|

市场调查报告书

商品编码

1699373

备用建筑发电机组市场机会、成长动力、产业趋势分析及 2025-2034 年预测Standby Construction Generator Sets Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

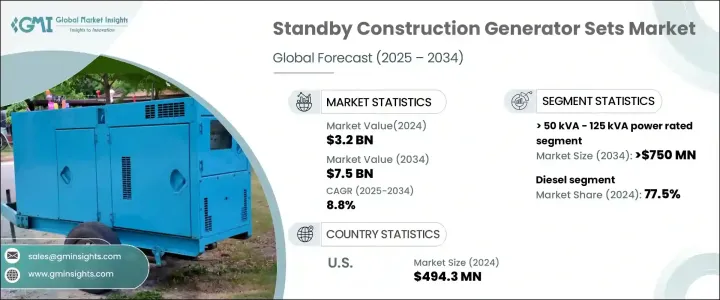

2024 年全球备用建筑发电机组市场价值为 32 亿美元,预计 2025 年至 2034 年的复合年增长率为 8.8%。这项快速扩张受到基础设施建设加速、城市化以及人工智慧 (AI) 和自动化技术日益融入备用发电机系统的推动。随着建筑工程变得越来越复杂,电力可靠性仍然是重中之重,对先进发电机解决方案的需求也不断增加。建筑业正在经历新发展的浪潮,特别是在新兴经济体,电气化的挑战需要可靠的备用电源。极端天气条件、电网不稳定以及各地区停电发生率的上升进一步增加了对发电机的需求。此外,对再生能源和混合动力解决方案的投资正在影响市场趋势,推动製造商采用更清洁、更有效率的备用发电机模型进行创新。

旨在减少碳排放的更严格的环境法规正在加速低排放发电机技术的采用。自动负载管理和智慧燃料优化等功能越来越受欢迎,使公司能够提高燃油效率,同时满足严格的永续性标准。随着世界各国政府实施减少建筑活动排放的政策,企业正积极投资合规、有效率的备用电源解决方案。此外,对营运成本的日益担忧也推动了人们向更智慧的发电机系统转变,以便在不影响电力输出的情况下降低燃料消耗。混合发电机系统的创新将传统燃料源与电池储存和再生能源相结合,为实现永续发展目标而不断获得发展动力。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 32亿美元 |

| 预测值 | 75亿美元 |

| 复合年增长率 | 8.8% |

额定功率小于等于 50 kVA 的发电机组预计将大幅成长,预计到 2034 年复合年增长率为 9%。这一增长归因于人们对适合中小型建筑项目的紧凑型、节能发电机的偏好日益增长。这些发电机因其能够以较低的营运成本提供可靠的电力而越来越受欢迎,对于注重成本效益和效率的建筑商来说,它们是一个有吸引力的选择。小型建筑专案、偏远地区和紧急备份需求正在推动对这些便携式和可扩展电源解决方案的需求。

备用建筑发电机组市场按燃料类型细分为柴油、天然气和其他,其中柴油发电机占据主导地位。柴油发电机凭藉其卓越的燃油效率、耐用性以及在大规模和关键施工环境中提供可靠电力的能力,在 2024 年占据了 77.5% 的市场份额。儘管人们越来越追求更环保的替代品,但柴油仍然是重型应用的首选,因为不间断电源至关重要。燃油效率和排放控制的不断进步进一步增强了柴油发电机组的吸引力。

预计到 2034 年,北美备用建筑发电机组市场将以 8% 的复合年增长率扩张,这得益于混合动力解决方案、提高燃油效率和增强远端监控能力等持续的技术进步。这些创新正在帮助建筑公司在优化成本的同时保持不间断运营,从而加强了整个地区对可靠备用电源解决方案的需求。随着城市化进程的推进和建设项目规模的扩大,对下一代备用发电机的投资预计将保持强劲,进一步推动市场成长。

