|

市场调查报告书

商品编码

1936604

汽车雷达市场机会、成长要素、产业趋势分析及预测(2026年至2035年)Automotive Radar Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

全球汽车雷达市场预计到 2025 年将达到 72 亿美元,到 2035 年将达到 292 亿美元,年复合成长率为 15.3%。

高级驾驶辅助系统 (ADAS) 的日益普及是推动汽车雷达需求成长的主要动力,因为雷达是这些系统的关键组件。与 ADAS 技术相关的专利申请数量的增加也印证了对雷达解决方案的持续需求。汽车产业也见证了联网汽车的蓬勃发展,这些汽车整合了多个雷达感测器,以增强安全性和自动化功能。这些雷达支援即时人工智慧和机器学习应用,使车辆能够快速做出决策、预测危险并优化交通操控。短程雷达透过精确侦测周围物体,在停车辅助、盲点监控和低速防撞正变得越来越重要。製造商目前正将这些雷达与摄影机和超音波感测器结合,以提高商用车和乘用车的精度、恶劣天气的性能和成本效益。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 72亿美元 |

| 预测金额 | 292亿美元 |

| 复合年增长率 | 15.3% |

预计到2025年,77GHz雷达市场规模将达42亿美元。 77GHz雷达拥有卓越的精度和侦测范围,能够可靠地辨识不同距离的车辆、行人和障碍物。这项功能对于现代ADAS(高级驾驶辅助系统)至关重要,例如主动式车距维持定速系统、自动紧急煞车、前碰撞警报和盲点监测,这些功能在多个地区已成为强制性配置。汽车製造商正在车辆的前部、后部和四个角落安装多个雷达单元,其中许多製造商选择使用77GHz感测器,因为其具有高可靠性和扩充性。

预计到2025年,中程雷达(MRR)将占据42.3%的市场份额,到2035年市场规模将达到123亿美元。 MRR系统对于实现自动停车、都市区防撞以及全面感知周围环境至关重要。随着都市区向智慧型运输系统转型,商用车队、共享出行服务和末端配送车辆都高度依赖MRR在高流量区域行驶。智慧交通倡议和互联基础设施的成长,正在提升商用车和乘用车对基于雷达的安全解决方案的需求。

预计到2025年,美国汽车雷达市场规模将达到8.174亿美元。商用卡车车队正日益广泛地整合雷达探测技术,以最大限度地减少高速公路事故,并在长途行驶中增强驾驶员辅助功能。此外,随着国内主要汽车製造商生产高科技汽车,乘用车也越来越多地采用这些系统,以增强盲点监测和车道偏离预警等安全功能。

目录

第一章调查方法

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 成本结构

- 每个阶段的附加价值

- 影响价值链的因素

- 中断

- 产业影响因素

- 司机

- 扩大ADAS(进阶驾驶辅助系统)的应用

- 自动驾驶和半自动驾驶汽车的需求日益增长

- 更重视避免碰撞和道路安全

- 电动车和软体定义汽车的兴起

- 产业潜在风险与挑战

- 汽车雷达系统及整合高成本

- 讯号处理和校准的复杂性

- 市场机会

- 扩展 L2+ 和 L3 级自动驾驶能力

- 在商用车和车队安全领域推广应用

- 汽车雷达在新兴市场的快速发展

- 停车辅助和盲点侦测应用中对短程雷达的需求

- 司机

- 成长潜力分析

- 监管环境

- 北美洲

- 美国联邦通讯委员会(FCC)

- 美国国家标准协会(ANSI)

- 美国汽车工程师协会(SAE)

- 欧洲

- 欧洲电讯标准协会(ETSI)

- 联合国欧洲经济委员会

- 欧洲电工标准化委员会

- 亚太地区

- 车辆网路通讯协定(中国)

- 无线产业和商业协会

- 内务部(MIC)

- 拉丁美洲

- 国家电讯(ANATEL)

