|

市场调查报告书

商品编码

1940802

美国POS终端:市场占有率分析、产业趋势与统计、成长预测(2026-2031年)United States (US) Point Of Sale (POS) Terminals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

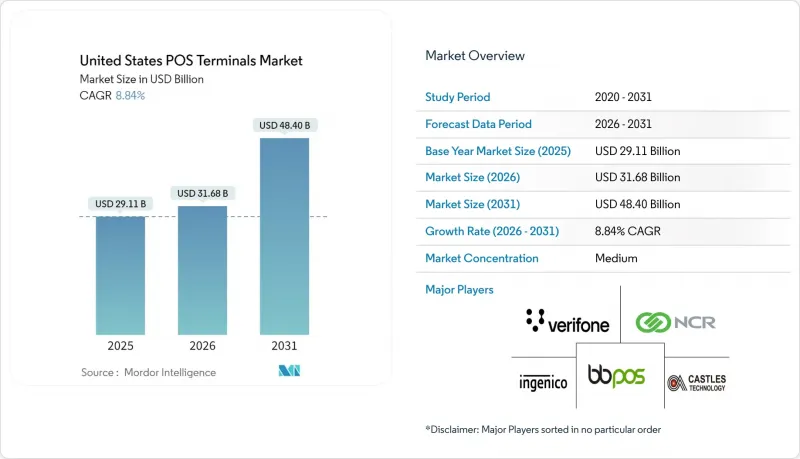

美国POS终端市场预计将从2025年的291.1亿美元成长到2026年的316.8亿美元,到2031年达到484亿美元,2026年至2031年的复合年增长率为8.84%。

这一成长主要得益于EMV和NFC升级的加速、非接触式支付的日益普及以及小规模企业向云端行动POS解决方案的迁移。监管因素,包括PCI DSS 4.0的强制要求,正在推动硬体更新换代,而包括FedNow在内的即时支付基础设施正在重塑人们对支付的预期。随着处理器费用的压缩降低了独立硬体的利润率,供应商整合的压力也越来越大。零售商也更倾向于支援半整合架构和嵌入式金融应用的安卓智慧设备,这些设备能够在不超出PCI监管范围的情况下实现统一的商业分析。

美国销售点终端市场趋势与洞察

EMV 和 NFC 终端的快速更新週期

EMVCo 的数据显示,到 2024 年,美国非接触式交易将成长 87%,其中轻触支付将占所有刷卡交易的 34%。非 EMV 硬体的责任转移增加了诈欺风险,促使商家升级到支援 NFC 的终端。非接触式支付比晶片插入快 53%,从而减少了等待时间和购物车弃购率。竞争压力迫使那些行动较慢的商家在 2027 年合约到期前升级终端。

小型企业正在转向基于云端的行动POS解决方案

根据美国联邦会的一项调查,67%的美国小型企业优先考虑在其支付系统中整合库存管理和分析功能。与传统的租赁方式相比,基于平板电脑的行动POS系统可降低初始硬体成本,并减少23%的每月处理费用。 Stripe和Square提供的嵌入式金融服务进一步降低了采用门槛,帮助快闪店零售商在任何有网路连线的地方接受付款。

针对POS终端机的网路攻击日益复杂化

FS-ISAC 的追踪研究表明,到 2024 年,针对 POS 系统的恶意软体变种将增加 34%,其中包括利用 NFC 通道和 Android 系统的漏洞。这迫使零售商将终端检测和加密通讯纳入累计,使 POS 系统的整体成本增加 15% 至 25%。由于担心系统复杂性增加,小规模企业越来越多地推迟升级,或在风险较高的环境中重新采用现金支付。

细分市场分析

非接触式支付解决方案是美国POS终端市场成长最快的细分领域,复合年增长率高达10.37%。然而,到2025年,接触式读卡机仍将占据美国POS终端市场68.15%的份额。万事达卡的研究显示,非接触式支付已占全球面对面交易的73%,在美国的使用率更是年增87%。联准会的数据显示,由于处理速度更快、更卫生,消费者对非接触式支付的偏好将从2023年的23%上升到2024年的41%。

商家正利用现有基础设施逐步引入NFC技术,同时继续支援晶片密码支付,以应对高额交易和老年人。双介面终端顺应了不断变化的支付习惯,Apple Pay和Google Pay已覆盖67%的35岁以下智慧型手机用户。能够无缝提供接触式和非接触式支付的供应商预计在2031年之前引领美国POS终端市场的成长。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 宏观经济因素的影响

- 市场驱动因素

- EMV 和 NFC 终端的快速更新週期

- 中小企业正在转向基于云端的行动支付解决方案

- 零售商需要整合式商务分析

- PCI-DSS 4.0 合规性推动硬体更新换代

- 销售点即时支付和电子钱包接受度激增

- 嵌入式金融独立软体开发商提供捆绑式终端和软体即服务 (SaaS) 服务。

- 市场限制

- 针对POS终端机的网路攻击正变得越来越复杂。

- 小规模导緻小型零售商推迟资本投资。

- 处理器和网关费用的压缩给硬体利润率带来了压力。

- 遍远地区的网路连线不足限制了无线POS机的效能

- 产业价值链分析

- 监管环境

- 技术展望

- 波特五力分析

- 买方的议价能力

- 供应商的议价能力

- 新进入者的威胁

- 竞争对手之间的竞争

- 替代品的威胁

- 对影响市场的宏观经济因素进行评估

第五章 市场规模与成长预测

- 透过付款方式

- 联繫类型

- 非接触式

- 按POS类型

- 固定式POS系统

- 行动/可携式POS系统

- 按最终用户行业划分

- 零售

- 饭店业

- 卫生保健

- 运输/物流

- 其他终端用户产业

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Verifone Systems Inc.

