|

市场调查报告书

商品编码

1940849

泰国金属包装:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Thailand Metal Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

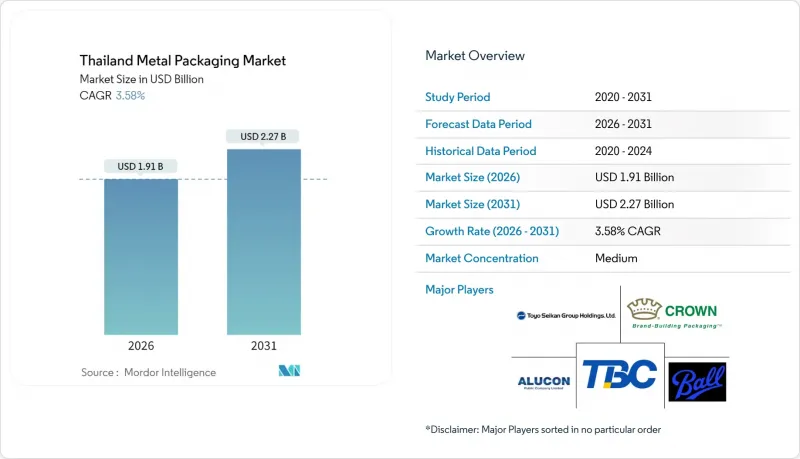

预计泰国金属包装市场规模将从 2025 年的 18.4 亿美元成长到 2026 年的 19.1 亿美元,到 2031 年将达到 22.7 亿美元,2026 年至 2031 年的复合年增长率为 3.58%。

饮料灌装商、食品加工商和出口型宠物食品製造商的强劲需求支撑着这一成长势头,而有利的贸易协定则维持了加工商的高运转率。铝的优势强化了品牌所有者所追求的高端定位,而罐体製造商持续消除瓶颈,确保了在原材料价格上涨的情况下供应安全。政府的永续性指令和废料处理激励措施进一步推动了金属产品规格向循环利用方向发展。泰国通往东协和中东的成熟货运路线缩短了前置作业时间,使当地灌装商能够平衡国内需求和盈利的出口生产,从而保护市场免受消费支出週期性放缓的影响。

泰国金属包装市场趋势与洞察

为即饮饮料增加高附加价值

预计到2023年,泰国饮料填充商的销售量将达到130.2亿公升(相当于253.2亿美元),体现了其高成本策略,该策略主要依赖铝罐的阻隔性能和高端展示效果。注重健康的配方和功能性添加剂正以每年3.5%至4.5%的速度增长,而精美的罐身设计已成为高端机能饮料的视觉象征。大型啤酒製造商和能量饮料品牌频繁推出限量版产品,频繁的规格变更也对反应敏捷的本地加工商有利。预计到2023年,非酒精饮料出口销售额将达到27.8亿美元,罐体生产线能够一夜之间切换国内和区域SKU,从而增强了产量稳定性。皇冠控股预测,2024年全球饮料罐市场将成长4%,其中亚太地区的成长速度将超过其他地区。这些数据支撑了泰国灌装商的持续需求。

泰国作为宠物食品出口基地的发展

预计泰国2023年加工食品出口额将达265亿美元,监管机构已将宠物食品列为下一代关键出口产品。密封金属容器至关重要。大型代加工商正在安装针对鲔鱼罐头优化的蒸馏线,采购政策也明确规定使用能够承受数週海运的拉伸和再拉伸罐。东部经济走廊的税收优惠政策持续吸引新的挤压颗粒饲料生产商,确保了对本地罐头供应商的长期稳定需求。从区域来看,越南、马来西亚和菲律宾的宠物拥有率成长最快,这些市场的进口代理商推荐使用金属容器,因为金属具有良好的抗氧化性,这对营养成分的保存至关重要。随着单位产量的增加,泰国加工商正在增强对捲材原料的采购能力,部分抵消了全球铝价上涨的影响。

轧延钢捲价格波动加剧

基准热轧捲板价格受建筑需求波动和地缘政治能源衝击的影响,导致捲材价格在短期内超过加工商的成本加上合约价格。钢罐製造商正在囤积库存或进行远期采购,占据了原本可用于维修生产效率的营运资金。当价格飙升与金枪鱼罐头和油漆罐的固定价格竞标同时发生时,缺乏国际采购规模的国内钢厂面临的利润压力最为显着。铝价曲线呈现更稳定的上升趋势,促使一些食品包装製造商考虑金属替代品。除非上游製造商透过长期指数合约稳定供应,否则随着加工商对老旧涂装生产线进行精简,泰国的钢罐产能将面临萎缩的风险。

