|

市场调查报告书

商品编码

2015359

移动机器人市场展望至2035年:产业趋势与全球预测Mobile Robots Market, till 2035: Industry Trends and Global Forecasts |

||||||

移动机器人市场展望

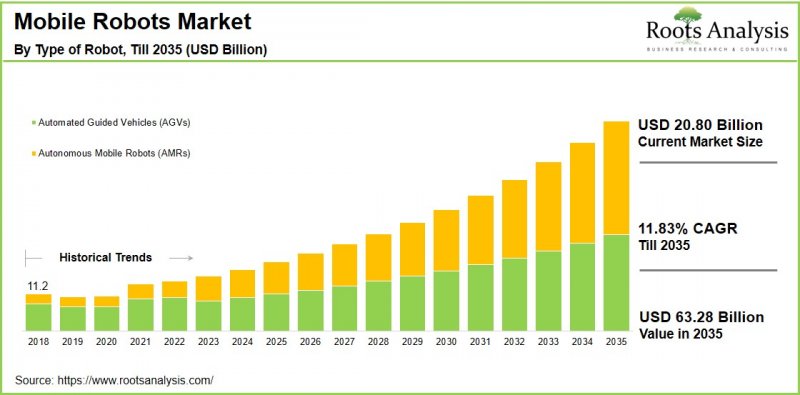

全球移动机器人市场预计到 2035 年将以 11.83% 的复合年增长率成长,达到 632.8 亿美元,高于目前的 207.9 亿美元。

移动机器人代表着一个快速发展的高阶自动化系统领域,其设计目的是在动态环境中自主或半自动执行任务。与固定式机器人系统不同,移动机器人配备了整合式感测器、控制系统和人工智慧演算法,能够实现导航、空间感知、避障和即时决策。这些系统正被广泛应用于製造业、物流业、医疗保健业、农业、国防业和零售业等行业,以提高营运效率和生产力。

在仓库和物流中心,自主移动机器人(AMR)能够简化物料搬运和库存移动;在医疗机构,它们可以协助药品配送和卫生管理;此外,在製造工厂,它们还能支援组装作业和内部运输。它们能够减少人工干预重复性、劳动密集或危险性任务,从而显着提高营运效率和职场安全。在工业自动化日益普及以及人工智慧导航和连接技术的整合应用的推动下,移动机器人市场预计在预测期内将实现显着增长。

为高阶主管提供的策略洞察

移动机器人市场成长的关键市场驱动因素

移动机器人市场的成长主要得益于製造业、物流业和医疗保健产业工业自动化技术的加速应用。企业正越来越多地部署自主移动机器人(AMR),以提高营运效率、减少对人工的依赖并优化工作流程管理。此外,电子商务和仓储自动化的快速发展也显着提升了对智慧物料输送方案的需求。人工智慧和边缘运算等技术的进步进一步提升了移动机器人的导航能力、适应性和安全性,即使在动态环境中也能保持其可靠性。此外,工业4.0的实施和互联基础设施的集成,使得机器人系统与企业平台之间能够实现无缝协作,从而加速了市场扩张。

移动机器人市场:产业内各公司的竞争格局

移动机器人市场的特色是大量企业参与企业,规模大小不一,导致竞争异常激烈,市场动态瞬息万变。全球跨国公司和区域企业都在积极努力提升自身的竞争优势。目前,大型成熟的跨国公司凭藉其广泛的分销网络、强大的技术实力和雄厚的财力,占据市场主导地位。同时,规模较小的製造商则专注于产品创新和客製化,以满足特定应用领域的需求,并提供专业的解决方案。为了扩大市场份额,业内企业正积极推行策略倡议,例如开发先进的机器人技术,以及建立策略联盟和企业发展关係,以拓展伙伴关係和地理覆盖范围。

移动机器人的发展历程-产业新趋势

移动机器人产业正在涌现多个新趋势。其中一个关键趋势是配备人工智慧、机器视觉和先进感测器技术(例如光达)的自主移动机器人(AMR)的日益普及。这使得它们能够在复杂环境中进行精细导航和即时决策。此外,利用工业4.0框架和物联网实现的连接性集成,也进一步促进了机器人、企业系统和云端平台之间的无缝通信,从而提高了营运可视性和协作效率。

此外,我们看到协作机器人正成为一种显着的趋势。这些移动机器人旨在与人类工人安全运作,在提高生产效率的同时保障职场的安全。电子商务的快速发展推动了仓储自动化的扩张,边缘运算技术的日益普及也促进了资料处理速度的提升,这些因素共同塑造了行动机器人产业的演进。

