成长。品牌方看重这种广告形式的高可见度和与购买路径的相关性,广告代理商也越来越多地将第一方资料迭加到动态创新中,以提高宣传活动的有效性。竞争优势将取决于能否获得黄金地段、LED供应链的效率,以及营运商部署满足即时优化需求的程式化广告管道的速度。

东南亚数位户外(DOOH)市场趋势与洞察

快速的都市化和交通枢纽游客数量的激增

人口持续从农村向大都会圈迁移,导致公共交通客流量和停留时间不断增加,创造了大量高价值的萤幕广告空间。泰国计划在2030年前投资1,800亿泰铢(约51亿美元)用于105个城市的数位化改造,以实现交通枢纽的数位化。印尼的努桑塔拉计画也包括为其新首都建造智慧基础设施。马来西亚槟城岛计划在2027年前投资23亿马币(约5.06亿美元)开发综合导览系统和收益分成广告网路。通勤者平均每天花费42.9分钟搭乘公共运输工具,这为高额CPM(每千次展示成本)提供了支撑。新加坡地铁和吉隆坡铁路枢纽的数位广告看板月租金已超过1.5万美元,充分展现了其巨大的商业价值。

政府主导的智慧城市数位电子看板投资

国家数位化计画将广告支援的萤幕引入交通、医疗和市政设施,并向媒体业者提供长期特许经营合约。泰国数位经济总体规划强制要求在新国家设施中数位电子看板,以促进规模化和技术标准化。印尼320亿美元的「努桑塔拉」计画预算包含一个覆盖全城的物联网网络,重点是开放式和程式化介面。马来西亚数位经济蓝图的目标是到2030年数位产业对GDP的贡献达到25.5%,并鼓励地方政府实施广告支援的基础建设。明确的采购规则缩短了销售週期,统一的技术规格降低了营运商和广告商的整合成本。

高昂的资本投入和持续的维护成本

全动态LED显示器需要大量的初始投资和持续的维护,这给依赖进口管道的小规模企业带来了障碍。在新兴市场,融资成本仍然很高,利率通常超过两位数,投资回收期往往超过五年。此外,外汇波动也会推高以美元计价的组件成本。本地电力供应、冷却和光纤连接等持续性支出会挤压广告价格较低的区域性城市的利润空间。资金负担限制了扩张速度,延缓了现代化改造週期,从而减少了库存累积。

细分市场分析

到2025年,户外广告看板收入将占总收入的34.78%,这印证了品牌对沿着主要公路(例如新加坡的乌节路和马来西亚的联邦大道)大尺寸广告看板的持续青睐。随着各国政府将LED广告看板融入城市景观,东南亚数位户外(DOOH)市场的广告看板规模预计将稳定扩大。然而,预计成长最快的将是3D变形广告牌,其复合年增长率(CAGR)将达到6.12%,因为身临其境型视觉效果能够推动社交媒体的普及,并使高额的CPM(广告曝光率成本)成为合理选择。

由于智慧城市政策将导向功能与广告空间结合,包括公车候车亭和路灯面板在内的街道设施正日益成为市政收入的稳定来源。儘管基于场所的媒体广告目前仍占比最小,但在机场、电影院和医疗机构等人们停留时间更长、受众品质更高的场所,其需求正在增长。像Shining这样的LED供应商正在开发用于公车的防震显示器和支援GPS定位的定向技术,以推动基于路线的商业化。

到2025年,室内环境将占据39.25%的市场份额,到2031年将达到5.68%的最高复合年增长率。购物中心业主正在改造液晶电视墙和电梯萤幕,以将客流量转化为广告收入,同时改善消费者的购物体验。在新加坡樟宜机场,支援VIOOH(户外影片广告)的面板将航班数据与动态创新排播相结合,以投放与情境相关的讯息。

户外萤幕透过路边广告看板和政府基础设施预算资助的交通候车亭等设施,覆盖范围广泛。整合的QR码和NFC标籤将实体萤幕与行动商务连接起来,使品牌能够即时衡量转换率。透过将室内精准投放与户外规模化投放相结合,营运商能够更好地在东南亚数位户外(DOOH)市场实现全通路行销目标。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 快速的都市化和交通枢纽人流量的快速成长

