|

市场调查报告书

商品编码

1740851

冷冻马铃薯市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Frozen Potatoes Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

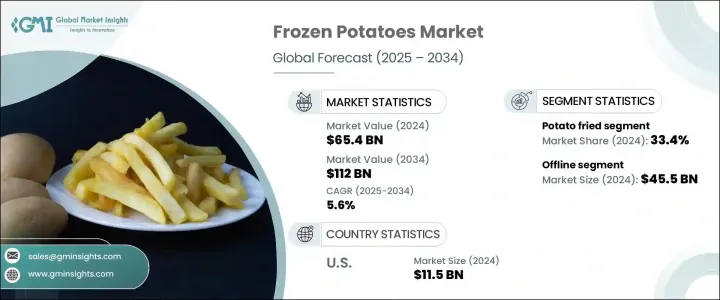

2024年,全球冷冻马铃薯市场规模达654亿美元,预计到2034年将以5.6%的复合年增长率成长,达到1120亿美元。这得归功于消费者生活方式的转变以及对便捷即食食品日益增长的需求。随着消费者在快节奏的日常生活和更紧凑的日程安排中忙碌,冷冻马铃薯已成为家庭厨房和专业餐饮服务场所的必备食品。此品类的稳定成长反映了消费者对便利饮食解决方案的广泛需求,这些解决方案在口味、品质和营养价值方面均不打折扣。冷冻马铃薯产品已不再局限于传统的炸薯条,而是涵盖了一系列创新产品,包括薯角、烘焙产品和无麸质产品,每一种都旨在满足现代消费者不断变化的需求。

人们对健康饮食习惯的认知日益增强,加上冷冻技术的进步,正在重塑市场模式。供应链物流的增强、快餐消费的激增以及新兴经济体的不断渗透,进一步增强了市场前景。随着全球饮食习惯转向速度、口味和种类,冷冻马铃薯产品势必将占据全球冷冻柜、菜单和外带平台的主导地位。这一上升趋势得益于製造商在产品创新、清洁标籤开发和分销管道优化方面的策略性投资,这些投资使冷冻马铃薯比以往任何时候都更容易获得。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 654亿美元 |

| 预测值 | 1120亿美元 |

| 复合年增长率 | 5.6% |

繁忙的都市生活方式和日益普及的快餐休閒餐饮是推动冷冻马铃薯产品成长的主要因素。随着人们寻求既美味又令人满意的快餐解决方案,对长保质期产品的需求也日益增长。餐饮服务业在提升销售方面发挥关键作用,提供品质稳定且易于大规模製备的冷冻马铃薯产品。经营者依靠这些产品来简化厨房操作,缩短准备时间,并在不牺牲风味和品质的情况下满足不断变化的客户需求。同时,随着越来越多的消费者在冰箱里储备各种用途广泛的马铃薯食品以方便在家食用,零售通路也蓬勃发展。

以健康为中心的创新正在为市场成长增添新的维度。低脂、气炸和无防腐剂的食品正吸引註重健康的消费者,他们希望在享受美味的同时,减少妥协。清洁标籤趋势日益流行,促使製造商推出低钠、无麸质和天然成分的产品。这些替代品不仅吸引了个人消费者,在学校、医院和公司餐厅等机构场所也越来越受欢迎,因为在这些场所,均衡营养和饮食合规是重中之重。随着口味和口感的不断改进,以及标籤的日益透明,这些「更健康」的选择正在渗透到主流市场和小众市场。

炸马铃薯目前占据最大的市场份额,2024 年占比为 33.4%,预计到 2034 年将以 4.8% 的复合年增长率成长。由于快餐连锁店的需求以及消费者对酥脆金黄口感的持续喜爱,炸马铃薯依然备受欢迎。除了薯条之外,其他形式的薯条,例如薯角、薯馅、薯片、薯条、薯条和烘焙薯条,也正在蓬勃发展。这些产品迎合了不同的烹饪偏好和饮食需求,薯条非常适合搭配丰盛的炖菜,而烘焙薯条则提供了更清淡、无油的选择,符合健康潮流。