- 通信监理委员会

- 中东和非洲

- 波湾合作理事会(GCC)法律规范

- 阿联酋国家电信管理局

- 车辆安全系统相关法规

- 北美洲

- 波特五力分析

- PESTEL 分析

- 技术与创新展望

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 副产品

- 生产统计

- 生产基地

- 消费基础

- 出口和进口

- 成本細項分析

- 永续性和环境影响

- 环境影响评估

- 社会影响力和社区服务

- 公司管治与企业社会责任

- 永续金融与投资趋势

- 网路安全与功能安全框架

- 网路安全威胁和漏洞评估

- 空中更新 (OTA) 安全通讯协定

- 冗余和故障安全设计

- 雷达感测中的资料隐私与保护

- 安装、校准和维护生态系统

- 工厂校准与现场校准要求

- 售后安装的复杂性

- 碰撞修復后需要重新校准

- 诊断工具和设备要求

- 半导体和晶片组生态系统分析

- 绘製ADAS和自动驾驶蓝图

- OEM雷达策略和采购模式

- 案例研究

第四章 竞争情势

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 重大进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 企业扩张计画和资金筹措

第五章 依频率分類的市场估计与预测,2022-2035年

- 24 GHz 雷达

- 77 GHz 雷达

- 79 GHz 雷达

- 其他的

第六章 2022-2035年各地区市场估算与预测

- 短程雷达(SRR)

- 中程雷达(MRR)

- 远程雷达(LRR)

第七章 依安装地点分類的市场估计与预测,2022-2035年

- 外部的

- 前雷达

- 后方雷达

- 侧雷达

- 内部的

- 驾驶员监控雷达

- 乘员监控雷达

第八章 按车辆类型分類的市场估算与预测,2022-2035年

- 搭乘用车

- 掀背车

- SUV

- 轿车

- 商用车辆

- 轻型商用车(LCV)

- 中型商用车(MCV)

- 重型商用车(HCV)

第九章 依车辆类型分類的市场估计与预测,2022-2035年

- 经济型(25,000 美元以下)

- 中檔(25,000 美元 - 50,000 美元)

- 高端/豪华(超过 50,000 美元)

第十章 依推进方式分類的市场估计与预测,2022-2035年

- 内燃机(ICE)

- 电动车(EV)

- 电池式电动车(BEV)

- HEV

- PHEV

第十一章 按应用领域分類的市场估算与预测,2022-2035年

- 主动式车距维持定速系统(ACC)

- 盲点侦测(BSD)

- 前向碰撞警报(FCW)

- 车道偏离预警系统(LDWS)

- 自动紧急煞车(AEB)

- 停车辅助系统(PA)

- 其他的

第十二章 依销售管道分類的市场估计与预测,2022-2035年

- OEM

- 售后市场

第十三章 2022-2035年各地区市场估算与预测

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 北欧国家

- 比荷卢经济联盟

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- ANZ

- 新加坡

- 马来西亚

- 印尼

- 越南

- 泰国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 哥伦比亚

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十四章:公司简介

- 世界公司

- Robert Bosch

- Continental

- Denso

- Aptiv

- NXP Semiconductors

- ZF Friedrichshafen

- Valeo

- Magna

- Infineon

- Texas Instruments

- Autoliv

- Analog Devices

- Renesas Electronics

- BorgWarner

- Hyundai Mobis

- Mobileye

- 当地公司

- Huawei Technologies

- Cheng-Tech

- HASCO

- HiRain Technologies

- Calterah Semiconductor

- HL Klemove

- Desay SV Automotive

- WeiFu

- Fusionride

- 新兴企业

- Uhnder

- Zendar

- Waveye

- Altos Radar

- Xavveo

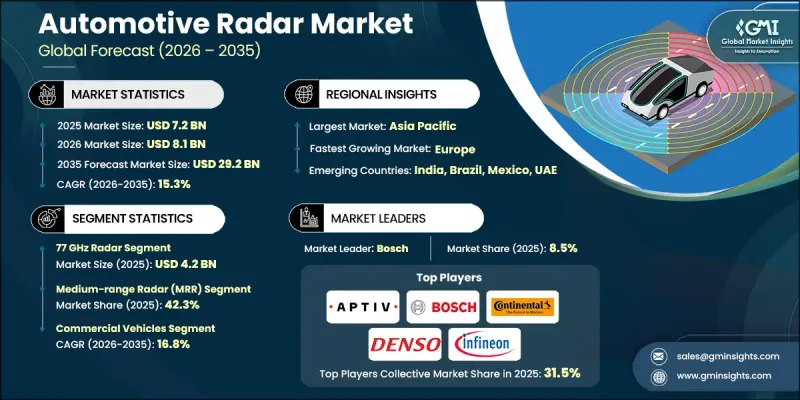

The Global Automotive Radar Market was valued at USD 7.2 billion in 2025 and is estimated to grow at a CAGR of 15.3% to reach USD 29.2 billion by 2035.