区域分析-亚太地区引领移动机器人市场

我们的分析表明,亚太地区今年将占据最大的市场份额。这主要得益于该地区强大的製造业基础、快速发展的工业自动化以及政府对先进技术的积极支持。中国、日本和韩国等国家在机器人技术应用方面取得了显着进展,这主要得益于高密度的机器人部署、大规模的生产设施以及对智慧工厂的大量投资。此外,该地区电子商务产业的蓬勃发展以及对仓储自动化日益增长的需求,也进一步加速了自主移动机器人在物流和配送中心的部署。

此外,政府推行的有利于工业4.0、数位转型和国内机器人製造的政策,正在增强该地区的竞争力。

移动机器人市场面临的主要挑战

行动机器人普及应用的主要障碍包括采购、系统整合和基础设施升级所需的高额初始投资,这对中小企业而言尤其构成重大阻碍。此外,将行动机器人与现有系统和企业软体整合通常需要先进的技术专长和客製化服务。网路安全、资料隐私和系统可靠性方面的担忧也构成风险,尤其是在机器人透过物联网平台日益互联的情况下。

此外,诸如在快速变化且结构化环境中导航、电池续航能力限制以及维护需求等操作挑战也会影响效能和扩充性。另外,缺乏能够管理和维护先进机器人系统的熟练人员仍然是阻碍因素。

移动机器人市场 - 主要市场区隔

提供

- 硬体

- 软体和服务

机器人类型

- 自动导引运输车(AGV)

- 自主移动机器人(AMR)

负载容量

- 高负载容量(1000公斤或以上)

- 中等负载容量(100-1000公斤)

- 负载容量低(小于100公斤)

导航模式

- SLAM

- QR码

- 磁导航

- 带反射器的雷射器

- 其他的

外形规格

- 升降机/输送机

- 堆高机

- 牵引拖拉机/匕首

- 手提箱/料箱机器人

- 组装机器人

- 其他的

公司类型

- 大公司

- 中小企业

销售管道

- 直销

- 间接销售

- 机器人租赁/RaaS

应用领域

- 製造业

- 后勤

最终用户

- 汽车产业

- 半导体和电子产业

- 物流与电子商务产业

- 製造业和机械业

- 日常消费品(FMCG)产业

- 医疗产业

- 其他的

地区

- 北美洲

- 北美洲

- 亚太地区

- 拉丁美洲

- 中东、非洲等地区

移动机器人市场主要企业范例

- ABB Robotics

- Blue Skye Automation

- Boston Dynamics

- E-COBOT

- Geekplus Technology

- Gideon Brothers

- GreyOrange

- Honda Motor

- iRobot

- Kongsberg Maritime

- Kuka

- Locus Robotics

- Mobile Industrial Robots

- Northrop Grumman

- Omron Group

- SoftBank Robotics

- SuperDroid Robots

- Zebra Fetch Robotics

移动机器人市场:报告范围

这份移动机器人市场报告深入分析了以下几个面向:

- 市场规模和机会分析:这是对移动机器人市场的详细分析,重点关注关键市场细分,例如 [A] 产品类型、[B] 机器人类型、[C]负载容量、[D] 导航模式、[E]外形规格、[F] 企业类型、[G] 分销主要渠道、[H] 应用领域、[I] 最终用户、[J] 主要主要企业和地区。

- 竞争格局:我们根据相关参数(如[A]成立年份、[B]公司规模、[C]总部所在地和[D]所有权结构)对进入移动机器人市场的公司进行全面分析。

- 公司简介:这些是进入移动机器人市场的主要企业的详细简介,提供以下信息:[A] 总部所在地,[B] 公司规模,[C] 企业理念,[D]企业发展区域,[E]经营团队,[F] 联繫方式,[G] 财务信息,[H]业务部门,[I] 产品和技术组合,[J] 展望未来的未来。