在分销方面,餐饮服务领域在2024年占据了39.6%的市场份额,预计到2034年将以5.2%的复合年增长率成长。餐厅、餐饮服务和机构厨房严重依赖冷冻马铃薯产品来维持效率并提供稳定的菜餚。零售也是一个关键的成长动力,消费者越来越多地从超市、社区商店和线上平台购买即食马铃薯产品。

光是美国冷冻马铃薯市场在2024年就创造了115亿美元的产值,预计到2034年将以4.8%的复合年增长率稳定成长。美国强大的快餐文化和完善的餐饮服务提供者网路确保了持续的需求。连锁餐厅的菜单创新,加上冷冻产品在杂货店、会员制仓储式超市和专业零售商的广泛供应,共同推动了市场持续成长的势头。

全球冷冻马铃薯领域的主要参与者包括麦凯恩食品有限公司 (McCain Foods Limited)、JR Simplot 公司、Farm Frites International BV、Lamb Weston Holdings, Inc. 和 Cavendish Farms。这些公司正在积极投资美食风格产品线,与餐饮服务业者合作,向高成长地区扩张,并采用自动化技术来提高生产效率。随着对数位行销和电子商务的日益关注,领先品牌正在更直接、更有效地接触消费者,从而确保在全球市场上拥有强大的知名度、可及性和客户忠诚度。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 影响价值链的因素

- 利润率分析

- 中断

- 未来展望

- 製造商

- 经销商

- 川普政府关税

- 对贸易的影响

- 贸易量中断

- 报復措施

- 对产业的影响

- 供给侧影响(原料)

- 主要材料价格波动

- 供应链重组

- 生产成本影响

- 需求面影响(售价)

- 价格传导至终端市场

- 市占率动态

- 消费者反应模式

- 供给侧影响(原料)

- 受影响的主要公司

- 策略产业反应

- 供应链重组

- 定价和产品策略

- 政策参与

- 展望与未来考虑

- 对贸易的影响

- 贸易统计(HS编码)

- 2021-2024年主要出口国

- 2021-2024年主要进口国

註:以上贸易统计仅针对重点国家。

- 供应商格局

- 利润率分析

- 重要新闻和倡议

- 监管格局

- 衝击力

- 成长动力

- 方便食品和即食食品的需求不断增长

- 快餐店 (QSR) 的全球扩张

- 冷冻食品零售基础设施的成长

- 产业陷阱与挑战

- 对加工食品和油炸食品的健康担忧

- 气候影响导致生马铃薯价格波动

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第五章:市场规模及预测:依产品类型 2021 - 2034

- 主要趋势

- 炸马铃薯

- 马铃薯角

- 酿马铃薯

- 洋芋片

- 马铃薯块

- 马铃薯丁

- 烤马铃薯

- 其他的

第六章:市场规模及预测:依最终用途,2021 - 2034

- 主要趋势

- 餐饮服务

- 零售

- 速食店

- 家庭

第七章:市场规模及预测:按配销通路,2021 - 2034

- 主要趋势

- 离线

- 超市和大卖场

- 便利商店

- 专卖店

- 在线的

- 电子商务平台

- 公司自有网站

第八章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

第九章:公司简介

- Agristo

- Aviko BV

- Bart's Potato Company

- Cavendish Farms

- Farm Frites International BV

- JR Simplot Company

- Lamb Weston Holdings, Inc.

- McCain Foods Limited

- Mydibel Group

- Pohjolan Peruna Oy

The Global Frozen Potatoes Market was valued at USD 65.4 billion in 2024 and is estimated to grow at a CAGR of 5.6% to reach USD 112 billion by 2034, fueled by changing consumer lifestyles and an ever-increasing demand for convenient, ready-to-cook food options. As consumers juggle fast-paced routines and tighter schedules, frozen potatoes have become a staple in both household kitchens and professional food service settings. The category's steady rise reflects a broader shift toward convenient meal solutions that don't compromise on taste, quality, or nutritional value. Frozen potato products are no longer limited to traditional French fries-they now span an array of innovative offerings including wedges, baked options, and gluten-free varieties, each tailored to meet the evolving expectations of modern consumers.