- 政府智慧城市投资数位电子看板

- 程序化数位户外广告购买平台的激增

- 全通路零售和不断成长的消费者品牌广告支出

- 利用3D变形标誌推广优质库存

- 超级应用零售媒体与户外数位媒体整合

- 市场限制

- 高昂的资本投入和持续的维护成本

- 供应分散限制了统一测量。

- 国家/地区特定的亮度和内容限制

- 熟练的LED/IoT工程师短缺

- 宏观经济因素的影响

- 监管环境

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 产业生态系分析

第五章 市场规模与成长预测

- 按格式

- 广告看板

- 街道家具

- 交通广告

- 基于位置的媒体

- 透过使用

- 户外数位户外(DOOH)

- 室内数位户外(DOOH)

- 按最终用户行业划分

- 零售

- 车

- 娱乐与媒体

- 食品/饮料

- 沟通

- BFSI

- 其他终端用户产业

- 透过技术

- 程式化数位户外广告

- 非程式化数位户外广告

- 按地区

- 新加坡

- 马来西亚

- 泰国

- 印尼

- 菲律宾

- 越南

- 东南亚及其他地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- JCDecaux Singapore Pte Ltd

- Clear Channel Singapore Pte Ltd

- oOh!media Limited

- Hivestack Inc.

- Moove Media Pte Ltd

- SPHMBO Pte Ltd(Singapore Press Holdings)

- Vistar Media Inc.

- Talon Outdoor Ltd

- Mediatech Services Pte Ltd

- Daktronics Inc.

- Neosys Documail(S)Pte Ltd

- TAC Media Sdn Bhd

- Moving Walls Pte Ltd

- Pi Interactive Sdn Bhd

- Plan B Media Public Co Ltd

- VGI Public Co Ltd

- Big Tree Outdoor Sdn Bhd

- City Vision Outdoor Advertising PT

- Redberry Media Sdn Bhd

- SEAtronics Inc.

第七章 市场机会与未来展望

The South East Asia Digital Out-of-Home market is expected to grow from USD 684.93 million in 2025 to USD 720.42 million in 2026 and is forecast to reach USD 927.46 million by 2031 at 5.18% CAGR over 2026-2031.

This growth reflects the steady migration from static displays toward data-driven, programmatic inventory as rapid urbanization, government smart-city budgets, and super-app advertising ecosystems converge across the region. Rising commuter volumes in mass-transit corridors, coupled with shopping-mall digitization projects and retail-media network rollouts, are expanding premium screen locations and lifting average yields per panel. Brands value the format's high viewability and path-to-purchase relevance, and agencies increasingly layer first-party data onto dynamic creative to improve campaign lift. Competition hinges on access to grade-A locations, LED supply-chain efficiencies, and the speed at which each operator can deploy programmatic pipes that meet real-time optimization demands.

South East Asia Digital Out-of-Home (DooH) Market Trends and Insights

Rapid Urbanization and Transit-Hub Footfall Surge

Continued migration from rural areas to metropolitan corridors raises daily ridership on mass-transit systems, lifting dwell times and creating concentrated, high-value screen real estate. Thailand's 105-city initiative allocates THB 180 billion (USD 5.1 billion) through 2030 to digitize transport terminals, while Indonesia's Nusantara project earmarks smart infrastructure for its new capital. On Penang Island, Malaysia committed MYR 2.3 billion (USD 506 million) through 2027 for integrated way-finding and revenue-share ad networks. Commuters spend 42.9 minutes per day onboard public transport, a captive interval that supports premium CPMs. Singapore's MRT and Kuala Lumpur's rail hubs already price digital panels above USD 15,000 per month, validating the monetization upside.

Government Smart-City Investments in Digital Signage

National digitization plans embed advertising-ready screens into transport, healthcare, and municipal facilities, providing long-term concession contracts for media owners. Thailand's Digital Economy masterplan mandates digital signage in new state buildings, encouraging scale and technical standardization. Indonesia's USD 32 billion Nusantara budget includes city-wide IoT networks that favor open, programmatic interfaces. Malaysia's Digital Economy Blueprint targets a 25.5% GDP contribution from digital sectors by 2030, pushing local councils to adopt ad-funded infrastructure. Clear procurement rules shorten selling cycles, while uniform technical specs reduce integration costs for operators and advertisers.

