|

市场调查报告书

商品编码

1680164

全球国防航空平台发动机市场:2025-2035年Global Defense Air Platforms Engines Market 2025-2035 |

||||||

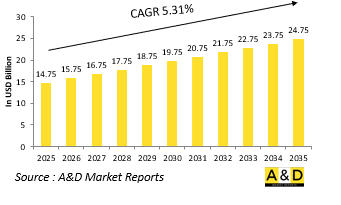

全球国防航空平台发动机市场规模预计到2025年将成长至 147.5亿美元,到2035年将成长至 247.5亿美元,2025-2035年预测期内的年复合成长率(CAGR)为 5.31%。

全球国防航空航太平台发动机市场是国防航空航太工业的重要领域,其驱动因素是战斗机、轰炸机、运输机、直升机和无人机(UAV)等军用飞机对高性能推进系统的需求不断成长。由于空中优势仍是现代战争的决定性因素,各国不断投资先进的推进技术,以提高速度、燃油效率、续航力和隐身能力。军用飞机引擎必须满足严格的性能要求,包括在恶劣条件下运作的能力、保持高机动性和支援远程任务的能力。该市场的特点是持续的研究和开发(R&D),目的是提高推力重量比、提高可靠性和降低维护成本。全球国防现代化计划、不断变化的地缘政治动态以及新出现的威胁推动对下一代推进系统的投资,使该市场成为全球国防承包商和军事组织关注的重点领域。

技术在塑造国防航空平台发动机市场方面发挥着变革性的作用,材料、製造技术和数位整合方面的创新显着提高了发动机性能。最显着的进步之一是自适应循环引擎的引进。自适应循环引擎根据任务要求动态调节气流,提高燃油效率并增加推力。这些发动机,例如根据美国自适应发动机过渡计划(AETP)开发的发动机,将提供更大的操作灵活性,使飞机能够在省油模式和高性能模式之间无缝切换。推进技术的另一项突破是陶瓷基复合材料(CMC)的整合。陶瓷基复合材料可提高耐热性,减轻引擎重量并提高效率和耐用性。积层製造(通常称为 3D 列印)透过减少材料浪费、缩短交货时间并实现复杂零件的快速生产,彻底改变了引擎製造业。使用数位孪生(实体引擎的虚拟复製品)可以实现预测性维护和即时性能监控,最大限度地减少停机时间并最佳化车队的准备状态。此外,混合动力和氢动力推进系统的进步被视为长期永续发展努力的一部分,但这些技术在军事应用方面仍处于起步阶段。

有几个关键驱动因素推动国防航空平台发动机市场的成长。其中一个主要因素是世界各地不断增加的军用飞机的采购和升级。许多国家用现代平台取代老化的飞机,而这些现代平台需要能够提供卓越性能的下一代引擎。向第五代和第六代战斗机的转变,例如 F-35 Lightning II、Tempest 和下一代空中优势(NGAD)计划,推动对更强大、更省油的引擎的需求。另一个重要驱动因素是人们越来越重视隐身性和生存力。在现代空战中,躲避雷达侦测非常重要,因此引擎製造商致力于降低红外线特征和噪音等级,以使飞机更加隐身。无人机在国防行动中的兴起也扩大了市场机会,军队寻求高耐力发动机来实现长时间的侦察和攻击任务。此外,联合防卫规划和多边合作日益频繁,盟友们汇集资源,加速技术进步和成本分摊举措,刺激引擎开发的创新。

在中东,军事现代化努力和先进战斗机的采购增加推动对国防航空平台发动机的需求。沙乌地阿拉伯和阿拉伯联合大公国等GCC国家投资新一代飞机和维护能力,以加强其防空系统。这些国家经常采购西方製造的飞机,例如F-15、F-16和F-35,这些飞机依赖美国和欧洲主要製造商提供的发动机。该地区恶劣的气候条件还需要对引擎进行特殊的改造,以确保在极端温度和沙尘环境下的运作可靠性。此外,与西方国防公司的合作促进了技术转移和本地维护能力,加强了该地区的国防和航太部门。

