|

市场调查报告书

商品编码

1721382

AI硬体设备市场 (~2035年):AI硬体设备·展开·产品类型·设备·消耗功率·流程·各地区的产业趋势与全球预测AI Hardware Market Till 2035; Distribution by Type of AI Hardware, by Type of Deployment, by Type of Product, by Type of Device, by Type of Power Consumption, by Type of Process and Key Geographical Regions : Industry Trends and Global Forecasts |

||||||

预计到 2035 年,全球 AI 硬体市场规模将从目前的 314 亿美元增长至 6,244 亿美元,预测期内的复合年增长率为 31.23%。

受全球各利益相关者不断增长的投资和兴趣的推动,预计 AI 硬体市场在预测期内将保持健康成长。

AI硬体设备的市场机会:各市场区隔

AI各硬体设备

- 编入音处理器

- 编入愿景处理器

- 独立的愿景处理器

- 独立的音处理器

各部署

- 云端

- 内部部署

各产品类型

- 记忆体

- DRAM

- NVM

- SRAM

- 处理器

- CPU

- FPGA

- GPU

- TPU

- 网路

- 储存

各设备

- 汽车

- 相机

- 机器人

- 智慧型手机

- 智慧镜子

- 智慧喇叭

- 穿戴式

按消耗功率

- 不满1W

- 1-3W

- 3-5W

- 5-10W

- 10W多

流程类别

- 推论

- 训练

各终端用户

- 航太·防卫

- 汽车·运输

- BFSI

- CE产品

- 电子商务

- 教育

- 能源·公共事业

- 政府·公共服务

- 导航

- 不动产

- 智慧家庭

- 通讯·IT

- 其他

不同企业规模

- 大企业

- 中小企业

不同商业模式

- B2B

- B2C

- B2B2C

各地区

- 北美

- 美国

- 加拿大

- 墨西哥

- 其他的北美各国

- 欧洲

- 奥地利

- 比利时

- 丹麦

- 法国

- 德国

- 爱尔兰

- 义大利

- 荷兰

- 挪威

- 俄罗斯

- 西班牙

- 瑞典

- 瑞士

- 英国

- 其他欧洲各国

- 亚洲

- 中国

- 印度

- 日本

- 新加坡

- 韩国

- 其他亚洲各国

- 南美

- 巴西

- 智利

- 哥伦比亚

- 委内瑞拉

- 其他的南美各国

- 中东·北非

- 埃及

- 伊朗

- 伊拉克

- 以色列

- 科威特

- 沙乌地阿拉伯

- UAE

- 其他的中东·北非各国

- 全球其他地区

- 澳洲

- 纽西兰

- 其他的国家

AI 硬体市场:成长与趋势

随着 AI 工作负载日益复杂且资料密集,对专用高性能、高能源效率和可扩展性的硬体正在推动人工智慧的创新和发展。这种日益增长的需求促使人们在专用人工智慧硬体开发方面投入大量资金,从而推动了市场的显着成长。

随着全球产业的发展,对高效能运算能力的需求日益增长,以便更有效地处理和管理人工智慧演算法。为此,人工智慧硬体製造商正投入资源开发新产品。边缘人工智慧的普及、跨产业人工智慧模型和产品的使用,以及半导体产业技术创新和趋势的演变,为人工智慧硬体製造商创造了将创新产品推向市场的新机会。

此外,客製化人工智慧晶片组和高能效人工智慧硬体的开发预计将成为许多公司关注的重点。各大公司也努力加强储存加速器的生产,以满足日益增长的需求。为了满足不断发展的储存解决方案的需求,人工智慧也正在推动非挥发性记忆体的发展。