- 专利分析:我们根据相关参数(如[A]专利类型、[B]专利公开年份、[C]专利年龄和[D]主要企业)对移动机器人领域已提交和已註册的专利进行深入分析。

目录

第一章:计划概述

第二章:调查方法

第三章 市场动态

第四章 宏观经济指标

第五章执行摘要

第六章:引言

- 移动机器人概述

- 移动机器人类型

- 移动机器人的优势

- 移动机器人的主要应用领域

- 移动机器人的未来发展趋势

第七章 市场概览:主要移动机器人供应商

- 调查方法和关键参数

- 依成立年份进行分析

- 按公司规模分析

- 按总部所在地进行分析

- 机器人类型分析

- 有效载荷支撑分析

- 按应用领域进行分析

- 最终用户分析

第八章:移动机器人市场的Start-Ups生态系统

第九章:公司简介

- ABB

- FANUC

- Geekplus

- iRobot

- KUKA

- Locus Robotics9.11. E-COBOT

- Gideon

- Honda Motor

- Omron

- Siasun

- SoftBank Robotics

- Staubli

- Zebra Technologies

第十章:价值链分析

第十一章:大趋势分析

第十二章:波特五力模型分析

第十三章:全球政策分析

第十四章 市场影响分析

第十五章:全球移动机器人市场

第十六章 透过产品/服务掌握市场机会

第十七章 按机器人类型分類的市场机会

第十八章 以有效载荷分類的市场机会

第十九章 导航模式下的市场机会

第20章 按外形规格的市场机会

第21章 依业务类型分類的市场机会

第22章 按分销管道分類的市场机会

第23章 按应用领域分類的市场机会

第24章 终端用户市场机会

第25章 主要区域的市场机会

- 关键假设和调查方法

- 移动机器人市场(按主要地区划分)

- 北美洲

- 欧洲

- 亚洲

- 拉丁美洲

- 中东、非洲等地区

第26章附录1:表格形式数据

第27章 附录2:公司与组织列表

Mobile Robots Market Outlook

As per Roots Analysis, the global mobile robots market size is estimated to grow from USD 20.79 billion in current year to USD 63.28 billion by 2035, at a CAGR of 11.83% during the forecast period, till 2035.

Mobile robots represent a rapidly evolving segment of advanced automation systems designed to perform tasks autonomously or semi-autonomously while navigating dynamic environments. Unlike fixed robotic systems, mobile robots are equipped with integrated sensors, control systems, and artificial intelligence algorithms that enable movement, spatial awareness, obstacle avoidance, and real-time decision-making. These systems are widely deployed across manufacturing, logistics, healthcare, agriculture, defense, and retail sectors to streamline operations and enhance productivity.

In warehouses and distribution centers, autonomous mobile robots (AMRs) facilitate material handling and inventory movement; in healthcare settings, they support medication delivery and sanitation. Further, in manufacturing environments, they assist with assembly line operations and internal transportation. Their ability to reduce human intervention in repetitive, labor-intensive, or hazardous tasks significantly improves operational efficiency and workplace safety. The mobile robots market is expected to grow significantly during the forecast period. This is due to the growing emphasis on industrial automation and the increasing integration of AI-driven navigation and connectivity technologies.

Strategic Insights for Senior Leaders

Key Drivers Propelling Growth of Mobile Robots Market

The growth of the mobile robots market is primarily driven by the accelerating adoption of industrial automation across manufacturing, logistics, and healthcare sectors. Companies are increasingly deploying autonomous mobile robots (AMRs) to enhance operational efficiency, reduce labor dependency, and optimize workflow management. Additionally, the rapid expansion of e-commerce and warehouse automation has significantly boosted demand for intelligent material handling solutions. Technological advancements, including artificial intelligence, and edge computing have further enhanced the navigation, adaptability, and safety capabilities of mobile robots, making them more reliable in dynamic environments. Moreover, the integration of Industry 4.0 practices and connected infrastructure is enabling seamless coordination between robotic systems and enterprise platforms, thereby accelerating market expansion.

Mobile Robots Market: Competitive Landscape of Companies in this Industry

The mobile robots market is characterized by the presence of numerous small and large players, resulting in intense competition and evolving market dynamics. Both global multinational corporations and regional players are actively working to strengthen their competitive positioning. Currently, major enterprises and established multinational companies hold a dominant share of the market, supported by their extensive distribution networks, technological capabilities, and financial resources. At the same time, small manufacturers are focusing on product innovation and customization to address niche application areas and deliver specialized solutions. To enhance their market presence, industry players are adopting strategic initiatives such as developing advanced robotic technologies, entering into strategic alliances and partnerships to broaden their portfolios and geographic reach.

Mobile Robots Evolution: Emerging Trends in the Industry

The mobile robots industry is witnessing several emerging trends. A key trend is the increasing adoption of autonomous mobile robots (AMRs) equipped with artificial intelligence, machine vision, and advanced sensor technologies such as LiDAR, enabling enhanced navigation, and real-time decision-making in complex environments. The growing integration of Industry 4.0 frameworks and IoT-enabled connectivity is further facilitating seamless communication between robots, enterprise systems, and cloud platforms, improving operational visibility and coordination.

Additionally, there is a notable shift toward collaborative robotics, where mobile robots are designed to safely operate alongside human workers, enhancing productivity while maintaining workplace safety. The expansion of warehouse automation, fueled by the rapid growth of e-commerce, and the rising deployment of edge computing for faster data processing are also shaping the evolution of the mobile robots industry.

