|

市场调查报告书

商品编码

1817405

医疗保健的生成AI市场:2035年前的产业趋势和全球预测 - 各目的,各报价环类型,各应用领域,各终端用户,各主要地区,主要加入企业Generative AI in Healthcare Market: Industry Trends and Global Forecasts, Till 2035 - Distribution by Purpose, Type of Offering, Application Area, End-User, Key Geographical Regions and Leading Players: |

||||||

医疗保健生成式人工智慧市场概览

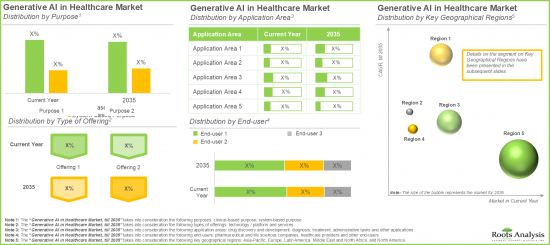

全球医疗保健生成式人工智慧市场目前估值 33 亿美元,预计在预测期内将以 28% 的复合年增长率成长,到 2035 年将达到 398 亿美元。

医疗保健生成式人工智慧市场机会细分为以下几个部分:

目的

- 临床为基础的目的

- 系统为基础的目的

报价环类型

- 科技/平台

- 服务

应用领域

- 药物研发与开发

- 诊断

- 治疗

- 管理业务

- 其他

终端用户

- 製药公司及生命科学企业

- 医疗保健供应商

- 其他的终端用户

主要地区

- 北美

- 欧洲

- 亚太地区

- 中东·北非

- 南美

北美市场

- 美国

- 加拿大

欧洲市场

- 德国

- 英国

- 法国

- 西班牙

- 瑞士

- 荷兰

- 其他欧洲

亚太地区市场

- 中国

- 日本

- 韩国

- 新加坡

- 印度

- 其他

中东·北非市场

- 以色列

- 阿拉伯联合大公国

- 其他

南美市场

- 巴西

- 其他

医疗保健市场中的生成式人工智慧成长与趋势

生成式人工智慧是人工智慧的一个分支,它利用生成模型创建资料驱动的输出,例如洞察、图像、视讯和其他格式。在医疗保健领域,这项技术正在迅速发展,并有可能改变病患照护、研究和治疗方式。

医疗保健产业目前正面临许多课题,错综复杂,包括临床工作流程效率低、治疗成本上升、人员短缺以及医护人员倦怠。根据 Medscape 发布的 "2024 年医生倦怠与忧郁报告" ,约 49% 的医生表示经历过倦怠,其中包括行政负担(62%)和长时间工作(41%)。此外,传统的药物研发方法缺乏对个人化治疗方案的关注,并且仍然耗时且耗力。此外,儘管投入了大量的时间和金钱,但仍有约 90% 的新药候选药物未能进入临床试验阶段。如此高的失败率不仅扼杀了创新,也增加了全球医疗保健系统的财务负担。

为了应对这些课题,一些製药和生命科学公司对采用生成式人工智慧 (CGAI) 的兴趣日益浓厚。此外,值得强调的是,医疗产业的生成性人工智慧在自动化行政流程以提高整体营运效率、透过高阶成像提高诊断准确性、个人化患者参与以及加速药物发现和开发方面具有巨大潜力。具体而言,仅在行政营运中实施生成性人工智慧就可以为整个医疗产业节省约1500亿美元。此外,研究表明,生成性人工智慧可以将诊断错误减少高达85%,将护理师加班时间减少21%,从而在三年内为每家医院节省约469,000美元的潜在成本。然而,随着医疗机构将生成性人工智慧整合到其系统中,建立一个强大的治理框架至关重要,以确保人工智慧的道德使用并解决资料隐私、演算法偏差和透明度等关键问题。

近年来,多家製药和医疗保健公司与多家人工智慧公司建立了策略合作伙伴关係,共同探索生成式人工智慧在医疗保健领域的应用。同时,多家生成式人工智慧开发公司已获得大量资金,以增强其针对各种医疗应用的模型能力。鑑于投资者兴趣日益增长以及合作环境不断扩大,医疗健康领域的生成式人工智慧市场预计将在未来几年持续成长。

医疗健康领域的生成式人工智慧市场:关键洞察

本报告深入探讨了医疗健康领域生成式人工智慧市场的现状,并揭示了该行业的潜在成长机会。报告的主要内容包括:

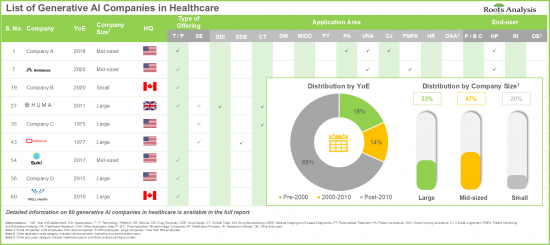

- 在医疗保健产业提供生成式人工智慧解决方案的公司中,超过 45% 为中型企业,其中 79% 总部位于北美。

- 超过 85% 的公司提供生成式人工智慧技术/平台,以简化各种医疗保健流程,27% 的生成式人工智慧公司能够满足医疗保健提供者和 P/B 公司不断变化的需求。

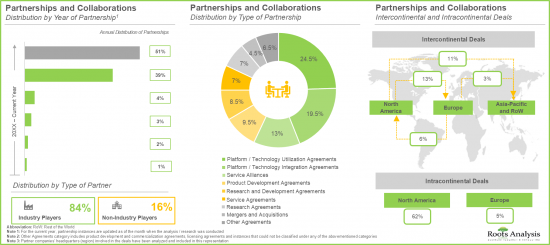

- 人们对该领域日益增长的兴趣也体现在合作活动的增多,近 90% 的交易是在过去两年内达成的。

- 我们的分析预测,买方在生成式人工智慧医疗保健市场的议价能力非常高。

- 医疗保健领域行政负担的增加、资金和投资的增加以及人工智慧和机器学习的进步预计将推动医疗保健领域生成式人工智慧市场的发展,并在可预见的未来实现稳步增长。

- 技术/平台部分目前占近 75% 的市场。预计到2035年,医疗保健领域的生成式人工智慧市场将以28%的复合年增长率持续成长。

医疗保健领域的生成式人工智慧市场:主要细分市场

依用途划分,全球市场分为基于临床用途及基于系统用途两大类。其中,基于临床用途的细分市场目前占了整个市场的最大占有率。这可能是因为医疗保健领域的生成式人工智慧能够帮助临床医生做出更明智的决策,并且在医院和诊所的应用日益广泛,直接影响患者护理。

依产品类型划分,全球医疗保健领域的生成式人工智慧市场分为平台/技术和服务。目前,平台/技术部门占了整个市场的最大占有率。然而,值得注意的是,服务部门预计在预测期内将以相对较高的复合年增长率成长。

依应用领域划分,全球医疗保健生成式人工智慧市场分为药物研发和市场推广、诊断、治疗、行政营运和其他应用。目前,治疗领域在医疗保健生成式人工智慧市场中处于领先地位。需要强调的是,这一趋势未来不太可能改变。这是因为生成式人工智慧可以改善治疗效果和患者护理,减轻行政负担,并促进临床应用的持续成长。

按最终用户划分,全球医疗保健生成式人工智慧市场分为製药和生命科学公司、医疗保健提供者和其他最终用户。目前,该市场主要由供医疗保健提供者使用的系统产生的收入主导。此外,由于基因人工智慧解决方案的广泛应用,包括增强患者护理、提高营运效率、数据驱动的洞察以及潜在的成本节约,这一市场趋势未来不太可能改变。

依主要地区划分,市场分为北美、欧洲、亚太、中东和北非以及拉丁美洲。在当前情况下,北美很可能占最大的市场占有率。此外,值得注意的是,预计亚太地区在预测期内将以相对较高的复合年增长率成长。

