|

市场调查报告书

商品编码

1286721

氧化物基全固态电池技术趋势及市场前景<2023> Oxide-based Solid-state Battery Technology Trends and Market Outlook |

||||||

预计2030年全固态电池整体市场规模将增长至149GWh,2035年将增长至950GWh,占电池市场总量的10%。 其中,使用氧化物固体电解质的全固态电池分为大块型、小型薄膜型和层压型。 预计将针对xEV开发散装型,但由于实际应用存在较高的技术壁垒,目前预计将用作WeLion和半固态电池等混合动力电池,并预计在2030年左右投入使用。到2035 年,发电量将从27GWh 增长到约87GWh。

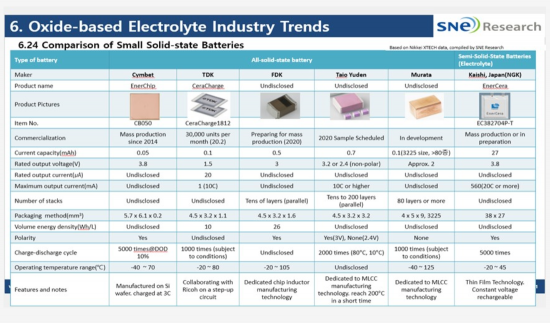

下表总结了目前商业化或正在准备的使用氧化物固体电解质的电池的製造商和规格。 其中大部分已被MLCC技术实力雄厚的日本公司商业化。

另一方面,最近有人尝试在xEV中采用使用氧化物基固体电解质的电池,中国的WeLion开发了一种使用石榴石和NASICON型氧化物的混合电池,并进行了安全测试。据报导,已获批准,将采用蔚来的150kWh电池组。 WeLion目前正在建设一条产能2GWh的大型生产线。

本报告调查了氧化物基全固态电池市场,详细介绍了无机固体电解质的概况和技术,以及氧化物固体电解质面临的主要挑战以及旨在解决这些问题的研发现状.. 我们还提供有关氧化物电池商业化公司的最新趋势和製造工艺以及重要专利的信息。

此报告的特点

氧化物固体电解质技术含量丰富

- 1. 氧化物固体电解质的研发现状、主要挑战及解决方案

- 2.氧化物基固体电解质製造工艺技术

- 3.氧化物电解液行业主要企业趋势及技术

- 4.氧化物固体电解质的市场前景

- 5.氧化物固体电解质相关主要企业专利分析

The performance of lithium-ion batteries (LIBs) has improved dramatically, especially in energy density, due to continuous technology development driven by the explosive demand for new electronics and electric vehicles. However, high energy density also poses the risk of fire or explosion, and explosive reactions can occur due to mechanical damage, over-discharge, electrical faults from overcharging, internal overheating, and secondary heat dissipation caused by external factors.

To prevent these risks, solid-state batteries are emerging as the next-generation battery technology that uses solid-state electrolytes. Solid-state batteries have the advantages of excellent safety, high energy density, high power output, and wide operating temperature range, and are free from the risk of explosion, while solid-state electrolytes have better ionic conductivity than liquid electrolytes at low temperatures below 0°C and high temperatures between 60~100°C.

Solid-state electrolytes, the most essential part of a solid-state battery, are divided into polymer-based and ceramic-based electrolytes, and ceramic-based electrolytes are further categorized into sulfide-based and oxide-based electrolytes. This report will discuss oxide-based solid-state electrolytes among ceramic-based solid-state electrolytes.

The full-scale development of oxide-based solid electrolytes began with the development of LiPON in 1992, which has the advantages of stable contact with lithium metal, a wide electrochemical window (0-5.5 V vs. Li/Li+), and negligible electrical conductivity. Therefore, LiPON was widely used as a reference electrolyte in the R&D of thin-film solid-state lithium batteries. However, it was only suitable for use as a thin-film electrolyte due to its low ionic conductivity (about 10-6 S/cm at 25°C) and was too fragile for application to large-scale batteries.

