|

市场调查报告书

商品编码

1741046

化学液氢市场机会、成长动力、产业趋势分析及2025-2034年预测Chemical Liquid Hydrogen Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

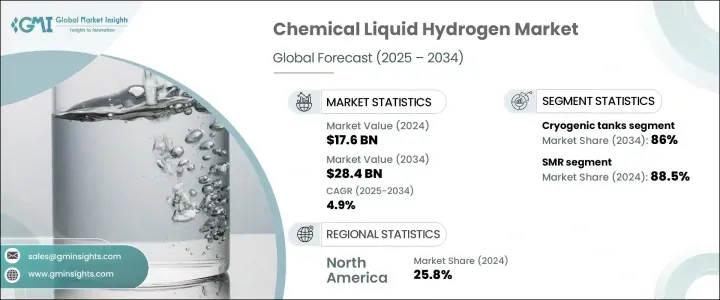

2024年,全球化学液氢市场规模达176亿美元,预计到2034年将以4.9%的复合年增长率增长,达到284亿美元,因为化学品生产商正在寻求低排放原料以符合全球气候目标。随着全球各行各业积极推动脱碳策略,对化学液氢的需求正在加速成长。各国政府和私人企业正大力投资氢能基础设施,以满足实现净零排放目标的迫切需求。受再生能源成本下降和技术突破的推动,市场正朝着绿色氢气生产方向转变。政策支持、投资者信心的增强以及策略性的公私合作伙伴关係正在为氢能发展创造一个充满活力的生态系统。电解槽改进、碳捕获技术和可扩展液化系统的资金投入不断增加,使化学液氢更具商业可行性和环境永续性。随着化学、重工业和交通运输等工业部门加大对清洁能源的投入,对可及性强、灵活的氢能解决方案的需求也变得更加迫切。这一势头为未来十年强劲的市场成长奠定了基础。

日益增长的绿氢能转型正在推动其在工业领域的应用。再生能源(尤其是太阳能和风能)成本的降低,使得电解氢更具商业可行性。同时,电解槽技术和碳捕集系统的进步正在提高生产流程的效率和永续性。这些创新使各行各业能够更快地实现脱碳,并满足监管要求。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 176亿美元 |

| 预测值 | 284亿美元 |

| 复合年增长率 | 4.9% |

灵活基础设施和定价模式的持续部署,使工业用户更容易获得氢气。透明的现货定价为那些倾向于按需供应且无需长期承诺的买家创造了新的机会,鼓励了跨行业的更广泛参与。这项进展增强了投资者信心,加速了清洁氢能计画的融资。公私部门合作伙伴关係持续协助推动基础建设,特别是液态氢的储存和运输。

用于氢气输送的大型氨转化和液化系统的商业化努力正在获得越来越多的关注。这些进展正在提高长途运输的经济可行性,有助于满足日益增长的全球需求。然而,现行的国际贸易政策提高了氢能相关设备的进口关税,这可能会推高未来的生产成本,从而在全球供应链中造成摩擦。这也可能限制创新,并减缓一些地区的市场扩张,尤其是在清洁能源基础设施尚在萌芽的地区。

煤气化领域在2024年创造了11亿美元的产值,预计到2034年将进一步成长。其吸引力在于将丰富的煤炭储量转化为氢气,支持能源多元化策略。随着人们越来越重视能源安全并减少对传统燃料进口的依赖,人们对这种方法的兴趣仍然浓厚。将碳捕获技术融入煤製氢工艺,使整个过程更加清洁,有助于衔接向完全可再生替代能源的过渡。

在分配方面,管道和低温储罐仍然是运输化学液氢的两种主要方式,每种方式根据用例和地理需求各有优势。 2024年,低温储槽占据了86%的市场份额,凸显了其在化学生产环境中储存和运输大量液态氢的关键作用。这些储槽经过精心设计,能够承受极低温度,将氢气保持在液化状态,并最大限度地减少储存和运输过程中的能量损失。真空绝缘和多层复合材料的创新进一步巩固了低温储罐的主导地位,这些创新显着降低了液化速率,并提高了整体安全性。

2024年,美国化学液氢市场产值达41亿美元,这得益于国家大力发展清洁能源,以及公部门和私部门的大量投资。联邦政府的激励措施、拨款和政策框架推动了主要工业区域氢气生产和储存设施的快速发展。化工、重工业和交通运输等产业对氢能的兴趣日益浓厚,推动了对稳健氢气供应链的需求。

