|

市场调查报告书

商品编码

1700502

工业机械健康监测:2029 年的机会与预测Industrial Machine Health Monitoring: Opportunities & Forecasts Through 2029 |

||||||

随着工业营运商扩大采用由 IIoT 支援的数据驱动策略,他们优先投资于监控其营运设备健康状况的解决方案。透过持续监测压缩机、变速箱、马达、泵浦和其他工业机械的状况和性能,製造商和其他工业运营商可以製定和管理维护策略,以帮助最大限度地提高正常运行时间和生产产量。因此,将感测硬体、即时监控功能和进阶分析(如预测模型)整合到完整的端到端解决方案中的工业机器健康监控解决方案正在成为企业寻求营运效率和优化的关键工具。

本报告研究了全球工业机器健康监测解决方案市场,并按地区、销售管道和行业垂直提供分析和预测。

它将回答哪些问题?

- 工业机械健康监测解决方案的市场规模是多少?

- 未来五年哪些地区和产业将推动成长?

- OT、IT 和 IoT 的整合如何塑造这个市场?

- 哪些工业自动化供应商最积极支持机器健康计画?

- 网路安全问题如何影响这些解决方案的采用和实施?

本报告中介绍的供应商

|

|

|

感测技术的不断成熟是该市场早期阶段的一个基本成长因素。展望未来,工业人工智慧的出现和成熟有望成为市场最重要的技术成长动力之一。

市场多种多样,包括机器健康新创公司、成熟的工业技术供应商、工业零件供应商和全球工业自动化巨头。Augury、i-care 和 KCF Technologies 等专业机器健康提供者在早期阶段创造强劲需求方面尤为成功。从解决方案的角度来看,该市场的竞争对手分为以下几类:销售感测器的公司、销售感测器并透过服务合约提供手动诊断和建议的公司、销售感测器并利用人工智慧提供自动诊断和建议的公司。除了主要供应商之外,该市场的竞争格局还充满了各种专注于特定地区、产业或机器健康监测的利基竞争对手。

预计到 2024 年,食品和饮料产业将成为市场最大的收入驱动力。这主要是因为该行业的设施内有大量机器。食品和饮料行业的营运环境相对易于监控且不太复杂,这使得实施系统和节省成本变得更加容易。同时,预计到2029年,能源和发电产业将成为成长最快的工业产业。这是因为公司的环境、社会和治理 (ESG) 目标迫使他们解决碳排放和能源管理方面的要求。此外,汽车製造商和零件供应商也预计在预测期内大幅推动市场成长。

目录

将会涉及哪些问题?

谁该阅读这份报告?

本报告中介绍的供应商

执行摘要

- 主要发现

世界市场概览

- 市场概况

- 市场驱动力和策略

- 推动数位转型的劳动课题

- 感测器成熟度和互通性要求将塑造市场

竞争格局

- 概述

- 任务

- 透过收购获得市场占有率

- 增加一线工人的支持

- 扩展您的部署并适应不断变化的客户需求

- 机会

- 人工智慧解谜

- 实现跨 OT 堆迭的集成

- 寻求合作伙伴关係以进入新市场

全球市场:按细分市场

- 区域市场和预测

- 概述

- 工业化创造市场机遇

- 各行业市场及预测

- 概述

- 产业孤岛限制了市场成长

- 监控技术市场预测

- 概述

- 机器知识的限制阻碍了替代技术

- 各通路市场预测

- 概述

- 最终用户对 OEM 解决方案持谨慎态度

供应商亮点

- Advanced Technology Services (ATS)

- AssetWatch

- Augury

- I-care

- KCF Technologies

- 其他

- Bently Nevada

- Emerson

- MaintainX

- TRACTIAN

- Waites

关于作者

Inside this Report

As industrial organizations increasingly embrace the data-driven strategies enabled by the Industrial Internet of Things (IIoT), many have prioritized investments in solutions that monitor the health of their operational equipment. By continuously monitoring the status and performance of compressors, gear boxes, motors, pumps, and other industrial machinery, manufacturers and other industrial operators can develop and manage maintenance strategies that help maximize production uptime and output. As such, industrial machine health monitoring solutions - which combine sensing hardware, real-time monitoring capabilities, and advanced analytics (e.g., predictive modeling) within a complete, end-to-end solution - have emerged as critical tools in these organizations' pursuit of operational efficiency and optimization. This report covers the global market for industrial machine health monitoring solutions, including segmentations and forecasts by geographic region, channel, and industry.

What Questions are Addressed?

- How large is the market for industrial machine health solutions?

- Which regions and industries will drive growth over the next five years?

- How is the convergence of OT, IT, and IoT shaping this market?

- Which industrial automation suppliers have been most aggressive in supporting machine health initiatives?

