|

市场调查报告书

商品编码

1706271

聚变能及其他等离子工程材料与硬体机会:2025-2045 年市场Nuclear Fusion Power and Other Plasma Engineering Materials and Hardware Opportunities: Markets 2025-2045 |

|||||||

硼作为 "融合体操运动员" :

硼的应用范围除了核融合之外,还涵盖从医学到航空航太等各种领域,这将降低开发成本风险。例子包括高温超导体、高功率雷射、钨、铜、硅、锂、铁和碳同位素,它们的使用形式多种多样,包括合金、化合物和基于奈米技术的形式。为什么硼基材料被称为 "聚变体操运动员" ?这是因为它是聚变装置中许多重要应用的基础。稀土元素、有机聚合物等许多材料也正在引起人们的注意。

投资洪流,展望未来:

核融合开发商目前正在向高价值材料和结构投入巨额且快速增长的资金。聚变能及相关新兴应用的进一步成功将为等离子技术、雷射和低温技术等技术开闢庞大的硬体市场。报告确定了有前景的应用领域、潜在的合作伙伴和竞争对手,还包括 2025 年至 2045 年的路线图和市场预测。

目录

第 1 章执行摘要与概述

- 本报告的目标

- 分析法

- 一般结论(7 项)

- 材料和硬体结论(11 项)

- 根据 2025 年的研发重点,列出 23 种关键材料和硬体机会

- 等离子体相关材料与硬体机会

- 核融合价值链中膜材料和相关设备的分类(依复杂程度)

- 关于聚变公司私人投资趋势的三个结论

- 核融合在电网电力应用潜力方面的 SWOT 分析

- 磁约束聚变作为电网电源的 SWOT 分析

- 惯性约束聚变作为电网电源的 SWOT 分析

- 聚变及相关系统的材料和硬体技术和市场路线图

- 22 个市场预测与图表(2025-2045 年)

第2章 再生能源、重组氢能经济及其他产业中的聚变能及其他等离子体技术

- 概述

- 氢能经济:失败的开端、重组和氢聚变的前景

- 私人核融合公司和政府竞相进入氢聚变发电领域

- 政府大力投资核融合能源

- 氢同位素的主要用途

- 普通氢(氕)与其他燃料、氘和氚的性质比较

- 氢气:电气化的合作伙伴和替代方案

- 实际裂变发电系统与拟议的聚变发电系统的比较

- 核融合供电最早预计时间

- 使用氘的其他聚变和等离子工程应用

第3章 核融合的基本原理及高附加价值材料机会的具体实例

- 概述

- 候选燃料、反应方法、反应器运作原理与设计

- 聚变发电的重大里程碑、设备小型化的原因以及代表公司

- 材料机会的全貌:液体、固体、气体和等离子体

- 用于聚变反应器设施的钢和其他铁基合金的配方和结构设计

- 氢气罐材料和化学储氢材料

- 核融合价值链中膜材料及相关设备的分类(依复杂程度)

第4章 磁约束聚变能:材料与硬体机会

- 概述

- 磁约束聚变作为电网电源:SWOT分析

- 核融合发电磁约束系统的设计

- 等离子体邻近材料的机会

- 磁铁技术的进步

- 散热器/传热和冷却材料的创新

- 截至 2025 年的偏滤器材料研究与新 ITER 设备

- 等离子加热系统与机器人技术的进步

- 核融合供电系统与发电系统

- 託卡马克和 Z-Pinch 硬体的机会范例:JET、ITER 等。

- 2025 年环状及相关聚变能硬体研究

- 由内而外的磁约束

第5章 惯性约束与磁惯性聚变动力:材料与硬体潜力

- 概述

- 惯性约束聚变作为电网电力:SWOT分析

- 以雷射为基础的惯性约束聚变的雷射设计

- 聚变目标机会(燃料颗粒等)

- 劳伦斯利弗莫尔国家实验室 (LLNL) 的国家点火装置 (NIF)

- 中国正在引领潮流? (国际竞争情势)

- 其他惯性约束聚变 (ICF) 和磁惯性约束聚变 (MIF) 开发商

第6章:投资重点的变化:值得关注的公司、硬体和材料

- 兴趣和投资激增:哪些技术以及为什么?