巴拉德动力系统公司、道达尔能源公司、查特工业公司、梅塞尔集团、林德公司、普拉格能源公司、ENGIE公司、空气化工产品公司、岩谷公司、ENEOS公司、大阳日酸公司、液化空气公司和Nel ASA等公司正专注于多种策略以巩固市场份额。关键倡议包括投资高效生产技术、与能源和化学公司建立策略联盟以及建造模组化、可扩展的氢气工厂。这些公司优先考虑透过数位整合来监控供应,并投资基础设施以确保可靠的能源分配,同时与区域清洁能源政策保持一致。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统

- 川普政府关税分析

- 对贸易的影响

- 贸易量中断

- 报復措施

- 对产业的影响

- 供应方影响(原料)

- 主要材料价格波动

- 供应链重组

- 生产成本影响

- 需求面影响(售价)

- 价格传导至终端市场

- 市占率动态

- 消费者反应模式

- 供应方影响(原料)

- 受影响的主要公司

- 策略产业反应

- 供应链重组

- 定价和产品策略

- 政策参与

- 展望与未来考虑

- 对贸易的影响

- 监管格局

- 产业衝击力

- 成长动力

- 产业陷阱与挑战

- 成长潜力分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 战略仪表板

- 创新与永续发展格局

第五章:市场规模及预测:依产量,2021 年至 2034 年

- 主要趋势

- 瓦斯化

- 小型磁共振

- 电解

第六章:市场规模及预测:依分布,2021 年至 2034 年

- 主要趋势

- 管道

- 低温储罐

第七章:市场规模及预测:依地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 世界其他地区

第八章:公司简介

- Air Liquide

- Air Products and Chemicals

- Ballard Power Systems

- Chart Industries

- ENGIE

- ENEOS Corporation

- Hexagon Composites

- Iwatani Corporation

- Linde

- Messer Group

- Nel ASA

- Plug Power

- TotalEnergies

- Taiyo Nippon Sanso Corporation

The Global Chemical Liquid Hydrogen Market was valued at USD 17.6 billion in 2024 and is estimated to grow at a CAGR of 4.9% to reach USD 28.4 billion by 2034 as chemical producers pursue low-emission feedstocks to align with global climate targets. Demand for chemical liquid hydrogen is accelerating as industries worldwide move aggressively toward decarbonization strategies. Governments and private players are investing heavily in hydrogen infrastructure, driven by the urgency to meet net-zero goals. The market is witnessing a shift toward green hydrogen production, fueled by lower renewable energy costs and technological breakthroughs. Policy support, growing investor confidence, and strategic public-private partnerships are creating a vibrant ecosystem for hydrogen development. Increasing funding in electrolyzer advancements, carbon capture technologies, and scalable liquefaction systems is making chemical liquid hydrogen more commercially feasible and environmentally sustainable. As industrial sectors such as chemicals, heavy industries, and transportation sectors ramp up their clean energy commitments, the need for accessible and flexible hydrogen solutions is becoming even more critical. This momentum is setting the stage for robust market growth through the next decade.

A growing shift toward green hydrogen is driving adoption across industrial applications. Cost reductions in renewable energy, particularly solar and wind, are making electrolytic hydrogen more commercially viable. Simultaneously, advancements in electrolyzer technology and carbon capture systems are improving the efficiency and sustainability of production processes. These innovations are allowing industries to decarbonize more rapidly and meet regulatory expectations.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $17.6 Billion |

| Forecast Value | $28.4 Billion |

| CAGR | 4.9% |

The increased deployment of flexible infrastructure and pricing models makes hydrogen more accessible to industrial users. Transparent spot pricing creates new opportunities for buyers who prefer on-demand supply without long-term commitments, encouraging broader participation across sectors. This progress boosts investor confidence, accelerating funding for clean hydrogen initiatives. Public-private partnerships continue to help in advancing infrastructure, particularly for liquid hydrogen storage and transportation.

Efforts to commercialize large-scale ammonia conversion and liquefaction systems for hydrogen distribution are gaining traction. These developments are improving the economic viability of long-distance transport, helping meet rising global demand. However, ongoing international trade policies that raise import tariffs on hydrogen-related equipment may inflate future production costs, creating friction in global supply chains. This may also restrict innovation and slow market expansion in several regions, particularly where clean energy infrastructure is still emerging.