Regional Analysis: Asia-Pacific Lead the Mobile Robots Market

According to our analysis, in the current year, the mobile robots market in Asia-Pacific captures the largest share. This is due to its strong manufacturing base, rapid industrial automation, and proactive government support for advanced technologies. Countries such as China, Japan, and South Korea are adopting robotics, driven by high robot density, large-scale production facilities, and significant investments in smart factories. Further, the region's expanding e-commerce sector and the growing demand for warehouse automation have further accelerated the deployment of autonomous mobile robots in logistics and distribution centers.

Additionally, favorable government initiatives promoting Industry 4.0, digital transformation, and domestic robotics manufacturing have strengthened regional competitiveness.

Key Challenges in Mobile Robots Market

Key challenges hindering the adoption of mobile robots include high initial investment required for procurement, system integration, and infrastructure upgrades, which can be particularly challenging for small and medium-sized enterprises. Additionally, the complexity of integrating mobile robots with existing systems and enterprise software often demands significant technical expertise and customization. Concerns related to cybersecurity, data privacy, and system reliability further pose risks, especially as robots become increasingly connected through IoT-enabled platforms.

Further, operational challenges such as navigation in highly dynamic or unstructured environments, battery limitations, and maintenance requirements also impact performance and scalability. Moreover, the shortage of skilled professionals capable of managing and maintaining advanced robotic systems remains a critical constraint for widespread adoption.

Mobile Robots Market: Key Market Segmentation

Type of Offering

- Hardware

- Software and Services

Type of Robot

- Automated Guided Vehicles (AGV)

- Autonomous Mobile Robots (AMR)

Payload

- High Payloads (> 1000 Kgs)

- Medium Payloads (100 to 1000 Kgs)

- Low Payloads (< 100 Kgs)

Navigation Mode

- SLAM

- QR Code

- Magnetic Navigation

- Laser with Reflector

- Others

Form Factor

- Latent Lifts / Conveyors

- Forklifts

- Tow Tractors / Tuggers

- Tote / Bin Robots

- Assembly Robots

- Others

Type of Enterprise

- Large Enterprises

- Small and Medium Enterprises (SMEs)

Distribution Channel

- Direct Sales

- Indirect Sales

- Robot Rental / RaaS

Application Area

- Manufacturing

- Logistics

End-User

- Automotive Industry

- Semiconductor and Electronics Industry

- Logistics and E-commerce Industry

- Manufacturing and Machinery Industry

- FMCG Industry

- Medical Industry

- Others

Geographical Regions

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa, and Rest of the World

Example Players in Mobile Robots Market

- ABB Robotics

- Blue Skye Automation

- Boston Dynamics

- E-COBOT

- Geekplus Technology

- Gideon Brothers

- GreyOrange

- Honda Motor

- iRobot

- Kongsberg Maritime

- Kuka

- Locus Robotics

- Mobile Industrial Robots

- Northrop Grumman

- Omron Group

- SoftBank Robotics

- SuperDroid Robots

- Zebra Fetch Robotics

Mobile Robots Market: Report Coverage

The report on the mobile robots market features insights on various sections, including:

- Market Sizing and Opportunity Analysis: An in-depth analysis of the mobile robots market, focusing on key market segments, including [A] type of offering, [B] type of robot, [C] payload, [D] navigation mode, [E] form factor, [F] type of enterprise, [G] distribution channel, [H] application area, [I] end-user, [J] geographical regions and [K] key players.

- Competitive Landscape: A comprehensive analysis of the companies engaged in the mobile robots market, based on several relevant parameters, such as [A] year of establishment, [B] company size, [C] location of headquarters and [D] ownership structure.

- Company Profiles: Elaborate profiles of prominent players engaged in the mobile robots market, providing details on [A] location of headquarters, [B] company size, [C] company mission, [D] company footprint, [E] management team, [F] contact details, [G] financial information, [H] operating business segments, [I] product / technology portfolio, [J] recent developments, and an informed future outlook.

- Patent Analysis: An insightful analysis of patents filed / granted in the mobile robots domain, based on relevant parameters, including [A] type of patent, [B] patent publication year, [C] patent age and [D] leading players.

Key Questions Answered in this Report

- What is the current and future market size?

- Who are the leading companies in this market?

- What are the growth drivers that are likely to influence the evolution of this market?

- What are the key partnership and funding trends shaping this industry?

- Which region is likely to grow at higher CAGR till 2035?

- How is the current and future market opportunity likely to be distributed across key market segments?

