|

市场调查报告书

商品编码

1940811

英国区域供热:市场占有率分析、产业趋势与统计、成长预测(2026-2031)United Kingdom District Heating - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

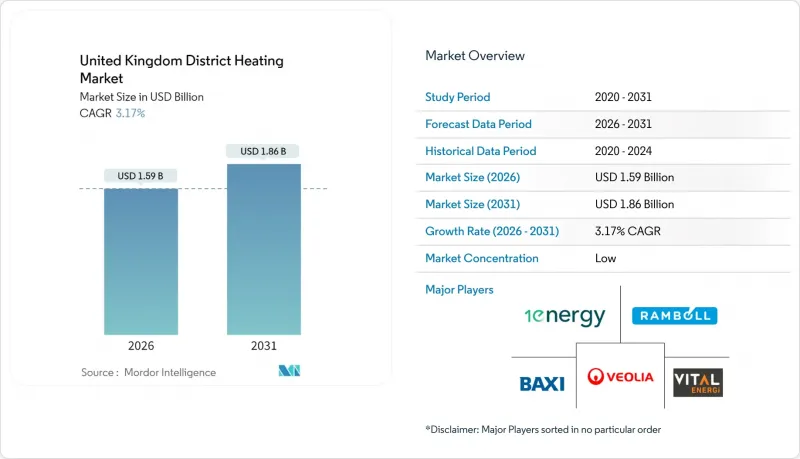

2025年英国区域供热市场价值为15.4亿美元,预计将从2026年的15.9亿美元成长到2031年的18.6亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 3.17%。

这项预测反映了整个系统正从依赖天然气的资产转向低碳热泵、余热回收和大规模储热。强制性供热网路分区确立了具有法律约束力的连接区域,降低了客户获取的风险。同时,绿色供热网路基金降低了利用废弃物发电和再生能源计划的资本支出。政府补贴现在优先考虑能够实现检验碳减排的计划,鼓励营运商部署将河流、矿井水和污水热源与联网地源热泵结合的系统。投资者正在响应这些政策讯号。机构投资者正在加强资产整合,将分散的网路整合到专业管理之下,并加速技术升级,例如建造12小时储热坑。熟练劳动力和金属商品的供应链限制仍然是不利因素,但英国天然气和电力市场管理局(英国)即将推出的消费者保护计画有望增强终端用户的信心,并促进连接率的提高。

英国区域供热市场趋势及展望

2025-2026 年法定供热网路区域指定

供热管网分区赋予地方政府法律权力,强制规定使用者在特定区域内接入供热管网,从而确保商业性可行性所需的供热密度。英国能源安全与净零排放部发布了一份针对16个地区的机会报告,指导伯明罕、利兹和纽卡斯尔等城市製定强制性分区方案,涵盖新建筑和许多维修项目。分区将区域供热从自愿性技术转变为强制性要求,降低了营运商的需求风险,并为长期投资者提供了可观且可预测的收入来源。开发商可以更清楚地了解管网规模和分阶段扩建计划,而现有建筑业主则面临明确的脱碳期限。因此,这项政策将市场优势转移到了拥有快速资本投入和成熟营运能力的管网所有者手中。

绿色供热网络基金和 HNES津贴

自成立以来,绿色热力网络基金已拨款超过3.8亿英镑(4.75亿美元),其中包括为利兹的艾尔河谷热电网络提供的1950万英镑,以及为伦敦大学布鲁姆斯伯里能源网络提供的720万英镑。津贴降低了加权平均资本成本,鼓励开发大规模的废弃物发电热源,并将内部收益率提高至多两个百分点。遴选标准评估那些将废热回收与热泵结合的计划,引导市场设计朝着混合配置方向发展,以实现低于50克二氧化碳/千瓦时的目标。资金筹措的确定性也鼓励了私人贷款机构参与,目前已有几家商业银行在建立优先债务时将绿色热力网路基金的津贴作为风险缓解工具。

初始资本投资增加

材料通膨导致隔热材料价格在2024年至2025年间上涨了2%至11.7%,而铜和钢价格的波动进一步加剧了资产负债表的压力。 Arloop估计,地热网路建置成本为每兆瓦热容量200万至400万英镑,其中钻井成本就占总支出的45%之多。这种高资本投入延长了投资回收期,并限制了小规模开发商的资金筹措管道。 GHNF津贴可以缓解但无法完全消除可行性研究和审批阶段的沉没成本风险。因此,股权投资者要求更高的内部收益率,并推迟了没有锚定负载或长期购热协议的计划的资金筹措完成。