- Ingenico Inc.

- PAX Technology Limited

- Toshiba Global Commerce Solutions, Inc.

- NCR Corporation

- Diebold Nixdorf Incorporated

- Castles Technology Co., Ltd.

- BBPOS Limited

- Newland Payment Technology Co., Ltd.

- UIC Payworld Inc.

- Equinox Payments, LLC

- Clover Network, LLC

- Square Inc.(Block Inc.)

- Toast, Inc.

- Lightspeed Commerce Inc.

- Posiflex Technology, Inc.

- Epson America, Inc.

- Elo Touch Solutions, Inc.

- HP Inc.(Retail Solutions)

- Zebra Technologies Corporation

第七章 市场机会与未来展望

The United States Point Of Sale Terminals market is expected to grow from USD 29.11 billion in 2025 to USD 31.68 billion in 2026 and is forecast to reach USD 48.4 billion by 2031 at 8.84% CAGR over 2026-2031.

This growth is driven by accelerated EMV and NFC upgrades, rising contactless adoption, and the migration of small merchants to cloud-based mobile POS solutions. Regulatory triggers, including PCI DSS 4.0 mandates, are prompting hardware refresh cycles, while FedNow and other real-time rails are reshaping settlement expectations. Processor fee compression is intensifying vendor consolidation pressures as margins on standalone hardware narrow. Merchants also favor Android smart terminals that support semi-integrated architectures and embedded finance applications, enabling unified commerce analytics without breaching PCI scope.

United States (US) Point Of Sale (POS) Terminals Market Trends and Insights

Rapid EMV and NFC Terminal Upgrade Cycle

EMVCo recorded an 87% rise in U.S. contactless transactions during 2024, with tap-to-pay now accounting for 34% of all card-present activity. Liability shifts on non-EMV hardware elevate fraud risk, pushing merchants toward NFC-ready replacements. Contactless processing is 53% faster than chip insert, cutting wait times and limiting basket abandonment. Competitive pressure now compels even late-adopting small businesses to refresh terminals ahead of 2027 contract renewals.

SME Shift to Cloud-Based mPOS Solutions

Federal Reserve polling shows 67% of U.S. small firms prioritize integrated inventory and analytics within payment systems. Tablet-based mPOS reduces upfront hardware costs and lowers monthly processing fees by 23% versus legacy leases. Embedded finance bundles from Stripe and Square further compress adoption friction, helping pop-up retailers accept payments wherever connectivity exists.

Intensifying Cyber-Attack Sophistication on POS End-Points

FS-ISAC tracked a 34% rise in POS-targeted malware variants during 2024, including exploits on NFC channels and Android vulnerabilities. Merchants now budget for endpoint detection and encrypted communications that raise overall POS system costs 15-25%. Smaller operators, deterred by added complexity, postpone upgrades or revert to cash-only in high-risk settings.

Other drivers and restraints analyzed in the detailed report include:

- Retailer Demand for Unified Commerce Analytics

- PCI-DSS 4.0 Compliance Driving Hardware Refresh

- Inflation-Driven Cap-Ex Deferrals by Small Merchants

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Contactless solutions constitute the fastest-moving slice of the US POS terminals market at a 10.37% CAGR, although contact-based readers still held a 68.15% US POS terminals market share in 2025. Mastercard found tap-to-pay already represents 73% of face-to-face transactions globally, and U.S. usage climbed 87% year over year. Federal Reserve data shows consumer preference for contactless rose to 41% in 2024 from 23% in 2023, sustained by quicker throughput and hygiene benefits.

Merchants continue to support chip-and-PIN for large-ticket sales and older consumer cohorts, leveraging the installed base while gradually layering in NFC. Dual-interface devices accommodate evolving wallet habits as Apple Pay and Google Pay reach 67% penetration among under-35 smartphone owners. Vendors able to furnish seamless contact and contactless acceptance stand to capture the incremental US POS terminals market size expansion through 2031.

The United States Point of Sale Terminals Market Report is Segmented by Mode of Payment Acceptance (Contact-Based and Contactless), POS Type (Fixed Point-Of-Sale Systems, Mobile/Portable Point-Of-Sale Systems), End-User Industry (Retail, Hospitality, Healthcare, Transportation and Logistics, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Verifone Systems Inc.

- Ingenico Inc.

- PAX Technology Limited

- Toshiba Global Commerce Solutions, Inc.