医疗保健的生成AI市场参与企业案例

- Amazon Web Services

- C3 AI

- Exscientia

- Huma

- IBM

- Iktos

- LeewayHertz

- Medical IP

- Microsoft

- NVIDIA

- OpenAI

- Oracle

- PhamaX

- Syntegra

初步研究概要

本研究中提出的观点和见解受到与多位利害关係人讨论的影响。本研究报告包含与以下产业参与者的详细访谈记录:

- 一家美国中型公司的财务副总裁兼投资者关係主管

- 一家以色列中型公司的行销总监

- 一家法国中型公司的亚洲应用科学家

医疗保健领域生成式人工智慧市场研究报告

本报告研究了医疗保健领域生成式人工智慧市场,并得出以下结论:

- 市场规模和机会分析:本报告深入分析了医疗保健领域生成式人工智慧市场的当前市场机会和未来成长潜力,重点关注关键细分市场,例如[A] 目标、[B] 交付类型、[C] 应用领域、[D] 最终用户、[E] 主要地区和[G] 关键参与者。

- 市场影响分析:对可能影响市场成长的各种因素进行全面分析,包括[A]推动因素、[B]阻碍因素、[C]机会和[D]现有课题。

- 市场格局:本报告基于若干相关参数,对医疗保健提供者中的生成性人工智慧进行了全面评估,包括[A]交付类型、[B]应用领域和[C]最终用户。

- 医疗保健提供者中的生成性人工智慧展望:列出在此领域运营的医疗保健提供者中的生成性人工智慧公司,并基于[A]成立年份、[B]公司规模、[C]总部位置和[D]生成性人工智慧公司类型进行分析。

- 竞争分析:基于各种相关参数,例如[A]公司优势、[B]服务组合优势等。基于市场占有率,对医疗领域生成式人工智慧提供者进行深入的竞争分析。

- 公司简介:包含以下资讯:A) 公司概况、[B] 财务资讯(如有)、[C] 医疗领域生成式人工智慧产品组合、[D] 近期发展和 [E] 未来展望。

- 合作伙伴关係与合作:基于若干相关参数,对医疗领域生成式人工智慧市场利益相关者之间达成的合作伙伴关係进行详细分析,例如 A) 合作年份、[B] 合作类型、[C] 合作公司类型、[D] 合作目标、[E] 地区和 [G] 最活跃的参与者(合作伙伴数量)。

- 医疗领域生成式人工智慧用例:医疗领域生成式人工智慧用例的详细案例研究,介绍医疗领域各生成式人工智慧公司之间达成的合作资讯。每个用例都提供有关各种参数的信息,例如 [A] 参与公司概况、[B] 业务需求、[C] 已实现目标的详细资讯以及 [D] 提供的解决方案。

目录

章节1 报告概要

第1章 序文

第2章 调查手法

第3章 市场动态

- 章概要

- 预测调查手法

- 市场评估组成架构

- 预测工具和技巧

- 重要的考虑事项

- 限制事项

第4章 宏观经济指标

- 章概要

- 市场动态

- 结论

章节2 定性洞察

第5章 摘要整理

第6章 简介

章节3 场概要

第7章 竞争情形

- 章概要

- 医疗保健的生成AI企业:市场形势

第8章 企业竞争力分析

- 章概要

- 前提主要的参数

- 调查手法

- 医疗保健的生成AI企业:企业竞争力分析

章节4 企业简介

第9章 北美的医疗保健的生成AI企业

- 章概要

- 北美设置据点的生成AI企业的详细介绍

- IBM

- Microsoft

- NVIDIA

- OpenAI

- 北美设置据点的生成AI企业的简介

- Amazon Web Services

- C3 AI

- Oracle

- Syntegra

第10章 欧洲和亚太地区的医疗保健的生成AI企业

- 章概要

- 在欧洲和亚太地区设置据点的生成AI企业的详细介绍

- Huma

- LeewayHertz

- 在欧洲和亚太地区设置据点的生成AI企业的简介

- Exscientia

- Iktos

- Medical IP

- PhamaX

章节5 市场趋势

第11章 伙伴关係和合作

第12章 医疗保健的生成AI:使用案例

- 章概要

- 使用案例1:NVIDIA和Genentech的合作

- 使用案例2:Insilico Medicine和Inimmune的合作

- 使用案例3:OpenAI和Moderna的合作

- 使用案例4:Amazon Web Services和Pfizer的合作

- 使用案例5:Suki和Ascension Saint Thomas的合作

- 使用案例6:Abridge和Emory Healthcare的合作

- 使用案例7:Google和China Medical University Hospital的联合

章节6 市场机会分析

第13章 市场影响分析:促进因素,阻碍因素,机会,课题

第14章 医疗保健市场上全球的生成AI

第15章 医疗保健市场上生成AI(各目的)

第16章 医疗保健市场上生成AI(各提供类型)

第17章 医疗保健市场上生成AI(各应用领域)

第18章 医疗保健市场上生成AI(各终端用户)

第19章 医疗保健市场上生成AI(各地区)

第20章 医疗保健市场上生成AI(主要加入企业)

第21章 邻近市场分析

章节7 策略工具

第22章 波特的五力分析

章节8 其他独家洞察

第23章 来自初步研究的洞察

第24章 结论

章节9 附录

第25章 表格形式资料

第26章 企业·团体一览

第27章 客制化的机会

第28章 始祖订阅服务

第29章 着者详细内容

GENERATIVE AI in HEALTHCARE MARKET: OVERVIEW

As per Roots Analysis, the global generative AI in healthcare market is currently valued at USD 3.3 billion and is projected to reach USD 39.8 billion by 2035, growing at a CAGR of 28% during the forecast period.

The opportunity for generative AI in healthcare market has been distributed across the following segments:

Purpose

- Clinical-based Purpose

- System-based Purpose

Type of Offering

- Technology / Platform

- Service

Application Area

- Drug Discovery and Development

- Diagnosis

- Treatment

- Administrative Tasks

- Other Application Areas

End-User

- Pharmaceutical and Life Science Companies

- Healthcare Providers

- Other End-Users

Key Geographical Regions

- North America

- Europe

- Asia-Pacific

- Middle East and North Africa

- Latin America

Market in North America

- US

- Canada

Market in Europe

- Germany

- UK

- France

- Spain

- Switzerland

- The Netherlands

- Rest of Europe

Market in Asia-Pacific

- China

- Japan

- South Korea

- Singapore

- India

- Rest of Asia-Pacific

Market in Middle East and North Africa

- Israel

- UAE

- Rest of Middle East and North Africa

Market in Latin America

- Brazil

- Rest of Latin America

Generative AI in Healthcare Market: Growth and Trends

Generative AI is a part of artificial intelligence that utilizes generative models to create data-driven outputs, such as insights, images, videos, and other formats. In the healthcare sector, this technology is evolving rapidly, with the potential to transform patient care, research and treatment.

The healthcare industry is currently navigating a complex landscape marked by a number of challenges, including inefficiencies in clinical workflows, escalating treatment costs, staff shortages, and burnout of the healthcare workers. According to Medscape's 2024 Physician Burnout and Depression Report, nearly 49% of physicians reported feeling burnt out, with administrative burdens (62%) and long working hours (41%). In addition, the conventional drug discovery methods remain time-intensive with no focus on the personalized treatment approaches. Moreover, about 90% of drug candidates fail to progress to advanced clinical trial phases, despite significant time and financial investments. This high failure rate not only impedes innovation but also intensifies the financial strains on the global healthcare systems.

To address these challenges, several pharmaceutical and life sciences companies have increasingly shown interest in exploring the adoption of generative AI. Further, it is important to highlight that generative AI in healthcare industry holds great potential in automating administrative processes for improving the overall operational efficiency, enhancing diagnostic accuracy through advanced imaging, personalizing patient engagement, and accelerating drug discovery and development. Notably, the implementation of generative AI in administrative tasks alone could generate annual savings of approximately USD 150 billion across the healthcare sector. Additionally, studies suggest generative AI could reduce diagnostic errors by up to 85% and reduce nursing overtime by 21%, resulting in potential cost savings of nearly USD 469,000 over the span of three years per hospital. However, as healthcare organizations integrate generative AI into their systems, it is essential to establish robust governance frameworks that ensure ethical AI use and address key concerns, such as data privacy, algorithmic bias, and transparency.

