|

市场调查报告书

商品编码

1708177

箱板纸包装市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Boxboard Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

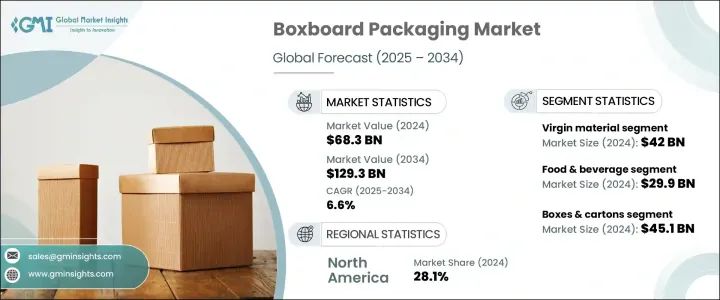

2024 年全球箱板纸包装市场规模达 683 亿美元,预估 2025 年至 2034 年的复合年增长率为 6.6%。受各行各业对永续、耐用、多功能包装解决方案需求不断增长的推动,市场将继续保持稳定成长。随着消费者偏好转向环保和轻质包装,纸板包装因其适应性和可回收性而越来越受到重视。城市化进程的加速和生活方式的改变进一步提高了对紧凑、方便和即用型包装的需求,尤其是在食品和饮料领域。

此外,电子商务的蓬勃发展,加上对美观和保护性包装的需求不断增长,为箱板包装製造商带来了新的机会。公司目前正在大力投资符合环境要求和消费者期望的创新设计和材料。随着世界各国政府加强对一次性塑胶的监管并强调循环经济的重要性,预计纸板包装市场仍将是全球包装领域的重要组成部分。从高檔化妆品到药品和快速消费品,纸板包装因其兼具外形、功能和永续性的能力而脱颖而出。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 683亿美元 |

| 预测值 | 1293亿美元 |

| 复合年增长率 | 6.6% |

市场主要以材料分为原生材料和再生材料两大类,其中原生材料部分在 2024 年创造 420 亿美元。原生箱板纸材料因其卓越的强度、光滑的表面和卓越的印刷品质而备受推崇,使其成为高端展示和强大保护至关重要的行业的理想选择。它们能够支持优质的饰面和详细的图形,使其成为奢侈品、化妆品和药品包装的首选。随着品牌越来越多地寻求不仅能保护产品而且还能增强其在商店货架上的视觉吸引力的包装,对原生材料的需求预计将保持强劲。

按最终用途行业细分,食品和饮料行业在 2024 年的规模为 299 亿美元,是纸板包装市场中最大的份额之一。即食食品、外带和方便食品消费量的不断增长直接影响了对轻量耐用包装解决方案的需求。随着消费者在不影响产品品质的情况下继续优先考虑便利性,提供保护和延长保质期的包装变得至关重要。此外,线上杂货配送和电子商务平台的快速扩张加剧了对坚固且可客製化的包装的需求,以确保产品的安全运输和储存。

从地区来看,2024 年北美占据了全球箱板纸包装市场的 28.1%。这种主导地位很大程度上得益于食品和饮料、製药和消费品等行业的强劲需求,这些行业都需要高品质和永续的包装选择。政府推出了严格的法规,鼓励使用环保包装并逐步淘汰一次性塑料,这推动了涂层再生板和固体漂白硫酸盐等可回收材料的采用。北美各地的公司正致力于增强其包装产品组合,以满足不断变化的消费者需求和监管标准,从而进一步推动区域市场的成长。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 食品饮料业的成长