The rising adoption of advanced driver-assistance systems (ADAS) has significantly fueled the demand for automotive radars, as they serve as critical components within these systems. Increasing patent filings related to ADAS technologies further sustain the consistent need for radar solutions. The automotive sector is also experiencing growth in connected vehicles, which integrate multiple radar sensors to enhance safety and automation features. These radars support real-time AI and machine learning applications, enabling vehicles to make faster decisions, anticipate hazards, and optimize traffic handling. Short-range radar is gaining prominence in assisting parking, monitoring blind spots, and preventing low-speed collisions by accurately detecting nearby objects. Manufacturers are now combining these radars with cameras and ultrasonic sensors to improve precision, performance in adverse weather conditions, and cost efficiency for both commercial and passenger vehicles.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $7.2 Billion |

| Forecast Value | $29.2 Billion |

| CAGR | 15.3% |

The 77 GHz radar segment accounted for USD 4.2 billion in 2025. Offering superior accuracy and detection range, 77 GHz radars are highly reliable for identifying vehicles, pedestrians, and obstacles at varying distances. Their capabilities are crucial for modern ADAS features, including adaptive cruise control, autonomous emergency braking, forward collision alerts, and blind-spot monitoring, which are increasingly mandated in several regions. Automotive companies are deploying multiple radar units throughout vehicles' front, rear, and corners, most of which rely on 77 GHz sensors due to their robustness and scalability.

The medium-range radar (MRR) held a 42.3% share in 2025 and is expected to reach USD 12.3 billion by 2035. MRR systems are essential for autonomous parking, urban collision prevention, and enabling a comprehensive awareness of the surrounding environment. As urban centers transition toward intelligent transportation systems, commercial fleets, ride-hailing services, and last-mile delivery vehicles are relying heavily on MRR for navigating high-traffic zones. The growth of smart transport initiatives and connected infrastructure is creating increasing demand for radar-based safety solutions in both commercial and passenger vehicles.

United States Automotive Radar Market reached USD 817.4 million in 2025. Commercial trucking fleets are increasingly integrating radar detection technologies to minimize highway accidents and enhance driver assistance during long-haul operations. These systems are also being installed in passenger vehicles to provide improved safety features such as blind-spot detection and lane departure alerts, driven by the presence of major domestic automakers producing high-tech vehicles.

Key players dominating the Global Automotive Radar Market include Bosch, Denso, Aptiv, Continental, Infineon, NXP Semiconductors, Analog Devices, ZF Friedrichshafen, Valeo, and Texas Instruments. Leading companies in the automotive radar market are adopting strategic measures to solidify their market presence. These include forging alliances and partnerships with automotive manufacturers to integrate radar technologies into new vehicles, expanding research and development for next-generation radar sensors, and investing in AI and machine learning capabilities to enhance real-time decision-making in vehicles. They are also focusing on regional expansion, acquiring smaller tech firms, and offering cost-effective, high-performance solutions for both commercial and passenger vehicles. By continuously innovating and diversifying product portfolios, these companies strengthen their foothold in the growing radar market while meeting evolving regulatory and technological demands.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Frequency

- 2.2.3 Range

- 2.2.4 Placement

- 2.2.5 Vehicle

- 2.2.6 Vehicle Class

- 2.2.7 Propulsion

- 2.2.8 Application

- 2.2.9 Sales Channel

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising adoption of advanced driver assistance systems (ADAS)

- 3.2.1.2 Growing demand for autonomous and semi-autonomous vehicles

- 3.2.1.3 Increasing focus on collision avoidance and road safety

- 3.2.1.4 Expansion of electric and software-defined vehicles

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of automotive radar systems and integration

- 3.2.2.2 Complexity in signal processing and calibration

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of level 2+ and level 3 autonomous driving functions

- 3.2.3.2 Increasing adoption in commercial vehicles and fleet safety

- 3.2.3.3 Rapid growth of automotive radar in emerging markets

- 3.2.3.4 Demand for short-range radar in parking and blind spot applications

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 Federal Communications Commission (FCC)