In recent years, several pharmaceutical and healthcare companies have entered into strategic partnerships with various AI firms to explore applications of generative AI in healthcare. Simultaneously, several generative AI developers are securing significant funding in order to enhance their model capabilities for diverse medical applications. Given the growing interest of the investors and the expanding collaborative landscape, generative AI in healthcare market is poised for sustained growth in the coming years.

Generative AI in Healthcare Market: Key Insights

The report delves into the current state of the generative AI in healthcare market and identifies potential growth opportunities within industry. The key takeaways of the report are:

- More than 45% of the companies engaged in offering generative AI solutions in the healthcare industry are mid-sized firms; of these, 79% of the firms are headquartered in North America.

- >85% of the companies offer gen AI technology / platforms to streamline various healthcare processes; of these, 27% of the gen AI companies cater to the evolving needs of both, healthcare providers and P / B companies.

- The rising interest in this domain is reflected by the rise in partnership activity; notably, close to 90% of the deals were inked in the last two years.

- Based on our analysis, in the generative AI in healthcare market, we expect the buyers to have a very high bargaining power; any initiative taken must be carefully evaluated, considering the likely future market dynamics.

- The increasing administrative burden in healthcare, rising funding and investments, and advancements in AI and ML are likely to drive the market for gen AI in healthcare, leading to steady growth in the foreseeable future.

- The technology / platform segment dominates the current market with close to 75% of the market share; notably, generative AI in healthcare market is anticipated to grow at a lucrative growth rate (CAGR of 28%) till 2035.

Generative AI in Healthcare Market: Key Segments

Generative AI used for Clinical-based Purposes is Likely to Hold the Largest Share of the Current Market During the Forecast Period

Based on purpose, the global market is segmented into clinical-based and system-based purposes. Amongst these types, the clinical-based purpose segment occupies the largest share of the current overall market. This can be attributed to their direct impact on patient care, as these would help the clinicians make informed decisions, increasing their adoption in the hospitals and clinics.

Based on the Type of Offering, Platform / Technology Segment Captures the Majority of the Current Market Share

Based on the type of offerings, the global generative AI in healthcare market is segmented into platform / technology and service. Presently, the platform / technology segment occupies the highest share in the overall market. However, it is important to note that the services segment is anticipated to grow at a relatively higher CAGR during the forecast period.

Treatment Segment is Likely to Hold the Largest Share in the Generative AI in Healthcare Market During the Forecast Period

Based on the application area, the global generative AI in healthcare market is segmented into drug discovery and development, diagnosis, treatment, administrative tasks and other application areas. Currently, the treatment segment leads generative AI in healthcare market. It is important to highlight that this trend is unlikely to change in the future as well. This can be attributed to the fact that generative AI boosts treatment efficacy and patient care, reducing administrative burdens, driving sustained growth in clinical applications.

Generative AI in Healthcare Market for Healthcare Providers is Likely to Grow at a Relatively Faster Pace During the Forecast Period

Based on the end-user, the global generative AI in healthcare market is segmented across pharmaceutical and life science companies, healthcare providers and other end-users. Presently, the market is dominated by the revenues generated through the systems intended for use by healthcare providers. Further, this market trend is unlikely to change in the future as well owing to the wider applicability of the gen AI solutions, such as enhanced patient care, improved operational efficiency, data driven insights and cost saving potential.

North America Accounts for the Largest Share in the Market

Based on key geographical regions, the market is segmented into North America, Europe, Asia-Pacific, Middle East and North Africa and Latin America. In the current scenario, North America is likely to capture the largest market share. Further, it is worth highlighting that Asia-Pacific is expected to grow at a relatively high CAGR during the forecast period.

Example Players in the Generative AI in Healthcare Market

- Amazon Web Services

- C3 AI

- Exscientia

- Huma

- IBM

- Iktos

- LeewayHertz

- Medical IP

- Microsoft

- NVIDIA

- OpenAI

- Oracle

- PhamaX

- Syntegra

Primary Research Overview

The opinions and insights presented in this study were influenced by discussions conducted with multiple stakeholders. The research report features detailed transcripts of interviews held with the following industry stakeholders:

- Vice President, Finance and Head of Investor Relations, Mid-sized Company in the US

- Marketing Director, Mid-sized Company in Israel

- Application Scientist of Asia, Mid-sized Company in France

Generative AI in Healthcare Market: Research Coverage

The report on generative AI in healthcare market features insights into various sections, including:

- Market Sizing and Opportunity Analysis: An in-depth analysis of current market opportunity and the future growth potential of generative AI in healthcare market, focusing on key market segments, including [A] purpose, [B] type of offering, [C] application area, [D] end-user, [E] key geographical regions, and [G] leading players.

- Market Impact Analysis: A thorough analysis of various factors, such as [A] drivers, [B] restraints, [C] opportunities, and [D] existing challenges that are likely to impact market growth.

- Market Landscape: A comprehensive evaluation of generative AI in healthcare providers, based on several relevant parameters, such as [A] type of offering, [B] application area, and [C] end-user.

- Generative AI in Healthcare Providers Landscape: The report features a list of generative AI in healthcare providers engaged in this domain, along with analyses based on [A] year of establishment, [B] company size [C] location of headquarters, and [D] type of generative AI company.

- Company Competitiveness Analysis: An insightful competitiveness analysis of the generative AI in healthcare providers, based on various relevant parameters, such as [A] company strength, and [B] service portfolio strength.

- Company Profiles: Comprehensive profiles of key industry players in the generative AI in the healthcare domain, featuring information on [A] company overview, [B] financial information (if available), [C] generative AI in healthcare portfolio, [D] recent developments, and [E] future outlook statements.

- Partnerships and Collaborations: A detailed analysis of partnerships inked between stakeholders in the generative AI in healthcare market, based on several relevant parameters, such as [A] year of partnership, [B] type of partnership, [C] type of partner company, [D] purpose of partnership, [E] geography, and [G] most active players (in terms of number of partnerships).

- Generative AI in Healthcare Use Cases: A detailed case study of the use cases of generative AI in healthcare, presenting information on collaborations inked between various generative AI companies in healthcare. Each use case provides information on various parameters, such as [A] a brief overview of the companies involved, [B] business needs [C] details on the objectives achieved, and [D] solutions provided.

Key Questions Answered in this Report

- How many companies are currently engaged in this market?

- Which are the leading companies in this market?

- What factors are likely to influence the evolution of this market?

- What is the current and future market size?

- What is the CAGR of this market?

- How is the current and future market opportunity likely to be distributed across key market segments?

Reasons to Buy this Report

- The report provides a comprehensive market analysis, offering detailed revenue projections of the overall market and its specific sub-segments. This information is valuable to both established market leaders and emerging entrants.

- Stakeholders can leverage the report to gain a deeper understanding of the competitive dynamics within the market. By analyzing the competitive landscape, businesses can make informed decisions to optimize their market positioning and develop effective go-to-market strategies.

- The report offers stakeholders a comprehensive overview of the market, including key drivers, barriers, opportunities, and challenges. This information empowers stakeholders to stay abreast of market trends and make data-driven decisions to capitalize on growth prospects.

