|

市场调查报告书

商品编码

1685063

智慧电网市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Smart Grid Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

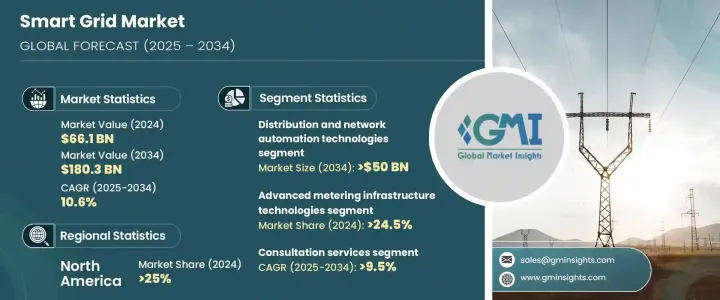

2024 年全球智慧电网市场价值为 661 亿美元,预计在 2025 年至 2034 年期间将实现 10.6% 的强劲复合年增长率,这受到电力需求不断增长、快速城市化以及对现代能源基础设施的迫切需求的推动。随着世界向再生能源转型,智慧电网技术对于确保高效的能源分配、最大限度地减少传输损耗和提高电网可靠性变得至关重要。世界各国政府和公用事业供应商都在大力投资电网现代化、实施自动化和整合数位通讯工具以优化能源流。随着电动车和智慧家庭解决方案的普及,对即时监控和智慧电网管理的需求达到了前所未有的高度。随着气候变迁问题和监管要求推动产业走向永续能源解决方案,智慧电网创新被证明是建立有弹性、面向未来的能源生态系统的关键推动因素。人工智慧、物联网和机器学习的整合正在进一步改变市场,实现预测性维护、需求预测和增强电网安全。公用事业公司正在利用这些进步来提高营运效率并降低成本,而消费者则受益于更高的能源透明度和具有成本效益的电力消耗。

多年来,市场稳步扩张,其价值从 2022 年的 552 亿美元增加到 2023 年的 602 亿美元和 2024 年的 661 亿美元。该产业根据技术分为消费者介面、配电和网路自动化、智慧输配电设备、先进计量基础设施以及通讯和无线基础设施。其中,配电和网路自动化技术预计到 2034 年将超过 500 亿美元,因为公用事业公司专注于实施自动控制和即时监控,以增强电网弹性并优化能源分配。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 661亿美元 |

| 预测值 | 1803亿美元 |

| 复合年增长率 | 10.6% |

部署和整合服务在 2024 年占据主导地位,占据超过 44% 的市场份额,并有望持续成长。日益普及的复杂IT系统和先进的智慧技术,推动了对智慧电网解决方案的无缝整合和大规模实施的需求。电动车充电站普及率的提高也在加速智慧电网技术的采用方面发挥着至关重要的作用。能源供应商正在积极投资先进的系统,以有效管理配电并平衡电力供应和波动的需求。

2024 年,北美智慧电网市场占全球份额的 25%,预计到 2034 年将实现强劲成长。光是美国市场在 2022 年的价值就达到 118 亿美元,到 2023 年将成长到 127 亿美元,到 2024 年将成长到 137 亿美元。老化能源基础设施的现代化,加上对智慧能源解决方案的监管支持不断增加,正在推动这一成长。同时,受电力消耗增加、城市快速扩张以及政府主导的电网技术升级措施的推动,亚太地区预计将在 2034 年创造 750 亿美元的收入。随着对先进能源管理解决方案的投资不断增加,智慧电网市场将在全球主要地区大幅扩张。