- 对永续和环保包装的需求不断增长

- 印刷技术的进步

- 电子商务产业快速扩张

- 消费品产业的崛起

- 产业陷阱与挑战

- 供应链中断

- 原物料价格波动

- 成长动力

- 成长潜力分析

- 监管格局

- 技术格局

- 未来市场趋势

- 差距分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 策略仪表板

第五章:市场估计与预测:按材料,2021 年至 2034 年

- 主要趋势

- 处女

- 回收利用

第六章:市场估计与预测:按产品,2021 年至 2034 年

- 主要趋势

- 盒子和纸箱

- 插页和分隔页

- 托盘

- 其他的

第七章:市场估计与预测:依最终用途产业,2021 年至 2034 年

- 主要趋势

- 食品和饮料

- 製药

- 工业品

- 电子产品

- 其他的

第八章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

第九章:公司简介

- Cellmark

- CMPC Biopackaging

- Crusader Packaging

- Custom Boxes Zone

- DS Smith

- Folbb

- Graphic Packaging International

- Huhtamaki

- ITC

- James Cropper

- Metsa Group

- Mondi

- Netpak

- Nippon Paper Industries

- Sappi

- Smurfit Kappa

- Spento Papers

- Stora Enso

The Global Boxboard Packaging Market generated USD 68.3 billion in 2024 and is expected to grow at a CAGR of 6.6% from 2025 to 2034. The market continues to witness steady growth, fueled by the rising demand for sustainable, durable, and versatile packaging solutions across multiple industries. As consumer preferences shift toward eco-friendly and lightweight packaging, boxboard packaging is gaining prominence for its adaptability and recyclability. Increasing urbanization and changing lifestyles have further heightened the need for compact, convenient, and ready-to-use packaging, particularly within the food and beverage sector.

Additionally, the boom in e-commerce, coupled with the growing demand for attractive and protective packaging, is shaping new opportunities for boxboard packaging manufacturers. Companies are now investing heavily in innovative designs and materials that align with both environmental mandates and consumer expectations. With governments worldwide tightening regulations around single-use plastics and emphasizing the importance of circular economies, the boxboard packaging market is expected to remain a vital part of the global packaging landscape. From premium cosmetics to pharmaceutical products and fast-moving consumer goods, boxboard packaging stands out for its ability to combine form, function, and sustainability.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $68.3 Billion |

| Forecast Value | $129.3 Billion |

| CAGR | 6.6% |

The market is primarily segmented by material into virgin and recycled categories, with the virgin material segment generating USD 42 billion in 2024. Virgin boxboard materials are highly valued for their superior strength, smooth surface, and exceptional print quality, making them an ideal choice for industries where high-end presentation and robust protection are crucial. Their ability to support premium finishes and detailed graphics makes them a preferred option for luxury goods, cosmetics, and pharmaceutical packaging. The demand for virgin materials is expected to hold strong as brands increasingly seek packaging that not only protects the product but also enhances its visual appeal on store shelves.

When segmented by end-use industries, the food and beverage sector accounted for USD 29.9 billion in 2024, representing one of the largest shares in the boxboard packaging market. The rising consumption of ready-to-eat meals, takeout, and convenience foods is directly impacting the demand for lightweight and durable packaging solutions. As consumers continue to prioritize convenience without compromising product quality, packaging that offers both protection and extended shelf life is becoming essential. Moreover, the rapid expansion of online grocery delivery and e-commerce platforms has intensified the need for sturdy and customizable packaging to ensure safe product transport and storage.

Regionally, North America held a 28.1% share of the global boxboard packaging market in 2024. This dominance is largely driven by robust demand from industries such as food and beverage, pharmaceuticals, and consumer goods, all of which require high-quality and sustainable packaging options. Stringent government regulations encouraging eco-friendly packaging and phasing out single-use plastics are driving the adoption of recyclable materials like coated recycled boards and solid bleached sulfate. Companies across North America are focusing on enhancing their packaging portfolios to meet evolving consumer demands and regulatory standards, further boosting the regional market growth.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growth of food & beverage industry

- 3.2.1.2 Rise in demand for sustainable and Eco-friendly packaging

- 3.2.1.3 Advancement in printing technology

- 3.2.1.4 Rapid expansion of E-commerce industry

- 3.2.1.5 Rise in consumer goods industry

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Supply chain disruption

- 3.2.2.2 Fluctuation in raw materials price

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Material, 2021 – 2034 (USD Billion & Kilo Tons)

- 5.1 Key trends

- 5.2 Virgin

- 5.3 Recycled

Chapter 6 Market Estimates and Forecast, By Product, 2021 – 2034 (USD Billion & Kilo Tons)

- 6.1 Key trends

- 6.2 Boxes & cartons

- 6.3 Inserts & dividers

- 6.4 Trays

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By End Use Industry, 2021 – 2034 (USD Billion & Kilo Tons)

- 7.1 Key trends

- 7.2 Food & beverage

- 7.3 Pharmaceuticals

- 7.4 Industrial goods

- 7.5 Electronics

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Billion & Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Cellmark

- 9.2 CMPC Biopackaging

- 9.3 Crusader Packaging

- 9.4 Custom Boxes Zone

- 9.5 DS Smith

- 9.6 Folbb

- 9.7 Graphic Packaging International

- 9.8 Huhtamaki

- 9.9 ITC

- 9.10 James Cropper

- 9.11 Metsa Group

- 9.12 Mondi

- 9.13 Netpak

- 9.14 Nippon Paper Industries

- 9.15 Sappi

- 9.16 Smurfit Kappa

- 9.17 Spento Papers

- 9.18 Stora Enso