|

市场调查报告书

商品编码

1684712

汽车并联混合动力系统市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Automotive Parallel Hybrid Power System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

2024 年全球汽车并联混合动力系统市场价值为 632 亿美元,预计 2025 年至 2034 年期间的复合年增长率为 8.2%。随着人们越来越重视减少温室气体排放和提高燃油效率,市场正在见证巨大的发展动能。世界各国政府正在实施严格的法规并提供激励措施,以加速混合动力电动车 (HEV) 的普及。这些政策,包括减税、补贴和对电动车基础设施的投资,使得混合动力技术更容易获得,也更受消费者的青睐。此外,燃料价格上涨和永续发展意识的增强也推动消费者青睐节能的行动解决方案。

汽车製造商正在迅速扩大其混合动力汽车产品组合,以满足不断变化的监管标准和消费者期望。再生煞车系统和优化电池性能等先进动力总成技术的日益融合,进一步提高了混合动力汽车的效率和吸引力。随着混合动力系统不断缩小传统内燃机(ICE)汽车与全电动替代品之间的差距,其在全球市场的采用预计将激增。混合动力车型日益增多且价格具有竞争力,也促进了市场成长,特别是在电动车充电基础设施仍不发达的地区。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 632亿美元 |

| 预测值 | 1357亿美元 |

| 复合年增长率 | 8.2% |

市场细分为关键零件,包括电动马达、内燃机、电池、电力电子和传动系统。内燃机领域仍占据主导地位,到 2024 年将占 39% 的市场。儘管向电气化转变,但基于 ICE 的混合动力系统在向更清洁的交通运输过渡过程中仍然发挥关键作用。汽油和柴油加油基础设施的经济性和广泛可用性使混合动力汽车成为实用的选择,尤其是在发展中经济体。到 2034 年,在燃油效率和减排技术进步的推动下,内燃机汽车市场的规模预计将超过 500 亿美元。

根据车辆类型,汽车并联混合动力系统市场分为两轮车、乘用车和商用车。由于消费者优先考虑省油且经济高效的交通解决方案,乘用车在 2024 年占据了 64% 的市场份额。城市地区对混合动力乘用车的需求尤其强劲,因为交通拥堵和燃料成本使得能源效率成为首要考虑因素。汽车製造商正在推出创新的混合动力车型,这些车型具有改进的动力系统性能、更长的电池寿命和无缝整合的智慧技术,对于寻求性能和永续性之间平衡的消费者来说,它们越来越有吸引力。

美国仍然是汽车并联混合动力系统最大的市场,到 2024 年将占据总市场份额的 78%。该国广泛的公路网络、强大的基础设施以及消费者对燃油效率的日益增强的意识是推动采用的关键因素。随着国内製造商在混合动力汽车创新方面处于领先地位,美国继续成为永续交通技术进步的主要枢纽。随着混合动力汽车需求的不断增长,汽车製造商正在大力投资研发,以改善混合动力系统、提高能源效率并提供传统汽油动力汽车的经济高效的替代品。

目录

第 1 章:方法论与范围

- 研究设计

- 研究方法

- 资料收集方法

- 基础估计和计算

- 基准年计算

- 市场估计的主要趋势

- 预测模型

- 初步研究与验证

- 主要来源

- 资料探勘来源

- 市场定义

第 2 章:执行摘要

第 3 章:产业洞察

- 产业生态系统分析

- 原物料供应商

- 製造商

- 分销管道

- 服务提供者

- 最终用户

- 供应商概况

- 利润率分析

- 技术与创新格局

- 案例研究

- 重要新闻及倡议

- 监管格局

- 衝击力

- 成长动力

- 政府法规和激励措施

- 燃料价格上涨和成本效率

- 增强环保意识

- 技术进步

- 产业陷阱与挑战

- 电池寿命有限和回收问题

- 全电动汽车竞争激烈

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第五章:市场估计与预测:按组件,2021 - 2034 年

- 主要趋势

- 电动机

- 冰

- 电池和储能係统

- 电力电子与控制器

- 传动系统

第六章:市场估计与预测:依车型,2021 - 2034 年

- 主要趋势

- 搭乘用车

- 紧凑型车

- 中型车

- SUV 和豪华轿车

- 商用车

- 轻型商用车 (LCV)