本报告提供全球AI硬体设备的市场调查、彙整市场概要,背景,市场影响因素的分析,市场规模的转变·预测,各种区分·各地区的详细分析,竞争情形,主要企业简介等资讯。

目录

第1章 序文

第2章 调查手法

第3章 经济以及其他的计划特有的考虑事项

第4章 宏观经济指标

第5章 摘要整理

第6章 简介

第7章 竞争情形

第8章 AI硬体设备市场上Start-Ups生态系统

第9章 企业简介

- 章概要

- Advanced Micro Devices

- Amazon Web Services

- Allied Vision Technologies

- Alibaba

- Baidu

- Cadence Design Systems

- Cerebras Design Systems

- Cisco

- CEVA

- Fujitsu

- Graphcore

- Huawei

- IBM

- Intel

- Micron

- Microsoft

- Mythic

- NXP

- NVIDIA

- Oracle

- Qualcomm Technologies

第10章 价值链分析

第11章 SWOT分析

第12章 全球AI硬体设备市场

第13章 AI各硬体设备的市场机会

第14章 各部署的市场机会

第15章 各产品的市场机会

第16章 各设备的市场机会

第17章 各电力消耗的市场机会

第18章 各流程的市场机会

第19章 各终端用户的市场机会

第20章 北美AI硬体设备的市场机会

第21章 欧洲的AI硬体设备的市场机会

第22章 亚洲的AI硬体设备的市场机会

第23章 中东·北非的AI硬体设备的市场机会

第24章 南美的AI硬体设备的市场机会

第25章 全球其他地区的AI硬体设备的市场机会

第26章 表格形式资料

第27章 企业·团体一览

第28章 客制化的机会

第29章 ROOTS订阅服务

第30章 着者详细内容

GLOBAL AI HARDWARE MARKET: OVERVIEW

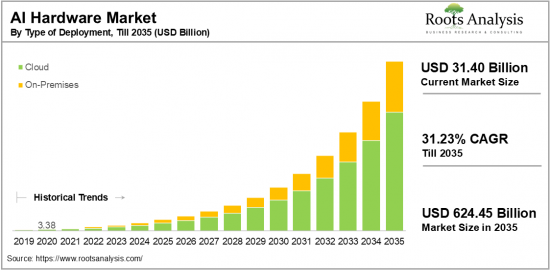

As per Roots Analysis, the global AI hardware market size is estimated to grow from USD 31.40 billion in the current year to USD 624.4 billion by 2035, at a CAGR of 31.23% during the forecast period, till 2035.

Driven by increasing investments and interest from various stakeholders worldwide, the AI hardware market is anticipated to grow at a healthy pace during the forecast period.

The opportunity for AI hardware market has been distributed across the following segments:

Type of AI Hardware

- Embedded Sound Processor

- Embedded Vision Processor

- Stand-alone Vision Processor

- Stand-alone Sound Processor

Type of Deployment

- Cloud

- On-premises

Type of Product

- Memory

- DRAM

- NVM

- SRAM

- Processors

- CPU

- FPGA

- GPU

- TPU

- Networking

- Storage

Type of Device

- Automotive

- Cameras

- Robots

- Smartphones

- Smart Mirror

- Smart Speaker

- Wearable

Type of Power Consumption

- Less than 1W

- 1-3W

- 3-5W

- 5-10W

- More than 10W

Type of Process

- Inference

- Training

Type of End-Users

- Aerospace & Defense

- Automotive & Transportation

- BFSI

- Consumer Electronics

- E-Commerce

- Education

- Energy & Utilities

- Government & Public Services

- Navigation

- Real Estate

- Smart Home

- Telecommunication & IT

- Others

Company Size

- Large Enterprises

- Small and Medium Enterprises

Type of Business Model

- B2B

- B2C

- B2B2C

Geographical Regions

- North America

- US

- Canada

- Mexico

- Other North American countries

- Europe

- Austria

- Belgium

- Denmark

- France

- Germany

- Ireland

- Italy

- Netherlands

- Norway

- Russia

- Spain

- Sweden

- Switzerland

- UK

- Other European countries

- Asia

- China

- India

- Japan

- Singapore

- South Korea

- Other Asian countries

- Latin America

- Brazil

- Chile

- Colombia

- Venezuela

- Other Latin American countries

- Middle East and North Africa

- Egypt

- Iran

- Iraq

- Israel

- Kuwait

- Saudi Arabia

- UAE

- Other MENA countries

- Rest of the World

- Australia

- New Zealand

- Other countries

AI HARDWARE MARKET: GROWTH AND TRENDS

AI hardware refers to equipment specifically engineered and developed for use in artificial intelligence technologies. It encompasses a range of devices and systems optimized to enhance the performance of AI algorithms, deep learning models, and other computational tasks integral to AI applications. As AI workloads become increasingly intricate and data-heavy, the demand for specialized hardware solutions that can provide high performance, energy efficiency, and scalability to foster AI innovation and development has significantly increased. This surge in need has resulted in substantial investments aimed at creating dedicated AI hardware, consequently leading to tremendous market growth.

In the context of global industrial advancement, there is a considerable demand for enhanced processing and computational capabilities to more effectively manage AI algorithms, which in turn encourages manufacturers of AI hardware to channel resources into the development of new products. The growing prevalence of edge AI, as well as AI models and products across various sectors, alongside trends and technological advancements in the semiconductor industry, is opening up new avenues for AI hardware manufacturers to launch innovative offerings. Additionally, the creation of custom AI chipsets and energy-efficient AI hardware is projected to be the primary focus for many companies in the AI hardware space. Moreover, leading market players are also working to boost production of storage accelerators in response to rising demand. To meet the evolving requirements for storage solutions, artificial intelligence is contributing to the development of non-volatile memory.