High Capex and Ongoing Maintenance Costs

Full-motion LED billboards require substantial upfront spend and continual servicing, a hurdle for small operators that rely on syndicated import channels. Financing terms remain expensive in emerging markets where interest rates exceed double digits, stretching payback periods beyond five years. In addition, fluctuating foreign-exchange rates inflate component costs indexed in USD. On-site power, cooling, and fiber connectivity add recurring overhead, squeezing margins in secondary cities where ad rates are lower. The capital burden limits fleet expansion and slows modernization cycles, curbing inventory growth.

Other drivers and restraints analyzed in the detailed report include:

- Explosion of Programmatic DOOH Buying Platforms

- Omnichannel Retail and Consumer-Brand Ad-Spend Uptick

- Fragmented Supply Limiting Unified Measurement

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Billboards accounted for 34.78% of 2025 revenue, underscoring enduring brand preference for large-format reach along arterial roads such as Singapore's Orchard Road and Malaysia's Federal Highway. The South East Asia Digital Out-of-Home market size for billboard formats is forecast to expand at a steady clip as governments integrate LED structures into urban streetscapes. Yet the fastest acceleration comes from 3D anamorphic sites, projected at a 6.12% CAGR, because immersive visuals drive social-media amplification and justify premium CPMs.

Street furniture, including bus shelters and lamp-post panels, gains from smart-city mandates that bundle way-finding with ad inventory, providing predictable municipal revenue. Place-based media remains the smallest slice but sees rising demand in airports, cinemas, and healthcare facilities where dwell times boost audience quality. LED suppliers like Shining develop anti-vibration bus displays and GPS-enabled targeting to advance route-based monetization.

Indoor environments captured 39.25% share in 2025, and this slice registers the highest 5.68% CAGR through 2031. Shopping-mall owners retrofit LCD videowalls and elevator screens to convert footfall into advertising revenue while enhancing shopper navigation. At Singapore's Changi Airport, VIOOH-enabled panels marry flight data with dynamic creative scheduling, delivering contextually relevant messaging.

Outdoor screens retain broad reach via roadside billboards and transit shelters funded by government infrastructure budgets. Integrated QR codes and NFC tags bridge physical screens to mobile commerce, letting brands measure conversions in real time. The blend of indoor precision and outdoor scale positions operators to serve full-funnel marketing objectives across the South East Asia Digital Out-of-Home market.

The South East Asia Digital Out-Of-Home Market Report is Segmented by Format (Billboards, Street Furniture, Transit, and Place-Based Media), Application (Outdoor DOOH, and Indoor DOOH), End-User Industry (Retail, Automotive, Entertainment and Media, Food and Beverages, Telecom, BFSI, and More), Technology (Programmatic DOOH, and Non-Programmatic DOOH), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- JCDecaux Singapore Pte Ltd

- Clear Channel Singapore Pte Ltd

- oOh!media Limited

- Hivestack Inc.

- Moove Media Pte Ltd

- SPHMBO Pte Ltd (Singapore Press Holdings)

- Vistar Media Inc.

- Talon Outdoor Ltd

- Mediatech Services Pte Ltd

- Daktronics Inc.

- Neosys Documail (S) Pte Ltd

- TAC Media Sdn Bhd

- Moving Walls Pte Ltd

- Pi Interactive Sdn Bhd

- Plan B Media Public Co Ltd

- VGI Public Co Ltd

- Big Tree Outdoor Sdn Bhd

- City Vision Outdoor Advertising PT

- Redberry Media Sdn Bhd

- SEAtronics Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid urbanisation and transit-hub footfall surge

- 4.2.2 Government smart-city investments in digital signage

- 4.2.3 Explosion of programmatic DOOH buying platforms

- 4.2.4 Omnichannel retail and consumer-brand ad spend uptick

- 4.2.5 3D anamorphic billboards driving premium inventory

- 4.2.6 Super-app retail-media integration with DOOH

- 4.3 Market Restraints

- 4.3.1 High capex and ongoing maintenance costs

- 4.3.2 Fragmented supply limiting unified measurement

- 4.3.3 Country-specific brightness and content limits

- 4.3.4 Shortage of skilled LED/IoT technicians

- 4.4 Impact of Macroeconomic Factors

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Industry Ecosystem Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Format