Reasons to Buy this Report

- Detailed Market Analysis: The report provides a comprehensive market analysis, offering detailed revenue projections of the overall market and its specific sub-segments. This information is valuable to both established market leaders and emerging entrants.

- In-depth Analysis of Trends: Stakeholders can leverage the report to gain a deeper understanding of the competitive dynamics within the market. Each report maps ecosystem activity across partnerships, funding, and patent landscapes to reveal growth hotspots and white spaces in the industry.

- Opinion of Industry Experts: The report features extensive interviews and surveys with key opinion leaders and industry experts to validate market trends mentioned in the report.

- Decision-ready Deliverables: The report offers stakeholders with strategic frameworks (Porter's Five Forces, value chain, SWOT), and complimentary Excel / slide packs with customization support.

Additional Benefits

- Complimentary Dynamic Excel Dashboards for Analytical Modules

- Exclusive 15% Free Content Customization

- Personalized Interactive Report Walkthrough with Our Expert Research Team

- Free Report Updates for Versions Older than 6-12 Months

TABLE OF CONTENTS

1. PROJECT OVERVIEW

- 1.1. Context

- 1.2. Project Objectives

2. RESEARCH METHODOLOGY

- 2.1. Chapter Overview

- 2.2. Research Assumptions

- 2.2.1. Market Landscape and Market Trends

- 2.2.2. Market Forecast and Opportunity Analysis

- 2.2.3. Comparative Analysis

- 2.3. Database Building

- 2.3.1. Data Collection

- 2.3.2. Data Validation

- 2.3.3. Data Analysis

- 2.4. Project Methodology

- 2.4.1. Secondary Research

- 2.4.1.1. Annual Reports

- 2.4.1.2. Academic Research Papers

- 2.4.1.3. Company Websites

- 2.4.1.4. Investor Presentations

- 2.4.1.5. Regulatory Filings

- 2.4.1.6. White Papers

- 2.4.1.7. Industry Publications

- 2.4.1.8. Conferences and Seminars

- 2.4.1.9. Government Portals

- 2.4.1.10. Media and Press Releases

- 2.4.1.11. Newsletters

- 2.4.1.12. Industry Databases

- 2.4.1.13. Roots Proprietary Databases

- 2.4.1.14. Paid Databases and Sources

- 2.4.1.15. Social Media Portals

- 2.4.1.16. Other Secondary Sources

- 2.4.2. Primary Research

- 2.4.2.1. Types of Primary Research

- 2.4.2.1.1. Qualitative Research

- 2.4.2.1.2. Quantitative Research

- 2.4.2.1.3. Hybrid Approach

- 2.4.2.2. Advantages of Primary Research

- 2.4.2.3. Techniques for Primary Research

- 2.4.2.3.1. Interviews

- 2.4.2.3.2. Surveys

- 2.4.2.3.3. Focus Groups

- 2.4.2.3.4. Observational Research

- 2.4.2.3.5. Social Media Interactions

- 2.4.2.4. Key Opinion Leaders Considered in Primary Research

- 2.4.2.4.1. Company Executives (CXOs)

- 2.4.2.4.2. Board of Directors

- 2.4.2.4.3. Company Presidents and Vice Presidents

- 2.4.2.4.4. Research and Development Heads

- 2.4.2.4.5. Technical Experts

- 2.4.2.4.6. Subject Matter Experts

- 2.4.2.4.7. Scientists

- 2.4.2.4.8. Doctors and Other Healthcare Providers

- 2.4.2.5. Ethics and Integrity

- 2.4.2.5.1. Research Ethics

- 2.4.2.5.2. Data Integrity

- 2.4.2.1. Types of Primary Research

- 2.4.3. Analytical Tools and Databases

- 2.4.1. Secondary Research

- 2.5. Robust Quality Control

3. MARKET DYNAMICS

- 3.1. Chapter Overview

- 3.2. Forecast Methodology

- 3.2.1. Top-down Approach

- 3.2.2. Bottom-up Approach

- 3.2.3. Hybrid Approach

- 3.3. Market Assessment Framework

- 3.3.1. Total Addressable Market (TAM)

- 3.3.2. Serviceable Addressable Market (SAM)

- 3.3.3. Serviceable Obtainable Market (SOM)

- 3.3.4. Currently Acquired Market (CAM)