AI HARDWARE MARKET: KEY SEGMENTS

Market Share by Type of AI Hardware

Based on the type of AI hardware, the global AI hardware market is segmented into embedded sound processors, embedded vision processors, stand-alone vision processors, and stand-alone sound processors. According to our estimates, currently, stand-alone vision processors segment captures the majority share of the market. This can be attributed to the rising adoption of edge AI, increased demand for computer vision applications, and advancements in technology. However, embedded sound processors segment is anticipated to grow at a higher CAGR during the forecast period.

Market Share by Type of Deployment

Based on the type of deployment, the AI hardware market is segmented into cloud, and on-premises. According to our estimates, currently, cloud segment captures the majority share of the market. This can be attributed to the accessibility, flexibility, scalability, and cost-effectiveness that cloud-based AI solutions provide. Additionally, the growing emphasis on accessibility and efficiency by numerous businesses is driving the expansion of this segment. Cloud-based deployment enables organizations of all sizes to utilize advanced AI tools and technologies without the requirement of significant initial investments in hardware and infrastructure.

Market Share by Type of Product

Based on the type of product, the AI hardware market is segmented into memory (DRAM, NVM, SRAM), processors (CPU, FPGA, GPU, TPU), networking and storage. According to our estimates, currently, processors segment captures the majority share of the market. This can be attributed to their high computing speed, which is particularly beneficial for applications in machine learning, including deep learning and machine learning itself. They are also commonly utilized in supervised reinforcement learning. Further, a significant factor driving growth in the processor market is the rising global demand for machine learning devices. This has led major market players to invest in order to deliver innovative and high-speed computing processors.

Market Share by Type of Device

Based on the type of device, the AI hardware market is segmented into automotive, cameras, robots, smartphones, smart mirror, smart speaker and wearable technologies. According to our estimates, currently, automotive segment captures the majority share of the market. This can be attributed to the rise of advanced driver-assistance systems that heavily depend on AI hardware for features related to safety and efficiency, such as collision avoidance and cruise control. However, smart speaker segment is anticipated to grow at a higher CAGR during the forecast period.

Market Share by Type of Power Consumption

Based on the type of application, the AI hardware market is segmented into less than 1W, 1-3W, 3-5W, 5-10W, and more than 10W. According to our estimates, currently, 1-3W power consumption segment captures the majority share of the market. This can be attributed to the prevalent use of AI hardware in consumer electronics, where power consumption in the 1-3W range is common. Additionally, devices that operate within this range can provide adequate performance while also being energy-efficient, making them ideal for power-saving applications. However, less than 1W segment is anticipated to grow at a higher CAGR during the forecast period.

Market Share by Type of Process

Based on the type of process, the AI hardware market is segmented into inference and training. According to our estimates, currently, inference segment captures the majority share of the market. This can be attributed to its essential function in real-time applications that demand quick decision-making, such as autonomous vehicles and smart cameras. The broad adoption of this segment across various industries is another factor contributing to its growth. However, training segment is anticipated to grow at a higher CAGR during the forecast period.

Market Share by Type of End Users

Based on the type of end-users, the AI hardware market is segmented into aerospace & defense, automotive & transportation, BFSI, consumer electronics, e-commerce, education, energy & utilities, government & public services, navigation, real estate, smart home, telecommunication & IT and others. According to our estimates, currently, telecommunication & IT segment captures the majority share of the market. This can be attributed to the application of AI in making efficient decisions within the telecom sector, where significant volumes of big data are processed. The implementation of AI in this field is particularly beneficial for addressing the intricate challenges faced by the telecommunications industry.

Market Share by Type of Enterprise

Based on the type of enterprise, the AI hardware market is segmented into large and small and medium enterprise. According to our estimates, currently, large enterprise segment captures the majority share of the market. However, small and medium enterprise segment is anticipated to grow at a higher CAGR during the forecast period. This growth can be attributed to their agility, innovative capabilities, targeted focus on niche markets, and their ability to respond to shifting customer preferences and changes in market conditions.

Market Share by Geographical Regions

Based on the geographical regions, the AI hardware market is segmented into North America, Europe, Asia, Latin America, Middle East and North Africa, and Rest of the World. According to our estimates, currently, North America captures the majority share of the market. This can be attributed to the growing number of startups dedicated to creating AI hardware, which in turn creates new opportunities for AI hardware firms in this area. However, market share in Asia is anticipated to grow at a higher CAGR during the forecast period.