Additional Benefits

- Complimentary PPT Insights Packs

- Complimentary Excel Data Packs for all Analytical Modules in the Report

- 15% Free Content Customization

- Detailed Report Walkthrough Session with Research Team

- Free Updated report if the report is 6-12 months old or older

TABLE OF CONTENTS

SECTION I: REPORT OVERVIEW

1. PREFACE

- 1.1. Introduction

- 1.2. Market Share Insights

- 1.3. Key Market Insights

- 1.4. Report Coverage

- 1.5. Key Questions Answered

- 1.6. Chapter Outlines

2. RESEARCH METHODOLOGY

- 2.1. Chapter Overview

- 2.2. Research Assumptions

- 2.2.1. Market Landscape and Market Trends

- 2.2.2. Market Forecast and Opportunity Analysis

- 2.2.3. Comparative Analysis

- 2.3. Database Building

- 2.3.1. Data Collection

- 2.3.2. Data Validation

- 2.3.3. Data Analysis

- 2.4. Project Methodology

- 2.4.1. Secondary Research

- 2.4.1.1. Annual Reports

- 2.4.1.2. Academic Research Papers

- 2.4.1.3. Company Websites

- 2.4.1.4. Investor Presentations

- 2.4.1.5. Regulatory Filings

- 2.4.1.6. White Papers

- 2.4.1.7. Industry Publications

- 2.4.1.8. Conferences and Seminars

- 2.4.1.9. Government Portals

- 2.4.1.10. Media and Press Releases

- 2.4.1.11. Newsletters

- 2.4.1.12. Industry Databases

- 2.4.1.13. Roots Proprietary Databases

- 2.4.1.14. Paid Databases and Sources

- 2.4.1.15. Social Media Portals

- 2.4.1.16. Other Secondary Sources

- 2.4.2. Primary Research

- 2.4.2.1. Types of Primary Research

- 2.4.2.1.1. Qualitative Research

- 2.4.2.1.2. Quantitative Research

- 2.4.2.1.3. Hybrid Approach

- 2.4.2.2. Advantages of Primary Research

- 2.4.2.3. Techniques for Primary Research

- 2.4.2.3.1. Interviews

- 2.4.2.3.2. Surveys

- 2.4.2.3.3. Focus Groups

- 2.4.2.3.4. Observational Research

- 2.4.2.3.5. Social Media Interactions

- 2.4.2.4. Key Opinion Leaders Considered in Primary Research

- 2.4.2.4.1. Company Executives (CXOs)

- 2.4.2.4.2. Board of Directors

- 2.4.2.4.3. Company Presidents and Vice Presidents

- 2.4.2.4.4. Research and Development Heads

- 2.4.2.4.5. Technical Experts

- 2.4.2.4.6. Subject Matter Experts

- 2.4.2.4.7. Scientists

- 2.4.2.4.8. Doctors and Other Healthcare Providers

- 2.4.2.5. Ethics and Integrity

- 2.4.2.5.1. Research Ethics

- 2.4.2.5.2. Data Integrity

- 2.4.2.1. Types of Primary Research

- 2.4.3. Analytical Tools and Databases

- 2.4.1. Secondary Research

- 2.5. Robust Quality Control

3. MARKET DYNAMICS

- 3.1. Chapter Overview

- 3.2. Forecast Methodology

- 3.2.1. Top-down Approach

- 3.2.2. Bottom-up Approach

- 3.2.3. Hybrid Approach

- 3.3. Market Assessment Framework

- 3.3.1. Total Addressable Market (TAM)

- 3.3.2. Serviceable Addressable Market (SAM)

- 3.3.3. Serviceable Obtainable Market (SOM)

- 3.3.4. Currently Acquired Market (CAM)

- 3.4. Forecasting Tools and Techniques

- 3.4.1. Qualitative Forecasting

- 3.4.2. Correlation

- 3.4.3. Regression

- 3.4.4. Extrapolation

- 3.4.5. Convergence

- 3.4.6. Sensitivity Analysis

- 3.4.7. Scenario Planning

- 3.4.8. Data Visualization

- 3.4.9. Time Series Analysis

- 3.4.10. Forecast Error Analysis

- 3.5. Key Considerations

- 3.5.1. Demographics

- 3.5.2. Government Regulations

- 3.5.3. Reimbursement Scenarios

- 3.5.4. Market Access

- 3.5.5. Supply Chain

- 3.5.6. Industry Consolidation

- 3.5.7. Pandemic / Unforeseen Disruptions Impact

- 3.6. Limitations

4. MACRO-ECONOMIC INDICATORS

- 4.1. Chapter Overview

- 4.2. Market Dynamics

- 4.2.1. Time Period

- 4.2.1.1. Historical Trends

- 4.2.1.2. Current and Forecasted Estimates

- 4.2.2. Currency Coverage

- 4.2.2.1. Major Currencies Affecting the Market

- 4.2.2.2. Factors Affecting Currency Fluctuations on the Industry

- 4.2.2.3. Impact of Currency Fluctuations on the Industry

- 4.2.3. Foreign Currency Exchange Rate

- 4.2.3.1. Impact of Foreign Exchange Rate Volatility on the Market

- 4.2.3.2. Strategies for Mitigating Foreign Exchange Risk

- 4.2.4. Recession

- 4.2.4.1. Assessment of Current Economic Conditions and Potential Impact on the Market

- 4.2.4.2. Historical Analysis of Past Recessions and Lessons Learnt

- 4.2.5. Inflation

- 4.2.5.1. Measurement and Analysis of Inflationary Pressures in the Economy

- 4.2.5.2. Potential Impact of Inflation on the Market Evolution

- 4.2.6. Interest Rates

- 4.2.6.1. Interest Rates and Their Impact on the Market

- 4.2.6.2. Strategies for Managing Interest Rate Risk

- 4.2.7. Commodity Flow Analysis

- 4.2.7.1. Type of Commodity

- 4.2.7.2. Origins and Destinations

- 4.2.7.3. Values and Weights

- 4.2.7.4. Modes of Transportation

- 4.2.8. Global Trade Dynamics

- 4.2.8.1. Import Scenario

- 4.2.8.2. Export Scenario

- 4.2.8.3. Trade Policies

- 4.2.8.4. Strategies for Mitigating the Risks Associated with Trade Barriers

- 4.2.8.5. Impact of Trade Barriers on the Market

- 4.2.9. War Impact Analysis

- 4.2.9.1. Russian-Ukraine War

- 4.2.9.2. Israel-Hamas War

- 4.2.10. COVID Impact / Related Factors

- 4.2.10.1. Global Economic Impact

- 4.2.10.2. Industry-specific Impact

- 4.2.10.3. Government Response and Stimulus Measures

- 4.2.10.4. Future Outlook and Adaptation Strategies

- 4.2.11. Other Indicators

- 4.2.11.1. Fiscal Policy

- 4.2.11.2. Consumer Spending

- 4.2.11.3. Gross Domestic Product

- 4.2.11.4. Employment

- 4.2.11.5. Taxes

- 4.2.11.6. Stock Market Performance

- 4.2.11.7. Cross Border Dynamics

- 4.2.1. Time Period

- 4.3. Conclusion

SECTION II: QUALITATIVE INSIGHTS

5. EXECUTIVE SUMMARY

6. INTRODUCTION

- 6.1. Chapter Overview

- 6.2. Introduction to Generative AI

- 6.3. Evolution of AI

- 6.4. Applications of Generative AI in Healthcare

- 6.4.1. Healthcare Research

- 6.4.1.1. Drug Discovery and Development

- 6.4.2. Disease Diagnosis and Prognosis

- 6.4.3. Treatment and Medical Care

- 6.4.4. Marketing and Administrative Tasks

- 6.4.1. Healthcare Research

- 6.5. Challenges Associated with the Adoption of Generative AI

- 6.6. Future Perspectives

SECTION III: MARKET OVERVIEW

7. COMPETITIVE LANDSCAPE

- 7.1. Chapter Overview

- 7.2. Generative AI Companies in Healthcare: Overall Market Landscape

- 7.2.1. Analysis by Year of Establishment

- 7.2.2. Analysis by Company Size

- 7.2.3. Analysis by Location of Headquarters

- 7.2.4. Analysis by Company Size and Location of Headquarters (Region)

