|

市场调查报告书

商品编码

1687308

柴油引擎:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)Diesel Power Engine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

价格

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

简介目录

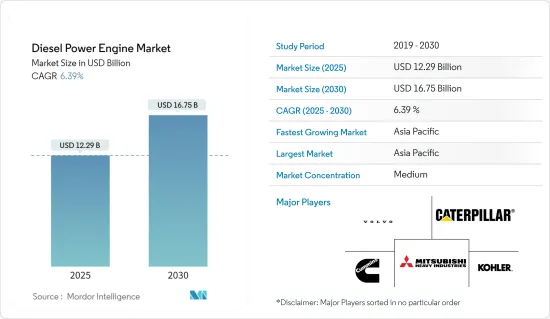

预计 2025 年柴油引擎市场规模为 122.9 亿美元,到 2030 年预计将达到 167.5 亿美元,预测期内(2025-2030 年)的复合年增长率为 6.39%。

主要亮点

- 从中期来看,工业部门需求增加、停电次数增加等因素正在增加对柴油发电机的需求,进而推动柴油引擎市场的发展。

- 然而,由于天然气丰富且环保,各终端用户行业越来越多地转向使用天然气燃气引擎代替柴油发动机,预计这将在预测期内抑制柴油发动机市场的成长。

- 然而,混合动力柴油发电机的日益普及将为未来几年柴油引擎市场的参与者提供巨大的机会。

- 亚太地区预计将成为最大且成长最快的市场,其中大部分需求来自印度和中国等国家。

柴油引擎市场趋势

工业领域占市场主导地位

- *柴油发电是工业部门最适合的备用电源。一般来说,工业部门在其业务运作中消耗大量电力。柴油动力引擎可靠并提高了供电品质。

- *全球范围内的电力需求正在增加。工业的快速扩张和商业基础设施的发展导致柴油引擎的使用率增加。严重依赖柴油发电的关键产业包括建筑业、製造业、医疗保健、石油和天然气、通讯和资料中心。

- 柴油发电机配备了先进的技术,可以监控电流,如果电源出现任何失真或干扰,它将自动启动,并在电源恢復时返回关闭模式。

- 柴油引擎挥发性低,是采矿业的理想选择。重型工作,特别是在采矿业,需要完美的电力和备用电源。这就是采矿业依赖耐用柴油引擎的原因。在医疗保健领域,氧合器、输液帮浦、心电图机和心臟去颤器等精密设备用于治疗患者。需要高品质的电源来避免中断。柴油引擎是医院最可靠的备用电源,能够提供不间断的电力。

- 在建筑业,停电常常会导致计划停滞。长时间停电将延迟计划实施并导致财务损失。为了提高施工现场的安全性和电力供应,需要柴油引擎。

- 製造业停电导致产量下降和产品交付不合格。当製造业发生停电时,通常会影响所有营运。因此,为了避免此类障碍,生产单位选择使用柴油引擎作为首选动力来源。

- 此外,钢铁业使用柴油引擎来满足电力需求或作为停电时的备用电源。根据世界钢铁协会统计,截至2022年12月,中国是全球最大的粗钢生产国,产量为7,790万吨,年减与前一年同期比较%。印度、日本、美国和俄罗斯则远远落后。

- 因此,由于上述因素,预计预测期内柴油引擎市场将由工业部门主导。

亚太地区占市场主导地位

- 亚太地区基础设施建设和电力需求的不断增长,以及平均能源消耗率和 GDP 成长率的大幅增加,预计将推动柴油动力引擎市场的发展。

- 由于计划不断增加、电力供需缺口不断扩大、全国范围内製造设施的扩张以及商业办事处的不断增长,中国引领亚太柴油发电机市场。

- 中国的建设产业是世界上最大的建筑业之一,过去几十年经历了显着的成长。中国的快速工业化带动了建设活动的激增,包括住宅、商业和基础设施建设。随着新计划的推进,中国经济开始从新冠肺炎疫情的影响中復苏。

- 2023年4月,中国政府宣布将与前一年同期比较增1.8兆美元的大型建筑和计划支出,以协助地区经济从疫情中復苏。建设活动的扩大需要由柴油引擎驱动的机械,这有望推动市场成长。

- 印度政府致力于透过开放的外商直接投资规范、智慧城市计画和对基础设施领域的大量预算拨款等重点政策来发展基础设施和建筑服务。 2023 年 1 月,政府和建筑业发展委员会 (CIDC)核准在该国开发 21 个待开发区机场。建筑业的成长将需要备用柴油发电机,为市场发展铺平了道路。

- 在智慧城市使命下,截至 2022 年 11 月,PMAY-U 使命已批准超过 1,200 万住宅,其中超过 640 万套已经完工。其余均处于不同建设和施工阶段。截至 2024 年,AMRUT 2.0 任务下正在进行的计划有 177.42 个,总价值为 8.5512 亿美元,包括水体復原、供水、排污以及公园和绿地开发。印度的许多住宅都配备了柴油发电机(DG),以便在停电时提供电力。因此,预计预测期内柴油引擎的需求将会增加。