与其他地区相比,非洲的国防航空平台发动机市场相对较小,但随着各国寻求空军现代化,该市场逐步扩大。许多非洲国家运营的传统飞机需要升级或更换发动机,这为维护、维修和大修(MRO)服务创造了机会。阿尔及利亚、埃及和南非等国家是该地区的主要国防航空参与者,投资于西方和俄罗斯製造的飞机。此外,人们对反恐行动和边境安全的日益担忧也推动了对支援区域安全努力的军用运输机和直升机发动机的需求。

本报告涵盖全球国防航空平台发动机市场,并提供依细分市场的10年市场预测、技术趋势、机会分析、公司概况和 49个国家的资料。

目录

国防航空平台发动机市场报告定义

国防航空平台发动机市场细分

- 依用途

- 依地区

未来 10年国防航空平台发动机市场分析

国防航空平台发动机市场的市场技术

全球国防航空平台发动机市场预测

国防航空平台发动机市场趋势与预测(依地区)

- 北美洲

- 驱动因素、限制因素与挑战

- PEST

- 大型公司

- 供应商层级结构

- 企业基准

- 市场预测与情境分析

- 欧洲

- 中东

- 亚太地区

- 南美洲

国防航空平台发动机市场国家分析

- 美国

- 计划地图

- 最新消息

- 专利

- 目前该市场的技术成熟度

- 市场预测与情境分析

- 加拿大

- 义大利

- 法国

- 德国

- 荷兰

- 比利时

- 西班牙

- 瑞典

- 希腊

- 澳洲

- 南非

- 印度

- 中国

- 俄罗斯

- 韩国

- 日本

- 马来西亚

- 新加坡

- 巴西

国防航空平台发动机市场机会矩阵

国防航空平台发动机市场报告专家意见

结论

关于航空和国防市场报告

The Global Defense Air Platforms Engines market is estimated at USD 14.75 billion in 2025, projected to grow to USD 24.75 billion by 2035 at a Compound Annual Growth Rate (CAGR) of 5.31% over the forecast period 2025-2035.

Introduction to Defense Air Platforms Engines Market:

The global defense air platforms engines market is a critical sector within the defense aerospace industry, driven by the increasing demand for high-performance propulsion systems to power military aircraft, including fighter jets, bombers, transport planes, helicopters, and unmanned aerial vehicles (UAVs). As air superiority remains a decisive factor in modern warfare, nations continue to invest in advanced propulsion technologies to enhance speed, fuel efficiency, durability, and stealth capabilities. Military aircraft engines must meet stringent performance requirements, including the ability to operate in extreme conditions, sustain high maneuverability, and support long-range missions. The market is characterized by continuous research and development (R&D) efforts aimed at improving thrust-to-weight ratios, increasing reliability, and reducing maintenance costs. Global defense modernization programs, shifting geopolitical dynamics, and emerging threats are driving investments in next-generation propulsion systems, making this market a key area of focus for defense contractors and military organizations worldwide.

Technology Impact in Defense Air Platforms Engines Market:

Technology plays a transformative role in shaping the defense air platforms engines market, with innovations in materials, manufacturing techniques, and digital integration significantly enhancing engine performance. One of the most notable advancements is the incorporation of adaptive cycle engines, which offer improved fuel efficiency and greater thrust by dynamically adjusting airflow based on mission requirements. These engines, such as those being developed under the U.S. Adaptive Engine Transition Program (AETP), provide superior operational flexibility, allowing aircraft to switch between fuel-saving and high-performance modes seamlessly. Another breakthrough in propulsion technology is the integration of ceramic matrix composites (CMCs), which enhance heat resistance and reduce engine weight, leading to improved efficiency and durability. Additive manufacturing, commonly known as 3D printing, is revolutionizing engine production by enabling the rapid fabrication of complex components with reduced material waste and shorter lead times. The use of digital twins-virtual replicas of physical engines-allows for predictive maintenance and real-time performance monitoring, minimizing downtime and optimizing fleet readiness. Additionally, advancements in hybrid-electric and hydrogen-powered propulsion systems are being explored as part of long-term sustainability efforts, although these technologies are still in their early stages for military applications.