- 3.4.1.2 American National Standards Institute (ANSI)

- 3.4.1.3 Society of Automotive Engineers (SAE)

- 3.4.2 Europe

- 3.4.2.1 European Telecommunications Standards Institute (ETSI)

- 3.4.2.2 United Nations Economic Commission for Europe

- 3.4.2.3 European Committee for Electrotechnical Standardization

- 3.4.3 Asia Pacific

- 3.4.3.1 Vehicle Network Communication Protocol (China)

- 3.4.3.2 Association of Radio Industries and Businesses

- 3.4.3.3 Ministry of Internal Affairs and Communications (MIC)

- 3.4.4 Latin America

- 3.4.4.1 Agencia Nacional de Telecomunicacoes (ANATEL)

- 3.4.4.2 Comision de Regulacion de Comunicaciones

- 3.4.5 Middle East & Africa

- 3.4.5.1 Gulf Cooperation Council regulatory framework

- 3.4.5.2 National Communications Authority (UAE)

- 3.4.5.3 Vehicle regulations for safety systems

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Sustainability and environmental impact

- 3.11.1 Environmental impact assessment

- 3.11.2 Social impact & community benefits

- 3.11.3 Governance & corporate responsibility

- 3.11.4 Sustainable finance & investment trends

- 3.12 Cybersecurity and functional safety framework

- 3.12.1 Cybersecurity threats and vulnerability assessment

- 3.12.2 Over-the-air (OTA) update security protocols

- 3.12.3 Redundancy and fail-safe mechanism design

- 3.12.4 Data privacy and protection in radar sensing

- 3.13 Installation, calibration, and maintenance ecosystem

- 3.13.1 Factory calibration vs. field calibration requirements

- 3.13.2 Aftermarket installation complexity

- 3.13.3 Recalibration needs after collision repair

- 3.13.4 Diagnostic tools and equipment requirements

- 3.14 Semiconductor & Chipset Ecosystem Analysis

- 3.15 ADAS & Autonomy Roadmap Mapping

- 3.16 OEM Radar Strategy & Sourcing Models

- 3.17 Case studies

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Frequency, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 24 GHz Radar

- 5.3 77 GHz Radar

- 5.4 79 GHz Radar

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Range, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 Short-Range Radar (SRR)

- 6.3 Medium-Range Radar (MRR)

- 6.4 Long-Range Radar (LRR)

Chapter 7 Market Estimates & Forecast, By Placement, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 Exterior

- 7.2.1 Front Radar

- 7.2.2 Rear Radar

- 7.2.3 Side Radar

- 7.3 Interior

- 7.3.1 Driver Monitoring Radar

- 7.3.2 Occupant Monitoring Radar

Chapter 8 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 Passenger cars

- 8.2.1 Hatchback

- 8.2.2 SUV

- 8.2.3 Sedan

- 8.3 Commercial vehicles

- 8.3.1 Light Commercial Vehicles (LCV)

- 8.3.2 Medium Commercial Vehicles (MCV)

- 8.3.3 Heavy Commercial Vehicles (HCV)

Chapter 9 Market Estimates & Forecast, By Vehicle Class, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 Economy (Below USD 25,000)

- 9.3 Mid-Range (USD 25,000 - USD 50,000)

- 9.4 Premium/Luxury (Above USD 50,000)

Chapter 10 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Bn, Units)

- 10.1 Key trends

- 10.2 ICE

- 10.3 EV

- 10.3.1 BEV

- 10.3.2 HEV

- 10.3.3 PHEV

Chapter 11 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn, Units)

- 11.1 Key trends

- 11.2 Adaptive Cruise Control (ACC)

- 11.3 Blind Spot Detection (BSD)

- 11.4 Forward Collision Warning (FCW)

- 11.5 Lane Departure Warning System (LDWS)

- 11.6 Automatic Emergency Braking (AEB)

- 11.7 Parking Assistance (PA)

- 11.8 Others

Chapter 12 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Bn, Units)

