|

市场调查报告书

商品编码

1750453

素食配料市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Vegan Ingredients Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

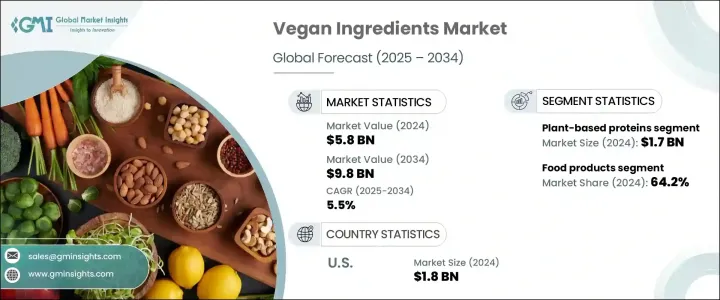

2024 年全球素食配料市场价值为 58 亿美元,预计到 2034 年将以 5.5% 的复合年增长率增长,达到 98 亿美元,这得益于向植物性食品的转变、消费者偏好的变化、环保意识的增强,以及比传统动物性食品更健康的替代品的普及。随着人们越来越注重自己的食物选择和对动物的道德对待,素食配料已成为食品创新的重点。人们对植物性营养日益增长的兴趣导致对植物蛋白的需求增加,包括大豆、豌豆、大米和扁豆,它们不仅更可持续,而且还在各种食品应用中提供功能性益处。这引发了食品生产、分配和消费方式的改变。

这一趋势背后的一个主要驱动力是植物性饮食的日益普及,这导致纯素食品在即食食品、零食、饮料甚至膳食补充剂等多个类别中呈现爆炸性增长。植物性成分的环境效益——生产所需的资源比动物产品更少——也推动了这一转变。政府支持永续农业和推广替代蛋白质来源的倡议进一步推动了市场扩张。随着对这些产品的需求不断增长,创新继续发挥重要作用,发酵菌蛋白等新成分不断进入市场,以提升植物性食品的口感和营养成分。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 58亿美元 |

| 预测值 | 98亿美元 |

| 复合年增长率 | 5.5% |

植物蛋白占了30.2%的市场份额,2024年的市值为17亿美元。这些来自大豆、豌豆和扁豆等作物的蛋白质,随着消费者寻求肉类替代品,正变得越来越受欢迎。随着各国政府大力推广豆类作物作为永续农业的重要作物,人们对植物蛋白的日益关注也导致了蛋白质来源的多样化。这些植物性蛋白质不仅被用于肉类替代品,还被用于其他食品,例如烘焙食品、零食和方便食品,这些食品的蛋白质含量被宣传为有益健康。

食品类产品在2024年价值37亿美元,在纯素食材市场占据主导地位,预计2034年将占64.2%的市场份额。此类别涵盖范围广泛,包括植物性乳製品和肉类替代品、即食烘焙食品、零食和糖果。该行业对纯素食材的巨大需求,主要源于消费者对健康益处、动物养殖伦理问题以及传统动物性食品生产对环境影响的意识不断增强。

2024年,美国纯素食材市场规模达18亿美元,预计2034年将持续维持6.3%的强劲复合年增长率。美国在消费和创新方面均处于领先地位,是全球市场的关键驱动力。推动这一增长的因素包括:个人健康意识的增强、对工厂化养殖伦理影响的日益担忧,以及向植物性饮食的转变。美国市场不仅满足了人们对更健康、更永续食品选择的需求,也推动了纯素食品的创新。

全球纯素原料市场的主要公司包括嘉吉、ADM、赢创、巴斯夫和Beyond Meat。这些公司一直致力于透过采用创新技术来扩展产品组合併改进产品供应。他们也透过投资环保生产流程和建立合作关係来推动植物基原料在各行各业的应用,从而加强永续发展。透过丰富产品系列并探索纯素原料的新应用,这些公司旨在巩固其在快速成长的市场中的地位。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 影响价值链的因素

- 利润率分析

- 中断

- 未来展望

- 製造商

- 经销商

- 川普政府关税

- 对贸易的影响

- 贸易量中断

- 报復措施

- 对产业的影响

- 供给侧影响(原料)