Key Drivers in Defense Air Platforms Engines market:

Several key drivers are propelling growth in the defense air platforms engines market. One of the primary factors is the increasing procurement and upgrade of military aircraft fleets worldwide. Many nations are replacing aging aircraft with modern platforms that require next-generation engines capable of delivering superior performance. The shift towards fifth- and sixth-generation fighter jets, such as the F-35 Lightning II, the Tempest, and the Next Generation Air Dominance (NGAD) program, is fueling demand for more powerful and fuel-efficient engines. Another major driver is the growing emphasis on stealth and survivability. As radar-evading capabilities become crucial in modern aerial warfare, engine manufacturers are focusing on reducing infrared signatures and noise levels to enhance aircraft stealth. The rise of UAVs in defense operations is also expanding market opportunities, with militaries seeking high-endurance engines that enable extended surveillance and strike missions. Furthermore, the increasing frequency of joint defense programs and multinational collaborations is fostering innovation in engine development, as allied nations pool resources to accelerate technological advancements and cost-sharing initiatives.

Regional Trends in Defense Air Platforms Engines Market:

In the Middle East, defense air platform engine demand is driven by military modernization efforts and increased procurement of advanced fighter jets. Gulf Cooperation Council (GCC) nations, including Saudi Arabia and the United Arab Emirates, are investing in new-generation aircraft and maintenance capabilities to enhance their aerial defense systems. These countries frequently procure Western-made aircraft, such as the F-15, F-16, and F-35, which rely on engines supplied by leading U.S. and European manufacturers. The region's harsh climatic conditions also necessitate specialized engine adaptations to ensure operational reliability in extreme temperatures and sand-laden environments. Additionally, partnerships with Western defense companies are facilitating technology transfers and local maintenance capabilities, strengthening the regional defense aerospace sector.

Africa's defense air platforms engines market is relatively smaller compared to other regions but is gradually expanding as nations seek to modernize their air forces. Many African countries operate legacy aircraft that require engine upgrades or replacements, creating opportunities for maintenance, repair, and overhaul (MRO) services. Nations such as Algeria, Egypt, and South Africa are among the leading defense aviation players in the region, investing in both Western and Russian-built aircraft. Additionally, increased counterterrorism operations and border security concerns are driving demand for military transport aircraft and helicopter engines, supporting regional security efforts.

Key Defense Air Platforms Engines Program:

In a significant boost to the Aatmanirbhar Bharat initiative, the Ministry of Defence (MoD) has signed a contract with Hindustan Aeronautics Limited (HAL) for the procurement of 240 AL-31FP aero engines for the Su-30MKI aircraft, valued at over Rs 26,000 crore. The agreement was formalized in New Delhi on September 9, 2024, in the presence of Defence Secretary Shri Giridhar Aramane, Secretary (Defence Production) Shri Sanjeev Kumar, and Chief of the Air Staff Air Chief Marshal VR Chaudhari. The engines will be produced at HAL's Koraput Division and will play a crucial role in maintaining the Indian Air Force's Su-30 fleet, ensuring sustained operational capability for national defense. Under the contractual schedule, HAL will supply 30 engines annually, with all 240 engines expected to be delivered over the next eight years.

In a major advancement for defense aviation, GE Aerospace has signed a five-year Performance-Based Logistics (PBL) contract with the Indian Air Force (IAF) to provide sustainment solutions for the T700-GE-701D engines powering the IAF's AH-64E-I Apache helicopters. This agreement strengthens the long-standing partnership between GE Aerospace and the IAF, highlighting the critical role of reliable maintenance and operational readiness for key defense assets.As part of the contract, GE Aerospace will manage the Maintenance, Repair, and Overhaul (MRO) of the T700 engines while also supplying flight line parts to ensure consistent engine availability. The PBL framework aims to streamline sustainment operations, minimize turnaround times, and improve the overall efficiency of the Apache helicopter fleet. By adopting a more integrated and performance-driven logistics approach, this collaboration ensures that the IAF's Apache helicopters remain mission-ready and fully operational.