- 投资私人公司

- 投资者意向和按技术划分的交易

- 全球努力

- 私人核融合公司竞相兴建氢聚变电站的分析

- 按国家/地区划分的领先核融合公司:根据各种绩效标准和资金状况进行评估

- 政府和私人投资在聚变发电方面的区域与技术优势

- 吸引投资的关键材料和硬件

- 经常提到的高附加价值材料的例子:核融合中的普及程度和具体应用

第7章:材料在核融合发电以外的核融合技术中的潜力

- 概述

- 提出的聚变推进太空船基本原理

- 静电惯性约束聚变的进展与 2025 年的目标应用

- 核融合及其他领域的中子源研究

- 迴旋加速器技术的衍生应用(除核融合以外的用途):地热钻探等。

- 高温超导体 (HTS) 除了核融合之外的可能用途

Summary

Good news. The quest for fusion power is opening up many opportunities for your high added value materials and hardware. Thoroughly analysing your opportunities is the new commercially-oriented 218-page Zhar Research report, "Nuclear Fusion and Other Plasma Engineering Materials and Hardware Opportunities: Markets 2025-2045". Whether your skills lie in metallurgy, composites or chemistry based on the many elements it examines, this report details your road ahead.

Boron the gymnast

Learn how your development costs are derisked by these materials having many other applications beyond fusion power from medical to aerospace. Examples include high temperature superconductors, high power lasers, tungsten, copper, silicon, lithium, iron, carbon isotopes, many in forms varying from alloys to compounds and nano technology. Why is boron-based material the gymnast of fusion, being the basis of so many vital uses in fusion machines? See how rare earths, organic polymers and many other materials are also in the frame.

Flood of investment, see the future

Fusion developers now have massive, rapidly-rising funding to spend on your essential added value materials and structures. Further success in fusion power or allied emerging applications means that these plasma, laser, cryogenic and other technologies will open up huge hardware markets. Winning applications, potential partners and competitors are identified with 2025-2045 roadmaps and forecasts.

Comprehensive report

The 35 page "Executive summary and conclusions" is sufficient in itself with 21 key conclusions, 3 SWOT appraisals, 2025-2045 roadmaps both for technology and for markets and 22 forecast lines as graphs and tables. New infograms make it all easy to absorb in a short time. 23 key materials and hardware opportunities from 2025 research and company initiatives are prioritised.

Pivoting to a hydrogen economy reinvented

Then comes context and options in Chapter 2. "Fusion power and other plasma engineering in the context of renewable energy, the hydrogen economy reinvented and other industry" (30 pages). Learn the significance of the hydrogen isotopes. Understand why the original idea of a hydrogen economy based on fuel for your car and house is doomed. We are pivoting to a reinvented hydrogen economy mostly based on fusion grid power, making basic chemicals and aerospace and ship propulsion because they have far greater chance of success, though nothing is guaranteed.

Derisk your investment

Then come four chapters detailing your opportunities in fusion and allied plasma engineering, with particular emphasis on 2025 research and breakthroughs. The report ends with a chapter on the other emerging markets needing the same or similar materials, often well before any possible success with fusion for electricity generation. This derisks your investment.

Size reduction and other priorities

Chapter 3. "Basics of fusion and examples of its high-value materials opportunities" (39 pages) presents the detail including candidate fuels, reactions, reactor operating principles and designs, with much 2025 research, most notably deuterium, tritium, alpha particle and neutron-related. See candidate operating principles and designs of fusion power reactors and understand the changing views on winning technologies and changing relative achievements, plans and the most important milestones ahead. Why is size reduction now a strong focus even if the materials achieving this are expensive? Here is the big picture of materials opportunities, encompassing liquids, solids, gases and plasma.

Materials surviving a perfect storm

See how fusion subsystems present many added burdens for materials, withstanding chemical, heat, radiation, hydrogen embrittlement and plasma damage. Here is appraisal of the research in 2025 that leads you to candidate materials solving identified future needs. Examples explained include many different steels and membranes, mostly using advanced polymers.