Example Players in AI Hardware Market

- Advanced Micro Devices

- Amazon Web Services

- Allied Vision Technologies

- Alibaba

- Baidu

- Cadence Design Systems

- Cerebras Systems

- Cisco

- CEVA

- Fujitsu

- Graphcore

- Huawei

- IBM

- Intel

- Micron

- Microsoft

- Mythic

- NXP

- NVIDIA

- Oracle

- Qualcomm Technologies

- Samsung

- Synopsys

- Xilinx

AI HARDWARE MARKET: RESEARCH COVERAGE

The report on the AI hardware market features insights on various sections, including:

- Market Sizing and Opportunity Analysis: An in-depth analysis of the AI hardware market, focusing on key market segments, including [A] type of AI hardware, [B] type of deployment, [C] type of product, [D] type of device, [E] type of power consumption, [F] type of process, [G] type of end-users, [H] company size, [I] type of business model and [J] geographical regions.

- Competitive Landscape: A comprehensive analysis of the companies engaged in the AI hardware market, based on several relevant parameters, such as [A] year of establishment, [B] company size, [C] location of headquarters, [D] ownership structure.

- Company Profiles: Elaborate profiles of prominent players engaged in the AI hardware market, providing details on [A] location of headquarters, [B]company size, [C] company mission, [D] company footprint, [E] management team, [F] contact details, [G] financial information, [H] operating business segments, [I] AI hardware portfolio, [J] moat analysis, [K] recent developments, and an informed future outlook.

- SWOT Analysis: An insightful SWOT framework, highlighting the strengths, weaknesses, opportunities and threats in the domain. Additionally, it provides Harvey ball analysis, highlighting the relative impact of each SWOT parameter.

KEY QUESTIONS ANSWERED IN THIS REPORT

- How many companies are currently engaged in this market?

- What challenges does the AI hardware market face?

- What are the emerging trends in the AI hardware market?

- What factors are likely to influence the evolution of this market?

- What are the future focus areas in AI hardware development?

- What is the current and future market size?

- What is the CAGR of this market?

- How is the current and future market opportunity likely to be distributed across key market segments?

REASONS TO BUY THIS REPORT

- The report provides a comprehensive market analysis, offering detailed revenue projections of the overall market and its specific sub-segments. This information is valuable to both established market leaders and emerging entrants.

- Stakeholders can leverage the report to gain a deeper understanding of the competitive dynamics within the market. By analyzing the competitive landscape, businesses can make informed decisions to optimize their market positioning and develop effective go-to-market strategies.

- The report offers stakeholders a comprehensive overview of the market, including key drivers, barriers, opportunities, and challenges. This information empowers stakeholders to stay abreast of market trends and make data-driven decisions to capitalize on growth prospects.

ADDITIONAL BENEFITS

- Complimentary Excel Data Packs for all Analytical Modules in the Report

- 10% Free Content Customization

- Detailed Report Walkthrough Session with Research Team

- Free Updated report if the report is 6-12 months old or older

TABLE OF CONTENTS

1. PREFACE

- 1.1. Introduction

- 1.2. Market Share Insights

- 1.3. Key Market Insights

- 1.4. Report Coverage

- 1.5. Key Questions Answered

- 1.6. Chapter Outlines

2. RESEARCH METHODOLOGY

- 2.1. Chapter Overview

- 2.2. Research Assumptions

- 2.3. Database Building

- 2.3.1. Data Collection

- 2.3.2. Data Validation

- 2.3.3. Data Analysis

- 2.4. Project Methodology

- 2.4.1. Secondary Research

- 2.4.1.1. Annual Reports

- 2.4.1.2. Academic Research Papers

- 2.4.1.3. Company Websites

- 2.4.1.4. Investor Presentations

- 2.4.1.5. Regulatory Filings

- 2.4.1.6. White Papers

- 2.4.1.7. Industry Publications

- 2.4.1.8. Conferences and Seminars

- 2.4.1.9. Government Portals

- 2.4.1.10. Media and Press Releases

- 2.4.1.11. Newsletters

- 2.4.1.12. Industry Databases

- 2.4.1.13. Roots Proprietary Databases

- 2.4.1.14. Paid Databases and Sources

- 2.4.1.15. Social Media Portals

- 2.4.1.16. Other Secondary Sources

- 2.4.2. Primary Research

- 2.4.2.1. Introduction

- 2.4.2.2. Types

- 2.4.2.2.1. Qualitative

- 2.4.2.2.2. Quantitative

- 2.4.2.3. Advantages

- 2.4.2.4. Techniques

- 2.4.2.4.1. Interviews

- 2.4.2.4.2. Surveys

- 2.4.2.4.3. Focus Groups

- 2.4.2.4.4. Observational Research

- 2.4.2.4.5. Social Media Interactions

- 2.4.2.5. Stakeholders

- 2.4.2.5.1. Company Executives (CXOs)