In 1993, perovskite-type LLTO (Li0.5La0.5TiO3) was developed, showing an ionic conductivity of over 2x10-5 S/cm, and in 1997, NASICON-type inorganic solid electrolytes including LAGP (Li1+xAlxGe2-x(PO4)3) and LATP (Li1+xAlxTi2-x(PO4)3) were first developed, showing high ionic conductivities of 10-4 S/cm and 1.3x10-3 S/cm, respectively. In 2007, a garnet-type ionic conductor LLZO (Li7La3Zr2O12) was first reported, which exhibited an excellent ionic conductivity of 3x10-4 S/cm at room temperature and excellent thermal and chemical stability, showing potential for application in solid-state lithium batteries.

Solid-state batteries with oxide solid electrolytes are still used as low-capacity power sources for IoT and small electronic devices because they need to be sintered at high temperatures, have low ionic conductivity, and are difficult to scale up, and the method using multilayer ceramic capacitor (MLCC) manufacturing technology is widely used.

The table below summarizes the manufacturers and specifications of cells with oxide-based solid electrolytes that are currently commercialized and in preparation. Most of them are commercialized by Japanese companies, which are strong in MLCC technology.

Meanwhile, attempts to use batteries with oxide-based solid electrolytes for xEVs have also been made recently, and WeLion, a Chinese company, has developed a hybrid battery using Garnet and NASICON-based oxides, which has passed safety tests and is reported to be used in the NIO 150kWh battery pack. WeLion is currently building a large-scale manufacturing line with a capacity of 2GWh.

The overall market outlook for solid-state batteries is expected to grow to 149 GWh in 2030 and 950 GWh in 2035, accounting for 10% of the total battery market. Among them, solid-state batteries with oxide solid electrolytes are divided into large bulk type and small thin-film and laminated types. The bulk type is expected to be developed for xEVs, but due to high technical barriers to commercialization, it is currently expected to be used as a hybrid or quasi solid battery like WeLion and is expected to grow from about 27 GWh in 2030 to about 87 GWh in 2035.

This report, in addition to dealing with the overall overview and technology of inorganic solid electrolytes, also summarizes the key issues related to oxide solid electrolytes and the research and development status for solving them in detail. It also covers the latest trends and manufacturing processes of companies that are commercializing oxide batteries, and finally conducts a survey and analysis of important patents. This report will be a great help to readers who want to know the status, technology flow, and market of oxide solid electrolytes and batteries that apply them.

Strong Points of this Report :

Technically rich content on oxide-based solid-state electrolytes:

- 1. Research and development status, major issues, and solutions for oxide-based solid-state electrolytes

- 2. Manufacturing process technology of oxide-based solid-state batteries

- 3. Trends and technologies of major players in the oxide-based electrolyte industry

- 4. Market outlook for oxide-based solid-state electrolytes

- 5. Patent analysis of major players related to oxide-based solid-state batteries

固体电解质-市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)

固体电解质-市场占有率分析、产业趋势与统计、成长预测(2025-2030 年) 2030年3D列印电池市场预测:按电池类型、电池成分、产品类型、生产规模、3D列印技术、最终用户和地区进行的全球分析2030 年固体电解质市场预测:按类型、形式、分销管道、应用、最终用户和地区进行的全球分析

2030年3D列印电池市场预测:按电池类型、电池成分、产品类型、生产规模、3D列印技术、最终用户和地区进行的全球分析2030 年固体电解质市场预测:按类型、形式、分销管道、应用、最终用户和地区进行的全球分析 锂离子电池用卤化物固态电解质:专利情形分析(2024年)

锂离子电池用卤化物固态电解质:专利情形分析(2024年) 全球固态电解质市场2024-2031

全球固态电解质市场2024-2031 固体电解质:全球与区域市场分析(2023-2033)

固体电解质:全球与区域市场分析(2023-2033) 全球3D打印电池市场研究报告 - 行业分析、规模、份额、增长、趋势及2023年至2030年预测

全球3D打印电池市场研究报告 - 行业分析、规模、份额、增长、趋势及2023年至2030年预测 固体电解质市场 - 2023-2031 年全球行业分析、规模、份额、增长、趋势和预测

固体电解质市场 - 2023-2031 年全球行业分析、规模、份额、增长、趋势和预测