Table of Contents

Defense Air Platforms Engines Market Report Definition

Defense Air Platforms Engines Market Segmentation

By Region

By Application

By End User

Defense Air Platforms Engines Market Analysis for next 10 Years

The 10-year defense air platforms engines market analysis would give a detailed overview of defense air platforms engines market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Defense Air Platforms Engines Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Defense Air Platforms Engines Market Forecast

The 10-year defense air platforms engines market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Defense Air Platforms Engines Market Trends & Forecast

The regional defense air platforms engines market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

REST

Key Companies

Supplier Tier Landscape

Company Benchmarking

Market Forecast & Scenario Analysis

Europe

Middle East

APAC

South America

Country Analysis of Defense Air Platforms Engines Market

This chapter deals with the key programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Program Mapping

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Defense Air Platforms Engines Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Defense Air Platforms Engines Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports

List of Tables

- Table 1: 10 Year Market Outlook, 2025-2035

- Table 2: Drivers, Impact Analysis, North America

- Table 3: Restraints, Impact Analysis, North America

- Table 4: Challenges, Impact Analysis, North America

- Table 5: Drivers, Impact Analysis, Europe

- Table 6: Restraints, Impact Analysis, Europe

- Table 7: Challenges, Impact Analysis, Europe

- Table 8: Drivers, Impact Analysis, Middle East

- Table 9: Restraints, Impact Analysis, Middle East

- Table 10: Challenges, Impact Analysis, Middle East

- Table 11: Drivers, Impact Analysis, APAC

- Table 12: Restraints, Impact Analysis, APAC

- Table 13: Challenges, Impact Analysis, APAC

- Table 14: Drivers, Impact Analysis, South America

- Table 15: Restraints, Impact Analysis, South America

- Table 16: Challenges, Impact Analysis, South America

- Table 17: Scenario Analysis, Scenario 1, By Region, 2025-2035

- Table 18: Scenario Analysis, Scenario 1, By Application, 2025-2035

- Table 19: Scenario Analysis, Scenario 1, By End User, 2025-2035

- Table 20: Scenario Analysis, Scenario 2, By Region, 2025-2035

- Table 21: Scenario Analysis, Scenario 2, By Application, 2025-2035

- Table 22: Scenario Analysis, Scenario 2, By End User, 2025-2035

List of Figures

- Figure 1: Global Defense Air Platforms Engines Market Forecast, 2025-2035

- Figure 2: Global Defense Air Platforms Engines Market Forecast, By Region, 2025-2035

- Figure 3: Global Defense Air Platforms Engines Market Forecast, By Application, 2025-2035

- Figure 4: Global Defense Air Platforms Engines Market Forecast, By End User, 2025-2035

- Figure 5: North America, Defense Air Platforms Engines Market, Market Forecast, 2025-2035

- Figure 6: Europe, Defense Air Platforms Engines Market, Market Forecast, 2025-2035

- Figure 7: Middle East, Defense Air Platforms Engines Market, Market Forecast, 2025-2035

- Figure 8: APAC, Defense Air Platforms Engines Market, Market Forecast, 2025-2035

- Figure 9: South America, Defense Air Platforms Engines Market, Market Forecast, 2025-2035

- Figure 10: United States, Defense Air Platforms Engines Market, Technology Maturation, 2025-2035

- Figure 11: United States, Defense Air Platforms Engines Market, Market Forecast, 2025-2035

- Figure 12: Canada, Defense Air Platforms Engines Market, Technology Maturation, 2025-2035

- Figure 13: Canada, Defense Air Platforms Engines Market, Market Forecast, 2025-2035

- Figure 14: Italy, Defense Air Platforms Engines Market, Technology Maturation, 2025-2035

- Figure 15: Italy, Defense Air Platforms Engines Market, Market Forecast, 2025-2035

- Figure 16: France, Defense Air Platforms Engines Market, Technology Maturation, 2025-2035

- Figure 17: France, Defense Air Platforms Engines Market, Market Forecast, 2025-2035

- Figure 18: Germany, Defense Air Platforms Engines Market, Technology Maturation, 2025-2035

- Figure 19: Germany, Defense Air Platforms Engines Market, Market Forecast, 2025-2035

- Figure 20: Netherlands, Defense Air Platforms Engines Market, Technology Maturation, 2025-2035

- Figure 21: Netherlands, Defense Air Platforms Engines Market, Market Forecast, 2025-2035

- Figure 22: Belgium, Defense Air Platforms Engines Market, Technology Maturation, 2025-2035

- Figure 23: Belgium, Defense Air Platforms Engines Market, Market Forecast, 2025-2035

- Figure 24: Spain, Defense Air Platforms Engines Market, Technology Maturation, 2025-2035