- 7.2.5. Analysis by Type of Generative AI Company

- 7.2.6. Analysis by Type of Offering

- 7.2.7. Analysis by Application Area

- 7.2.8. Analysis by End-user

8. COMPANY COMPETITIVENESS ANALYSIS

- 8.1. Chapter Overview

- 8.2. Assumptions and Key Parameters

- 8.3. Methodology

- 8.4. Generative AI Companies in Healthcare: Company Competitiveness Analysis

- 8.4.1. Generative AI Companies based in North America

- 8.4.2. Generative AI Companies based in Europe and Asia-Pacific

SECTION IV: COMPANY PROFILES

9. NORTH AMERICA BASED GENERATIVE AI COMPANIES IN HEALTHCARE

- 9.1. Chapter Overview

- 9.2. Detailed Profiles of Generative AI Companies Based in North America

- 9.2.1. IBM

- 9.2.1.1. Company Overview

- 9.2.1.2. Management Team

- 9.2.1.3. Contact Details

- 9.2.1.4. Financial Performance

- 9.2.1.5. Operating Business Segments

- 9.2.1.6. Generative AI in Healthcare Portfolio

- 9.2.1.7. Recent Developments and Future Outlook

- 9.2.2. Microsoft

- 9.2.3. NVIDIA

- 9.2.4. OpenAI

- 9.2.1. IBM

- 9.3. Short Profiles of Generative AI Companies Based in North America

- 9.3.1. Amazon Web Services

- 9.3.2. C3 AI

- 9.3.3. Google

- 9.3.4. Oracle

- 9.3.5. Syntegra

10. EUROPE AND ASIA-PACIFIC BASED GENERATIVE AI COMPANIES IN HEALTHCARE

- 10.1. Chapter Overview

- 10.2. Detailed Profiles of Generative AI Companies Based in Europe and Asia-Pacific

- 10.2.1. Huma

- 10.2.1.1. Company Overview

- 10.2.1.2. Management Team

- 10.2.1.3. Contact Details

- 10.2.1.4. Generative AI in Healthcare Portfolio

- 10.2.1.5. Recent Developments and Future Outlook

- 10.2.2. LeewayHertz

- 10.2.1. Huma

- 10.3. Short Profiles of Generative AI Companies Based in Europe and Asia-Pacific

- 10.3.1. Exscientia

- 10.3.2. Iktos

- 10.3.3. Medical IP

- 10.3.4. PhamaX

SECTION V: MARKET TRENDS

11. PARTNERSHIPS AND COLLABORATIONS

- 11.1. Chapter Overview

- 11.2. Partnership Models

- 11.3. Generative AI in Healthcare Providers: Partnerships and Collaborations

- 11.3.1. Analysis by Year of Partnership

- 11.3.2. Analysis by Type of Partnership

- 11.3.3. Analysis by Year and Type of Partnership

- 11.3.4. Analysis by Type of Partner Company

- 11.3.5. Analysis by Purpose of Partnership

- 11.3.6. Analysis by Geography

- 11.3.6.1. Local and International Agreements

- 11.3.6.2. Intracontinental and Intercontinental Agreements

- 11.3.7. Most Active Players: Analysis by Number of Partnerships

12. GENERATIVE AI IN HEALTHCARE: USE CASES

- 12.1. Chapter Overview

- 12.2. Use Case 1: Collaboration between NVIDIA and Genentech

- 12.2.1. NVIDIA

- 12.2.2. Genentech

- 12.2.3. Business Needs

- 12.2.4. Objectives Achieved and Solutions Provided

- 12.3. Use Case 2: Collaboration between Insilico Medicine and Inimmune

- 12.3.1. Insilico Medicine

- 12.3.2. Inimmune

- 12.3.3. Business Needs

- 12.3.4. Objectives Achieved and Solutions Provided

- 12.4. Use Case 3: Collaboration between OpenAI and Moderna

- 12.4.1. OpenAI

- 12.4.2. Moderna

- 12.4.3. Business Needs

- 12.4.4. Objectives Achieved and Solutions Provided

- 12.5. Use Case 4: Collaboration between Amazon Web Services and Pfizer

- 12.5.1. Amazon Web Services

- 12.5.2. Pfizer

- 12.5.3. Business Needs

- 12.5.4. Objectives Achieved and Solutions Provided

- 12.6. Use Case 5: Collaboration between Suki and Ascension Saint Thomas

- 12.6.1. Suki

- 12.6.2. Ascension Saint Thomas

- 12.6.3. Business Needs

- 12.6.4. Objectives Achieved and Solutions Offered

- 12.7. Use Case 6: Collaboration between Abridge and Emory Healthcare

- 12.7.1. Abridge

- 12.7.2. Emory Healthcare

- 12.7.3. Business Needs

- 12.7.4. Objectives Achieved and Solutions Offered

- 12.8. Use Case 7: Collaboration between Google and China Medical University Hospital

- 12.8.1. Google

- 12.8.2. China Medical University Hospital

- 12.8.3. Business Needs

- 12.8.4. Objectives Achieved and Solutions Provided

SECTION VI: MARKET OPPORTUNITY ANALYSIS

13. MARKET IMPACT ANALYSIS: DRIVERS, RESTRAINTS, OPPORTUNITIES AND CHALLENGES

- 13.1. Chapter Overview

- 13.2. Market Drivers

- 13.3. Market Restraints

- 13.4. Market Opportunities

- 13.5. Market Challenges

- 13.6. Conclusion

14. GLOBAL GENERATIVE AI IN HEALTHCARE MARKET

- 14.1. Chapter Overview

- 14.2. Key Assumptions and Methodology

- 14.3. Global Generative AI in Healthcare Market, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 14.4. Multivariate Scenario Analysis

- 14.4.1. Conservative Scenario

- 14.4.2. Optimistic Scenario

- 14.5. Key Market Segmentations

15. GENERATIVE AI IN HEALTHCARE MARKET, BY PURPOSE

- 15.1. Chapter Overview

- 15.2. Key Assumptions and Methodology

- 15.3. Generative AI in Healthcare Market: Distribution by Purpose

- 15.3.1. Generative AI in Healthcare Market for Clinical-based Purpose, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 15.3.2. Generative AI in Healthcare Market for System-based Purpose, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 15.4. Data Triangulation and Validation

- 15.4.1. Secondary Sources

- 15.4.2. Primary Sources

16. GENERATIVE AI IN HEALTHCARE MARKET, BY TYPE OF OFFERING

- 16.1. Chapter Overview

- 16.2. Key Assumptions and Methodology

- 16.3. Generative AI in Healthcare Market: Distribution by Type of Offering

- 16.3.1. Generative AI in Healthcare Market for Technology / Platform, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 16.3.2. Generative AI in Healthcare Market for Services, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 16.4. Data Triangulation and Validation

- 16.4.1. Secondary Sources

- 16.4.2. Primary Sources

17. GENERATIVE AI IN HEALTHCARE MARKET, BY APPLICATION AREA

- 17.1. Chapter Overview

- 17.2. Key Assumptions and Methodology

- 17.3. Generative AI in Healthcare Market: Distribution by Application Area

- 17.3.1. Generative AI in Healthcare Market for Drug Discovery and Development, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 17.3.2. Generative AI in Healthcare Market for Diagnosis, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 17.3.3. Generative AI in Healthcare Market for Treatment, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 17.3.4. Generative AI in Healthcare Market for Administrative Tasks, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 17.3.5. Generative AI in Healthcare Market for Other Applications, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 17.4. Data Triangulation and Validation

- 17.4.1. Secondary Sources

- 17.4.2. Primary Sources

18. GENERATIVE AI IN HEALTHCARE MARKET, BY END-USER

- 18.1. Chapter Overview

- 18.2. Key Assumptions and Methodology

- 18.3. Generative AI in Healthcare Market: Distribution by End-user

- 18.3.1. Generative AI in Healthcare Market for Pharmaceutical and Life Science Companies, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 18.3.2. Generative AI in Healthcare Market for Healthcare Providers, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 18.3.3. Generative AI in Healthcare Market for Other End-users, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 18.4. Data Triangulation and Validation