- 重型商用车 (HCV)

- 两轮车

第七章:市场估计与预测:依车型,2021 - 2034 年

- 主要趋势

- 全混合动力系统

- 轻度混合动力系统

第 8 章:市场估计与预测:按应用,2021 - 2034 年

- 主要趋势

- 城市交通

- 城际旅行

- 非公路应用

第 9 章:市场估计与预测:按技术,2021 - 2034 年

- 主要趋势

- 再生煞车系统

- 启动停止系统

- 电动辅助系统

第 10 章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 西班牙

- 义大利

- 俄罗斯

- 北欧

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳新银行

- 东南亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东及非洲

- 阿联酋

- 南非

- 沙乌地阿拉伯

第 11 章:公司简介

- Aisin

- BorgWarner

- Continental

- Denso

- Hitachi Astemo

- Infineon

- LG Chem

- Magna

- Panasonic

- Bosch

- Samsung SDI

- Schaeffler

- Siemens

- Valeo

- ZF

- BYD

- Mitsubishi Electric

- Toyota Industries

- YASA

- Mahle

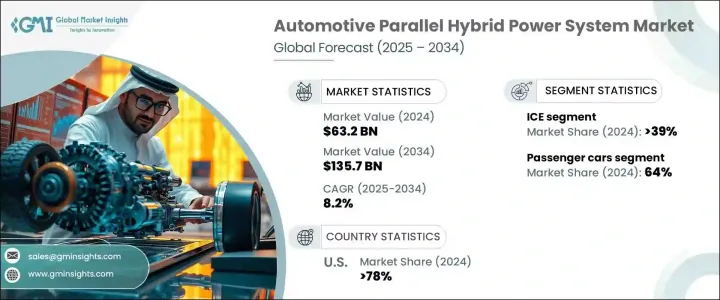

The Global Automotive Parallel Hybrid Power System Market was valued at USD 63.2 billion in 2024 and is projected to grow at a CAGR of 8.2% between 2025 and 2034. With a growing emphasis on reducing greenhouse gas emissions and enhancing fuel efficiency, the market is witnessing significant momentum. Governments worldwide are implementing stringent regulations and offering incentives to accelerate the adoption of hybrid electric vehicles (HEVs). These policies, including tax breaks, subsidies, and investment in EV infrastructure, are making hybrid technology more accessible and appealing to consumers. Additionally, rising fuel prices and increasing awareness of sustainability are driving consumer preferences toward energy-efficient mobility solutions.

Automakers are rapidly expanding their hybrid vehicle portfolios to meet evolving regulatory standards and consumer expectations. The growing integration of advanced powertrain technologies, including regenerative braking systems and optimized battery performance, is further enhancing the efficiency and appeal of hybrid vehicles. As hybrid power systems continue to bridge the gap between traditional internal combustion engine (ICE) vehicles and fully electric alternatives, their adoption is expected to surge across global markets. The increasing availability of hybrid models at competitive prices is also contributing to market growth, particularly in regions where EV charging infrastructure is still underdeveloped.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $63.2 Billion |

| Forecast Value | $135.7 Billion |

| CAGR | 8.2% |

The market is segmented into key components, including electric motors, internal combustion engines, batteries, power electronics, and transmission systems. The internal combustion engine segment remains dominant, accounting for 39% of the market share in 2024. Despite the shift toward electrification, ICE-based hybrid systems continue to play a crucial role in the transition to cleaner transportation. The affordability and widespread availability of gasoline and diesel refueling infrastructure make hybrid vehicles a practical choice, particularly in developing economies. By 2034, the ICE segment is expected to exceed USD 50 billion, driven by technological advancements in fuel efficiency and emissions reduction.

By vehicle type, the automotive parallel hybrid power system market is categorized into two-wheelers, passenger cars, and commercial vehicles. Passenger cars captured a 64% market share in 2024 as consumers prioritize fuel-efficient and cost-effective transportation solutions. The demand for hybrid passenger vehicles is particularly strong in urban areas, where traffic congestion and fuel costs make energy efficiency a top priority. Automakers are introducing innovative hybrid models with improved powertrain performance, extended battery life, and seamless integration of smart technologies, making them increasingly attractive to consumers seeking a balance between performance and sustainability.

