|

市场调查报告书

商品编码

1750587

备用往復式发电发动机市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Backup Reciprocating Power Generating Engine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

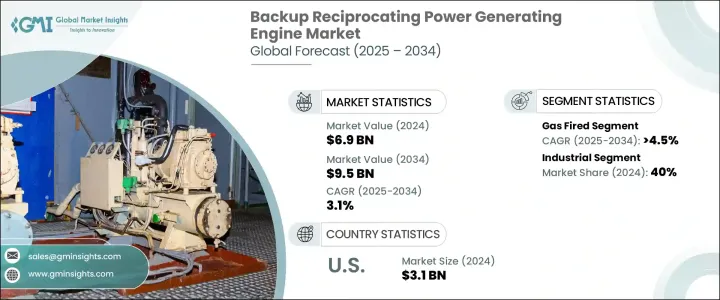

2024年,全球备用往復式发电引擎市值为69亿美元,预计到2034年将以3.1%的复合年增长率成长,达到95亿美元,这主要得益于对可靠备用电源系统的需求。向分散式能源发电的转变,尤其是在偏远地区,正在进一步扩大市场规模。这些引擎对于确保易受电力中断影响的地区(尤其是偏远或电力脆弱地区)的稳定供电至关重要。除了提供紧急电源外,备用往復式引擎对于在电力可靠性至关重要的行业中维持营运连续性也变得越来越重要。

发展中经济体电力供应波动性加剧,灾害频传地区能源需求不断成长,预计将推动备用电源系统的普及。此外,物联网 (IoT) 引擎的整合正在增强系统智能,促进预测性维护,从而提升关键和远端应用的效能。更严格的排放法规以及工业领域对备用电源日益增长的需求也促进了市场扩张。不断变化的监管环境,包括对进口零件征收关税,可能会影响国际贸易,并增加备用发电发动机的生产成本。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 69亿美元 |

| 预测值 | 95亿美元 |

| 复合年增长率 | 3.1% |

预计到2034年,燃气备用往復式发电发动机市场将以4.5%的复合年增长率强劲增长,这得益于更严格的环境法规和天然气价格日益亲民的推动,使其成为传统发电方式的可行且可持续的替代方案。与传统的化石燃料发电机相比,燃气备用往復式发电发动机效率更高、排放更低,具有显着优势,因此成为寻求减少碳足迹同时保持可靠电力供应的行业的首选。

此外,预计热电联产 (CHP) 系统将实现显着成长,到 2034 年的复合年增长率将达到 4.5%。对节能解决方案的需求不断增长,以及企业降低燃料消耗和营运成本的动力是推动这一趋势的关键因素。热电联产系统尤其受到重视,因为它能够同时发电并收集余热用于供暖,从而提高能源效率并降低整体营运成本。

2024年,美国备用往復式发电机市场规模达31亿美元,反映出对可靠电力日益增长的需求。这一增长主要归因于美国老化电网基础设施的现代化改造,以及对备用系统的需求,以确保在停电期间持续供电。此外,各行各业对节能技术的日益普及,加上商业和工业活动的扩张,预计将推动市场进一步成长。

全球备用往復式发电引擎市场的主要参与者正专注于产品创新和市场扩张,以巩固其市场地位。劳斯莱斯、曼恩能源解决方案和瓦锡兰等公司正加大研发投入,以提高引擎性能和燃油效率。他们还利用策略合作伙伴关係和收购来进入新的区域市场并增强产品供应。此外,各公司正致力于永续发展,开发符合严格排放标准的引擎。这些策略正被用于满足各行各业对可靠、环保的动力解决方案日益增长的需求。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 川普政府关税分析

- 对贸易的影响

- 贸易量中断

- 报復措施

- 对产业的影响

- 供应方影响(原料)

- 主要材料价格波动

- 供应链重组

- 生产成本影响

- 需求面影响(售价)

- 价格传导至终端市场

- 市占率动态

- 消费者反应模式

- 供应方影响(原料)