- NCR Corporation

- Diebold Nixdorf Incorporated

- Castles Technology Co., Ltd.

- BBPOS Limited

- Newland Payment Technology Co., Ltd.

- UIC Payworld Inc.

- Equinox Payments, LLC

- Clover Network, LLC

- Square Inc. (Block Inc.)

- Toast, Inc.

- Lightspeed Commerce Inc.

- Posiflex Technology, Inc.

- Epson America, Inc.

- Elo Touch Solutions, Inc.

- HP Inc. (Retail Solutions)

- Zebra Technologies Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Factors

- 4.3 Market Drivers

- 4.3.1 Rapid EMV and NFC Terminal Upgrade Cycle

- 4.3.2 SME Shift to Cloud-Based mPOS Solutions

- 4.3.3 Retailer Demand for Unified Commerce Analytics

- 4.3.4 PCI-DSS 4.0 Compliance Driving Hardware Refresh

- 4.3.5 Surge in Real-Time Payment and Wallet Acceptance at POS

- 4.3.6 Embedded-Finance ISVs Bundling Terminals with SaaS

- 4.4 Market Restraints

- 4.4.1 Intensifying Cyber-attack Sophistication on POS End-points

- 4.4.2 Inflation-Driven Cap-Ex Deferrals by Small Merchants

- 4.4.3 Processor and Gateway Fee Compression Squeezing Hardware Margins

- 4.4.4 Rural Connectivity Gaps Limiting Wireless POS Performance

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Intensity of Competitive Rivalry

- 4.8.5 Threat of Substitutes

- 4.9 Assessment of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Mode of Payment Acceptance

- 5.1.1 Contact-based

- 5.1.2 Contactless

- 5.2 By POS Type

- 5.2.1 Fixed Point-of-Sale Systems

- 5.2.2 Mobile / Portable Point-of-Sale Systems

- 5.3 By End-User Industry

- 5.3.1 Retail

- 5.3.2 Hospitality

- 5.3.3 Healthcare

- 5.3.4 Transportation and Logistics

- 5.3.5 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Verifone Systems Inc.

- 6.4.2 Ingenico Inc.

- 6.4.3 PAX Technology Limited

- 6.4.4 Toshiba Global Commerce Solutions, Inc.

- 6.4.5 NCR Corporation

- 6.4.6 Diebold Nixdorf Incorporated

- 6.4.7 Castles Technology Co., Ltd.

- 6.4.8 BBPOS Limited

- 6.4.9 Newland Payment Technology Co., Ltd.

- 6.4.10 UIC Payworld Inc.

- 6.4.11 Equinox Payments, LLC

- 6.4.12 Clover Network, LLC

- 6.4.13 Square Inc. (Block Inc.)

- 6.4.14 Toast, Inc.

- 6.4.15 Lightspeed Commerce Inc.

- 6.4.16 Posiflex Technology, Inc.

- 6.4.17 Epson America, Inc.

- 6.4.18 Elo Touch Solutions, Inc.

- 6.4.19 HP Inc. (Retail Solutions)

- 6.4.20 Zebra Technologies Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

餐饮POS终端市场:依组件、支付方式及产业划分-2026年至2032年全球市场预测POS设备市场:2026-2032年全球市场预测(以交付方式、连接方式、销售管道和最终用户划分)

餐饮POS终端市场:依组件、支付方式及产业划分-2026年至2032年全球市场预测POS设备市场:2026-2032年全球市场预测(以交付方式、连接方式、销售管道和最终用户划分) 影院POS解决方案市场规模、份额及成长分析:依解决方案组件、关键功能、服务通路、设施规模及地区划分-2026年至2033年产业预测

影院POS解决方案市场规模、份额及成长分析:依解决方案组件、关键功能、服务通路、设施规模及地区划分-2026年至2033年产业预测 2026年全球POS系统需求市场报告2026年全球销售点(POS)市场报告餐厅POS系统市场依部署方式、最终用户、组件、营运和支付方式划分,全球预测(2026-2032年)

2026年全球POS系统需求市场报告2026年全球销售点(POS)市场报告餐厅POS系统市场依部署方式、最终用户、组件、营运和支付方式划分,全球预测(2026-2032年) 销售点 (POS) 市场分析及至 2035 年预测:按类型、产品类型、服务、技术、组件、应用、设备、部署类型、最终用户和功能划分餐饮POS终端市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、部署类型、最终用户、功能及安装类型划分

销售点 (POS) 市场分析及至 2035 年预测:按类型、产品类型、服务、技术、组件、应用、设备、部署类型、最终用户和功能划分餐饮POS终端市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、部署类型、最终用户、功能及安装类型划分 2026-2034年全球餐饮POS终端市场规模、份额、趋势及成长分析报告

2026-2034年全球餐饮POS终端市场规模、份额、趋势及成长分析报告 日本POS终端市场规模、份额、趋势和预测:按组件、终端类型、企业规模、行业和地区划分,2026-2034年

日本POS终端市场规模、份额、趋势和预测:按组件、终端类型、企业规模、行业和地区划分,2026-2034年