- 此外,製造业蓬勃发展带来的能源需求不断增加,预计将为亚太地区的发电业务提供巨大推动力。因此,预计预测期内亚太地区将见证全球柴油引擎市场最快的成长。

柴油引擎产业概况

柴油引擎市场半分散。市场的主要企业(不分先后顺序)包括卡特彼勒公司、康明斯公司、科勒公司、沃尔沃公司和三菱重工有限公司。

其他福利

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究范围

- 市场定义

- 调查前提

第二章调查方法

第三章执行摘要

第四章 市场概况

- 介绍

- 2029 年市场规模与需求预测

- 最新趋势和发展

- 政府法规和政策

- 市场动态

- 驱动程式

- 工业部门需求增加

- 由于停电次数增加,柴油发电机的需求增加

- 限制因素

- 越来越多地转向清洁能源

- 驱动程式

- 供应链分析

- 波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场区隔

- 按最终用户

- 产业

- 商业的

- 住宅

- 按应用

- 支援

- 主要的

- 抑低尖峰负载

- 按地区

- 北美洲

- 美国

- 加拿大

- 北美其他地区

- 欧洲

- 英国

- 法国

- 德国

- 西班牙

- 其他欧洲国家

- 亚太地区

- 中国

- 印度

- 东南亚国协

- 澳洲

- 其他亚太地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 奈及利亚

- 南非

- 其他中东和非洲地区

- 北美洲

第六章 竞争格局

- 併购、合资、合作、协议

- 主要企业策略

- 公司简介

- Caterpillar Inc.

- Cummins Inc.

- Kohler Co

- Volvo AB

- Mitsubishi Heavy Industries Ltd

- Wartsila Oyj Abp

- Hyundai Heavy Industries Co. Ltd

- Man SE

- Rolls-Royce Holding PLC

- YANMAR HOLDINGS Co. Ltd

- Market Ranking/Share(%)Analysis

第七章 市场机会与未来趋势

- 混合柴油发电机越来越受欢迎

简介目录

Product Code: 61049

The Diesel Power Engine Market size is estimated at USD 12.29 billion in 2025, and is expected to reach USD 16.75 billion by 2030, at a CAGR of 6.39% during the forecast period (2025-2030).

Key Highlights

- Over the medium period, factors such as the increasing demand from the industrial sector and rising power outages have increased the demand for diesel generators, thereby driving the diesel power engine market.

- On the other hand, the abundance of natural gas, coupled with its environmental soundness, has led to an increasing shift toward natural gas engines as an alternative to diesel engines in various end-user industries and is expected to restrain the growth of the diesel engine market during the forecast period.

- Nevertheless, the increasing popularity of hybrid power diesel generators presents immense opportunities for the diesel power engine market players in the coming years.

- Asia-Pacific is expected to be the largest and fastest-growing market, with the majority of the demand coming from countries like India and China.

Diesel Power Engine Market Trends

The Industrial Segment to Dominate the Market

- * Diesel power generation is the most appropriate standby source for the industrial sector. Generally, the industrial sector consumes more power for its business operations. A diesel power engine offers better reliability and enhances the quality of the power supply.

- * The demand for electricity is growing worldwide. Rapid industrial expansions and commercial infrastructure development are increasing the utilization of diesel power engines. Significant industries that rely heavily on the power generated from diesel engines are the construction sector, manufacturing, health care, oil and gas, telecommunication and data centers, etc.

- Diesel generators are equipped with advanced technologies for monitoring electric current, which help automatically start when there are power distortions and failures and revert to switch-off mode when the power comes back.

- The diesel engine's low volatility rate makes it the finest option in mining fields. Especially in mining fields, heavy-duty activities need a perfect power source and backup. Hence, mining industries rely on diesel-powered engines for better durability. The healthcare segment uses sensitive equipment such as oxygen ventilators, infusion pumps, ECG machines, and defibrillators to treat patients. There is a need for a quality power supply to avoid interruptions. Diesel power engines are hospitals' most reliable backup power sources for uninterrupted power.

- In the construction sector, projects often stall due to power failures. Constant power interruptions result in delayed project execution, which leads to financial loss. There is a need for a diesel power engine to ensure safety and better power supply on construction sites.

- Disruptions of power in the manufacturing industry lead to low-volume production and result in the offering of low-standard products. When a blackout occurs in manufacturing divisions, it generally affects all the processes. Hence, the production units rely on the diesel power engine to avoid such failures, which acts as the best power source.

- The iron and steel industry also uses diesel power engines as backup power in case of power requirements or power shutdown. According to the World Steel Association, as of December 2022, China was the world leader in crude steel production, with 77.9 million metric tonnes produced, a 10% decrease from the previous year. India, Japan, the United States, and Russia trailed far behind.

- Therefore, based on the abovementioned factors, the industrial segment is expected to dominate the diesel power engine market during the forecast period.

Asia-Pacific to Dominate the Market

- The increasing infrastructural developments and electricity demand in Asia-Pacific, with the huge increase in average energy consumption rate and GDP growth rate, are expected to promulgate the diesel power engine market.