- 主要材料价格波动

- 供应链重组

- 生产成本影响

- 供给侧影响(原料)

- 需求面影响(售价)

- 价格传导至终端市场

- 市占率动态

- 消费者反应模式

- 受影响的主要公司

- 策略产业反应

- 供应链重组

- 定价和产品策略

- 政策参与

- 展望与未来考虑

- 对贸易的影响

- 贸易统计(HS编码)

- 2021-2024年主要出口国

- 2021-2024年主要进口国

- 供应商格局

- 利润率分析

- 重要新闻和倡议

- 监管格局

- 全球监理框架概览

- FDA法规

- 欧盟化妆品法规

- 中国化妆品监督管理条例

- 衝击力

- 成长动力

- 健康意识不断增强

- 环境永续性

- 植物性食品的技术进步

- 政府支持和政策倡议

- 产业陷阱与挑战

- 生产成本高

- 消费者认知度和接受度有限

- 成长动力

- 市场机会

- 向发展中经济体扩张

- 营养保健品和化妆品功能性素食成分的创新

- 为餐饮服务和自有品牌量身订製的 B2B 解决方案

- 永续包装和清洁标籤定位

- 市场进入和扩张策略

- 市场进入障碍与挑战

- 监管障碍和合规成本

- 智慧财产权限制

- 确立了玩家主导地位

- 技术专长要求

- 市场进入策略

- 合资企业和策略联盟

- 许可和技术转让

- 收购和棕地进入

- 绿地投资和有机成长

- 地理扩张机会

- 高成长区域市场

- 尚未开发的市场潜力评估

- 文化和监管考虑

- 在地化和适应策略

- 产品组合扩展策略

- 产品线延伸和产品变体

- 跨品类扩张

- 高端和价值细分市场定位

- 客製化和个人化方法

- 市场进入障碍与挑战

- 风险评估和缓解策略

- 市场风险

- 需求波动性和週期性

- 竞争强度与价格压力

- 替代产品和技术

- 消费者偏好转变

- 营运风险

- 供应链中断

- 品质控制和产品安全

- 製造和配方挑战

- 劳动力和人才管理

- 监理与合规风险

- 不断变化的监管格局

- 成分限制和禁令

- 标籤和行销索赔风险

- 市场风险

- 未来展望与市场预测

- 短期市场展望(1-2年)

- 立即成长的机会

- 近期挑战

- 竞争格局演变

- 中期市场展望(3-5年)

- 新兴市场领域

- 技术采用曲线

- 供需平衡预测

- 长期市场展望(5-10年)

- 颠覆性技术与创新

- 永续发展驱动的市场转型

- 消费者行为的演变

- 产业整合与重组情景

- 情境分析与应急计划

- 最佳成长情景

- 基准市场演变

- 最糟糕的市场萎缩

- 颠覆性情境分析

- 短期市场展望(1-2年)

- 投资机会和策略建议

- 投资吸引力评估

- 高成长细分市场

- 技术投资机会

- 地理投资热点

- 併购和合作机会

- 针对原料製造商的策略建议

- 产品开发与创新重点领域

- 市场定位和差异化策略

- 永续性和合规路线图

- 伙伴关係和合作机会

- 针对最终产品製造商的策略建议

- 配方和产品开发重点

- 消费者参与和行销策略

- 分销和通路优化

- 永续性和品牌定位

- 为投资者和金融利益相关者提供策略建议

- 高潜力投资目标

- 风险评估和缓解方法

- 投资组合多元化策略

- 退出策略考虑

- 投资吸引力评估

- 成长潜力分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第五章:市场估计与预测:按产品,2021 - 2034 年