- 3.4. Forecasting Tools and Techniques

- 3.4.1. Qualitative Forecasting

- 3.4.2. Correlation

- 3.4.3. Regression

- 3.4.4. Extrapolation

- 3.4.5. Convergence

- 3.4.6. Sensitivity Analysis

- 3.4.7. Scenario Planning

- 3.4.8. Data Visualization

- 3.4.9. Time Series Analysis

- 3.4.10. Forecast Error Analysis

- 3.5. Key Considerations

- 3.5.1. Demographics

- 3.5.2. Government Regulations

- 3.5.3. Reimbursement Scenarios

- 3.5.4. Market Access

- 3.5.5. Supply Chain

- 3.5.6. Industry Consolidation

- 3.5.7. Pandemic / Unforeseen Disruptions Impact

- 3.6. Limitations

4. MACRO-ECONOMIC INDICATORS

- 4.1. Chapter Overview

- 4.2. Market Dynamics

- 4.2.1. Time Period

- 4.2.1.1. Historical Trends

- 4.2.1.2. Current and Forecasted Estimates

- 4.2.2. Currency Coverage

- 4.2.2.1. Major Currencies Affecting the Market

- 4.2.2.2. Factors Affecting Currency Fluctuations

- 4.2.2.3. Impact of Currency Fluctuations on the Industry

- 4.2.3. Foreign Currency Exchange Rate

- 4.2.3.1. Impact of Foreign Exchange Rate Volatility on the Market

- 4.2.3.2. Strategies for Mitigating Foreign Exchange Risk

- 4.2.4. Recession

- 4.2.4.1. Assessment of Current Economic Conditions and Potential Impact on the Market

- 4.2.4.2. Historical Analysis of Past Recessions and Lessons Learnt

- 4.2.5. Inflation

- 4.2.5.1. Measurement and Analysis of Inflationary Pressures in the Economy

- 4.2.5.2. Potential Impact of Inflation on the Market Evolution

- 4.2.6. Interest Rates

- 4.2.6.1. Interest Rates and Their Impact on the Market

- 4.2.6.2. Strategies for Managing Interest Rate Risk

- 4.2.7. Commodity Flow Analysis

- 4.2.7.1. Type of Commodity

- 4.2.7.2. Origins and Destinations

- 4.2.7.3. Value and Weights

- 4.2.7.4. Modes of Transportation

- 4.2.8. Global Trade Dynamics

- 4.2.8.1. Import Scenario

- 4.2.8.2. Export Scenario

- 4.2.8.3. Trade Policies

- 4.2.8.4. Strategies for Mitigating the Risks Associated with Trade Barriers

- 4.2.8.5. Impact of Trade Barriers on the Market

- 4.2.9. War Impact Analysis

- 4.2.9.1. Russian-Ukraine War

- 4.2.9.2. Israel-Hamas War

- 4.2.10. COVID Impact / Related Factors

- 4.2.10.1. Global Economic Impact

- 4.2.10.2. Industry-specific Impact

- 4.2.10.3. Government Response and Stimulus Measures

- 4.2.10.4. Future Outlook and Adaptation Strategies

- 4.2.11. Other Indicators

- 4.2.11.1. Fiscal Policy

- 4.2.11.2. Consumer Spending

- 4.2.11.3. Gross Domestic Product (GDP)

- 4.2.11.4. Employment

- 4.2.11.5. Taxes

- 4.2.11.6. Stock Market Performance

- 4.2.11.7. Cross-Border Dynamics

- 4.2.1. Time Period

- 4.3. Conclusion

5. EXECUTIVE SUMMARY

6. INTRODUCTION

- 6.1. Overview of the Mobile Robots

- 6.2. Types of Mobile Robots

- 6.3. Advantages of Mobile Robots

- 6.4. Key Application Areas of Mobile Robots

- 6.5. Future Trends in Mobile Robots

7. MARKET LANDSCAPE: LEADING MOBILE ROBOTS PROVIDERS

- 7.1. Methodology and Key Parameters

- 7.2. Analysis by Year of Establishment

- 7.3. Analysis by Company Size

- 7.4. Analysis by Location of Headquarters

- 7.5. Analysis by Type of Robot

- 7.6. Analysis by Payload Supported

- 7.7. Analysis by Application Area

- 7.8. Analysis by End-User

8. STARTUP ECOSYSTEM IN THE MOBILE ROBOTS MARKET

- 8.1. Methodology and Key Parameters

- 8.2. Analysis by Year of Establishment

- 8.3. Analysis by Company Size

- 8.4. Analysis by Location of Headquarters

- 8.5. Analysis by Type of Robot

- 8.6. Analysis by Number of Robots Offered

- 8.7. Analysis by Payload Capacity

- 8.8. Analysis by Application Area

- 8.9. Analysis by Navigation Sensor

9. COMPANY PROFILES

- 9.1. ABB

- 9.1.1. Company Overview

- 9.1.2. Management Team

- 9.1.3. Mobile Robots Portfolio

- 9.1.4. Recent Developments and Future Outlook

- Similar details are presented for other below mentioned companies based on information in the public domain