- 2.4.2.5.2. Board of Directors

- 2.4.2.5.3. Company Presidents and Vice Presidents

- 2.4.2.5.4. Key Opinion Leaders

- 2.4.2.5.5. Research and Development Heads

- 2.4.2.5.6. Technical Experts

- 2.4.2.5.7. Subject Matter Experts

- 2.4.2.5.8. Scientists

- 2.4.2.5.9. Doctors and Other Healthcare Providers

- 2.4.2.6. Ethics and Integrity

- 2.4.2.6.1. Research Ethics

- 2.4.2.6.2. Data Integrity

- 2.4.3. Analytical Tools and Databases

- 2.4.1. Secondary Research

3. ECONOMIC AND OTHER PROJECT SPECIFIC CONSIDERATIONS

- 3.1. Forecast Methodology

- 3.1.1. Top-Down Approach

- 3.1.2. Bottom-Up Approach

- 3.1.3. Hybrid Approach

- 3.2. Market Assessment Framework

- 3.2.1. Total Addressable Market (TAM)

- 3.2.2. Serviceable Addressable Market (SAM)

- 3.2.3. Serviceable Obtainable Market (SOM)

- 3.2.4. Currently Acquired Market (CAM)

- 3.3. Forecasting Tools and Techniques

- 3.3.1. Qualitative Forecasting

- 3.3.2. Correlation

- 3.3.3. Regression

- 3.3.4. Time Series Analysis

- 3.3.5. Extrapolation

- 3.3.6. Convergence

- 3.3.7. Forecast Error Analysis

- 3.3.8. Data Visualization

- 3.3.9. Scenario Planning

- 3.3.10. Sensitivity Analysis

- 3.4. Key Considerations

- 3.4.1. Demographics

- 3.4.2. Market Access

- 3.4.3. Reimbursement Scenarios

- 3.4.4. Industry Consolidation

- 3.5. Robust Quality Control

- 3.6. Key Market Segmentations

- 3.7. Limitations

4. MACRO-ECONOMIC INDICATORS

- 4.1. Chapter Overview

- 4.2. Market Dynamics

- 4.2.1. Time Period

- 4.2.1.1. Historical Trends

- 4.2.1.2. Current and Forecasted Estimates

- 4.2.2. Currency Coverage

- 4.2.2.1. Overview of Major Currencies Affecting the Market

- 4.2.2.2. Impact of Currency Fluctuations on the Industry

- 4.2.3. Foreign Exchange Impact

- 4.2.3.1. Evaluation of Foreign Exchange Rates and Their Impact on Market

- 4.2.3.2. Strategies for Mitigating Foreign Exchange Risk

- 4.2.4. Recession

- 4.2.4.1. Historical Analysis of Past Recessions and Lessons Learnt

- 4.2.4.2. Assessment of Current Economic Conditions and Potential Impact on the Market

- 4.2.5. Inflation

- 4.2.5.1. Measurement and Analysis of Inflationary Pressures in the Economy

- 4.2.5.2. Potential Impact of Inflation on the Market Evolution

- 4.2.6. Interest Rates

- 4.2.6.1. Overview of Interest Rates and Their Impact on the Market

- 4.2.6.2. Strategies for Managing Interest Rate Risk

- 4.2.7. Commodity Flow Analysis

- 4.2.7.1. Type of Commodity

- 4.2.7.2. Origins and Destinations

- 4.2.7.3. Values and Weights

- 4.2.7.4. Modes of Transportation

- 4.2.8. Global Trade Dynamics

- 4.2.8.1. Import Scenario

- 4.2.8.2. Export Scenario

- 4.2.9. War Impact Analysis

- 4.2.9.1. Russian-Ukraine War

- 4.2.9.2. Israel-Hamas War

- 4.2.10. COVID Impact / Related Factors

- 4.2.10.1. Global Economic Impact

- 4.2.10.2. Industry-specific Impact

- 4.2.10.3. Government Response and Stimulus Measures

- 4.2.10.4. Future Outlook and Adaptation Strategies

- 4.2.11. Other Indicators

- 4.2.11.1. Fiscal Policy

- 4.2.11.2. Consumer Spending

- 4.2.11.3. Gross Domestic Product (GDP)