细分市场分析

截至2025年,住宅用户占英国区域供热市场的57.60%,这主要得益于城市住宅和混合用途改造项目的高热密度。社会住宅试点计画也印证了区域供热的提案,其中SHIELD试点计画表明,在满足房东维修义务的同时,低收入租户的租金预计将降低40%。非住宅需求正以每年4.41%的复合年增长率成长,这主要受环境、社会和治理(ESG)要求以及公共部门净零排放目标的推动。大学和医院正在推动兆瓦级扩建,以满足基本负载需求,并得到了政府拨款和长期资本规划的支持。

商业房地产所有者越来越将供热网路视为应对未来建筑排放税的有效手段。租赁协议中强制性的营运碳排放要求,促使企业转向碳係数有保障的低碳供热网路。同时,地方政府透过整合住宅和公共需求,实现了规模经济效益,进一步扩大了目标基本客群。这种多元化的客户组合有助于稳定现金流,并使其能够在私人债务市场进行再融资,从而支持英国区域供热市场的成长。

截至2025年,燃气热电联产将占英国区域供热市场的70.85%,但由于碳定价和生物质永续性法规的加强,其主导地位正在下降。低碳热泵和余热系统正以5.08%的复合年增长率成长,这反映了它们较高的绿色能源网路(GHNF)评分资格和较低的生命週期排放。 MEL Heat Networks公司从米勒山垃圾焚化发电回收余热,并利用大型热泵为其供热,为肖费尔镇供热。 Vattenfall公司估计,这种混合系统可以将基准排放减少高达90%。

地热系统正透过在住宅区内共用垂直钻孔的网路化布局而扩大规模,从而将单位钻井成本降低三分之一。空气源热泵越来越多地被用作夏季的辅助能源,而非唯一能源,从而优化了跨季节的性能。由于颗粒物排放限制,生质能在都市区仍属于小众选择,但农村住宅区仍持续使用当地材料。备用燃气锅炉仍然用于故障恢復,但由于储热技术和需量反应的改进,运作时间正在减少。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 2025-2026财年法定供热网路区域划定

- 绿色供热网络基金和 HNES津贴

- 废热回收义务(能源回收厂和污水处理)

- 降低河水和矿井水热泵的成本

- 向房东揭露费用的义务

- 将热能储存整合到ESO的柔软性中

- 市场限制

- 早期阶段的高资本投入

- 天然气和电力价格差异波动

- 技术纯熟劳工短缺(管道焊工/高压管道工)

- 消费者对「垄断收费」的看法

- 产业价值链分析

- 监管环境

- 技术展望

- 五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 最终用户

- 适用于住宅/一般家庭

- 非住宅

- 透过一次热源

- 瓦斯热电联产

- 低碳热泵和废热

- 生物质/沼气

- 其他备用方案(瓦斯、电力)

- 按行业和客户

- 混合用途重建区

- 公共和住宅住宅

- 大学和医院

- 商业/零售设施

- 利用蓄热设备

- 无集成存储

- 热水箱超过2小时

- 坑/罐存放 12 小时或以上

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Vital Energi Utilities Ltd.

- 1Energy Group Ltd.

- Baxi Heating UK Ltd.

- Ramboll UK Ltd.

- Veolia Environnement SA

- Sweco UK Ltd.

- Vattenfall Heat UK Ltd.

- Equans Services Ltd.

- E.ON UK plc

- SSE Heat Networks Ltd.

- Metropolitan Infrastructure Ltd.

- ThamesWey Energy Ltd.

- Pinnacle Power Ltd.

- Fortum Carlisle Heat Networks Ltd.

- Cory Heat Networks Ltd.

- Kensa Utilities Ltd.

- Ener-Vate Ltd.

- Centrica Business Solutions UK Ltd.

- ENGIE(Energy Solutions UK)Ltd.

- Danpower UK Ltd.

第七章 市场机会与未来展望

The UK district heating market was valued at USD 1.54 billion in 2025 and estimated to grow from USD 1.59 billion in 2026 to reach USD 1.86 billion by 2031, at a CAGR of 3.17% during the forecast period (2026-2031).

This measured trajectory reflects the systemwide pivot from gas-dominant assets toward low-carbon heat pumps, waste-heat recovery, and large-scale thermal storage. Mandatory heat-network zoning is creating legally enforceable connection areas that de-risk customer acquisition, while the Green Heat Network Fund reduces capital outlay for projects integrating energy-from-waste heat or renewable electricity. Government grants now prioritize schemes delivering verifiable carbon cuts, prompting operators to blend river, mine-water, and wastewater heat with networked ground-source heat pumps. Investors are responding to these policy signals: institutional capital has intensified asset roll-ups that pool fragmented networks under professional management, accelerating technology upgrades such as 12-hour storage pits. Supply-chain constraints in skilled labour and metal commodities remain headwinds, yet Ofgem's incoming consumer-protection regime is expected to strengthen end-user confidence and encourage higher connection rates.

