|

市场调查报告书

商品编码

1667129

原动力往復式发电发动机市场机会、成长动力、产业趋势分析与预测 2025 - 2034Prime Power Reciprocating Power Generating Engine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

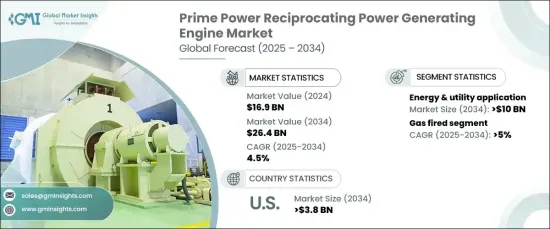

2024 年全球原动力往復式发电发动机市场价值为 169 亿美元,预计 2025-2034 年期间的复合年增长率为 4.5%。这种成长主要由多个领域对可靠、稳定电力的日益增长的需求所推动,包括工业、医疗保健、资料中心和离网地点。这些引擎因其效率、寿命和处理大量功率负载的能力而受到高度评价,使其成为发电应用的首选。

预计能源和公用事业部门将主导市场,到 2034 年收入将达到 100 亿美元。随着基础设施投资的成长和政府主导的电气化计画的不断扩大,对这些引擎的需求将会上升,从而进一步支持市场的扩张。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 169亿美元 |

| 预测值 | 264亿美元 |

| 复合年增长率 | 4.5% |

预计到 2034 年,燃气动力市场的复合年增长率将达到 5%。全球对再生能源的日益重视也在推动对燃气发动机的需求方面发挥了重要作用,燃气发动机具有高转化率、元件优化、燃烧效率高和维护成本低等优点。这些属性有助于这些引擎在各行业中得到更广泛的应用。

预计到 2034 年,美国主要动力往復式发电发动机市场将创收 38 亿美元。现有电网的压力加上不断增长的电力需求,凸显了这些引擎在提供可靠备用电源解决方案方面的重要性。此外,资料中心等关键设施对备用电源的需求不断增长,也推动了这些引擎的采用。人们对可靠电源需求的认识不断提高,进一步提升了市场的成长前景。

随着产业和政府注重确保能源效率和永续性,对原动力往復式发电引擎的需求预计将继续呈上升趋势,在满足日益增长的全球能源需求方面发挥关键作用。

目录

第 1 章:方法论与范围

- 市场范围和定义

- 市场估计和预测参数

- 预测计算

- 资料来源

- 基本的

- 次要

- 有薪资的

- 民众

第 2 章:执行摘要

第 3 章:产业洞察

- 产业生态系统分析

- 监管格局

- 产业衝击力

- 成长动力

- 产业陷阱与挑战

- 成长潜力分析

- 波特的分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- PESTEL 分析

第四章:竞争格局

- 介绍

- 战略展望

- 创新与永续发展格局

第 5 章:市场规模及预测:依燃料类型,2021 – 2034 年

- 主要趋势

- 瓦斯

- 柴油

- 双燃料

- 其他的

第六章:市场规模及预测:依额定功率,2021 – 2034 年

- 主要趋势

- 0.5 兆瓦 - 1 兆瓦

- > 1 兆瓦 - 2 兆瓦

- > 2 兆瓦 - 3.5 兆瓦

- > 3.5 兆瓦 - 5 兆瓦

- > 5 兆瓦 - 7.5 兆瓦

- >7.5兆瓦

第 7 章:市场规模与预测:按应用,2021 – 2034 年

- 主要趋势

- 工业的

- 热电联产

- 能源与公用事业

- 垃圾掩埋场和沼气

- 其他的

第 8 章:市场规模与预测:按地区,2021 – 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 英国

- 法国

- 德国

- 俄罗斯

- 义大利

- 西班牙

- 荷兰

- 丹麦

- 挪威

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 泰国

- 新加坡

- 印尼

- 马来西亚

- 中东和非洲

- 阿联酋

- 沙乌地阿拉伯

- 卡达

- 阿曼

- 科威特

- 伊朗

- 埃及

- 土耳其

- 约旦

- 南非

- 拉丁美洲

- 巴西

- 阿根廷

- 智利

- 秘鲁

第九章:公司简介

- AB Volvo Penta

- Caterpillar

- Cummins

- Deere & Company

- DEUTZ AG

- Kirloskar

- KUBOTA Corporation

- MITSUBISHI HEAVY INDUSTRIES

- Perkins Engines Company

- Rehlko

- Rolls-Royce

- Sulzer

- Wartsila

- YANMAR HOLDINGS

- Yuchai International

The Global Prime Power Reciprocating Power Generating Engines Market was valued at USD 16.9 billion in 2024 and is projected to grow at a CAGR of 4.5% during 2025-2034. This growth is primarily driven by the increasing need for reliable, constant power across several sectors, including industries, healthcare, data centers, and off-grid locations. These engines are highly regarded for their efficiency, longevity, and capacity to handle substantial power loads, making them a favored choice in power generation applications.