- 4.2.11.4. Employment

- 4.2.11.5. Taxes

- 4.2.11.6. R&D Innovation

- 4.2.11.7. Stock Market Performance

- 4.2.11.8. Supply Chain

- 4.2.11.9. Cross-Border Dynamics

- 4.2.1. Time Period

5. EXECUTIVE SUMMARY

6. INTRODUCTION

- 6.1. Chapter Overview

- 6.2. Overview of AI Hardware Market

- 6.2.1. Type of AI Hardware

- 6.2.2. Type of Deployment

- 6.2.3. Type of Product

- 6.2.4. Type of Device

- 6.2.5. Types of Power Consumption

- 6.2.6. Type of Processes

- 6.2.7. Type of End Users

- 6.3. Future Perspective

7. COMPETITIVE LANDSCAPE

- 7.1. Chapter Overview

- 7.2. AI Hardware: Overall Market Landscape

- 7.2.1. Analysis by Year of Establishment

- 7.2.2. Analysis by Company Size

- 7.2.3. Analysis by Location of Headquarters

- 7.2.4. Analysis by Ownership Structure

8. STARTUP ECOSYSTEM IN THE AI HARDWARE MARKET

- 8.1. AI Hardware Market: Market Landscape of Startups

- 8.1.1. Analysis by Year of Establishment

- 8.1.2. Analysis by Company Size

- 8.1.3. Analysis by Company Size and Year of Establishment

- 8.1.4. Analysis by Location of Headquarters

- 8.1.5. Analysis by Company Size and Location of Headquarters

- 8.1.6. Analysis by Ownership Structure

- 8.2. Key Findings

9. COMPANY PROFILES

- 9.1. Chapter Overview

- 9.2. Advanced Micro Devices*

- 9.2.1. Company Overview

- 9.2.2. Company Mission

- 9.2.3. Company Footprint

- 9.2.4. Management Team

- 9.2.5. Contact Details

- 9.2.6. Financial Performance

- 9.2.7. Operating Business Segments

- 9.2.8. Service / Product Portfolio (project specific)

- 9.2.9. MOAT Analysis

- 9.2.10. Recent Developments and Future Outlook

- 9.3. Amazon Web Services

- 9.4. Allied Vision Technologies

- 9.5. Alibaba

- 9.6. Baidu

- 9.7. Cadence Design Systems

- 9.8. Cerebras Design Systems

- 9.9. Cisco

- 9.10. CEVA

- 9.11. Fujitsu

- 9.12. Graphcore

- 9.13. Huawei

- 9.14. IBM

- 9.15. Intel

- 9.16. Micron

- 9.17. Microsoft

- 9.18. Mythic

- 9.19. NXP

- 9.20. NVIDIA

- 9.21. Oracle

- 9.22. Qualcomm Technologies

10. VALUE CHAIN ANALYSIS

11. SWOT ANALYSIS

12. GLOBAL AI HARDWARE MARKET

- 12.1. Chapter Overview

- 12.2. Key Assumptions and Methodology

- 12.3. Trends Disruption Impacting Market

- 12.4. Global AI Hardware Market, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 12.5. Multivariate Scenario Analysis

- 12.5.1. Conservative Scenario

- 12.5.2. Optimistic Scenario

- 12.6. Key Market Segmentations

13. MARKET OPPORTUNITIES BASED ON TYPE OF AI HARDWARE

- 13.1. Chapter Overview

- 13.2. Key Assumptions and Methodology

- 13.3. Revenue Shift Analysis

- 13.4. Market Movement Analysis

- 13.5. Penetration-Growth (P-G) Matrix

- 13.6. AI Hardware Market for Embedded Sound Processor: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 13.7. AI Hardware Market for Embedded Vision Processor: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 13.8. AI Hardware Market for Stand-alone Vision Processor: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 13.9. AI Hardware Market for Stand-alone Sound Processor: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 13.10. Data Triangulation and Validation

14. MARKET OPPORTUNITIES BASED ON TYPE OF DEPLOYMENT

- 14.1. Chapter Overview

- 14.2. Key Assumptions and Methodology

- 14.3. Revenue Shift Analysis

- 14.4. Market Movement Analysis

- 14.5. Penetration-Growth (P-G) Matrix

- 14.6. AI Hardware Market for Cloud: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 14.7. AI Hardware Market for On-Premises: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 14.8. Data Triangulation and Validation

15. MARKET OPPORTUNITIES BASED ON TYPE OF PRODUCT

- 15.1. Chapter Overview

- 15.2. Key Assumptions and Methodology

- 15.3. Revenue Shift Analysis

- 15.4. Market Movement Analysis

- 15.5. Penetration-Growth (P-G) Matrix

- 15.6. AI Hardware Market for Memory: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 15.6.1. AI Hardware Market for DRAM: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 15.6.2. AI Hardware Market for NVM: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 15.6.3. AI Hardware Market for SRAM: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 15.7. AI Hardware Market for Processors: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 15.7.1. AI Hardware Market for CPU: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 15.7.2. AI Hardware Market for FPGA: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 15.7.3. AI Hardware Market for GPU: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 15.7.4. AI Hardware Market for TPU: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 15.8. AI Hardware Market for Networking: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 15.9. AI Hardware Market for Storage: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 15.10. Data Triangulation and Validation