- How have cybersecurity concerns affected the adoption and implementation of these solutions?

Who Should Read this Report?

This report is intended for those making critical decisions regarding product development, partnerships, go-to- market planning, and competitive strategy and tactics. It is written for executives, senior managers, and other decision-makers involved in the development, deployment, marketing, management, or sales of industrial machine health solutions, including those in the following roles:

- CEO or other C-level executives

- Corporate development and M&A teams

- Marketing executives

- Business development and sales leaders

- Product development and product strategy leaders

- Channel management and channel strategy leaders

Vendors Listed in this Report:

|

|

|

Executive Summary

The continued maturation of sensing technologies has been a foundational growth driver throughout the early stages of this market. Moving forward, the emergence and maturation of industrial artificial intelligence will be among the most critical technological drivers for this market.

This market is populated by a diverse mix of machine health startups, established industrial technology vendors, industrial component suppliers, and global industrial automation giants. Through the early stages of this market, dedicated machine health providers such as Augury, I-care, and KCF Technologies have been the most successful in generating demand due to their laser focus on this sector. From a solution perspective, competitors in this market generally fit into one of several categories: companies that sell sensors, companies that sell sensors and provide manual diagnostics and recommendations via service engagements, and companies that sell sensors and provide automated diagnostics and recommendations leveraging AI. Beyond the leading vendors, the competitive landscape is further populated by variety of niche competitors that serve select geographies, industries, or machine health monitoring applications.

The food and beverage industry was the leading sources of industrial machine health monitoring revenue in 2024 due, in large part, to the high volume of machinery present in facilities within this space. Operating environments within the food and beverage industry are generally less complex to monitor, allowing for straightforward deployments and easily demonstrable cost savings. The energy and power generation sector will be the fastest- growing industry segment through 2029 as corporate environmental, societal, and governance (ESG) goals drive operators to address mounting requirements such as those around carbon emissions or energy management. Automotive manufacturers and component suppliers will also drive significant growth through the end of the forecast period.

Key Findings:

- The maturation of industrial artificial intelligence will be a critical growth driver for this market.

- Requirements around openness and interoperability have intensified as industrial organizations continue gaining access to new operational data sources.

- Competitors whose deployments rely on professional services will find it increasingly difficult to scale their services capacity as their install base grows.

- The Asia-Pacific region will attain the highest growth rate through the end of the forecast period.

- Vendors overwhelmingly rely on direct sales to engage with customers.

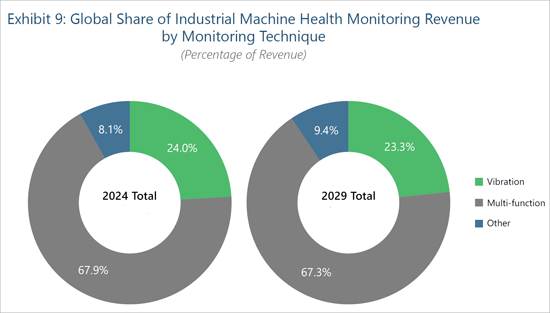

Monitoring Technique Segmentation and Forecast

Overview

Vibration monitoring - either via dedicated vibration sensors or multi-function sensors also including temperature and other measurements - generated the overwhelming majority of industrial machine health monitoring revenue in 2024. Due to its ability to identify abnormal behavior in common industrial equipment such as compressors, generators, fans, motors, pumps, and turbines, vibration monitoring is the de facto starting point for any industrial organization looking to prevent failures before they occur. The addition of temperature measurement allows multi-function sensors to provide a more comprehensive understanding of machine performance. Multi-function sensors from Augury, I-care, and other market leaders commonly include additional measurement parameters, such as impact and magnetic flux. The expanded coverage afforded by these additional measurement parameters will allow the growth rate of this segment to outpace that of the single- parameter vibration segment. Moving forward, vibration and multi-function sensors will continue to comprise the vast majority of this market through the end of the forecast period, however, alternative techniques such as corrosion monitoring, electrical monitoring, and oil analysis will grow at the greatest rate (nearly 16% per year through the end of the forecast period) as organizations begin to target non-rotating equipment such as drums, pipes, and tanks. Sensors measuring magnetic flux will become particularly attractive due to their ability to measure energy consumption and help organizations meet their ESG objectives.

Alternative Techniques Hindered by Limited Machine Knowledge

Even before the emergence of this IIoT-enabled market segment, vibration monitoring has long been at the forefront of industrial organizations' condition monitoring efforts. As such, solution providers have access to tremendous volumes of reference data detailing common failure points and fault conditions for most types of rotating industrial equipment. Used in conjunction with vendors' machine learning algorithms and AI capabilities, this reference data is a foundational element of the machine health market. Unfortunately, reference data for non- rotating, discrete machinery such as cranes and robots is comparatively scarce. Without a sufficient body of knowledge as to how these machines break and how they are fixed, vendors in this space have been hesitant to offer coverage in this area. To effectively cover assets with critical, non-rotating components, solution providers must amass not only sufficient reference data around each new class of machinery, but also sufficient in-house expertise to deliver value-adding advice to customers.