The U.S. remains the largest market for automotive parallel hybrid power systems, accounting for 78% of the total market share in 2024. The country's extensive road networks, robust infrastructure, and increasing consumer awareness of fuel efficiency are key factors driving adoption. With domestic manufacturers leading the charge in hybrid vehicle innovation, the U.S. continues to be a major hub for technological advancements in sustainable transportation. As demand for hybrid vehicles rises, automakers are investing heavily in research and development to refine hybrid powertrains, improve energy efficiency, and offer cost-effective alternatives to traditional gasoline-powered vehicles.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material suppliers

- 3.1.2 Manufacturers

- 3.1.3 Distribution channels

- 3.1.4 Service providers

- 3.1.5 End users

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Case studies

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Government regulations & incentives

- 3.8.1.2 Rising fuel prices & cost efficiency

- 3.8.1.3 Increasing environmental awareness

- 3.8.1.4 Technological advancements

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 Limited battery life and recycling issues

- 3.8.2.2 High competition from fully electric vehicles

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Electric motor

- 5.3 ICE

- 5.4 Battery & energy storage systems

- 5.5 Power electronics & controllers

- 5.6 Transmission system

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Passenger vehicles

- 6.2.1 Compact cars

- 6.2.2 Mid-size cars

- 6.2.3 SUVs & luxury cars

- 6.3 Commercial Vehicles

- 6.3.1 Light commercial vehicles (LCVs)

- 6.3.2 Heavy commercial vehicles (HCVs)

- 6.4 Two-Wheelers

Chapter 7 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Full hybrid system

- 7.3 Mild hybrid system

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Urban transportation

- 8.3 Intercity travel

- 8.4 Off-highway applications

Chapter 9 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 Regenerative braking systems

- 9.3 Start-stop systems

- 9.4 Electric-assist systems

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Aisin

- 11.2 BorgWarner

- 11.3 Continental

- 11.4 Denso

- 11.5 Hitachi Astemo

- 11.6 Infineon

- 11.7 LG Chem

- 11.8 Magna

- 11.9 Panasonic

- 11.10 Bosch

- 11.11 Samsung SDI

- 11.12 Schaeffler

- 11.13 Siemens

- 11.14 Valeo

- 11.15 ZF

- 11.16 BYD

- 11.17 Mitsubishi Electric

- 11.18 Toyota Industries

- 11.19 YASA

- 11.20 Mahle

混合动力轻型汽车市场(按推进类型、车辆类型和最终用户划分)—2025-2032 年全球预测混合动力自行车市场按类型、零件、齿轮类型、悬吊类型、车架材料、最终用户和分销管道划分 - 2025-2030 年全球预测

混合动力轻型汽车市场(按推进类型、车辆类型和最终用户划分)—2025-2032 年全球预测混合动力自行车市场按类型、零件、齿轮类型、悬吊类型、车架材料、最终用户和分销管道划分 - 2025-2030 年全球预测 全球混合动力传动系统市场

全球混合动力传动系统市场 全球轻度混合动力车市场评估:依车型、容量类型、电池类型、地区、机会及预测,2018-2032

全球轻度混合动力车市场评估:依车型、容量类型、电池类型、地区、机会及预测,2018-2032 轻度混合动力车市场规模、份额、成长分析(按产能、车型、电池、地区)—2025 年至 2032 年产业预测

轻度混合动力车市场规模、份额、成长分析(按产能、车型、电池、地区)—2025 年至 2032 年产业预测 非公路电动车零件市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

非公路电动车零件市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 全球混合动力自行车市场-按产品、地区和预测的市场规模

全球混合动力自行车市场-按产品、地区和预测的市场规模 轻度混合动力车:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)

轻度混合动力车:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年) 轻度混合动力车市场:按电池容量、车辆类型和地区划分

轻度混合动力车市场:按电池容量、车辆类型和地区划分 汽车并联混合动力系统市场,按组件、按车辆、按推进器、按应用、按技术、按国家和地区 - 2025 年至 2032 年全球行业分析、市场规模、市场份额和预测

汽车并联混合动力系统市场,按组件、按车辆、按推进器、按应用、按技术、按国家和地区 - 2025 年至 2032 年全球行业分析、市场规模、市场份额和预测