细分市场分析

截至2025年,铝在泰国金属包装市场占据主导地位,市场份额高达74.22%,预计到2031年将继续扩大其主导地位,复合年增长率预计为4.18%。 UACJ公司年产32万吨的工厂供应薄铝捲,Crown、Ball和Thai Beverage Can等公司将这些铝捲轧製成啤酒罐和能量饮料罐。铝的无限可再生满足了循环经济的需求,废料利用率超过90%。生命週期评估有助于减少生命週期排放。

在泰国金属包装市场,铝是出口宠物食品和清真认证水产品线的首选材料,因为这些产品对铝的抗凹陷性、耐海水腐蚀性和可追溯性要求极高。同时,钢材仍然是通用涂料、润滑剂和低成本炼乳生产线的首选材料,因为在这些领域,价格竞争力比永续性更为重要。然而,随着国内生产者延伸责任制(EPR)成本预计从2026年起上涨,铝的整体拥有成本优势将日益凸显,即使在低成本类别中也是如此。铝材的一体化供应链使加工商能够透过长期承购协议对冲原材料风险,从而确保即使全球价格上涨,扩大产能的经济效益仍具有吸引力。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 宏观经济因素的影响

- 市场驱动因素

- 为即饮饮料增加高附加价值

- 泰国宠物食品出口基地的成长

- 扩大清真认证罐装水产品

- 政府提倡铝循环经济

- 电子商务食品销售快速成长

- 酿酒产业正朝着更纤细、更时尚的罐装形式转型

- 市场限制

- 轧延钢捲价格波动加剧

- 从源头寻找生物聚合物袋的替代品

- 欧洲经济共同体(EEC)以外地区回收基础建设的延误

- 气雾剂工厂挥发性有机化合物(VOC)排放的严格规定

- 产业价值链分析

- 监管环境

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 依材料类型

- 铝

- 钢

- 依产品类型

- 能

- 食品罐头

- 饮料罐

- 气雾罐

- 散装容器

- 运输桶和罐

- 瓶盖和封口

- 能

- 终端用户产业

- 饮料

- 食物

- 油漆/化学品

- 工业和汽车用油

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Toyo Seikan Group Holdings, Ltd.

- ALUCON Public Company Limited

- Crown Holdings, Inc.

- Ball Corporation

- Thai Beverage Can Co., Ltd.

- Bangkok Can Manufacturing Co., Ltd.

- Swan Industries(Thailand)Co., Ltd.

- Lohakij Rung Charoen Sub Co., Ltd.

- Next Can Innovation Co., Ltd.

- Asian-Pacific Can Co., Ltd.

- Standard Can Co., Ltd.

- Royal Can Industries Co., Ltd.

- Great Siam Metal Packaging Co., Ltd.

- Siam Toppan Packaging Co., Ltd.

- Perfect Can Manufacturing Co., Ltd.

- Can One(Thailand)Co., Ltd.

- Thai Oil Can Manufacturing Co., Ltd.

- Supreme Metal Container Co., Ltd.

- Thien Long Metal Can(Thailand)Co., Ltd.

- WR Will(Thailand)Ltd.

第七章 市场机会与未来展望

The Thailand metal packaging market is expected to grow from USD 1.84 billion in 2025 to USD 1.91 billion in 2026 and is forecast to reach USD 2.27 billion by 2031 at 3.58% CAGR over 2026-2031.

Robust demand from beverage fillers, food processors, and export-oriented pet-food manufacturers underpins this trajectory, while supportive trade pacts keep converter utilization rates high. Aluminum's dominance reinforces the premium positioning sought by brand owners, and continuous debottlenecking by can-stock mills has protected supply security despite raw-material inflation. Government sustainability mandates and preferential scrap-handling rules further tilt specifications toward circular-ready metal formats. Thailand's established freight corridors into ASEAN and the Middle East shorten lead times, allowing local fillers to balance domestic volumes with lucrative export runs and thereby insulate the market from periodic softness in private consumption.