Table of Contents

What Questions are Addressed?

Who Should Read this Report?

Vendors Listed in this Report

Executive Summary

- Key Findings

Global Market Overview

- Market Summary

- Market Drivers and Strategies

- Labor Challenges Prompting Digital Transformation

- Sensor Maturity, Interoperability Requirements Shaping Market

Competitive Landscape

- Overview

- Challenges

- Seizing Market Share via Acquisition

- Fostering Buy-In from Frontline Workers

- Scaling Deployments and Adapting to Evolving Customer Requests

- Opportunities

- Solving the AI Puzzle

- Enabling Integrations Throughout the OT Stack

- Pursuing Partnerships to Reach New Markets

Global Market Segmentations

- Regional Segmentation and Forecast

- Overview

- Industrialization Creates Market Opportunities

- Industry Segmentation and Forecast

- Overview

- Industry Silos Limit Market Growth

- Monitoring Technique Segmentation and Forecast

- Overview

- Alternative Techniques Hindered by Limited Machine Knowledge

- Channel Segmentation and Forecast

- Overview

- End Users Wary of OEM Solutions

Vendor Highlights

- Advanced Technology Services (ATS)

- AssetWatch

- Augury

- I-care

- KCF Technologies

- Others

- Bently Nevada

- Emerson

- MaintainX

- TRACTIAN

- Waites

About the Authors

List of Exhibits

- Exhibit 1: Global Revenue for Industrial Machine Health Monitoring

- Exhibit 2: Global Revenue for Industrial Machine Health Monitoring by Leading Vendors (2024)

- Exhibit 3: Global Revenue for Industrial Machine Health Monitoring by Region

- Exhibit 4: Global Share of Industrial Machine Health Monitoring Revenue by Region

- Exhibit 5: Global Revenue for Industrial Machine Health Monitoring by Industry

- Exhibit 6: Global Share of Industrial Machine Health Monitoring Revenue by Industry

- Exhibit 7: Global Revenue for Industrial Machine Health Monitoring by Monitoring Technique

- Exhibit 8: Global Share of Industrial Machine Health Monitoring Revenue by Monitoring Technique

- Exhibit 9: Global Revenue for Industrial Machine Health Monitoring by Channel

- Exhibit 10: Global Share of Industrial Machine Health Monitoring Revenue by Channel

船舶状态监测工具:2026-2032年全球市占率及排名、总收入及需求预测

船舶状态监测工具:2026-2032年全球市占率及排名、总收入及需求预测 皮带状态监测系统市场:按组件、部署方式、监测类型、安装类型、皮带类型、最终用户划分,全球预测,2026-2032年离线分板设备市场:依基板类型、自动化程度、处理能力、设备技术及终端用户产业划分-全球预测,2026-2032年面板拆卸设备市场:依技术、PCB材料、终端用户产业、应用与销售管道,全球预测,2026-2032年工业分级机市场:依产品类型、技术、材料、最终用户和通路划分,全球预测(2026-2032年)

皮带状态监测系统市场:按组件、部署方式、监测类型、安装类型、皮带类型、最终用户划分,全球预测,2026-2032年离线分板设备市场:依基板类型、自动化程度、处理能力、设备技术及终端用户产业划分-全球预测,2026-2032年面板拆卸设备市场:依技术、PCB材料、终端用户产业、应用与销售管道,全球预测,2026-2032年工业分级机市场:依产品类型、技术、材料、最终用户和通路划分,全球预测(2026-2032年) 状态监测系统市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、部署类型、最终用户、设备及解决方案划分

状态监测系统市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、部署类型、最终用户、设备及解决方案划分 机械振动监测系统市场机会、成长要素、产业趋势分析及2026年至2035年预测

机械振动监测系统市场机会、成长要素、产业趋势分析及2026年至2035年预测 2026-2030年全球重工业状态监测感测器发展趋势工业机械监控系统市场:按组件、部署类型、感测器技术、应用和最终用户产业划分,全球预测(2026-2032年)开关设备状态监测市场(依开关设备类型、监测类型、技术、组件类型和最终用户划分),全球预测,2026-2032年

2026-2030年全球重工业状态监测感测器发展趋势工业机械监控系统市场:按组件、部署类型、感测器技术、应用和最终用户产业划分,全球预测(2026-2032年)开关设备状态监测市场(依开关设备类型、监测类型、技术、组件类型和最终用户划分),全球预测,2026-2032年