目录

第一章:方法论与范围

- 市场范围和定义

- 市场估计和预测参数

- 预测计算

- 资料来源

- 基本的

- 次要

- 有薪资的

- 民众

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 监管格局

- 产业衝击力

- 成长动力

- 产业陷阱与挑战

- 成长潜力分析

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 战略展望

- 创新与永续发展格局

第五章:市场规模及预测:依实力评级

- 主要趋势

- ≤50千伏安

- > 50千伏安 - 125千伏安

- > 125 千伏安 - 200 千伏安

- > 200 千伏安 - 330 千伏安

- > 330 千伏安 - 750 千伏安

- > 750千伏安

第六章:市场规模及预测:依燃料

- 主要趋势

- 柴油引擎

- 气体

- 其他的

第七章:市场规模及预测:按地区

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 俄罗斯

- 英国

- 德国

- 法国

- 西班牙

- 奥地利

- 义大利

- 亚太地区

- 中国

- 澳洲

- 印度

- 日本

- 韩国

- 印尼

- 马来西亚

- 泰国

- 越南

- 菲律宾

- 缅甸

- 孟加拉

- 中东

- 沙乌地阿拉伯

- 阿联酋

- 卡达

- 土耳其

- 伊朗

- 阿曼

- 非洲

- 埃及

- 奈及利亚

- 阿尔及利亚

- 南非

- 安哥拉

- 肯亚

- 莫三比克

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 智利

第八章:公司简介

- Aggreko

- Ashok Leyland

- Atlas Copco AB

- Caterpillar

- Cummins, Inc.

- Deere & Company

- Generac Power Systems, Inc.

- Greaves Cotton Limited

- HIMOINSA

- JC Bamford Excavators Ltd.

- Kirloskar

- Kohler Co.

- Mahindra Powerol

- Mitsubishi Heavy Industries Ltd.

- Powerica Limited

- Sterling and Wilson Pvt. Ltd.

- Wärtsilä

- Yamaha Motor Co., Ltd.

The Global Standby Construction Generator Sets Market was valued at USD 3.2 billion in 2024 and is projected to grow at a CAGR of 8.8% from 2025 to 2034. This rapid expansion is fueled by accelerating infrastructure development, urbanization, and the increasing integration of artificial intelligence (AI) and automation technologies into standby generator systems. As construction projects become more complex and power reliability remains a top priority, demand for advanced generator solutions is rising. The construction industry is experiencing a surge in new developments, particularly in emerging economies, where electrification challenges necessitate dependable backup power sources. The need for generators is further amplified by extreme weather conditions, grid instability, and the rising incidence of power outages in various regions. Furthermore, investments in renewable energy and hybrid power solutions are influencing market trends, pushing manufacturers to innovate with cleaner and more efficient standby generator models.

Tighter environmental regulations aimed at reducing carbon emissions are accelerating the adoption of low-emission generator technologies. Features such as automatic load management and smart fuel optimization are gaining traction, enabling companies to improve fuel efficiency while meeting stringent sustainability standards. With governments worldwide enforcing policies to curb emissions from construction activities, businesses are actively investing in compliant, high-efficiency backup power solutions. Additionally, increasing operational cost concerns are driving the shift toward smarter generator systems that reduce fuel consumption without compromising power output. Innovations in hybrid generator systems, which combine traditional fuel sources with battery storage and renewable energy, are gaining momentum in response to sustainability goals.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.2 Billion |

| Forecast Value | $7.5 Billion |

| CAGR | 8.8% |

The <= 50 kVA power rating segment is poised for substantial growth, with a forecasted CAGR of 9% through 2034. This growth is attributed to the rising preference for compact, fuel-efficient generators that cater to small- and medium-scale construction projects. These generators are gaining popularity due to their ability to provide reliable power at a lower operational cost, making them an attractive choice for builders focused on cost-effectiveness and efficiency. Smaller construction projects, remote sites, and emergency backup requirements are fueling demand for these portable and scalable power solutions.

The standby construction generator sets market is segmented by fuel type into diesel, gas, and others, with diesel-powered generators maintaining a dominant position. Diesel generators held a 77.5% market share in 2024, owing to their superior fuel efficiency, durability, and capacity to provide reliable power in large-scale and critical construction environments. Despite the increasing push for greener alternatives, diesel remains the preferred choice for heavy-duty applications where uninterrupted power supply is crucial. Continuous advancements in fuel efficiency and emissions control are further enhancing the appeal of diesel-powered generator sets.

North America standby construction generator sets market is expected to expand at a CAGR of 8% through 2034, driven by ongoing technological advancements, including hybrid power solutions, improved fuel efficiency, and enhanced remote monitoring capabilities. These innovations are helping construction companies maintain uninterrupted operations while optimizing costs, reinforcing the demand for reliable backup power solutions across the region. As urbanization continues and construction projects scale up, investments in next-generation standby generators are expected to remain strong, further propelling market growth.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2032

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's Analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL Analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Strategic outlook

- 4.2 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Power Rating (USD Million & Units)

- 5.1 Key trends

- 5.2 ≤ 50 kVA

- 5.3 > 50 kVA - 125 kVA

- 5.4 > 125 kVA - 200 kVA

- 5.5 > 200 kVA - 330 kVA

- 5.6 > 330 kVA - 750 kVA

- 5.7 > 750 kVA

Chapter 6 Market Size and Forecast, By Fuel (USD Million & Units)