Growing awareness around healthier eating habits, combined with advances in freezing technologies, is reshaping the market landscape. Enhanced supply chain logistics, a surge in quick-service restaurant consumption, and increasing penetration into emerging economies further strengthen the market's outlook. With global dining habits leaning toward speed, flavor, and variety, frozen potato products are set to dominate freezer aisles, menus, and food delivery platforms worldwide. This upward trend is underpinned by strategic manufacturer investments in product innovation, clean-label development, and enhanced distribution channels that make frozen potatoes more accessible than ever before.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $65.4 Billion |

| Forecast Value | $112 Billion |

| CAGR | 5.6% |

Busy urban lifestyles and the surging popularity of fast-casual dining are major factors driving the growth of frozen potato products. As people look for quick meal solutions that are both tasty and satisfying, the demand for long shelf-life options is rising. The food service industry plays a critical role in boosting sales, offering frozen potato products that deliver consistency and ease of preparation at scale. Operators rely on these items to streamline kitchen operations, reduce prep time, and meet fluctuating customer demands without sacrificing flavor or quality. At the same time, retail channels are thriving as more consumers stock their freezers with versatile potato items for at-home convenience.

Health-focused innovations are adding a new dimension to market growth. Low-fat, air-fried, and preservative-free options are catching the attention of health-conscious buyers who want indulgence with fewer compromises. Clean-label trends are gaining traction, prompting manufacturers to introduce products with reduced sodium, gluten-free attributes, and natural ingredients. These alternatives don't just appeal to individual consumers-they're also seeing increased uptake in institutional settings like schools, hospitals, and corporate cafeterias where balanced nutrition and dietary compliance are top priorities. As taste and texture continue to improve, and as labels become more transparent, these better-for-you options are penetrating both mainstream and niche markets alike.

Fried potatoes currently hold the largest share of the market, accounting for 33.4% in 2024, and are projected to grow at a CAGR of 4.8% through 2034. Their popularity remains strong due to the demand from fast-food chains and the enduring consumer love for crisp, golden textures. Beyond fries, other formats such as wedges, stuffed varieties, slices, dice, chunks, and baked alternatives are gaining momentum. These products cater to different cooking preferences and dietary needs, with chunks working well in hearty stews, and baked versions offering a lighter, oil-free option that aligns with wellness trends.

In terms of distribution, the food service segment held a 39.6% market share in 2024 and is set to grow at a CAGR of 5.2% through 2034. Restaurants, catering services, and institutional kitchens depend heavily on frozen potato offerings to maintain efficiency and deliver consistent dishes. Retail is also a key growth driver, with consumers increasingly purchasing ready-to-cook potato products from supermarkets, neighborhood stores, and online platforms.

The United States Frozen Potatoes Market alone generated USD 11.5 billion in 2024 and is forecasted to expand steadily at a CAGR of 4.8% through 2034. The nation's strong fast-food culture and well-established network of food service providers ensure consistent demand. Menu innovations across restaurant chains, coupled with the widespread availability of frozen products in grocery stores, club warehouses, and specialty retailers, contribute to the market's sustained momentum.

Key players in the global frozen potatoes space include McCain Foods Limited, J.R. Simplot Company, Farm Frites International B.V., Lamb Weston Holdings, Inc., and Cavendish Farms. These companies are actively investing in gourmet-style product lines, partnering with foodservice operators, expanding into high-growth regions, and embracing automation to enhance production efficiency. With a growing focus on digital marketing and e-commerce, leading brands are reaching consumers more directly and effectively-ensuring strong visibility, accessibility, and customer loyalty across global markets.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS Code)

- 3.3.1 Major exporting countries, 2021-2024 (Kilo Tons)

- 3.3.2 Major importing countries, 2021-2024 (Kilo Tons)

Note: the above trade statistics will be provided for key countries only.