16. MARKET OPPORTUNITIES BASED ON TYPE OF DEVICE

- 16.1. Chapter Overview

- 16.2. Key Assumptions and Methodology

- 16.3. Revenue Shift Analysis

- 16.4. Market Movement Analysis

- 16.5. Penetration-Growth (P-G) Matrix

- 16.6. AI Hardware Market for Automotive: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 16.7. AI Hardware Market for Cameras: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 16.8. AI Hardware Market for Robots: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 16.9. AI Hardware Market for Smartphones: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 16.10. AI Hardware Market for Smart Mirror: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 16.11. AI Hardware Market for Smart Speaker: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 16.12. AI Hardware Market for Wearable: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 16.13. Data Triangulation and Validation

17. MARKET OPPORTUNITIES BASED ON TYPES OF POWER CONSUMPTION

- 17.1. Chapter Overview

- 17.2. Key Assumptions and Methodology

- 17.3. Revenue Shift Analysis

- 17.4. Market Movement Analysis

- 17.5. Penetration-Growth (P-G) Matrix

- 17.6. AI Hardware Market for Less than 1W: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 17.7. AI Hardware Market for 1-3W: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 17.8. AI Hardware Market for 3-5W: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 17.9. AI Hardware Market for 5-10W: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 17.10. AI Hardware Market for More than 10W: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 17.11. Data Triangulation and Validation

18. MARKET OPPORTUNITIES BASED ON TYPE OF PROCESSES

- 18.1. Chapter Overview

- 18.2. Key Assumptions and Methodology

- 18.3. Revenue Shift Analysis

- 18.4. Market Movement Analysis

- 18.5. Penetration-Growth (P-G) Matrix

- 18.6. AI Hardware Market for Inference: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 18.7. AI Hardware Market for Training: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 18.8. Data Triangulation and Validation

19. MARKET OPPORTUNITIES BASED ON TYPE OF END USERS

- 19.1. Chapter Overview

- 19.2. Key Assumptions and Methodology

- 19.3. Revenue Shift Analysis

- 19.4. Market Movement Analysis

- 19.5. Penetration-Growth (P-G) Matrix

- 19.6. AI Hardware Market for Aerospace & Defense: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.7. AI Hardware Market for Automotive & Transportation: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.8. AI Hardware Market for BFSI: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.9. AI Hardware Market for Consumer Electronics: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.10. AI Hardware Market for E-Commerce: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.11. AI Hardware Market for Education: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.12. AI Hardware Market for Energy & Utilities: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.13. AI Hardware Market for Government & Public Services: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.14. AI Hardware Market for Navigation: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.15. AI Hardware Market for Real Estate: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.16. AI Hardware Market for Smart Home: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.17. AI Hardware Market for Telecommunication & IT: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.18. AI Hardware Market for Others: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.19. Data Triangulation and Validation

20. MARKET OPPORTUNITIES AI HARDWARE IN NORTH AMERICA

- 20.1. Chapter Overview

- 20.2. Key Assumptions and Methodology

- 20.3. Revenue Shift Analysis

- 20.4. Market Movement Analysis

- 20.5. Penetration-Growth (P-G) Matrix

- 20.6. AI Hardware Market in North America: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 20.6.1. AI Hardware Market in the US: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 20.6.2. AI Hardware Market in Canada: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 20.6.3. AI Hardware Market in Mexico: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 20.6.4. AI Hardware Market in Other North American Countries: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 20.7. Data Triangulation and Validation

21. MARKET OPPORTUNITIES FOR AI HARDWARE IN EUROPE

- 21.1. Chapter Overview

- 21.2. Key Assumptions and Methodology

- 21.3. Revenue Shift Analysis

- 21.4. Market Movement Analysis

- 21.5. Penetration-Growth (P-G) Matrix

- 21.6. AI Hardware Market in Europe: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 21.6.1. AI Hardware Market in Austria: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 21.6.2. AI Hardware Market in Belgium: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 21.6.3. AI Hardware Market in Denmark: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 21.6.4. AI Hardware Market in France: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 21.6.5. AI Hardware Market in Germany: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 21.6.6. AI Hardware Market in Ireland: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 21.6.7. AI Hardware Market in Italy: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 21.6.8. AI Hardware Market in Netherlands: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 21.6.9. AI Hardware Market in Norway: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 21.6.10. AI Hardware Market in Russia: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 21.6.11. AI Hardware Market in Spain: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 21.6.12. AI Hardware Market in Sweden: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 21.6.13. AI Hardware Market in Sweden: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 21.6.14. AI Hardware Market in Switzerland: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 21.6.15. AI Hardware Market in the UK: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 21.6.16. AI Hardware Market in Other European Countries: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 21.7. Data Triangulation and Validation