- 12.1 Key trends

- 12.2 OEM

- 12.3 Aftermarket

Chapter 13 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 13.1 Key trends

- 13.2 North America

- 13.2.1 US

- 13.2.2 Canada

- 13.3 Europe

- 13.3.1 Germany

- 13.3.2 UK

- 13.3.3 France

- 13.3.4 Italy

- 13.3.5 Spain

- 13.3.6 Russia

- 13.3.7 Nordics

- 13.3.8 Benelux

- 13.4 Asia Pacific

- 13.4.1 China

- 13.4.2 India

- 13.4.3 Japan

- 13.4.4 South Korea

- 13.4.5 ANZ

- 13.4.6 Singapore

- 13.4.7 Malaysia

- 13.4.8 Indonesia

- 13.4.9 Vietnam

- 13.4.10 Thailand

- 13.5 Latin America

- 13.5.1 Brazil

- 13.5.2 Mexico

- 13.5.3 Argentina

- 13.5.4 Colombia

- 13.6 MEA

- 13.6.1 South Africa

- 13.6.2 Saudi Arabia

- 13.6.3 UAE

Chapter 14 Company Profiles

- 14.1 Global companies

- 14.1.1 Robert Bosch

- 14.1.2 Continental

- 14.1.3 Denso

- 14.1.4 Aptiv

- 14.1.5 NXP Semiconductors

- 14.1.6 ZF Friedrichshafen

- 14.1.7 Valeo

- 14.1.8 Magna

- 14.1.9 Infineon

- 14.1.10 Texas Instruments

- 14.1.11 Autoliv

- 14.1.12 Analog Devices

- 14.1.13 Renesas Electronics

- 14.1.14 BorgWarner

- 14.1.15 Hyundai Mobis

- 14.1.16 Mobileye

- 14.2 Regional companies

- 14.2.1 Huawei Technologies

- 14.2.2 Cheng-Tech

- 14.2.3 HASCO

- 14.2.4 HiRain Technologies

- 14.2.5 Calterah Semiconductor

- 14.2.6 HL Klemove

- 14.2.7 Desay SV Automotive

- 14.2.8 WeiFu

- 14.2.9 Fusionride

- 14.3 Emerging companies

- 14.3.1 Uhnder

- 14.3.2 Zendar

- 14.3.3 Waveye

- 14.3.4 Altos Radar

- 14.3.5 Xavveo

汽车毫米波相容标誌市场:按材料类型、车辆类型、销售管道、国家和地区划分 - 全球行业分析、市场规模、市场份额及2025-2032年预测

汽车毫米波相容标誌市场:按材料类型、车辆类型、销售管道、国家和地区划分 - 全球行业分析、市场规模、市场份额及2025-2032年预测 日本汽车雷达市场报告:按距离、车辆类型、应用和地区划分(2026-2034年)

日本汽车雷达市场报告:按距离、车辆类型、应用和地区划分(2026-2034年) 汽车雷达市场规模、份额和成长分析(按范围、频率、应用和地区划分)-2026-2033年产业预测

汽车雷达市场规模、份额和成长分析(按范围、频率、应用和地区划分)-2026-2033年产业预测 汽车雷达感测器市场规模、份额和成长分析(按范围、应用、车辆类型和地区划分)—产业预测(2026-2033 年)

汽车雷达感测器市场规模、份额和成长分析(按范围、应用、车辆类型和地区划分)—产业预测(2026-2033 年) 汽车雷达应用市场-全球产业规模、份额、趋势、机会及预测,依频率、应用、技术、地区及竞争格局划分,2020-2030年预测

汽车雷达应用市场-全球产业规模、份额、趋势、机会及预测,依频率、应用、技术、地区及竞争格局划分,2020-2030年预测 汽车雷达用高频印刷电路基板:2025-2031年全球市场份额及排名、总收入及需求预测FMCW毫米波雷达:全球市场份额和排名、总收入和需求预测(2025-2031年)汽车毫米波雷达:全球市场份额排名、总销售量和需求预测(2025-2031年)

汽车雷达用高频印刷电路基板:2025-2031年全球市场份额及排名、总收入及需求预测FMCW毫米波雷达:全球市场份额和排名、总收入和需求预测(2025-2031年)汽车毫米波雷达:全球市场份额排名、总销售量和需求预测(2025-2031年) 汽车级晶片雷达解决方案市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)

汽车级晶片雷达解决方案市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年) 汽车雷达感测器市场按频段、车辆类型、应用、安装方式、最终用户和技术划分-2025-2032年全球预测

汽车雷达感测器市场按频段、车辆类型、应用、安装方式、最终用户和技术划分-2025-2032年全球预测