- 3.4 Supplier landscape

- 3.5 Profit margin analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Rising demand for convenience and ready-to-eat foods

- 3.8.1.2 Expansion of quick service restaurants (QSRs) globally

- 3.8.1.3 Growth in frozen food retail infrastructure

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 Health concerns over processed and fried foods

- 3.8.2.2 Volatility in raw potato prices due to climate impact

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Size and Forecast, By Product Type 2021 - 2034 (USD Billion, Kilo Tons)

- 5.1 Key trends

- 5.2 Potato fried

- 5.3 Potato wedges

- 5.4 Stuffed potatoes

- 5.5 Potato slices

- 5.6 Potato chunks

- 5.7 Potato dices

- 5.8 Baked potato

- 5.9 Others

Chapter 6 Market Size and Forecast, By End Use, 2021 - 2034 (USD Billion, Kilo Tons)

- 6.1 Key trends

- 6.2 Foodservice

- 6.3 Retail

- 6.4 Quick service restaurants

- 6.5 Households

Chapter 7 Market Size and Forecast, By Distribution Channel, 2021 - 2034 (USD Billion, Kilo Tons)

- 7.1 Key trends

- 7.2 Offline

- 7.2.1 Supermarkets & hypermarkets

- 7.2.2 Convenience stores

- 7.2.3 Specialty stores

- 7.3 Online

- 7.3.1 E-commerce platforms

- 7.3.2 Company-owned websites

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Agristo

- 9.2 Aviko B.V.

- 9.3 Bart’s Potato Company

- 9.4 Cavendish Farms

- 9.5 Farm Frites International B.V.

- 9.6 J.R. Simplot Company

- 9.7 Lamb Weston Holdings, Inc.

- 9.8 McCain Foods Limited

- 9.9 Mydibel Group

- 9.10 Pohjolan Peruna Oy

冷冻马铃薯市场规模、份额及成长分析(按产品类型、规格、应用、最终用户和地区划分)-2026-2033年产业预测

冷冻马铃薯市场规模、份额及成长分析(按产品类型、规格、应用、最终用户和地区划分)-2026-2033年产业预测 全球冷冻薯条市场全球冷冻马铃薯市场

全球冷冻薯条市场全球冷冻马铃薯市场 全球冷冻马铃薯市场按产品、应用和地区划分(2026-2032 年)

全球冷冻马铃薯市场按产品、应用和地区划分(2026-2032 年) 亚太地区冷冻马铃薯市场预测至 2031 年 - 区域分析 - 按产品类型(炸薯条、薯饼、成型、马铃薯泥、裹麵糊/煮熟、配料/馅料等)和最终用户(住宅和商业)

亚太地区冷冻马铃薯市场预测至 2031 年 - 区域分析 - 按产品类型(炸薯条、薯饼、成型、马铃薯泥、裹麵糊/煮熟、配料/馅料等)和最终用户(住宅和商业) 北美冷冻马铃薯市场预测至 2031 年 - 区域分析 - 按产品类型(炸薯条、薯饼、成型、土豆泥、裹麵糊/煮熟、浇头/馅料等)和最终用户(住宅和商业)

北美冷冻马铃薯市场预测至 2031 年 - 区域分析 - 按产品类型(炸薯条、薯饼、成型、土豆泥、裹麵糊/煮熟、浇头/馅料等)和最终用户(住宅和商业) 欧洲冷冻马铃薯市场预测至 2031 年 - 区域分析 - 按产品类型(炸薯条、薯饼、成型、马铃薯泥、裹麵糊/煮熟、配料/馅料等)和最终用户(住宅和商业)

欧洲冷冻马铃薯市场预测至 2031 年 - 区域分析 - 按产品类型(炸薯条、薯饼、成型、马铃薯泥、裹麵糊/煮熟、配料/馅料等)和最终用户(住宅和商业) 冷冻马铃薯市场规模和预测、全球和区域份额、趋势和成长机会分析报告范围:按产品类型、最终用户和地理位置

冷冻马铃薯市场规模和预测、全球和区域份额、趋势和成长机会分析报告范围:按产品类型、最终用户和地理位置