目录

第 1 章:方法论与范围

- 市场定义

- 基础估算与计算

- 预测计算

- 资料来源

- 基本的

- 次要

- 有薪资的

- 民众

第 2 章:执行摘要

第 3 章:产业洞察

- 产业生态系统分析

- 监管格局

- 产业衝击力

- 成长动力

- 产业陷阱与挑战

- 成长潜力分析

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 战略仪表板

- 创新与永续发展格局

第 5 章:市场规模与预测:依技术,2021 – 2034 年

- 主要趋势

- 智慧型输配电设备

- 配电和网路自动化

- 先进的计量基础设施

- 消费者介面

- 通讯和无线基础设施

第六章:市场规模及预测:依服务,2021 – 2034 年

- 主要趋势

- 咨询

- 部署与集成

- 支援与维护

第 7 章:市场规模与预测:依部署,2021 – 2034 年

- 主要趋势

- 世代

- 传染

- 分配

- 最终用途

第 8 章:市场规模与预测:按地区,2021 – 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 英国

- 法国

- 德国

- 西班牙

- 义大利

- 亚太地区

- 中国

- 澳洲

- 日本

- 韩国

- 印度

- 中东和非洲

- 沙乌地阿拉伯

- 阿联酋

- 南非

- 拉丁美洲

- 巴西

- 智利

第九章:公司简介

- ABB

- Belden

- Cisco Systems

- Fujitsu

- General Electric

- Honeywell International

- Hubbell

- IBM

- Itron

- Landis+Gyr

- Oracle

- Schneider Electric

- Siemens

- Wipro

The Global Smart Grid Marketm Valued At USD 66.1 Billion In 2024, Is Projected To Register A Robust CAGR Of 10.6% Between 2025 And 2034., Driven By The Increasing Demand For Electricity, Rapid Urbanization, And The Urgent Need For Modern Energy Infrastructure. As The World Transitions Toward Renewable Energy Sources, Smart Grid Technologies Are Becoming Essential To Ensure Efficient Energy Distribution, Minimize Transmission Losses, And Enhance Grid Reliability. Governments And Utility Providers Worldwide Are Making Substantial Investments In Modernizing Power Grids, Implementing Automation, And Integrating Digital Communication Tools To Optimize Energy Flow. With The Rising Adoption Of Electric Vehicles And Smart Home Solutions, The Demand For Real-Time Monitoring And Intelligent Grid Management Is At An All-Time High. As Climate Change Concerns And Regulatory Mandates Push The Industry Toward Sustainable Energy Solutions, Smart Grid Innovations Are Proving To Be A Critical Enabler Of A Resilient And Future-Ready Energy Ecosystem. The Integration Of Artificial Intelligence, IoT, And Machine Learning Is Further Revolutionizing The Market, allowing for predictive maintenance, demand forecasting, and enhanced grid security. Utility companies are leveraging these advancements to improve operational efficiency and reduce costs, while consumers benefit from greater energy transparency and cost-effective power consumption.

The market has seen steady expansion over the years, with its value increasing from USD 55.2 billion in 2022 to USD 60.2 billion in 2023 and USD 66.1 billion in 2024. The industry is categorized based on technology into consumer interface, distribution and network automation, smart transmission and distribution equipment, advanced metering infrastructure, and communication and wireless infrastructure. Among these, distribution and network automation technologies are expected to surpass USD 50 billion by 2034, as utilities focus on implementing automated controls and real-time monitoring to strengthen grid resilience and optimize energy distribution.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $66.1 Billion |

| Forecast Value | $180.3 Billion |

| CAGR | 10.6% |

Deployment and integration services held a dominant position in 2024, accounting for over 44% of the market share, with expectations for sustained growth. The increasing adoption of sophisticated IT systems and advanced smart technologies is driving the demand for seamless integration and large-scale implementation of intelligent grid solutions. The rising penetration of electric vehicle charging stations is also playing a crucial role in accelerating the adoption of smart grid technology. Energy providers are actively investing in advanced systems to efficiently manage power distribution and balance electricity supply with fluctuating demand.