Better materials urgently needed

Chapter 4. "Magnetic confinement fusion power: materials and hardware opportunities" (50 pages) concerns the fusion power option receiving the most public and private investment. Materials focus here particularly includes complex multi-wall structures for tokamaks and stellarators and identified derivatives. These formulations variously withstand or magnetically contain plasma, breed fuel, multiply neutrons, remove heat, block radiation. Can you rescue this industry from its lethally toxic and dangerously chemically-reactive materials? Metals, alloys, composites, compounds or what? High added value also comes from wall-conditioning, multipurpose blanket materials. Massive power supplies, "divertors" and other giant subsystems are needed. Why are- stellarators - gaining more attention and what are their materials? Inside-out magnetic confinement, levitated dipole, reverse triangulation and other approaches and needs? It is all here.

The 25 close-packed pages of Chapter 5. "Inertial confinement and magneto-inertial fusion power: materials and hardware opportunities" concerns the second most important fusion power option in investment and number of participants. It is the only one that has demonstrated "ignition" so far. See why it is now getting more attention as smaller, higher-power lasers, analysed here, arrive and China builds a massive facility 50% bigger than the American one. On the other hand, hybrid magneto-inertial options promise direct production of electricity but it is wrong to think of this as no-neutrons/ no-radioactivity. Which problems are your materials opportunities in magnetic confinement fusion? Colliding plasmas or projectiles instead of lasers?

Changing investment focus

Chapter 6. "Changing Investment focus, companies, hardware and materials to watch" (10 pages) explains the sudden surge in interest and investment: which technology and why. Detail is presented on investment in private companies, investor intentions and deals by technology. See how this is now a global effort. Here is analysis of private fusion companies racing to make hydrogen fusion electricity generators, winning fusion power companies by country, various performance criteria and funding. What are the winning fusion power locations and technologies for government vs private investments? What are significant key enabling materials and hardware attracting investment from analysis of 214 recent advances?

Profusion of opportunities

Those seeking investment may whisper it quietly but there is a possibility of fusion power not being commercialised in the 2025-2045 timeframe. Contrast allied technologies such as high temperature superconductors in medical scanners that are already commercialised with many more applications soon. The report therefore closes with Chapter 7. "Materials opportunities in fusion technologies beyond fusion power generation" (14 pages). Learn how spacecraft will not just drift after lift-off but use fusion power continuously and which options are emerging for this. Electrostatic inertial confinement fusion is not promising for generating electricity but see other advances and targetted uses for it from 2025. See plasma neutron sources for beyond fusion, with 2025 research. Gyrotron technology, not mainstream for power, can spin off beyond fusion for geothermal drilling and other uses. See detail on this high-profile new development and also the remarkable scope for high temperature superconductors beyond fusion.

Latest information and views

Fusion is now a fast-moving subject, so old information is useless. Most of the report, "Nuclear Fusion Power and Other Plasma Engineering Materials and Hardware Opportunities: Markets 2025-2045" interprets advances in 2025 and it is constantly updated so you only get the latest. It is your essential reading for your materials and hardware opportunities with realistic appraisal of timescales.

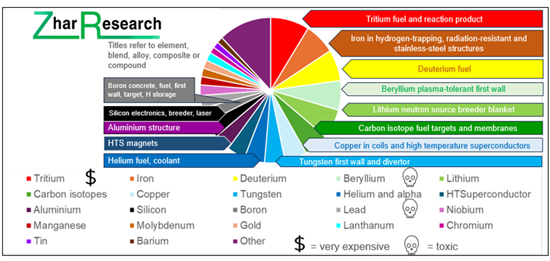

CAPTION: Simplified version of image in the report, "Nuclear Fusion Power and Other Plasma Engineering Materials and Hardware Opportunities: Markets 2025-2045", giving priority by number of primary mentions of high added-value materials and uses in the large amount of research and other activity analysed, with examples of applications.