United Kingdom District Heating Market Trends and Insights

Statutory heat-network zoning from 2025-26

Heat-network zoning gives local authorities legal power to mandate customer connections within defined boundaries, securing the heat density essential for commercial viability. The Department for Energy Security and Net Zero released opportunity reports for 16 areas, guiding Birmingham, Leeds, and Newcastle to map mandatory zones that cover new builds and many retrofit sites. Zoning transforms district heating from an optional technology into a compliance obligation, lowering demand risk for operators and offering predictable revenue streams attractive to long-term investors. Developers gain clarity on network sizing and phased expansion, while existing building owners face clear deadlines to decarbonize. The policy, therefore, shifts market power toward network owners capable of rapid capital deployment and proven operational competence.

Green Heat Network Fund and HNES grants

The Green Heat Network Fund has disbursed more than GBP 380 million (USD 475 million) since launch, including GBP 19.5 million for Leeds's Aire Valley Heat and Power Network and GBP 7.2 million for the University of London's Bloomsbury Energy Network. Grants reduce the weighted average cost of capital, unlock large energy-from-waste heat sources, and improve internal rates of return by up to 2 percentage points. Award criteria reward projects that combine waste-heat capture with heat pumps, pushing market design toward hybrid configurations that can meet sub-50 gCO2/kWh targets. Funding certainty has also catalysed private lenders; several commercial banks now accept GHNF awards as de-risking instruments when structuring senior debt.

High front-end capex

Material inflation lifted insulation prices by 2-11.7% during 2024-2025, while copper and steel volatility added further strain to balance sheets. Arup estimates geothermal networks cost GBP 2-4 million per MWth, with drilling alone accounting for up to 45% of expenditure. The capital intensity lengthens payback horizons and limits bankability for smaller developers. GHNF grants soften but do not eliminate the risk of sunk costs during feasibility and permitting. Equity investors, therefore, demand higher internal returns, slowing financial close for projects without anchor loads or long-term heat-offtake agreements.

Other drivers and restraints analyzed in the detailed report include:

- Waste-heat capture mandate (EfW and sewage)

- Falling cost of river and mine-water heat pumps

- Gas-power price-spread volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Residential connections delivered 57.60% of UK district heating market share in 2025, benefiting from higher heat density in urban housing estates and mixed-use regeneration schemes. Social housing pilots underline the value proposition: the SHIELD trial indicates potential bill cuts of 40% for low-income tenants while meeting landlord retrofit obligations. Non-domestic demand is gaining momentum at 4.41% CAGR, driven by ESG imperatives and public-sector net-zero targets. Universities and hospitals, armed with capital grants and long asset-life planning horizons, now underwrite multi-megawatt expansions that lock in baseload demand.

Commercial property owners increasingly view heat networks as a hedge against future building-emissions taxes. Mandatory disclosure of operational carbon in leasing contracts pushes landlords toward networks that guarantee low-carbon coefficients. Meanwhile, local authorities bundle residential and municipal loads to unlock economies of scale, further widening the addressable base. The resulting blended customer mix stabilizes cash flows, positioning schemes for refinancing in private debt markets, and supporting the UK district heating market growth trajectory.

Gas-fired CHP retained 70.85% of UK district heating market size in 2025, though its dominance is eroding as carbon pricing and biomass-sustainability rules tighten. Low-carbon heat pumps and waste-heat systems expand at 5.08% CAGR, reflecting their eligibility for higher GHNF scoring and lower lifecycle emissions. The MEL Heat Network captures waste heat from the Millerhill Energy-from-Waste facility and boosts it with large heat pumps to serve Shawfair Town; Vattenfall calculates the hybrid system will avoid up to 90% of baseline emissions.

Ground-source configurations gain scale through networked arrays that share vertical boreholes across housing clusters, cutting per-dwelling drill costs by one-third. Air-source units increasingly act as summer top-up rather than sole supply, optimizing seasonal performance. Biomass remains niche in urban areas due to particulate limits, though rural estates still exploit local feedstock. Backup gas boilers persist for resilience, yet their runtime falls as storage and demand response improve.

The United Kingdom District Heating Market Report is Segmented by End User (Residential/Domestic, and Non-Domestic), Primary Heat Source (Gas-CHP, Low-Carbon HP and Waste-Heat, and More), Sector and Customer (Mixed-Use Regeneration District, Public and Social Housing, and More), Thermal-Storage Usage (No Integrated Storage, >=2 H Hot-Water Tanks, and >=12 H Pit/Tank Storage). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Vital Energi Utilities Ltd.