22. MARKET OPPORTUNITIES FOR AI HARDWARE IN ASIA

- 22.1. Chapter Overview

- 22.2. Key Assumptions and Methodology

- 22.3. Revenue Shift Analysis

- 22.4. Market Movement Analysis

- 22.5. Penetration-Growth (P-G) Matrix

- 22.6. AI Hardware Market in Asia: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 22.6.1. AI Hardware Market in China: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 22.6.2. AI Hardware Market in India: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 22.6.3. AI Hardware Market in Japan: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 22.6.4. AI Hardware Market in Singapore: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 22.6.5. AI Hardware Market in South Korea: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 22.6.6. AI Hardware Market in Other Asian Countries: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 22.7. Data Triangulation and Validation

23. MARKET OPPORTUNITIES FOR AI HARDWARE IN MIDDLE EAST AND NORTH AFRICA (MENA)

- 23.1. Chapter Overview

- 23.2. Key Assumptions and Methodology

- 23.3. Revenue Shift Analysis

- 23.4. Market Movement Analysis

- 23.5. Penetration-Growth (P-G) Matrix

- 23.6. AI Hardware Market in Middle East and North Africa (MENA): Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.6.1. AI Hardware Market in Egypt: Historical Trends (Since 2019) and Forecasted Estimates (Till 205)

- 23.6.2. AI Hardware Market in Iran: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.6.3. AI Hardware Market in Iraq: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.6.4. AI Hardware Market in Israel: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.6.5. AI Hardware Market in Kuwait: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.6.6. AI Hardware Market in Saudi Arabia: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.6.7. AI Hardware Market in United Arab Emirates (UAE): Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.6.8. AI Hardware Market in Other MENA Countries: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 23.7. Data Triangulation and Validation

24. MARKET OPPORTUNITIES FOR AI HARDWARE IN LATIN AMERICA

- 24.1. Chapter Overview

- 24.2. Key Assumptions and Methodology

- 24.3. Revenue Shift Analysis

- 24.4. Market Movement Analysis

- 24.5. Penetration-Growth (P-G) Matrix

- 24.6. AI Hardware Market in Latin America: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.1. AI Hardware Market in Argentina: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.2. AI Hardware Market in Brazil: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.3. AI Hardware Market in Chile: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.4. AI Hardware Market in Colombia Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.5. AI Hardware Market in Venezuela: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.6.6. AI Hardware Market in Other Latin American Countries: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 24.7. Data Triangulation and Validation

25. MARKET OPPORTUNITIES FOR AI HARDWARE IN REST OF THE WORLD

- 25.1. Chapter Overview

- 25.2. Key Assumptions and Methodology

- 25.3. Revenue Shift Analysis

- 25.4. Market Movement Analysis

- 25.5. Penetration-Growth (P-G) Matrix

- 25.6. AI Hardware Market in Rest of the World: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 25.6.1. AI Hardware Market in Australia: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 25.6.2. AI Hardware Market in New Zealand: Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 25.6.3. AI Hardware Market in Other Countries

- 25.7. Data Triangulation and Validation

26. TABULATED DATA

27. LIST OF COMPANIES AND ORGANIZATIONS

28. CUSTOMIZATION OPPORTUNITIES

29. ROOTS SUBSCRIPTION SERVICES

30. AUTHOR DETAILS

NVIDIA H20 和 RTX PRO 推动中国 AI 晶片市场:2025 年展望

NVIDIA H20 和 RTX PRO 推动中国 AI 晶片市场:2025 年展望 人工智慧硬体市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

人工智慧硬体市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 2032 年人工智慧晶片市场预测:按晶片类型、处理类型、功能、技术节点、记忆体类型、应用、最终用户和地区进行全球分析

2032 年人工智慧晶片市场预测:按晶片类型、处理类型、功能、技术节点、记忆体类型、应用、最终用户和地区进行全球分析 2025-2029 年边缘设备 AI 硬体全球市场

2025-2029 年边缘设备 AI 硬体全球市场 SNEC 2025洞察:引领市场成熟度与下一波太阳能创新浪潮全球人工智慧(AI)影音SoC市场全球人工智慧处理器市场

SNEC 2025洞察:引领市场成熟度与下一波太阳能创新浪潮全球人工智慧(AI)影音SoC市场全球人工智慧处理器市场 人工智慧晶片市场,按产品类型、按技术、按应用、按功能、按最终用户、按国家和地区 - 2025 年至 2032 年全球行业分析、市场规模、市场份额和预测AI晶片市场 (~2035年):晶片类型·处理类型·技术·功能·用途·终端用户·企业类型·各地区的产业趋势与全球预测

人工智慧晶片市场,按产品类型、按技术、按应用、按功能、按最终用户、按国家和地区 - 2025 年至 2032 年全球行业分析、市场规模、市场份额和预测AI晶片市场 (~2035年):晶片类型·处理类型·技术·功能·用途·终端用户·企业类型·各地区的产业趋势与全球预测 2025年设备智慧全球市场报告

2025年设备智慧全球市场报告