Table of Contents

1. Executive summary and conclusions

- 1.1. Purpose of this report

- 1.2. Methodology of this analysis

- 1.3. Seven general conclusions

- 1.4. Eleven conclusions concerning materials and hardware

- 1.5. 23 key materials and hardware opportunities from 2025 research and developers prioritised

- 1.6. Materials and hardware opportunities adjacent to the plasma

- 1.7. Membrane materials in the fusion value chain and related devices by level of sophistication

- 1.8. Three conclusions: Investment trends in private fusion companies

- 1.9. SWOT appraisal of the potential of fusion grid power

- 1.10. SWOT appraisal of magnetic confinement fusion as a potential source grid electricity

- 1.11. SWOT appraisal of inertial confinement fusion as a potential source grid electricity

- 1.12. Fusion and allied systems, materials and hardware roadmap for technology vs market 2025-2045

- 1.13. Market forecasts in 22 lines, graphs 2025-2045

- 1.13.1. Specialist materials and assemblies for fusion power including experiments: market inorganic vs organic $ billion 2025-2045

- 1.13.2. Hydrogen hardware market: fusion reactors + 7 lines $ billion 2025-2045, table, graphs

- 1.13.3. Number of companies seeking to make fusion reactors 2025-2045

- 1.13.4. Fusion machine energy output trend with and without ignition

- 1.13.5. Hydrogen market million tonnes 2025-2045 in seven lines, table, graphs

2. Fusion power and other plasma engineering in the context of renewable energy, the hydrogen economy reinvented and other industry

- 2.1. Overview

- 2.2. Hydrogen economy: a false start, reinvention and the promise of hydrogen fusion

- 2.2.1. The big picture

- 2.2.2. Lessons of history and new objectives for 2025-2045

- 2.2.3. Materials for the hydrogen economy reinvented

- 2.2.4. Supporting information

- 2.3. Private fusion companies and governments race into hydrogen fusion power

- 2.4. Major government investment in fusion power

- 2.5. Hydrogen isotopes and their primary uses actual and targetted

- 2.6. Comparison of properties of regular hydrogen (protium) with other fuels and with the deuterium and tritium forms of hydrogen

- 2.7. Hydrogen is both partner and alternative to electrification

- 2.8. Comparison of actual fission and planned fusion power systems

- 2.9. Earliest dates for fusion grid electricity being delivered

- 2.10. Other fusion and plasma engineering and other uses for deuterium

3. Basics of fusion and examples of its high-value materials opportunities

- 3.1. Overview

- 3.2. Candidate fuels, reactions, reactor operating principles and designs

- 3.2.1. Candidate fusion fuels and reactions with 2025 research

- 3.2.2. Deuterium-related fusion research advances in 2025

- 3.2.3. Tritium-related fusion research advances in 2025

- 3.2.4. Alpha particle-related fusion research advances in 2025

- 3.2.5. Neutron-related fusion research advances in 2025

- 3.2.6. Candidate operating principles and designs of fusion power reactors

- 3.2.7. Changing views on winning technologies and changing relative achievements and plans

- 3.3. Milestones, reasons for size reduction and examples of companies for fusion power

- 3.4. Big picture of materials opportunities : liquids, solids, gases and plasma

- 3.4.1. Materials are a primary challenge to fusion power: premium pricing opportunities

- 3.4.2. Fusion subsystems present many added burdens for materials

- 3.4.3. Radiation and plasma damage of the materials: research in 2025 and future needs

- 3.4.4. Some candidate materials reflecting various of these needs

- 3.5. Steel and other iron-based alloy formulations and structures for fusion reactor facilities

- 3.5.1. Steels for general fusion facility structures, radiative environments with 2025 research

- 3.5.2. Resisting hydrogen embrittlement

- 3.5.3. Welding and other structural optimisation with 2025 research

- 3.6. Hydrogen tank materials and chemical hydrogen storage materials

- 3.6.1. Hydrogen tank materials

- 3.6.2. Hydrogen leakage causing global warming: research in 2025

- 3.7. Membrane materials in the fusion value chain and related devices by level of sophistication

4. Magnetic confinement fusion power: materials and hardware opportunities

- 4.1. Overview

- 4.2. SWOT appraisal of magnetic confinement fusion as a potential source grid electricity

- 4.3. Magnetic confinement geometries for fusion power

- 4.4. Materials opportunities adjacent to the plasma

- 4.4.1. Multilayer wall and proximate structures

- 4.4.2. Wall conditioning materials advances through 2025

- 4.4.3. Multifunctional blanket materials research in 2025

- 4.5. Magnet advances

- 4.6. Heat sink/ heat transfer, coolant materials advances

- 4.7. Divertor materials research in 2025 and the new ITER installation

- 4.8. Plasma heating systems and robotics

- 4.9. Fusion power supplies and electricity generation systems

- 4.9.1. Power generation from fusion reactors

- 4.9.2. Power supply to fusion reactors

- 4.10. Examples of tokamak and Z-Pinch hardware opportunities: JET, ITER and others

