|

市场调查报告书

商品编码

1667096

低强度甜味剂市场机会、成长动力、产业趋势分析与 2025 - 2034 年预测Low Intensity Sweeteners Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

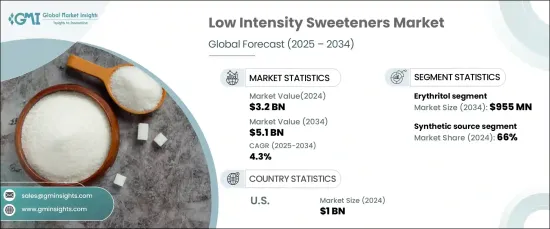

2024 年全球低强度甜味剂市场估值达到 32 亿美元,预计 2025 年至 2034 年期间的复合年增长率为 4.3%。受健康趋势变化和政府支持的减糖措施的推动,食品和饮料行业对减糖和低热量产品的需求强劲。此外,人们对清洁标籤和植物甜味剂的日益偏好正在推动创新,为市场扩张提供了巨大的潜力。

製造商正致力于改善口味、可扩展性和整体产品质量,以满足消费者的需求。生产过程的进步和满足饮食要求的新型甜味剂(如糖尿病患者适用和体重管理产品中的甜味剂)的推出,进一步推动了市场的成长。然而,市场面临挑战,包括监管限制和新兴地区的认知有限。儘管存在这些障碍,人们对永续和健康替代品的日益倾向将使市场在未来十年实现强劲成长。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 32亿美元 |

| 预测值 | 51亿美元 |

| 复合年增长率 | 4.3% |

市场依产品种类细分为赤藻醣醇、麦芽糖醇、木糖醇、d-塔格糖、山梨醇、甘露醇、阿洛酮糖等。其中,赤藻醣醇占据主导地位,2024 年的市场规模为 6.06 亿美元,预计到 2034 年将达到 9.55 亿美元。越来越注重健康的消费者对其的接受度凸显了其在塑造市场轨迹方面所扮演的角色。

根据来源,市场分为天然和合成部分。合成低强度甜味剂由于其成本效益和大规模生产的一致性,将在 2024 年占据 66% 的市场份额。它们在加工食品和饮料中的广泛使用符合了对符合现代饮食偏好的低热量配方日益增长的需求。

美国已成为全球市场的主要贡献者,2024 年的市场规模达到 10 亿美元。鑑于该地区肥胖症和糖尿病发病率不断上升,这种转变尤其重要。

随着消费者需求不断向健康和创新解决方案看齐,低强度甜味剂市场已准备好实现长期成长和多样化。

目录

第 1 章:方法论与范围

- 市场范围和定义

- 基础估算与计算

- 预测计算

- 资料来源

- 基本的

- 次要

- 付费来源

- 公共资源

第 2 章:执行摘要

第 3 章:产业洞察

- 产业生态系统分析

- 影响价值链的因素

- 利润率分析

- 中断

- 未来展望

- 製造商

- 经销商

- 供应商概况

- 利润率分析

- 重要新闻及倡议

- 监管格局

- 衝击力

- 成长动力

- 消费者对更健康替代品的需求不断增加

- 政府法规推动减糖

- 人们对低升糖指数甜味剂的认识不断提高

- 产业陷阱与挑战

- 与余韵相关的潜在问题

- 对食品中甜味剂的安全性和使用的持续审查和不断发展的法规

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第 5 章:市场规模与预测:依产品类型,2021-2034 年

- 主要趋势

- 赤藻醣醇

- 麦芽糖醇

- 木糖醇

- 塔格糖

- 山梨醇

- 甘露醇

- 阿洛酮糖

- 其他的

第 6 章:市场规模与预测:依来源,2021-2034 年

- 主要趋势

- 自然的

- 合成的

第 7 章:市场规模与预测:按应用,2021-2034 年

- 主要趋势

- 食品和饮料

- 药品

- 个人护理

- 其他的

第 8 章:市场规模与预测:按地区,2021-2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 中东及非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第九章:公司简介