- 5.1.1 Billboards

- 5.1.2 Street Furniture

- 5.1.3 Transit

- 5.1.4 Place-Based Media

- 5.2 By Application

- 5.2.1 Outdoor DOOH

- 5.2.2 Indoor DOOH

- 5.3 By End-User Industry

- 5.3.1 Retail

- 5.3.2 Automotive

- 5.3.3 Entertainment and Media

- 5.3.4 Food and Beverages

- 5.3.5 Telecom

- 5.3.6 BFSI

- 5.3.7 Other End-User Industries

- 5.4 By Technology

- 5.4.1 Programmatic DOOH

- 5.4.2 Non-programmatic DOOH

- 5.5 By Geography

- 5.5.1 Singapore

- 5.5.2 Malaysia

- 5.5.3 Thailand

- 5.5.4 Indonesia

- 5.5.5 Philippines

- 5.5.6 Vietnam

- 5.5.7 Rest of South-East Asia

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level overview, Market level overview, Core segments, Financials as available, Strategic information, Market rank/share, Products and Services, Recent developments)

- 6.4.1 JCDecaux Singapore Pte Ltd

- 6.4.2 Clear Channel Singapore Pte Ltd

- 6.4.3 oOh!media Limited

- 6.4.4 Hivestack Inc.

- 6.4.5 Moove Media Pte Ltd

- 6.4.6 SPHMBO Pte Ltd (Singapore Press Holdings)

- 6.4.7 Vistar Media Inc.

- 6.4.8 Talon Outdoor Ltd

- 6.4.9 Mediatech Services Pte Ltd

- 6.4.10 Daktronics Inc.

- 6.4.11 Neosys Documail (S) Pte Ltd

- 6.4.12 TAC Media Sdn Bhd

- 6.4.13 Moving Walls Pte Ltd

- 6.4.14 Pi Interactive Sdn Bhd

- 6.4.15 Plan B Media Public Co Ltd

- 6.4.16 VGI Public Co Ltd

- 6.4.17 Big Tree Outdoor Sdn Bhd

- 6.4.18 City Vision Outdoor Advertising PT

- 6.4.19 Redberry Media Sdn Bhd

- 6.4.20 SEAtronics Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and unmet-need assessment

2026年全球程序化户外广告平台市场报告

2026年全球程序化户外广告平台市场报告 数位户外广告市场:按形式、终端用户产业、技术、互动性和应用程式划分-全球预测,2026-2032年2026年全球户外数位广告市场报告

数位户外广告市场:按形式、终端用户产业、技术、互动性和应用程式划分-全球预测,2026-2032年2026年全球户外数位广告市场报告 数位户外广告市场报告:按形式、应用程式、最终用户和地区划分(2026-2034 年)

数位户外广告市场报告:按形式、应用程式、最终用户和地区划分(2026-2034 年) 亚太地区数位户外(DOOH):市场占有率分析、产业趋势与统计、成长预测(2026-2031)

亚太地区数位户外(DOOH):市场占有率分析、产业趋势与统计、成长预测(2026-2031) 全球数位户外广告市场规模、份额、趋势和成长分析报告(2026-2034年)全球数位户外广告市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的分析及预测(2026-2034 年)户外媒体广告市场按媒体类型、形式、所有权、应用程式和最终用户产业划分,全球预测(2026-2032年)中东和非洲数位户外广告 (DOOH) - 市场份额分析、行业趋势、统计数据和成长预测 (2026-2031)

全球数位户外广告市场规模、份额、趋势和成长分析报告(2026-2034年)全球数位户外广告市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的分析及预测(2026-2034 年)户外媒体广告市场按媒体类型、形式、所有权、应用程式和最终用户产业划分,全球预测(2026-2032年)中东和非洲数位户外广告 (DOOH) - 市场份额分析、行业趋势、统计数据和成长预测 (2026-2031) 全球户外数位广告 (DOOH) 市场评估:按应用程式、形式、产业和地区划分,机会与预测(2018-2032 年)

全球户外数位广告 (DOOH) 市场评估:按应用程式、形式、产业和地区划分,机会与预测(2018-2032 年)