- 受影响的主要公司

- 策略产业反应

- 供应链重组

- 定价和产品策略

- 政策参与

- 展望与未来考虑

- 对贸易的影响

- 监管格局

- 产业衝击力

- 成长动力

- 产业陷阱与挑战

- 成长潜力分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 战略展望

- 创新与永续发展格局

第五章:市场规模及预测:依燃料类型,2021 - 2034

- 主要趋势

- 瓦斯

- 柴油引擎

- 双燃料

- 其他的

第六章:市场规模及预测:依额定功率,2021 - 2034

- 主要趋势

- 0.5 兆瓦 - 1 兆瓦

- > 1 兆瓦 - 2 兆瓦

- > 2 兆瓦 - 3.5 兆瓦

- > 3.5 兆瓦 - 5 兆瓦

- > 5 兆瓦 - 7.5 兆瓦

- > 7.5 兆瓦

第七章:市场规模及预测:依应用,2021 - 2034

- 主要趋势

- 工业的

- 热电联产

- 能源与公用事业

- 垃圾掩埋场和沼气

- 其他的

第八章:市场规模及预测:按地区,2021 - 2034

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 英国

- 法国

- 德国

- 俄罗斯

- 义大利

- 西班牙

- 荷兰

- 丹麦

- 挪威

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 泰国

- 新加坡

- 印尼

- 马来西亚

- 中东和非洲

- 阿联酋

- 沙乌地阿拉伯

- 卡达

- 阿曼

- 科威特

- 伊朗

- 埃及

- 土耳其

- 约旦

- 南非

- 拉丁美洲

- 巴西

- 阿根廷

- 智利

- 秘鲁

第九章:公司简介

- AB Volvo Penta

- Atlas Copco

- Caterpillar

- Clarke Energy

- GE Vernova

- HIMOINSA

- Kirloskar

- MAN Energy Solutions

- Mitsubishi Heavy Industries

- Motorenfabrik Hatz

- Rehlko

- Rolls-Royce

- Scania

- Wartsilä

- Yamaha Motor

- Yuchai International

The Global Backup Reciprocating Power Generating Engine Market was valued at USD 6.9 billion in 2024 and is estimated to grow at a CAGR of 3.1% to reach USD 9.5 billion by 2034, driven by the demand for reliable backup power systems. The shift toward decentralized energy generation, particularly in remote areas, is further expanding the market. These engines are vital for ensuring a consistent power supply in areas prone to electrical disruptions, especially in isolated or vulnerable locations. In addition to providing emergency power, backup reciprocating engines are becoming increasingly important for maintaining operational continuity in industries where power reliability is critical.

The growing volatility of electricity supply in developing economies and the increasing need for energy in disaster-prone regions are expected to fuel the adoption of backup power systems. Furthermore, the integration of Internet of Things (IoT)-enabled engines is enhancing system intelligence and facilitating predictive maintenance, thus improving the performance of critical and remote applications. Stricter emission regulations and the rising demand for standby power in industrial sectors also contribute to market expansion. The evolving regulatory landscape, including tariffs on imported parts, may impact international trade and increase production costs for backup power-generating engines.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.9 Billion |

| Forecast Value | $9.5 Billion |

| CAGR | 3.1% |

The gas-fired backup reciprocating power generating engine market is projected to grow at a robust CAGR of 4.5% through 2034, driven by stricter environmental regulations and the increasing affordability of natural gas, making it a viable and sustainable alternative to traditional power generation methods. These engines offer a compelling advantage due to their higher efficiency and lower emissions compared to conventional fossil-fuel-powered generators, making them a preferred choice for industries looking to reduce their carbon footprint while maintaining a reliable power supply.

In addition to this, Combined Heat and Power (CHP) systems are expected to see notable growth, with an anticipated CAGR of 4.5% through 2034. The rising demand for energy-efficient solutions and the push for businesses to lower their fuel consumption and operating costs are key factors contributing to this trend. CHP systems are particularly valued for their ability to simultaneously generate electricity and capture waste heat for use in heating, thereby improving energy efficiency and reducing overall operational costs.

United States Backup Reciprocating Power Generating Engine Market was valued at USD 3.1 billion in 2024, reflecting the increasing demand for dependable electricity. This surge is largely attributed to the modernization of the nation's aging grid infrastructure and the need for backup systems to ensure continuous power during outages. Additionally, the growing adoption of energy-efficient technologies across various sectors, coupled with the expansion of commercial and industrial activities, is expected to drive further growth in the market.