- 4.11. Research in 2025 on toroidal and allied fusion power hardware

- 4.11.1. General

- 4.11.2. Stellarators and their materials research in 2025

- 4.12. Inside-out magnetic confinement:

- 4.12.1. OpenStar levitated dipole fusion reactor

- 4.12.2. Reverse triangulation

5. Inertial confinement and magneto-inertial fusion power: materials and hardware opportunities

- 5.1. Overview

- 5.2. SWOT appraisal of inertial confinement fusion as a potential source grid electricity

- 5.3. Laser-based inertial confinement fusion (LICF) laser designs

- 5.3.1. Neodymium glass lasers

- 5.3.2. Ultraviolet lasers

- 5.3.3. Quantum cascade lasers

- 5.4. Fusion target opportunities

- 5.4.1. HUB project targets

- 5.4.2. NIF project targets

- 5.4.3. Fundamentals of target operation

- 5.5. Lawrence Livermore National Laboratories LLNL National Ignition Facility NIF

- 5.6. China pulling ahead?

- 5.7. Other inertial and magneto-inertial confinement developers

- 5.7.1. General picture

- 5.7.2. Helion and its key materials and devices

- 5.7.3. Electrostatic inertial confinement fusion advances in 2025

6. Changing Investment focus, companies, hardware and materials to watch

- 6.1. Sudden surge in interest and investment: which technology and why

- 6.2. Investment in private companies

- 6.3. Investor intentions and deals by technology

- 6.4. Global effort

- 6.5. Analysis of private fusion companies racing to make hydrogen fusion electricity generators

- 6.6. Winning fusion power companies by country, various performance criteria, funding

- 6.6. Winning fusion power locations and technologies for government vs private investments

- 6.7. Significant key enabling materials and hardware attracting investment

- 6.8. Primary mentions of high added-value materials indicating popularity with examples of fusion uses

7. Materials opportunities in fusion technologies beyond fusion power generation

- 7.1. Overview

- 7.2. Principles proposed for fusion-propelled spacecraft

- 7.3. Electrostatic inertial confinement fusion advances, targeted uses in 2025

- 7.4. Neutron sources for fusion and beyond: 2025 research

- 7.5. Gyrotron technology spinoff beyond fusion: geothermal drilling, other

- 7.5.1. Principle of operation

- 7.5.2. Geothermal drilling, material processing, other

- 7.5.3. Recent research

- 7.5.4. Gyrotron materials and designs

- 7.6. High temperature superconductors beyond fusion

2026年全球核融合市场报告2026年全球聚变能源市场报告

2026年全球核融合市场报告2026年全球聚变能源市场报告 核能工程用超合金市场:按合金类型、产品形式、核子反应炉类型、製造方法和最终用途分類的全球预测(2026-2032年)

核能工程用超合金市场:按合金类型、产品形式、核子反应炉类型、製造方法和最终用途分類的全球预测(2026-2032年) 核融合能源的全球市场(2026年~2046年)按技术、燃料类型和最终用户分類的核融合能源市场—2025-2030 年全球预测

核融合能源的全球市场(2026年~2046年)按技术、燃料类型和最终用户分類的核融合能源市场—2025-2030 年全球预测 全球核融合市场

全球核融合市场 核融合能源市场 - 全球及区域分析:按应用、技术、燃料循环和国家 - 分析与预测(2025-2034 年)全球聚变能市场核融合全球市场:2034 年市场机会与策略

核融合能源市场 - 全球及区域分析:按应用、技术、燃料循环和国家 - 分析与预测(2025-2034 年)全球聚变能市场核融合全球市场:2034 年市场机会与策略 核融合市场-全球产业规模、份额、趋势、机会及预测(按技术、燃料、地区及竞争细分,2020-2030 年)

核融合市场-全球产业规模、份额、趋势、机会及预测(按技术、燃料、地区及竞争细分,2020-2030 年)