The energy and utility sector is expected to dominate the market, with revenues generating USD 10 billion by 2034. These engines are gaining traction as prime movers due to their ability to achieve impressive electrical efficiencies-over 50% in a single cycle and up to 70% in combined cycles. As investments in infrastructure grow and government-led electrification initiatives continue to expand, the demand for these engines is set to rise, further supporting the market's expansion.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $16.9 Billion |

| Forecast Value | $26.4 Billion |

| CAGR | 4.5% |

The gas-powered segment of the market is forecast to grow at a CAGR of 5% through 2034. This is attributed to technological advancements that enhance engine performance and efficiency, as well as the increasing need to adhere to stringent environmental regulations. The growing global emphasis on renewable energy sources has also played a significant role in driving the demand for gas-fired engines, which offer benefits such as high translation, optimized elements, efficient combustion, and low maintenance. These attributes contribute to the broader adoption of these engines across various industries.

U.S. prime power reciprocating power generating engine market is anticipated to generate USD 3.8 billion by 2034. Factors contributing to this growth include the increasing need for uninterrupted power and the growing frequency of power disruptions due to extreme weather events. The strain on existing electrical grids, coupled with the rising electricity demand, has underscored the importance of these engines in providing a reliable backup power solution. Additionally, the growing demand for backup power in critical facilities, such as data centers, is driving the adoption of these engines. Increased awareness of the need for reliable power sources further boosts the market's growth prospects.

As industries and governments focus on ensuring energy efficiency and sustainability, the demand for prime power reciprocating power generating engines is expected to continue its upward trajectory, playing a crucial role in meeting the growing global energy demands.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Strategic outlook

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Fuel Type, 2021 – 2034 (Units, MW & USD Million)

- 5.1 Key trends

- 5.2 Gas-fired

- 5.3 Diesel-fired

- 5.4 Dual fuel

- 5.5 Others

Chapter 6 Market Size and Forecast, By Rated Power, 2021 – 2034 (Units, MW & USD Million)

- 6.1 Key trends

- 6.2 0.5 MW - 1 MW

- 6.3 > 1 MW - 2 MW

- 6.4 > 2 MW - 3.5 MW

- 6.5 > 3.5 MW - 5 MW

- 6.6 > 5 MW - 7.5 MW

- 6.7 > 7.5 MW

Chapter 7 Market Size and Forecast, By Application, 2021 – 2034 (Units, MW & USD Million)

- 7.1 Key trends

- 7.2 Industrial

- 7.3 CHP

- 7.4 Energy & utility

- 7.5 Landfill & biogas

- 7.6 Others

Chapter 8 Market Size and Forecast, By Region, 2021 – 2034 (Units, MW & USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 France

- 8.3.3 Germany

- 8.3.4 Russia

- 8.3.5 Italy

- 8.3.6 Spain

- 8.3.7 Netherlands

- 8.3.8 Denmark

- 8.3.9 Norway

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.4.6 Thailand

- 8.4.7 Singapore

- 8.4.8 Indonesia

- 8.4.9 Malaysia

- 8.5 Middle East & Africa

- 8.5.1 UAE

- 8.5.2 Saudi Arabia

- 8.5.3 Qatar

- 8.5.4 Oman

- 8.5.5 Kuwait

- 8.5.6 Iran

- 8.5.7 Egypt

- 8.5.8 Turkey

- 8.5.9 Jordan

- 8.5.10 South Africa

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

- 8.6.3 Chile

- 8.6.4 Peru

Chapter 9 Company Profiles

- 9.1 AB Volvo Penta

- 9.2 Caterpillar

- 9.3 Cummins

- 9.4 Deere & Company

- 9.5 DEUTZ AG

- 9.6 Kirloskar

- 9.7 KUBOTA Corporation

- 9.8 MITSUBISHI HEAVY INDUSTRIES

- 9.9 Perkins Engines Company

- 9.10 Rehlko

- 9.11 Rolls-Royce

- 9.12 Sulzer

- 9.13 Wartsila

- 9.14 YANMAR HOLDINGS

- 9.15 Yuchai International

2026年全球柴油引擎市场报告2026年全球往復式发电发动机市场报告

2026年全球柴油引擎市场报告2026年全球往復式发电发动机市场报告 柴油动力引擎市场-全球产业规模、份额、趋势、机会与预测:按类型、估值、应用、产业垂直领域、地区和竞争格局划分,2021-2031年

柴油动力引擎市场-全球产业规模、份额、趋势、机会与预测:按类型、估值、应用、产业垂直领域、地区和竞争格局划分,2021-2031年 柴油引擎市场规模、份额和成长分析(按运转类型、额定功率、转速和地区划分)—产业预测(2026-2033 年)

柴油引擎市场规模、份额和成长分析(按运转类型、额定功率、转速和地区划分)—产业预测(2026-2033 年) 往復式发电发动机市场机会、成长驱动因素、产业趋势分析及预测(2026-2035年)

往復式发电发动机市场机会、成长驱动因素、产业趋势分析及预测(2026-2035年) 柴油引擎:全球市场份额和排名、总销售量和需求预测(2025-2031年)

柴油引擎:全球市场份额和排名、总销售量和需求预测(2025-2031年) 柴油引擎市场按应用、功率输出、技术、冷却方式、汽缸数和排放气体标准划分-2025-2032年全球预测备用往復式发电发动机市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

柴油引擎市场按应用、功率输出、技术、冷却方式、汽缸数和排放气体标准划分-2025-2032年全球预测备用往復式发电发动机市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 柴油引擎:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)

柴油引擎:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年) 2030 年柴油引擎市场预测:按燃料类型、引擎类型、零件、应用和地区进行的全球分析

2030 年柴油引擎市场预测:按燃料类型、引擎类型、零件、应用和地区进行的全球分析