- 18.4.1. Secondary Sources

- 18.4.2. Primary Sources

19. GENERATIVE AI IN HEALTHCARE MARKET, BY GEOGRAPHICAL REGIONS

- 19.1. Chapter Overview

- 19.2. Key Assumptions and Methodology

- 19.3. Generative AI in Healthcare Market: Distribution by Geographical Regions

- 19.3.1. Generative AI in Healthcare Market in North America, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.3.1.1. Generative AI in Healthcare Market in the US, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.3.1.2. Generative AI in Healthcare Market in Canada, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.3.2. Generative AI in Healthcare Market in Europe, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.3.2.1. Generative AI in Healthcare Market in Germany, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.3.2.2. Generative AI in Healthcare Market in the UK, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.3.2.3. Generative AI in Healthcare Market in France, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.3.2.4. Generative AI in Healthcare Market in Spain, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.3.2.5. Generative AI in Healthcare Market in Switzerland, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.3.2.6. Generative AI in Healthcare Market in the Netherlands, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.3.2.7. Generative AI in Healthcare Market in Rest of Europe, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.3.3. Generative AI in Healthcare Market in Asia-Pacific, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.3.3.1. Generative AI in Healthcare Market in China, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.3.3.2. Generative AI in Healthcare Market in Japan, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.3.3.3. Generative AI in Healthcare Market in South Korea, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.3.3.4. Generative AI in Healthcare Market in Singapore, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.3.3.5. Generative AI in Healthcare Market in India, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.3.3.6. Generative AI in Healthcare Market in Rest of Asia-Pacific, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.3.4. Generative AI in Healthcare Market in Middle East and North Africa, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.3.4.1. Generative AI in Healthcare Market in Israel, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.3.4.2. Generative AI in Healthcare Market in UAE, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.3.4.3. Generative AI in Healthcare Market in Rest of Middle East and North Africa, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.3.5. Generative AI in Healthcare Market in Latin America, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.3.5.1. Generative AI in Healthcare Market in Brazil, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.3.5.2. Generative AI in Healthcare Market in Rest of Latin America, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.3.1. Generative AI in Healthcare Market in North America, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035)

- 19.4. Generative AI in Healthcare Market, By Geographical Regions: Market Dynamics Assessment

- 19.4.1. Penetration-Growth (P-G) Matrix

- 19.4.2. Market Movement Analysis

- 19.5. Data Triangulation and Validation

- 19.5.1. Secondary Sources

- 19.5.2. Primary Sources

20. GENERATIVE AI IN HEALTHCARE MARKET, BY LEADING PLAYERS

- 20.1. Chapter Overview

- 20.2. Key Assumptions and Methodology

- 20.3. Generative AI in Healthcare Market: Distribution by Leading Generative AI Companies

- 20.4. Data Triangulation and Validation

21. ADJACENT MARKET ANALYSIS

SECTION VII: STRATEGIC TOOLS

22. PORTER'S FIVE FORCES ANALYSIS

- 22.1. Chapter Overview

- 22.2. Significance of Porter's Five Forces Analysis

- 22.3. Methodology and Assumptions

- 22.4. Porter's Five Forces

- 22.4.1. Threats of New Entrants

- 22.4.2. Bargaining Power of Buyers

- 22.4.3. Bargaining Power of Generative AI Companies

- 22.4.4. Threats of Substitute Products

- 22.4.5. Rivalry Among Existing Competitors

- 22.5. Concluding Remarks

SECTION VIII: OTHER EXCLUSIVE INSIGHTS

23. INSIGHTS FROM PRIMARY RESEARCH

24. CONCLUDING REMARKS

SECTION IX: APPENDIX

25. TABULATED DATA

26. LIST OF COMPANIES AND ORGANIZATIONS

27. CUSTOMIZATION OPPORTUNITIES

28. ROOTS SUBSCRIPTION SERVICES

29. AUTHOR DETAILS

List of Tables

- Table 7.1 Generative AI Companies in Healthcare: Information on Year of Establishment, Company Size and Location of Headquarters

- Table 7.2 Generative AI Companies in Healthcare: Information on Type of Generative AI Company and Type of Offering

- Table 7.3 Generative AI Companies in Healthcare: Information on Application Area

- Table 7.4 Generative AI Companies in Healthcare: Information on End-user

- Table 9.1 Generative AI Companies based in North America: List of Companies Profiled

- Table 9.2 IBM: Company Overview

- Table 9.3 IBM: Generative AI in Healthcare Portfolio

- Table 9.4 IBM: Recent Developments and Future Outlook

- Table 9.5 Microsoft: Company Overview

- Table 9.6 Microsoft: Generative AI in Healthcare Portfolio

- Table 9.7 Microsoft: Recent Developments and Future Outlook

- Table 9.8 NVIDIA: Company Overview

- Table 9.9 NVIDIA: Generative AI in Healthcare Portfolio

- Table 9.10 NVIDIA: Recent Developments and Future Outlook

- Table 9.11 OpenAI: Company Overview

- Table 9.12 OpenAI: Generative AI in Healthcare Portfolio

- Table 9.13 OpenAI: Recent Developments and Future Outlook

- Table 9.14 Amazon Web Services: Company Overview

- Table 9.15 Amazon Web Services: Generative AI in Healthcare Portfolio

- Table 9.16 C3 AI: Company Overview

- Table 9.17 C3 AI: Generative AI in Healthcare Portfolio

- Table 9.18 Google: Company Overview

- Table 9.19 Google: Generative AI in Healthcare Portfolio

- Table 9.20 Oracle: Company Overview

- Table 9.21 Oracle: Generative AI in Healthcare Portfolio

- Table 9.22 Syntegra: Company Overview

- Table 9.23 Syntegra: Generative AI in Healthcare Portfolio

- Table 10.1 Generative AI Companies based in Europe and Asia-Pacific: List of Companies Profiled

- Table 10.2 Huma: Company Overview

- Table 10.3 Huma: Generative AI in Healthcare Portfolio

- Table 10.4 Huma: Recent Developments and Future Outlook

- Table 10.5 LeewayHertz: Company Overview

- Table 10.6 LeewayHertz: Generative AI in Healthcare Portfolio

- Table 10.7 LeewayHertz: Recent Developments and Future Outlook

- Table 10.8 Exscientia: Company Overview

- Table 10.9 Exscientia: Generative AI in Healthcare Portfolio

- Table 10.10 Iktos: Company Overview

- Table 10.11 Iktos: Generative AI in Healthcare Portfolio

- Table 10.12 Medical IP: Company Overview

- Table 10.13 Medical IP: Generative AI in Healthcare Portfolio

- Table 10.14 PhamaX: Company Overview

- Table 10.15 PhamaX: Generative AI in Healthcare Portfolio

- Table 11.1 Generative AI Companies in Healthcare: List of Partnerships and Collaborations, Since 2019

- Table 11.2 Generative AI Companies in Healthcare: Information on Type of Partner Company and Purpose of Partnership

- Table 11.3 Generative AI Companies in Healthcare: Information on Type of Agreement (Country-wise and Region-wise)

- Table 23.1 Absci: Company Overview

- Table 23.2 aiOla: Company Overview

- Table 23.3 Iktos: Company Overview

- Table 25.1 Generative AI Companies in Healthcare: Distribution by Year of Establishment

- Table 25.2 Generative AI Companies in Healthcare: Distribution by Company Size

- Table 25.3 Generative AI Companies in Healthcare: Distribution by Location of Headquarters

- Table 25.4 Generative AI Companies in Healthcare: Distribution by Company Size and Location of Headquarters (Region)

- Table 25.5 Generative AI Companies in Healthcare: Distribution by Type of Generative AI Company

- Table 25.6 Generative AI Companies in Healthcare: Distribution by Type of Offering

- Table 25.7 Generative AI Companies in Healthcare: Distribution by Application Area

- Table 25.8 Generative AI Companies in Healthcare: Distribution by End-user

- Table 25.9 IBM: Annual Revenues, FY 2021 onwards (USD Million)

- Table 25.10 Microsoft: Annual Revenues, FY 2021 onwards (USD Million)