Thailand Metal Packaging Market Trends and Insights

Premiumisation of Ready-to-Drink Beverages

Thailand's beverage fillers sold 13.02 billion liters worth USD 25.32 billion in 2023, locking in higher value-per-liter price points that rely on aluminum cans for barrier integrity and upscale shelf appea. Health-centric formulas and functional additives are growing 3.5-4.5% annually, and the sleek can profile has become a visual shorthand for premium performance drinks. Major brewers and energy-drink brands schedule frequent limited-edition runs, driving specification turnover that favors agile local converters. Export sales of non-alcoholic drinks delivered USD 2.78 billion in 2023, reinforcing volume certainty for can-body lines that can switch between domestic and regional SKUs overnight. Crown Holdings posted 4% global beverage-can growth in 2024 with Asia Pacific outpacing all other regions, a data point that validates persistent demand from Thai fillers.

Growth of Thailand's Pet-food Export Hub

Thailand shipped USD 26.5 billion in processed foods in 2023, with pet food singled out by regulators as a next-wave export champion requiring hermetically sealed metal formats. Leading co-packers have installed retort lines optimized for tuna-based diets, and their procurement policies specify drawn-and-redrawn cans that withstand multi-week sea freight. Eastern Economic Corridor tax incentives continue to attract new extruded-kibble producers, ensuring sticky long-term offtake for local can-stock suppliers. Regional pet ownership is climbing fastest in Vietnam, Malaysia, and the Philippines, and import agencies in those markets cite metal's oxygen resistance as critical to nutrient preservation. As unit volumes swell, Thai converters gain purchasing leverage on coil feedstock, partially offsetting global aluminum price firming.

Rising Price Volatility of Rolled Steel Coil

Benchmark HRC prices track construction demand swings and geopolitical energy shocks, pushing coil quotes beyond converters' cost-plus contracts on short notice. Steel-can makers carry thicker inventories or buy futures, tying up working capital that could otherwise fund efficiency retrofits. When spikes overlap with fixed-price tenders to tuna or paint fillers, margin compression hits fastest on domestically owned plants that lack global purchasing scale. Aluminum price curves have shown steadier climbs, nudging some food packers into metal substitution. Unless upstream mills stabilize supply with longer-term index deals, Thailand's steel-can capacity risks attrition as converters rationalize older coating lines.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Halal-certified Canned Seafood

- Government Push for Circular-economy Aluminium

- Substitution by Bio-polymer Pouches in Sauces

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Aluminum captured a commanding 74.22% of the Thailand metal packaging market share in 2025, and its 4.18% forecast CAGR ensures the substrate will widen its lead through 2031. UACJ's 320,000-ton mill supplies light-gauge coil that Crown, Ball, and Thai Beverage Can draw into bodies consumed by breweries and energy-drink brands. Aluminum's infinite recyclability resonates with circular-economy levies, and scrap yields north of 90% lower life-cycle emissions in life-cycle assessments.

Thailand metal packaging market buyers give aluminum premium preference on export-grade pet food and halal seafood lines where dent resistance, salty-brine compatibility, and regulatory traceability are paramount. Steel retains relevance on commodity paints, lubricants, and budget condensed-milk lines where price sensitivity overrides sustainability messaging. Still, national EPR fees are expected to rise from 2026, gradually tipping cost-of-ownership math toward aluminum even in value categories. The substrate's consolidated supply chain allows converters to hedge raw-material risk through long-term offtake deals, keeping capacity-addition economics attractive despite global price firming.

The Thailand Metal Packaging Market Report is Segmented by Material Type (Aluminium, Steel), Product Type (Cans, Bulk Containers, Shipping Barrels and Drums, and More), End-User Vertical (Beverage, Food, Paints and Chemicals, Industrial and Automotive Oils). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Toyo Seikan Group Holdings, Ltd.

- ALUCON Public Company Limited

- Crown Holdings, Inc.

- Ball Corporation

- Thai Beverage Can Co., Ltd.

- Bangkok Can Manufacturing Co., Ltd.

- Swan Industries (Thailand) Co., Ltd.

- Lohakij Rung Charoen Sub Co., Ltd.

- Next Can Innovation Co., Ltd.

- Asian-Pacific Can Co., Ltd.

- Standard Can Co., Ltd.

- Royal Can Industries Co., Ltd.

- Great Siam Metal Packaging Co., Ltd.

- Siam Toppan Packaging Co., Ltd.

- Perfect Can Manufacturing Co., Ltd.

- Can One (Thailand) Co., Ltd.

- Thai Oil Can Manufacturing Co., Ltd.

- Supreme Metal Container Co., Ltd.

- Thien Long Metal Can (Thailand) Co., Ltd.