- China is the leading diesel generator market in Asia-Pacific owing to increasing infrastructure projects, widening power demand-supply gap, expanding manufacturing facilities across the nation, and rising commercial office spaces.

- The construction industry in China, one of the largest in the world, has experienced significant growth over the last few decades. Rapid industrialization in China has led to a surge in construction activities, including residential, commercial, and infrastructure construction. The Chinese economy is beginning to recover from the effects of the COVID-19 pandemic as new projects are pushed forward.

- In April 2023, the Chinese government announced that it was set to increase its spending on large construction and infrastructure projects by USD 1.8 trillion Y-o-Y to help regional economies recover from the pandemic. The growing construction activities require machinery fitted with diesel engines; this is expected to promote the growth of the market.

- The Indian government has been focusing on developing infrastructure and construction services through focused policies such as open FDI norms, smart city missions, and large budget allocation to the infrastructure sector. In January 2023, the government and the Construction Industry Development Council (CIDC) approved the development of 21 greenfield airports in the country. The growth in the construction sector will, in turn, need diesel generators to power backup, which will create avenues for the development of the market.

- Under the Smart City Mission, as of November 2022, more than 12.0 million houses were sanctioned under the PMAY-U Mission, out of which more than 6.4 million were completed. The rest are in various stages of construction/grounding. As of 2024, 1174 projects worth USD 855.12 million of Water Body Rejuvenation, Water Supply, Sewage & Sewage Management, and Parks & Green Space Development are ongoing under the AMRUT 2.0 mission. Many of the residential societies in India are equipped with diesel generator (DG) sets to supply electricity during power outages. Thus, such commitments are expected to increase the demand for diesel engines during the forecast period.

- Moreover, the growing energy demands of the burgeoning manufacturing industry are expected to provide a huge impetus to the generator business in Asia-Pacific. As a result, Asia-Pacific is expected to witness the fastest growth in the global diesel power engine market during the forecast period.

Diesel Power Engine Industry Overview

The diesel power engine market is semi fragmented. Some of the key players in this market (in no particular order) include Caterpillar Inc., Cummins Inc., Kohler Co., Volvo AB, and Mitsubishi Heavy Industries Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Demand From Industrial Sector

- 4.5.1.2 Rising Power Outages To Increase The Demand For Diesel Generators

- 4.5.2 Restraints

- 4.5.2.1 Increasing Shift Toward Cleaner Energy Resources

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By End User

- 5.1.1 Industrial

- 5.1.2 Commercial

- 5.1.3 Residential

- 5.2 By Application

- 5.2.1 Standby

- 5.2.2 Prime

- 5.2.3 Peak Shaving

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 France

- 5.3.2.3 Germany

- 5.3.2.4 Spain

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 ASEAN Countries

- 5.3.3.4 Australia

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 Nigeria

- 5.3.5.3 South Africa

- 5.3.5.4 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Caterpillar Inc.

- 6.3.2 Cummins Inc.

- 6.3.3 Kohler Co

- 6.3.4 Volvo AB

- 6.3.5 Mitsubishi Heavy Industries Ltd

- 6.3.6 Wartsila Oyj Abp

- 6.3.7 Hyundai Heavy Industries Co. Ltd

- 6.3.8 Man SE

- 6.3.9 Rolls-Royce Holding PLC

- 6.3.10 YANMAR HOLDINGS Co. Ltd

- 6.4 Market Ranking/Share (%) Analysis

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Popularity Of Hybrid Power Diesel Generators

02-2729-4219

+886-2-2729-4219

全球柴油引擎市场分析及预测(至2032年)

全球柴油引擎市场分析及预测(至2032年) 2026年全球主用往復式发电发动机市场报告2026年全球柴油引擎市场报告2026年全球往復式发电发动机市场报告

2026年全球主用往復式发电发动机市场报告2026年全球柴油引擎市场报告2026年全球往復式发电发动机市场报告 柴油动力引擎市场-全球产业规模、份额、趋势、机会与预测:按类型、估值、应用、产业垂直领域、地区和竞争格局划分,2021-2031年

柴油动力引擎市场-全球产业规模、份额、趋势、机会与预测:按类型、估值、应用、产业垂直领域、地区和竞争格局划分,2021-2031年 柴油引擎市场规模、份额和成长分析(按运转类型、额定功率、转速和地区划分)—产业预测(2026-2033 年)

柴油引擎市场规模、份额和成长分析(按运转类型、额定功率、转速和地区划分)—产业预测(2026-2033 年) 往復式发电发动机市场机会、成长驱动因素、产业趋势分析及预测(2026-2035年)

往復式发电发动机市场机会、成长驱动因素、产业趋势分析及预测(2026-2035年) 柴油引擎:全球市场份额和排名、总销售量和需求预测(2025-2031年)备用往復式发电发动机市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

柴油引擎:全球市场份额和排名、总销售量和需求预测(2025-2031年)备用往復式发电发动机市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 2030 年柴油引擎市场预测:按燃料类型、引擎类型、零件、应用和地区进行的全球分析

2030 年柴油引擎市场预测:按燃料类型、引擎类型、零件、应用和地区进行的全球分析

▼