- 1Energy Group Ltd.

- Baxi Heating UK Ltd.

- Ramboll UK Ltd.

- Veolia Environnement SA

- Sweco UK Ltd.

- Vattenfall Heat UK Ltd.

- Equans Services Ltd.

- E.ON UK plc

- SSE Heat Networks Ltd.

- Metropolitan Infrastructure Ltd.

- ThamesWey Energy Ltd.

- Pinnacle Power Ltd.

- Fortum Carlisle Heat Networks Ltd.

- Cory Heat Networks Ltd.

- Kensa Utilities Ltd.

- Ener-Vate Ltd.

- Centrica Business Solutions UK Ltd.

- ENGIE (Energy Solutions UK) Ltd.

- Danpower UK Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Statutory heat-network zoning from 2025-26

- 4.2.2 Green Heat Network Fund and HNES grants

- 4.2.3 Waste-heat capture mandate (EfW and sewage)

- 4.2.4 Falling cost of river/mine-water heat pumps

- 4.2.5 Mandatory landlord tariff disclosure

- 4.2.6 Aggregation of thermal storage into ESO flexibility

- 4.3 Market Restraints

- 4.3.1 High front-end capex

- 4.3.2 Gas-power price-spread volatility

- 4.3.3 Skilled-labour shortage (pipe-welders/HIU)

- 4.3.4 Consumer "monopoly billing" perception

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter"s Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By End User

- 5.1.1 Residential / Domestic

- 5.1.2 Non-domestic

- 5.2 By Primary Heat Source

- 5.2.1 Gas-CHP

- 5.2.2 Low-carbon HP and Waste-heat

- 5.2.3 Biomass / Biogas

- 5.2.4 Other back-up (gas, electric)

- 5.3 By Sector and Customer

- 5.3.1 Mixed-use regeneration districts

- 5.3.2 Public and Social Housing

- 5.3.3 Universities and Hospitals

- 5.3.4 Commercial / Retail Parks

- 5.4 By Thermal-Storage Usage

- 5.4.1 No integrated storage

- 5.4.2 >=2 h hot-water tanks

- 5.4.3 >=12 h pit / tank storage

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Vital Energi Utilities Ltd.

- 6.4.2 1Energy Group Ltd.

- 6.4.3 Baxi Heating UK Ltd.

- 6.4.4 Ramboll UK Ltd.

- 6.4.5 Veolia Environnement SA

- 6.4.6 Sweco UK Ltd.

- 6.4.7 Vattenfall Heat UK Ltd.

- 6.4.8 Equans Services Ltd.

- 6.4.9 E.ON UK plc

- 6.4.10 SSE Heat Networks Ltd.

- 6.4.11 Metropolitan Infrastructure Ltd.

- 6.4.12 ThamesWey Energy Ltd.

- 6.4.13 Pinnacle Power Ltd.

- 6.4.14 Fortum Carlisle Heat Networks Ltd.

- 6.4.15 Cory Heat Networks Ltd.

- 6.4.16 Kensa Utilities Ltd.

- 6.4.17 Ener-Vate Ltd.

- 6.4.18 Centrica Business Solutions UK Ltd.

- 6.4.19 ENGIE (Energy Solutions UK) Ltd.

- 6.4.20 Danpower UK Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

区域供热市场:网路类型、电站容量、能源来源、供热温度、应用、最终用途-2026-2032年全球市场预测

区域供热市场:网路类型、电站容量、能源来源、供热温度、应用、最终用途-2026-2032年全球市场预测 全球区域供热市场规模、份额、趋势和成长分析报告(2026-2034年)住宅区域供热市场规模、份额、成长及全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测商业区域供热市场规模、份额、成长及全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测

全球区域供热市场规模、份额、趋势和成长分析报告(2026-2034年)住宅区域供热市场规模、份额、成长及全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测商业区域供热市场规模、份额、成长及全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测 2026年全球区域供热市场报告

2026年全球区域供热市场报告 区域供热市场规模、份额和趋势分析报告:按热源、类型、应用、工厂类型、地区和细分市场预测(2026-2033 年)

区域供热市场规模、份额和趋势分析报告:按热源、类型、应用、工厂类型、地区和细分市场预测(2026-2033 年) 区域供热市场机会、成长动力、产业趋势分析及2025-2034年预测

区域供热市场机会、成长动力、产业趋势分析及2025-2034年预测 全球热力网路市场

全球热力网路市场 区域供热的全球市场:厂房类型·热源·用途·各地区 (~2032年)

区域供热的全球市场:厂房类型·热源·用途·各地区 (~2032年) 按工厂类型、热源、应用和地区分類的区域供热市场

按工厂类型、热源、应用和地区分類的区域供热市场