- WR Will (Thailand) Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Factors

- 4.3 Market Drivers

- 4.3.1 Premiumisation of Ready-to-Drink Beverages

- 4.3.2 Growth of Thailand's pet-food export hub

- 4.3.3 Expansion of halal-certified canned seafood

- 4.3.4 Government push for circular-economy aluminium

- 4.3.5 Rapid scale-up of E-commerce grocery formats

- 4.3.6 Brewery shift to sleek and slim can formats

- 4.4 Market Restraints

- 4.4.1 Rising price volatility of rolled steel coil

- 4.4.2 Substitution by bio-polymer pouches in sauces

- 4.4.3 Slow uptake of recycling infrastructure outside EEC

- 4.4.4 Stringent VOC emission norms for aerosol plants

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Aluminium

- 5.1.2 Steel

- 5.2 By Product Type

- 5.2.1 Cans

- 5.2.1.1 Food Cans

- 5.2.1.2 Beverage Cans

- 5.2.1.3 Aerosol Cans

- 5.2.2 Bulk Containers

- 5.2.3 Shipping Barrels and Drums

- 5.2.4 Caps and Closures

- 5.2.1 Cans

- 5.3 By End-user Vertical

- 5.3.1 Beverage

- 5.3.2 Food

- 5.3.3 Paints and Chemicals

- 5.3.4 Industrial and Automotive Oils

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Toyo Seikan Group Holdings, Ltd.

- 6.4.2 ALUCON Public Company Limited

- 6.4.3 Crown Holdings, Inc.

- 6.4.4 Ball Corporation

- 6.4.5 Thai Beverage Can Co., Ltd.

- 6.4.6 Bangkok Can Manufacturing Co., Ltd.

- 6.4.7 Swan Industries (Thailand) Co., Ltd.

- 6.4.8 Lohakij Rung Charoen Sub Co., Ltd.

- 6.4.9 Next Can Innovation Co., Ltd.

- 6.4.10 Asian-Pacific Can Co., Ltd.

- 6.4.11 Standard Can Co., Ltd.

- 6.4.12 Royal Can Industries Co., Ltd.

- 6.4.13 Great Siam Metal Packaging Co., Ltd.

- 6.4.14 Siam Toppan Packaging Co., Ltd.

- 6.4.15 Perfect Can Manufacturing Co., Ltd.

- 6.4.16 Can One (Thailand) Co., Ltd.

- 6.4.17 Thai Oil Can Manufacturing Co., Ltd.

- 6.4.18 Supreme Metal Container Co., Ltd.

- 6.4.19 Thien Long Metal Can (Thailand) Co., Ltd.

- 6.4.20 WR Will (Thailand) Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

金属包装市场:依产品类型、材料类型、涂层类型、产品设计、生产技术和最终用途产业划分-2026-2032年全球预测

金属包装市场:依产品类型、材料类型、涂层类型、产品设计、生产技术和最终用途产业划分-2026-2032年全球预测 2026-2030年全球轻量化金属包装市场

2026-2030年全球轻量化金属包装市场 金属包装:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

金属包装:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 金属包装市场规模、份额及成长分析(依产品类型、材料、应用及地区划分)-2026-2033年产业预测

金属包装市场规模、份额及成长分析(依产品类型、材料、应用及地区划分)-2026-2033年产业预测 全球金属包装市场预测(至2032年):按产品类型、材质、最终用户和地区分類的分析

全球金属包装市场预测(至2032年):按产品类型、材质、最终用户和地区分類的分析 金属包装市场:依材料、产品类型、最终用途产业及地区划分

金属包装市场:依材料、产品类型、最终用途产业及地区划分 2025-2033年金属包装市场报告(依产品类型、材料、应用和地区)乳製品金属包装市场按容器类型、材料类型、封盖类型、应用和分销管道划分 - 全球预测 2025-2030

2025-2033年金属包装市场报告(依产品类型、材料、应用和地区)乳製品金属包装市场按容器类型、材料类型、封盖类型、应用和分销管道划分 - 全球预测 2025-2030 全球金属包装市场:市场规模、份额、趋势分析(按材料、产品类型、最终用途和地区)、细分市场预测(2025-2030 年)印度金属包装:市场占有率分析、行业趋势和成长预测(2025-2030 年)

全球金属包装市场:市场规模、份额、趋势分析(按材料、产品类型、最终用途和地区)、细分市场预测(2025-2030 年)印度金属包装:市场占有率分析、行业趋势和成长预测(2025-2030 年)