- Archer Daniels Midland

- Cargill

- GLG Life Tech

- Hill Pharmaceutical

- Ingredion

- Madhava Natural Sweeteners

- Merisant

- Monk Fruit

- PureCircle

- Roquette Frères

- S&W Seed Company

- Stevia

- Sunwin Stevia

The Global Low Intensity Sweeteners Market achieved a valuation of USD 3.2 billion in 2024 and is poised to grow at a CAGR of 4.3% from 2025 to 2034. This steady growth reflects increasing consumer awareness about the adverse effects of excessive sugar consumption, particularly the rising prevalence of health conditions like diabetes and obesity. The food and beverage industry is witnessing a robust demand for sugar-reduced and calorie-conscious products, fueled by evolving health trends and government-backed initiatives promoting sugar reduction. Additionally, the increasing preference for clean-label and plant-based sweeteners is driving innovation, offering significant potential for market expansion.

Manufacturers are responding to consumer demand by focusing on improving taste profiles, scalability, and overall product quality. Advances in production processes and the introduction of novel sweeteners that cater to dietary requirements, such as those in diabetic-friendly and weight-management products, are further propelling market growth. However, the market faces challenges, including regulatory constraints and limited awareness in emerging regions. Despite these hurdles, the growing inclination toward sustainable and health-oriented alternatives positions the market for strong growth over the next decade.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.2 Billion |

| Forecast Value | $5.1 Billion |

| CAGR | 4.3% |

The market is segmented by product type into erythritol, maltitol, xylitol, d-tagatose, sorbitol, mannitol, allulose, and others. Among these, erythritol stood out as a dominant segment, recording USD 606 million in 2024, with projections to reach USD 955 million by 2034. Erythritol's widespread appeal stems from its natural origin, ability to replicate sugar's taste without influencing blood sugar levels, and digestive-friendly properties. Its increasing adoption among health-conscious consumers underscores its role in shaping the market's trajectory.

By source, the market is categorized into natural and synthetic segments. Synthetic low-intensity sweeteners accounted for 66% of the market share in 2024, driven by their cost efficiency and consistency in large-scale production. Their extensive use in processed foods and beverages aligns with the growing demand for calorie-conscious formulations that meet modern dietary preferences.

The United States emerged as a key contributor to the global market, generating USD 1 billion in 2024. The growing awareness of the health risks linked to high-calorie sweeteners has led American consumers to actively seek alternatives that provide sweetness without compromising health. This shift is particularly relevant given the rising incidence of obesity and diabetes in the region.

As consumer demand continues to align with health-forward and innovative solutions, the low-intensity sweeteners market is well-positioned for long-term growth and diversification.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increasing consumer demand for healthier alternatives

- 3.6.1.2 Government regulations promoting sugar reduction

- 3.6.1.3 Rising awareness of low-glycemic index sweeteners

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 Potential issues related to aftertaste

- 3.6.2.2 Constant scrutiny and evolving regulations regarding the safety and use of sweeteners in food

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Size and Forecast, By Product Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Erythritol

- 5.3 Maltitol

- 5.4 Xylitol

- 5.5 DTagatose

- 5.6 Sorbitol

- 5.7 Mannitol

- 5.8 Allulose

- 5.9 Others

Chapter 6 Market Size and Forecast, By Source, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Natural

- 6.3 Synthetic

Chapter 7 Market Size and Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Food & beverages

- 7.3 Pharmaceuticals

- 7.4 Personal care

- 7.5 Others

Chapter 8 Market Size and Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Archer Daniels Midland

- 9.2 Cargill

- 9.3 GLG Life Tech

- 9.4 Hill Pharmaceutical

- 9.5 Ingredion

- 9.6 Madhava Natural Sweeteners

- 9.7 Merisant

- 9.8 Monk Fruit

- 9.9 PureCircle

- 9.10 Roquette Frères

- 9.11 S&W Seed Company

- 9.12 Stevia

- 9.13 Sunwin Stevia