- 9.2. FANUC

- 9.3. Geekplus

- 9.4. iRobot

- 9.5. KUKA

- 9.6. Locus Robotics9.11. E-COBOT

- 9.12. Gideon

- 9.13. Honda Motor

- 9.14. Omron

- 9.15. Siasun

- 9.16. SoftBank Robotics

- 9.17. Staubli

- 9.18. Zebra Technologies

10. VALUE CHAIN ANALYSIS

11. MEGA TRENDS ANALYSIS

12. PORTER'S FIVE FORCES ANALYSIS

13. GLOBAL POLICY ANALYSIS

14. MARKET IMPACT ANALYSIS

15. GLOBAL MOBILE ROBOTS MARKET

- 15.1. Key Assumptions and Methodology

- 15.2. Global Mobile Robots Market, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 15.2.1. Scenario Analysis

- 15.2.1.1. Conservative Scenario

- 15.2.1.2. Optimistic Scenario

- 15.2.1. Scenario Analysis

- 15.3. Key Market Segmentations

16. MARKET OPPORTUNITIES BASED ON TYPE OF OFFERING

- 16.1. Key Assumptions and Methodology

- 16.2. Mobile Robots Market, by Type of Offering

- 16.2.1. Mobile Robots Market for Hardware, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 16.2.2. Mobile Robots Market for Software and Services, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

17. MARKET OPPORTUNITIES BASED ON TYPE OF ROBOT

- 17.1. Key Assumptions and Methodology

- 17.2. Mobile Robots Market, by Type of Robot

- 17.2.1. Mobile Robots Market for Automated Guided Vehicles (AGV), Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 17.2.2. Mobile Robots Market for Autonomous Mobile Robots (AMR), Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

18. MARKET OPPORTUNITIES BASED ON PAYLOAD

- 18.1. Key Assumptions and Methodology

- 18.2. Mobile Robots Market, by Payload

- 18.2.1. Mobile Robots Market for High Payloads (>1000 Kgs), Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 18.2.2. Mobile Robots Market for Medium Payloads (100 to 1000 Kgs), Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 18.2.3. Mobile Robots Market for Small Payloads (<100 Kgs), Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

19. MARKET OPPORTUNITIES BASED ON NAVIGATION MODE

- 19.1. Key Assumptions and Methodology

- 19.2. Mobile Robots Market, by Navigation Mode

- 19.2.1. Mobile Robots Market for SLAM, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 19.2.2. Mobile Robots Market for QR Code, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 19.2.3. Mobile Robots Market for Magnetic Navigation, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 19.2.4. Mobile Robots Market for Laser with Reflector, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 19.2.5. Mobile Robots Market for Others, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

20. MARKET OPPORTUNITIES BASED ON FORM FACTOR

- 20.1. Key Assumptions and Methodology

- 20.2. Mobile Robots Market, by Form Factor

- 20.2.1. Mobile Robots Market for Latent Lifts / Conveyors, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 20.2.2. Mobile Robots Market for Forklifts, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 20.2.3. Mobile Robots Market for Tow Tractors / Tuggers, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 20.2.4. Mobile Robots Market for Tote / Bin Robots, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 20.2.5. Mobile Robots Market for Assembly Robots, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 20.2.6. Mobile Robots Market for Others, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

21. MARKET OPPORTUNITIES BASED ON TYPE OF ENTERPRISE

- 21.1. Key Assumptions and Methodology

- 21.2. Metamaterials Market, by Type of Enterprise

- 21.2.1. Metamaterials Market for Large Enterprises, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 21.2.2. Metamaterials Market for Small and Medium Enterprises, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

22. MARKET OPPORTUNITIES BASED ON DISTRIBUTION CHANNEL

- 22.1. Key Assumptions and Methodology

- 22.2. Metamaterials Market, by Distribution Channel

- 22.2.1. Metamaterials Market for Direct Sales, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.2.2. Metamaterials Market for Indirect Sales, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 22.2.3. Metamaterials Market for Robot Rental / RaaS, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

23. MARKET OPPORTUNITIES BASED ON APPLICATION AREA

- 23.1. Key Assumptions and Methodology

- 23.2. Metamaterials Market, by Application Area

- 23.2.1. Metamaterials Market for Manufacturing, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 23.2.2. Metamaterials Market for Logistics, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