Key players in the Global Backup Reciprocating Power Generating Engine Market are focusing on product innovation and market expansion to strengthen their positions. Companies like Rolls-Royce, MAN Energy Solutions, and Wartsila are increasingly investing in research and development to improve engine performance and fuel efficiency. Strategic partnerships and acquisitions are also being utilized to enter new regional markets and enhance product offerings. Additionally, firms are focusing on sustainability by developing engines that comply with stringent emission standards. These strategies are being adopted to meet the growing demand for reliable, environmentally friendly power solutions across various industries.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Regulatory landscape

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Strategic outlook

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Fuel Type, 2021 - 2034 (USD Million, MW & Units)

- 5.1 Key trends

- 5.2 Gas-fired

- 5.3 Diesel-fired

- 5.4 Dual fuel

- 5.5 Others

Chapter 6 Market Size and Forecast, By Rated Power, 2021 - 2034 (USD Million, MW & Units)

- 6.1 Key trends

- 6.2 0.5 MW - 1 MW

- 6.3 > 1 MW - 2 MW

- 6.4 > 2 MW - 3.5 MW

- 6.5 > 3.5 MW - 5 MW

- 6.6 > 5 MW - 7.5 MW

- 6.7 > 7.5 MW

Chapter 7 Market Size and Forecast, By Application, 2021 - 2034 (USD Million, MW & Units)

- 7.1 Key trends

- 7.2 Industrial

- 7.3 CHP

- 7.4 Energy & utility

- 7.5 Landfill & biogas

- 7.6 Others

Chapter 8 Market Size and Forecast, By Region, 2021 - 2034 (USD Million, MW & Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 France

- 8.3.3 Germany

- 8.3.4 Russia

- 8.3.5 Italy

- 8.3.6 Spain

- 8.3.7 Netherlands

- 8.3.8 Denmark

- 8.3.9 Norway

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.4.6 Thailand

- 8.4.7 Singapore

- 8.4.8 Indonesia

- 8.4.9 Malaysia

- 8.5 Middle East & Africa

- 8.5.1 UAE

- 8.5.2 Saudi Arabia

- 8.5.3 Qatar

- 8.5.4 Oman

- 8.5.5 Kuwait

- 8.5.6 Iran

- 8.5.7 Egypt

- 8.5.8 Turkey

- 8.5.9 Jordan

- 8.5.10 South Africa

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

- 8.6.3 Chile

- 8.6.4 Peru

Chapter 9 Company Profiles

- 9.1 AB Volvo Penta

- 9.2 Atlas Copco

- 9.3 Caterpillar

- 9.4 Clarke Energy

- 9.5 GE Vernova

- 9.6 HIMOINSA

- 9.7 Kirloskar

- 9.8 MAN Energy Solutions

- 9.9 Mitsubishi Heavy Industries

- 9.10 Motorenfabrik Hatz

- 9.11 Rehlko

- 9.12 Rolls-Royce

- 9.13 Scania

- 9.14 Wartsilä

- 9.15 Yamaha Motor

- 9.16 Yuchai International

全球柴油引擎市场分析及预测(至2032年)

全球柴油引擎市场分析及预测(至2032年) 2026年全球主用往復式发电发动机市场报告2026年全球柴油引擎市场报告2026年全球往復式发电发动机市场报告

2026年全球主用往復式发电发动机市场报告2026年全球柴油引擎市场报告2026年全球往復式发电发动机市场报告 柴油动力引擎市场-全球产业规模、份额、趋势、机会与预测:按类型、估值、应用、产业垂直领域、地区和竞争格局划分,2021-2031年

柴油动力引擎市场-全球产业规模、份额、趋势、机会与预测:按类型、估值、应用、产业垂直领域、地区和竞争格局划分,2021-2031年 柴油引擎市场规模、份额和成长分析(按运转类型、额定功率、转速和地区划分)—产业预测(2026-2033 年)

柴油引擎市场规模、份额和成长分析(按运转类型、额定功率、转速和地区划分)—产业预测(2026-2033 年) 往復式发电发动机市场机会、成长驱动因素、产业趋势分析及预测(2026-2035年)

往復式发电发动机市场机会、成长驱动因素、产业趋势分析及预测(2026-2035年) 柴油引擎:全球市场份额和排名、总销售量和需求预测(2025-2031年)

柴油引擎:全球市场份额和排名、总销售量和需求预测(2025-2031年) 柴油引擎:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)

柴油引擎:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年) 2030 年柴油引擎市场预测:按燃料类型、引擎类型、零件、应用和地区进行的全球分析

2030 年柴油引擎市场预测:按燃料类型、引擎类型、零件、应用和地区进行的全球分析