- 6.1 Key trends

- 6.2 Diesel

- 6.3 Gas

- 6.4 Others

Chapter 7 Market Size and Forecast, By Region (USD Million & Units)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Russia

- 7.3.2 UK

- 7.3.3 Germany

- 7.3.4 France

- 7.3.5 Spain

- 7.3.6 Austria

- 7.3.7 Italy

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Australia

- 7.4.3 India

- 7.4.4 Japan

- 7.4.5 South Korea

- 7.4.6 Indonesia

- 7.4.7 Malaysia

- 7.4.8 Thailand

- 7.4.9 Vietnam

- 7.4.10 Philippines

- 7.4.11 Myanmar

- 7.4.12 Bangladesh

- 7.5 Middle East

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 Qatar

- 7.5.4 Turkey

- 7.5.5 Iran

- 7.5.6 Oman

- 7.6 Africa

- 7.6.1 Egypt

- 7.6.2 Nigeria

- 7.6.3 Algeria

- 7.6.4 South Africa

- 7.6.5 Angola

- 7.6.6 Kenya

- 7.6.7 Mozambique

- 7.7 Latin America

- 7.7.1 Brazil

- 7.7.2 Mexico

- 7.7.3 Argentina

- 7.7.4 Chile

Chapter 8 Company Profiles

- 8.1 Aggreko

- 8.2 Ashok Leyland

- 8.3 Atlas Copco AB

- 8.4 Caterpillar

- 8.5 Cummins, Inc.

- 8.6 Deere & Company

- 8.7 Generac Power Systems, Inc.

- 8.8 Greaves Cotton Limited

- 8.9 HIMOINSA

- 8.10 J C Bamford Excavators Ltd.

- 8.11 Kirloskar

- 8.12 Kohler Co.

- 8.13 Mahindra Powerol

- 8.14 Mitsubishi Heavy Industries Ltd.

- 8.15 Powerica Limited

- 8.16 Sterling and Wilson Pvt. Ltd.

- 8.17 Wärtsilä

- 8.18 Yamaha Motor Co., Ltd.

发电机市场-2025年至2030年预测

发电机市场-2025年至2030年预测 柴油动力建筑发电机组市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)

柴油动力建筑发电机组市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年) 全球发电机市场(至2030年):依燃料种类(柴油、天然气、液化石油气、生质燃料)、额定输出功率(50kW以下、51-280kW、281-500kW、501-2000kW、2001-3500kW、3500kW以上)、销售管道、最终

全球发电机市场(至2030年):依燃料种类(柴油、天然气、液化石油气、生质燃料)、额定输出功率(50kW以下、51-280kW、281-500kW、501-2000kW、2001-3500kW、3500kW以上)、销售管道、最终 住宅发电机市场按应用、产品类型、销售管道、功率输出和燃料类型划分-2025-2032年全球预测全球发电机组市场(按燃料类型、类型、相数、额定功率和最终用户划分)- 2025 年至 2032 年预测双燃料发电机市场按运转模式、功率输出、最终用户、引擎转速、冷却方式、安装类型和喷射技术划分-2025-2032年全球预测双馈型感应发电机市场额定功率、类型、冷却方式和应用划分-2025-2032年全球预测发电机控制单元市场依产品类型、最终用途、应用、控制功能、电压等级、通讯技术、安装方式及技术标准划分-2025-2032年全球预测家用备用发电机市场按最终用户、燃料类型、相数类型、额定功率和分销管道划分 - 全球预测 2025-2032黑启动发电机市场:2025-2032年全球预测(依燃料类型、应用、功率输出、冷却方式及相数划分)

住宅发电机市场按应用、产品类型、销售管道、功率输出和燃料类型划分-2025-2032年全球预测全球发电机组市场(按燃料类型、类型、相数、额定功率和最终用户划分)- 2025 年至 2032 年预测双燃料发电机市场按运转模式、功率输出、最终用户、引擎转速、冷却方式、安装类型和喷射技术划分-2025-2032年全球预测双馈型感应发电机市场额定功率、类型、冷却方式和应用划分-2025-2032年全球预测发电机控制单元市场依产品类型、最终用途、应用、控制功能、电压等级、通讯技术、安装方式及技术标准划分-2025-2032年全球预测家用备用发电机市场按最终用户、燃料类型、相数类型、额定功率和分销管道划分 - 全球预测 2025-2032黑启动发电机市场:2025-2032年全球预测(依燃料类型、应用、功率输出、冷却方式及相数划分)