- Figure 25: Spain, Defense Air Platforms Engines Market, Market Forecast, 2025-2035

- Figure 26: Sweden, Defense Air Platforms Engines Market, Technology Maturation, 2025-2035

- Figure 27: Sweden, Defense Air Platforms Engines Market, Market Forecast, 2025-2035

- Figure 28: Brazil, Defense Air Platforms Engines Market, Technology Maturation, 2025-2035

- Figure 29: Brazil, Defense Air Platforms Engines Market, Market Forecast, 2025-2035

- Figure 30: Australia, Defense Air Platforms Engines Market, Technology Maturation, 2025-2035

- Figure 31: Australia, Defense Air Platforms Engines Market, Market Forecast, 2025-2035

- Figure 32: India, Defense Air Platforms Engines Market, Technology Maturation, 2025-2035

- Figure 33: India, Defense Air Platforms Engines Market, Market Forecast, 2025-2035

- Figure 34: China, Defense Air Platforms Engines Market, Technology Maturation, 2025-2035

- Figure 35: China, Defense Air Platforms Engines Market, Market Forecast, 2025-2035

- Figure 36: Saudi Arabia, Defense Air Platforms Engines Market, Technology Maturation, 2025-2035

- Figure 37: Saudi Arabia, Defense Air Platforms Engines Market, Market Forecast, 2025-2035

- Figure 38: South Korea, Defense Air Platforms Engines Market, Technology Maturation, 2025-2035

- Figure 39: South Korea, Defense Air Platforms Engines Market, Market Forecast, 2025-2035

- Figure 40: Japan, Defense Air Platforms Engines Market, Technology Maturation, 2025-2035

- Figure 41: Japan, Defense Air Platforms Engines Market, Market Forecast, 2025-2035

- Figure 42: Malaysia, Defense Air Platforms Engines Market, Technology Maturation, 2025-2035

- Figure 43: Malaysia, Defense Air Platforms Engines Market, Market Forecast, 2025-2035

- Figure 44: Singapore, Defense Air Platforms Engines Market, Technology Maturation, 2025-2035

- Figure 45: Singapore, Defense Air Platforms Engines Market, Market Forecast, 2025-2035

- Figure 46: United Kingdom, Defense Air Platforms Engines Market, Technology Maturation, 2025-2035

- Figure 47: United Kingdom, Defense Air Platforms Engines Market, Market Forecast, 2025-2035

- Figure 48: Opportunity Analysis, Defense Air Platforms Engines Market, By Region (Cumulative Market), 2025-2035

- Figure 49: Opportunity Analysis, Defense Air Platforms Engines Market, By Region (CAGR), 2025-2035

- Figure 50: Opportunity Analysis, Defense Air Platforms Engines Market, By Application (Cumulative Market), 2025-2035

- Figure 51: Opportunity Analysis, Defense Air Platforms Engines Market, By Application (CAGR), 2025-2035

- Figure 52: Opportunity Analysis, Defense Air Platforms Engines Market, By End User (Cumulative Market), 2025-2035

- Figure 53: Opportunity Analysis, Defense Air Platforms Engines Market, By End User (CAGR), 2025-2035

- Figure 54: Scenario Analysis, Defense Air Platforms Engines Market, Cumulative Market, 2025-2035

- Figure 55: Scenario Analysis, Defense Air Platforms Engines Market, Global Market, 2025-2035

- Figure 56: Scenario 1, Defense Air Platforms Engines Market, Total Market, 2025-2035

- Figure 57: Scenario 1, Defense Air Platforms Engines Market, By Region, 2025-2035

- Figure 58: Scenario 1, Defense Air Platforms Engines Market, By Application, 2025-2035

- Figure 59: Scenario 1, Defense Air Platforms Engines Market, By End User, 2025-2035

- Figure 60: Scenario 2, Defense Air Platforms Engines Market, Total Market, 2025-2035

- Figure 61: Scenario 2, Defense Air Platforms Engines Market, By Region, 2025-2035

- Figure 62: Scenario 2, Defense Air Platforms Engines Market, By Application, 2025-2035

- Figure 63: Scenario 2, Defense Air Platforms Engines Market, By End User, 2025-2035

- Figure 64: Company Benchmark, Defense Air Platforms Engines Market, 2025-2035