- Table 25.11 NVIDIA: Annual Revenues, FY 2021 onwards (USD Million)

- Table 25.12 Partnerships and Collaborations: Cumulative Year-wise Trend, Since 2019

- Table 25.13 Partnerships and Collaborations: Distribution by Type of Partnership

- Table 25.14 Partnerships and Collaborations: Distribution by Year and Type of Partnership

- Table 25.15 Partnerships and Collaborations: Distribution by Type of Partner Company

- Table 25.16 Partnerships and Collaborations: Distribution by Purpose of Partnership

- Table 25.17 Partnerships and Collaborations: Distribution by Local and International Agreements

- Table 25.18 Partnerships and Collaborations: Distribution by Intracontinental and Intercontinental Agreements

- Table 25.19 Most Active Players: Distribution by Number of Partnerships

- Table 25.20 Global Generative AI in Healthcare Market, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035) (USD Billion)

- Table 25.21 Global Generative AI in Healthcare Market, Forecasted Estimates (Till 2035): Conservative Scenario (USD Billion)

- Table 25.22 Global Generative AI in Healthcare Market, Forecasted Estimates (Till 2035): Optimistic Scenario (USD Billion)

- Table 25.23 Generative AI in Healthcare Market: Distribution by Type of Purpose

- Table 25.24 Generative AI in Healthcare Market for Clinical-based Purpose, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035), Conservative, Base and Optimistic Scenarios (USD Billion)

- Table 25.25 Generative AI in Healthcare Market for System-based Purpose, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035), Conservative, Base and Optimistic Scenarios (USD Billion)

- Table 25.26 Generative AI in Healthcare Market: Distribution by Type of Offering

- Table 25.27 Generative AI in Healthcare Market for Technology / Platform, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035), Conservative, Base and Optimistic Scenarios (USD Billion)

- Table 25.28 Generative AI in Healthcare Market for Services, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035), Conservative, Base and Optimistic Scenarios (USD Billion)

- Table 25.29 Generative AI in Healthcare Market: Distribution by Application Area

- Table 25.30 Generative AI in Healthcare Market for Drug Discovery and Development, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035), Conservative, Base and Optimistic Scenarios (USD Billion)

- Table 25.31 Generative AI in Healthcare Market for Diagnosis, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035), Conservative, Base and Optimistic Scenarios (USD Billion)

- Table 25.32 Generative AI in Healthcare Market for Treatment, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035), Conservative, Base and Optimistic Scenarios (USD Billion)

- Table 25.33 Generative AI in Healthcare Market for Administrative Tasks, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035), Conservative, Base and Optimistic Scenarios (USD Billion)

- Table 25.34 Generative AI in Healthcare Market for Other Applications, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035), Conservative, Base and Optimistic Scenarios (USD Billion)

- Table 25.35 Generative AI in Healthcare Market: Distribution by End-user

- Table 25.36 Generative AI in Healthcare Market for Pharmaceutical and Life Science Companies, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035), Conservative, Base and Optimistic Scenarios (USD Billion)

- Table 25.37 Generative AI in Healthcare Market for Healthcare Providers, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035), Conservative, Base and Optimistic Scenarios (USD Billion)

- Table 25.38 Generative AI in Healthcare Market for Other End-users, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035), Conservative, Base and Optimistic Scenarios (USD Billion)

- Table 25.39 Generative AI in Healthcare Market: Distribution by Key Geographical Regions

- Table 25.40 Generative AI in Healthcare Market in North America, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035), Conservative, Base and Optimistic Scenarios (USD Billion)

- Table 25.41 Generative AI in Healthcare Market in the US, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035), Conservative, Base and Optimistic Scenarios (USD Billion)

- Table 25.42 Generative AI in Healthcare Market in Canada, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035), Conservative, Base and Optimistic Scenarios (USD Billion)

- Table 25.43 Generative AI in Healthcare Market in Europe, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035) (USD Billion), Conservative, Base and Optimistic Scenarios (USD Billion)

- Table 25.44 Generative AI in Healthcare Market in Germany, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035), Conservative, Base and Optimistic Scenarios (USD Billion)

- Table 25.45 Generative AI in Healthcare Market in the UK, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035), Conservative, Base and Optimistic Scenarios (USD Billion)

- Table 25.46 Generative AI in Healthcare Market in France, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035), Conservative, Base and Optimistic Scenarios (USD Billion)

- Table 25.47 Generative AI in Healthcare Market in Spain, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035), Conservative, Base and Optimistic Scenarios (USD Billion)

- Table 25.48 Generative AI in Healthcare Market in Switzerland, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035), Conservative, Base and Optimistic Scenarios (USD Billion)

- Table 25.49 Generative AI in Healthcare Market in the Netherlands, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035), Conservative, Base and Optimistic Scenarios (USD Billion)

- Table 25.50 Generative AI in Healthcare Market in Rest of Europe, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035), Conservative, Base and Optimistic Scenarios (USD Billion)

- Table 25.51 Generative AI in Healthcare Market in Asia-Pacific, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035), Conservative, Base and Optimistic Scenarios (USD Billion)

- Table 25.52 Generative AI in Healthcare Market in China, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035), Conservative, Base and Optimistic Scenarios (USD Billion)

- Table 25.53 Generative AI in Healthcare Market in Japan, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035), Conservative, Base and Optimistic Scenarios (USD Billion)

- Table 25.54 Generative AI in Healthcare Market in South Korea, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035), Conservative, Base and Optimistic Scenarios (USD Billion)

- Table 25.55 Generative AI in Healthcare Market in Singapore, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035), Conservative, Base and Optimistic Scenarios (USD Billion)

- Table 25.56 Generative AI in Healthcare Market in India, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035), Conservative, Base and Optimistic Scenarios (USD Billion)

- Table 25.57 Generative AI in Healthcare Market in Middle East and North Africa, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035), Conservative, Base and Optimistic Scenarios (USD Billion)

- Table 25.58 Generative AI in Healthcare Market in Israel, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035), Conservative, Base and Optimistic Scenarios (USD Billion)

- Table 25.59 Generative AI in Healthcare Market in UAE, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035), Conservative, Base and Optimistic Scenarios (USD Billion)

- Table 25.60 Generative AI in Healthcare Market in Rest of Middle East and North Africa, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035), Conservative, Base and Optimistic Scenarios (USD Billion)

- Table 25.61 Generative AI in Healthcare Market in Latin America, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035), Conservative, Base and Optimistic Scenarios (USD Billion)

- Table 25.62 Generative AI in Healthcare Market in Brazil, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035), Conservative, Base and Optimistic Scenarios (USD Billion)

- Table 25.63 Generative AI in Healthcare Market in Rest of Latin America, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035), Conservative, Base and Optimistic Scenarios (USD Billion)

- Table 25.64 Generative AI in Healthcare Market: Distribution by Leading Generative AI Companies

List of Figures

- Figure 2.1 Research Methodology: Project Methodology

- Figure 2.2 Research Methodology: Data Sources for Secondary Research

- Figure 2.3 Research Methodology: Robust Quality Control

- Figure 3.1 Market Dynamics: Forecast Methodology

- Figure 3.2 Market Dynamics: Market Assessment Framework

- Figure 4.1 Lesson Learnt from Past Recessions

- Figure 5.1 Executive Summary: Market Landscape

- Figure 5.2 Executive Summary: Partnerships and Collaborations

- Figure 5.3 Executive Summary: Market Forecast and Opportunity Analysis

- Figure 6.1 Workflow of Generative AI

- Figure 6.2 Evolution of AI

- Figure 6.3 Applications of Generative AI in Healthcare

- Figure 6.4 Challenges Associated with the Adoption of Generative AI

- Figure 7.1 Generative AI Companies in Healthcare: Distribution by Year of Establishment

- Figure 7.2 Generative AI Companies in Healthcare: Distribution by Company Size

- Figure 7.3 Generative AI Companies in Healthcare: Distribution by Location of Headquarters

- Figure 7.4 Generative AI Companies in Healthcare: Distribution by Company Size and Location of Headquarters (Region)