North America smart grid market accounted for 25% of the global share in 2024, with strong growth projections through 2034. The U.S. market alone was valued at USD 11.8 billion in 2022, growing to USD 12.7 billion in 2023 and USD 13.7 billion in 2024. The modernization of aging energy infrastructure, coupled with increasing regulatory support for smart energy solutions, is fueling this growth. Meanwhile, the Asia Pacific region is on track to generate USD 75 billion by 2034, driven by rising electricity consumption, rapid urban expansion, and government-led initiatives to upgrade grid technology. As investments in advanced energy management solutions continue to rise, the smart grid market is set to witness substantial expansion across key global regions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Strategic dashboard

- 4.2 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Technology, 2021 – 2034 (USD Million)

- 5.1 Key trends

- 5.2 Smart T&D equipment

- 5.3 Distribution & network automation

- 5.4 Advanced metering infrastructure

- 5.5 Consumer interface

- 5.6 Communication & wireless infrastructure

Chapter 6 Market Size and Forecast, By Service, 2021 – 2034 (USD Million)

- 6.1 Key trends

- 6.2 Consulting

- 6.3 Deployment & integration

- 6.4 Support & maintenance

Chapter 7 Market Size and Forecast, By Deployment, 2021 – 2034 (USD Million)

- 7.1 Key trends

- 7.2 Generation

- 7.3 Transmission

- 7.4 Distribution

- 7.5 End use

Chapter 8 Market Size and Forecast, By Region, 2021 – 2034 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 France

- 8.3.3 Germany

- 8.3.4 Spain

- 8.3.5 Italy

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Australia

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 India

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 South Africa

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Chile

Chapter 9 Company Profiles

- 9.1 ABB

- 9.2 Belden

- 9.3 Cisco Systems

- 9.4 Fujitsu

- 9.5 General Electric

- 9.6 Honeywell International

- 9.7 Hubbell

- 9.8 IBM

- 9.9 Itron

- 9.10 Landis+Gyr

- 9.11 Oracle

- 9.12 Schneider Electric

- 9.13 Siemens

- 9.14 Wipro

全球虚拟电厂 (VPP) 市场:预测至 2032 年 - 按产品、动力来源、技术、最终用户和地区分類的分析智慧电网解决方案市场预测至2032年:按组件、解决方案类型、应用、最终用户和地区分類的全球分析智慧电网基础设施市场预测至2032年:按组件、部署类型、技术、应用、最终用户和地区分類的全球分析

全球虚拟电厂 (VPP) 市场:预测至 2032 年 - 按产品、动力来源、技术、最终用户和地区分類的分析智慧电网解决方案市场预测至2032年:按组件、解决方案类型、应用、最终用户和地区分類的全球分析智慧电网基础设施市场预测至2032年:按组件、部署类型、技术、应用、最终用户和地区分類的全球分析 智慧电网市场(按组件、产品、应用、最终用户和技术)—2025-2032 年全球预测智慧电网託管服务市场(按服务类型、部署模式、最终用户和电网细分)—全球预测 2025-2032智慧电网通讯市场(按组件、网路类型、通讯技术、应用和最终用户划分)—2025-2032 年全球预测

智慧电网市场(按组件、产品、应用、最终用户和技术)—2025-2032 年全球预测智慧电网託管服务市场(按服务类型、部署模式、最终用户和电网细分)—全球预测 2025-2032智慧电网通讯市场(按组件、网路类型、通讯技术、应用和最终用户划分)—2025-2032 年全球预测 智慧电网网路市场规模、份额、成长分析(硬体、软体、服务和地区)—2025-2032 年产业预测

智慧电网网路市场规模、份额、成长分析(硬体、软体、服务和地区)—2025-2032 年产业预测 2025年全球智慧电网技术市场报告2025年全球智慧电网通讯市场报告2032 年智慧电网市场预测:按组件、部署模型、通讯技术、应用、最终用户和地区进行的全球分析

2025年全球智慧电网技术市场报告2025年全球智慧电网通讯市场报告2032 年智慧电网市场预测:按组件、部署模型、通讯技术、应用、最终用户和地区进行的全球分析