The coal gasification segment generated USD 1.1 billion in 2024 and is poised to grow further by 2034. Its appeal lies in converting abundant coal reserves into hydrogen, supporting energy diversification strategies. As more emphasis is placed on energy security and reducing reliance on traditional fuel imports, interest in this method remains strong. Integrating carbon capture into coal-based hydrogen production makes the process cleaner, helping bridge the transition to fully renewable alternatives.

In terms of distribution, pipelines and cryogenic tanks remain the two primary methods for transporting chemical liquid hydrogen, each offering distinct advantages based on use cases and geographic needs. Cryogenic tanks held an 86% share in 2024, underscoring their critical role in enabling the storage and movement of large volumes of liquid hydrogen within chemical production environments. These tanks are engineered to withstand extreme cold temperatures, preserving hydrogen in its liquefied state and minimizing energy losses during storage and transport. Their dominance is further supported by innovations in vacuum insulation and multilayer composite materials, which significantly reduce boil-off rates and improve overall safety.

U.S. Chemical Liquid Hydrogen Market generated USD 4.1 billion in 2024, fueled by an aggressive national push toward clean energy, backed by significant public and private sector investments. Federal incentives, grants, and policy frameworks have enabled the rapid development of hydrogen production and storage facilities across key industrial regions. Increased interest from sectors such as chemicals, heavy industry, and transportation is driving the need for robust hydrogen supply chains.

Companies like Ballard Power Systems, TotalEnergies, Chart Industries, Messer Group, Linde, Plug Power, ENGIE, Air Products and Chemicals, Iwatani Corporation, ENEOS Corporation, Taiyo Nippon Sanso Corporation, Air Liquide, and Nel ASA are focusing on multiple strategies to secure market share. Key initiatives include investing in high-efficiency production technologies, forming strategic alliances with energy and chemical firms, and building modular, scalable hydrogen plants. These players prioritize digital integration for supply monitoring and investing in infrastructure to ensure reliable distribution while aligning with regional clean energy policies.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 – 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.2 Trump administration tariff analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Regulatory landscape

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Strategic dashboard

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Production, 2021 – 2034 (USD Billion & MT)

- 5.1 Key trends

- 5.2 Coal gasification

- 5.3 SMR

- 5.4 Electrolysis

Chapter 6 Market Size and Forecast, By Distribution, 2021 – 2034 (USD Billion & MT)

- 6.1 Key trends

- 6.2 Pipelines

- 6.3 Cryogenic tanks

Chapter 7 Market Size and Forecast, By Region, 2021 – 2034 (USD Billion & MT)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Italy

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 South Korea

- 7.4.5 Australia

- 7.5 Rest of World

Chapter 8 Company Profiles

- 8.1 Air Liquide

- 8.2 Air Products and Chemicals

- 8.3 Ballard Power Systems

- 8.4 Chart Industries

- 8.5 ENGIE

- 8.6 ENEOS Corporation

- 8.7 Hexagon Composites

- 8.8 Iwatani Corporation

- 8.9 Linde

- 8.10 Messer Group

- 8.11 Nel ASA

- 8.12 Plug Power

- 8.13 TotalEnergies

- 8.14 Taiyo Nippon Sanso Corporation

化学液氢市场规模、份额和成长分析:按纯度、製造方法、储存类型、应用、最终用户和地区划分-2026-2033年产业预测

化学液氢市场规模、份额和成长分析:按纯度、製造方法、储存类型、应用、最终用户和地区划分-2026-2033年产业预测 液氢市场规模、份额及成长分析(依生产方式、分销方式、终端用户产业及地区划分)-2026-2033年产业预测

液氢市场规模、份额及成长分析(依生产方式、分销方式、终端用户产业及地区划分)-2026-2033年产业预测 全球煤炭气化液氢市场全球电解液氢市场化学液氢全球市场全球液氢市场

全球煤炭气化液氢市场全球电解液氢市场化学液氢全球市场全球液氢市场 液氢市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

液氢市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 液氢-市场占有率分析、产业趋势与统计、成长预测(2025-2030)亚太液氢 -市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)北美液氢 -市场占有率分析、产业趋势与统计、成长预测(2025-2030)

液氢-市场占有率分析、产业趋势与统计、成长预测(2025-2030)亚太液氢 -市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)北美液氢 -市场占有率分析、产业趋势与统计、成长预测(2025-2030)