24. MARKET OPPORTUNITIES BASED ON END-USER

- 24.1. Key Assumptions and Methodology

- 24.2. Mobile Robots Market, by End-User

- 24.2.1. Mobile Robots Market for Semiconductor and Electronics Industry, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 24.2.2. Mobile Robots Market for Logistics and E-commerce Industry, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 24.2.3. Mobile Robots Market for Automotive Industry, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 24.2.4. Mobile Robots Market for Manufacturing and Machinery Industry, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 24.2.5. Mobile Robots Market for FMCG Industry, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 24.2.6. Mobile Robots Market for Medical Industry, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 24.2.6. Mobile Robots Market for Others, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

25. MARKET OPPORTUNITIES BASED ON KEY GEOGRAPHICAL REGIONS

- 25.1. Key Assumptions and Methodology

- 25.2. Mobile Robots Market, by Key Geographical Regions

- 25.2.1. Mobile Robots Market in North America, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 25.2.1.1. Mobile Robots Market in the US, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 25.2.1.2. Mobile Robots Market in Canada, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 25.2.1.3. Mobile Robots Market in Mexico, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 25.2.1.4. Mobile Robots Market in Rest of North America, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 25.2.2. Mobile Robots Market in Europe, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 25.2.2.1. Mobile Robots Market in Germany, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 25.2.2.2. Mobile Robots Market in Italy, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 25.2.2.3. Mobile Robots Market in France, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 25.2.2.4. Mobile Robots Market in Spain, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 25.2.2.5. Mobile Robots Market in Turkey, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 25.2.2.6. Mobile Robots Market in the UK, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 25.2.2.7. Mobile Robots Market in Rest of Europe, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 25.2.3. Mobile Robots Market in Asia, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 25.2.3.1. Mobile Robots Market in China, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 25.2.3.2. Mobile Robots Market in Japan, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 25.2.3.3. Mobile Robots Market in South Korea, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 25.2.3.4. Mobile Robots Market in Taiwan, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 25.2.3.5. Mobile Robots Market in Singapore, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 25.2.3.6. Mobile Robots Market in India, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 25.2.3.7. Mobile Robots Market in Thailand, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 25.2.3.8. Mobile Robots Market in Rest of Asia, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 25.2.4. Mobile Robots Market in Latin America, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 25.2.4.1. Mobile Robots Market in Brazil, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 25.2.4.2. Mobile Robots Market in Rest of Latin America, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 25.2.5. Mobile Robots Market in Middle East and Africa and Rest of the World, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 25.2.5.1. Mobile Robots Market in North Africa, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 25.2.5.2. Mobile Robots Market in South Africa, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 25.2.5.3. Mobile Robots Market in Rest of Middle East and Africa, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 25.2.5.4. Mobile Robots Market in Rest of the World, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

- 25.2.1. Mobile Robots Market in North America, Historical Trends (Since 2018) and Forecasted Estimates (Till 2035)

26. APPENDIX 1: TABULATED DATA

27. APPENDIX 2: LIST OF COMPANIES AND ORGANIZATIONS

2026年全球移动机器人市场报告2026年全球移动机器人软体市场报告

2026年全球移动机器人市场报告2026年全球移动机器人软体市场报告 行动控制机器人市场 - 全球产业规模、份额、趋势、机会、预测:按类型、产品、应用、地区和竞争格局划分,2021-2031年

行动控制机器人市场 - 全球产业规模、份额、趋势、机会、预测:按类型、产品、应用、地区和竞争格局划分,2021-2031年 移动机器人:市场占有率分析、产业趋势与统计、成长预测(2026-2031)移动机器人市场-全球产业规模、份额、趋势、机会和预测(按类型、应用、地区和竞争格局划分,2020-2030 年预测)

移动机器人:市场占有率分析、产业趋势与统计、成长预测(2026-2031)移动机器人市场-全球产业规模、份额、趋势、机会和预测(按类型、应用、地区和竞争格局划分,2020-2030 年预测) 全球移动机器人市场 - 预测 2025-2030

全球移动机器人市场 - 预测 2025-2030 移动机器人市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

移动机器人市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 移动机器人市场规模、份额和成长分析(按机器人类型、有效载荷、最终用途和地区)- 产业预测 2025-2032

移动机器人市场规模、份额和成长分析(按机器人类型、有效载荷、最终用途和地区)- 产业预测 2025-2032 全球移动机器人市场:市场规模、份额、趋势分析(按组件、产品、应用和地区)、细分市场预测(2025-2030 年)

全球移动机器人市场:市场规模、份额、趋势分析(按组件、产品、应用和地区)、细分市场预测(2025-2030 年) 行动机器人充电站的全球市场:产业分析,规模,占有率,成长,趋势,预测(2024年~2031年)

行动机器人充电站的全球市场:产业分析,规模,占有率,成长,趋势,预测(2024年~2031年)