- Figure 7.5 Generative AI Companies in Healthcare: Distribution by Type of Generative AI Company

- Figure 7.6 Generative AI Companies in Healthcare: Distribution by Type of Offering

- Figure 7.7 Generative AI Companies in Healthcare: Distribution by Application Area

- Figure 7.8 Generative AI Companies in Healthcare: Distribution by End-user

- Figure 8.1 Company Competitiveness Analysis: Generative AI Companies based in North America

- Figure 8.2 Company Competitiveness Analysis: Generative AI Companies based in Europe and Asia-Pacific

- Figure 9.1 IBM: Annual Revenues, FY 2021 onwards (USD Million)

- Figure 9.2 Microsoft: Annual Revenues, FY 2021 onwards (USD Million)

- Figure 9.3 NVIDIA: Annual Revenues, FY 2021 onwards (USD Million)

- Figure 11.1 Partnerships and Collaborations: Cumulative Year-wise Trend, Since 2019

- Figure 11.2 Partnerships and Collaborations: Distribution by Type of Partnership

- Figure 11.3 Partnerships and Collaborations: Distribution by Year and Type of Partnership

- Figure 11.4 Partnerships and Collaborations: Distribution by Type of Partner Company

- Figure 11.5 Partnerships and Collaborations: Distribution by Purpose of Partnership

- Figure 11.6 Partnerships and Collaborations: Distribution by Local and International Agreements

- Figure 11.7 Partnerships and Collaborations: Distribution by Intracontinental and Intercontinental Agreements

- Figure 11.8 Most Active Players: Distribution by Number of Partnerships

- Figure 13.1 Global Generative AI in Healthcare Market, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 13.2 Global Generative AI in Healthcare Market, Forecasted Estimates (Till 2035): Conservative Scenario (USD Billion)

- Figure 13.3 Global Generative AI in Healthcare Market, Forecasted Estimates (Till 2035): Optimistic Scenario (USD Billion)

- Figure 15.1 Generative AI in Healthcare Market: Distribution by Type of Purpose

- Figure 15.2 Generative AI in Healthcare Market for Clinical-based Purpose, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 15.3 Generative AI in Healthcare Market for System-based Purpose, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 16.1 Generative AI in Healthcare Market: Distribution by Type of Offering

- Figure 16.2 Generative AI in Healthcare Market for Technology / Platform, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 16.3 Generative AI in Healthcare Market for Services, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 17.1 Generative AI in Healthcare Market: Distribution by Application Area

- Figure 17.2 Generative AI in Healthcare Market for Drug Discovery and Development, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 17.3 Generative AI in Healthcare Market for Diagnosis, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 17.4 Generative AI in Healthcare Market for Treatment, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 17.5 Generative AI in Healthcare Market for Administrative Tasks, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 17.6 Generative AI in Healthcare Market for Other Applications, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 18.1 Generative AI in Healthcare Market: Distribution by End-user

- Figure 18.2 Generative AI in Healthcare Market for Pharmaceutical and Life Science Companies, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 18.3 Generative AI in Healthcare Market for Healthcare Providers, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 18.4 Generative AI in Healthcare Market for Other End-users, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 19.1 Generative AI in Healthcare Market: Distribution by Key Geographical Regions

- Figure 19.2 Generative AI in Healthcare Market in North America, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 19.3 Generative AI in Healthcare Market in the US, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 19.4 Generative AI in Healthcare Market in Canada, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 19.5 Generative AI in Healthcare Market in Europe, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035) (USD Billion) (USD Billion)

- Figure 19.6 Generative AI in Healthcare Market in Germany, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 19.7 Generative AI in Healthcare Market in the UK, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 19.8 Generative AI in Healthcare Market in France, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 19.9 Generative AI in Healthcare Market in Spain, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 19.10 Generative AI in Healthcare Market in Switzerland, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 19.11 Generative AI in Healthcare Market in the Netherlands, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 19.12 Generative AI in Healthcare Market in Rest of Europe, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 19.13 Generative AI in Healthcare Market in Asia-Pacific, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 19.14 Generative AI in Healthcare Market in China, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 19.15 Generative AI in Healthcare Market in Japan, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 19.16 Generative AI in Healthcare Market in South Korea, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 19.17 Generative AI in Healthcare Market in Singapore, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 19.18 Generative AI in Healthcare Market in India, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 19.19 Generative AI in Healthcare Market in Rest of Asia-Pacific, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 19.20 Generative AI in Healthcare Market in Middle East and North Africa, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 19.21 Generative AI in Healthcare Market in Israel, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 19.22 Generative AI in Healthcare Market in UAE, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 19.23 Generative AI in Healthcare Market in Rest of Middle East and North Africa, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 19.24 Generative AI in Healthcare Market in Latin America, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 19.25 Generative AI in Healthcare Market in Brazil, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 19.26 Generative AI in Healthcare Market in Rest of Latin America, Historical Trends (Since 2019) and Forecasted Estimates (Till 2035) (USD Billion)

- Figure 19.27 Penetration-Growth (P-G) Matrix

- Figure 19.28 Market Movement Analysis

- Figure 20.1 Generative AI in Healthcare Market: Distribution by Leading Generative AI Companies

- Figure 22.1 Porter's Five Forces

- Figure 22.2 Threats of New Entrants: Key Factors

- Figure 22.3 Bargaining Power of Buyers: Key Factors

- Figure 22.4 Bargaining Power of Generative AI Companies: Key Factors

- Figure 22.5 Threats of Substitute Products: Key Factors

- Figure 22.6 Rivalry Among Existing Competitors: Key Factors

- Figure 22.7 Porter's Five Forces Analysis: Concluding Remarks

- Figure 23.1 Concluding Remarks: Market Landscape

- Figure 23.2 Concluding Remarks: Partnerships and Collaborations

- Figure 23.3 Concluding Remarks: Market Forecast and Opportunity Analysis

2026-2034年全球医疗领域生成式人工智慧市场规模、份额、趋势和成长分析报告

2026-2034年全球医疗领域生成式人工智慧市场规模、份额、趋势和成长分析报告 2025-2029年全球製药业生成式人工智慧市场

2025-2029年全球製药业生成式人工智慧市场 医疗保健领域生成式人工智慧市场规模、份额和趋势分析报告:按组件、功能、最终用途、应用、地区和细分市场预测(2025-2033 年)

医疗保健领域生成式人工智慧市场规模、份额和趋势分析报告:按组件、功能、最终用途、应用、地区和细分市场预测(2025-2033 年) 全球医疗保健领域生成式人工智慧市场:预测至 2032 年—按解决方案类型、监管领域、部署方式、组织规模、最终用户和地区进行分析

全球医疗保健领域生成式人工智慧市场:预测至 2032 年—按解决方案类型、监管领域、部署方式、组织规模、最终用户和地区进行分析 2025年医疗保健领域生成式人工智慧全球市场报告

2025年医疗保健领域生成式人工智慧全球市场报告 2025-2029年全球医疗保健市场中的生成人工智慧

2025-2029年全球医疗保健市场中的生成人工智慧 医疗保健市场中的生成式人工智慧机会、成长动力、产业趋势分析和 2025 - 2034 年预测

医疗保健市场中的生成式人工智慧机会、成长动力、产业趋势分析和 2025 - 2034 年预测 医疗保健领域的生成式人工智慧市场:按组件、按功能、按应用、按最终用户、按地区、机会、预测,2017-2031 年

医疗保健领域的生成式人工智慧市场:按组件、按功能、按应用、按最终用户、按地区、机会、预测,2017-2031 年 全球产生人工智慧医疗保健市场规模研究,按应用程式(治疗、诊断、药物发现、研究)、最终用户(医院和诊所、医疗保健组织等)以及 2022-2032 年区域预测

全球产生人工智慧医疗保健市场规模研究,按应用程式(治疗、诊断、药物发现、研究)、最终用户(医院和诊所、医疗保健组织等)以及 2022-2032 年区域预测