- 主要趋势

- 植物蛋白

- 大豆蛋白

- 大豆分离蛋白

- 大豆浓缩蛋白

- 组织化大豆蛋白

- 大豆粉

- 其他的

- 豌豆蛋白

- 豌豆分离蛋白

- 豌豆蛋白浓缩物

- 组织豌豆蛋白

- 小麦蛋白

- 活性小麦麸质

- 小麦分离蛋白

- 组织化小麦蛋白

- 米蛋白

- 米分离蛋白

- 米蛋白浓缩物

- 其他的

- 马铃薯蛋白

- 藻类蛋白

- 螺旋藻

- 小球藻

- 其他的

- 大豆蛋白

- 植物基乳製品替代品

- 植物奶

- 杏仁奶成分

- 豆浆原料

- 燕麦奶成分

- 椰奶成分

- 米浆成分

- 其他的

- 植物性起司成分

- 蛋白质碱基

- 油脂

- 调味剂

- 功能性成分

- 植物优格成分

- 蛋白质碱基

- 培养物和发酵剂

- 质地改良剂

- 调味料

- 植物性奶油和涂抹酱原料

- 植物油脂

- 乳化剂

- 调味剂

- 着色剂

- 植物性冰淇淋原料

- 植物乳基

- 脂肪和油

- 甜味剂

- 稳定剂和乳化剂

- 植物奶

- 蛋替代品

- 淀粉类鸡蛋替代品

- 蛋白质类鸡蛋替代品

- 纤维类鸡蛋替代品

- 豆类蛋替代品

- 水果蛋替代品

- 鹰嘴豆水

- 植物性脂肪和油

- 椰子油

- 棕榈油

- 橄榄油

- 酪梨油

- 葵花籽油

- 菜籽油

- 特种植物油

- 结构化植物脂质

- 天然香料及增味剂

- 植物风味

- 植物甜味剂

- 鲜味增强剂

- 烟熏口味

- 香料萃取物

- 草本萃取物

- 自然色彩

- 花青素

- 类胡萝卜素

- 叶绿素

- 姜黄素

- 甜菜根

- 其他的

- 水胶体和组织剂

- 琼脂

- 角叉菜胶

- 瓜尔胶

- 刺槐豆胶

- 果胶

- 黄原胶

- 蒟蒻胶

- 改性淀粉

- 素食甜味剂

- 蔗糖

- 甜菜糖

- 椰子糖

- 枫糖浆

- 龙舌兰蜜

- 枣糖浆

- 甜菊糖

- 罗汉果萃取物

- 素食乳化剂

- 卵磷脂(大豆、葵花籽)

- 单甘油酯和双甘油酯(植物衍生)

- 柑橘纤维

- 其他的

- 素食防腐剂

- 迷迭香萃取物

- 生育酚

- 抗坏血酸

- 其他的

- 特色素食配料

- 营养酵母

- 海藻和藻类衍生物

- 发酵原料

- 其他的

第六章:市场估计与预测:按应用,2021 - 2034 年

- 主要趋势

- 食品

- 植物性肉类替代品

- 汉堡和肉饼

- 香肠和热狗

- 鸡块和鸡条

- 碎肉替代品

- 熟食切片

- 植物基乳製品替代品

- 牛奶替代品

- 起司替代品

- 优格替代品

- 奶油和抹酱替代品

- 冰淇淋替代品

- 烘焙产品

- 麵包和捲饼

- 蛋糕和糕点

- 饼干和饼干

- 糖果

- 小吃

- 美味小吃

- 能量棒

- 汤和肉汤

- 酱汁和肉汁

- 调味品和蛋黄酱替代品

- 即食食品

- 冷冻食品

- 婴儿配方奶粉和婴儿食品

- 植物性肉类替代品

- 饮料

- 植物奶

- 植物性蛋白质饮料

- 冰沙和果汁

- 咖啡和茶添加剂

- 酒精饮料

- 个人护理和化妆品

- 保养产品

- 护髮产品

- 彩妆

- 口腔护理产品

- 膳食补充剂

- 动物饲料替代品

- 宠物食品

- 牲畜饲料

- 水产饲料

- 其他的

第七章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙乌地阿拉伯

- 阿联酋

第八章:公司简介

- Aadhunik Ayurveda

- ADM

- BASF

- Beyond Meat

- Cargill

- Evonik

- Schouten

- Symega

- Tofurky

- Trader Joe's

The Global Vegan Ingredients Market was valued at USD 5.8 billion in 2024 and is estimated to grow at a CAGR of 5.5% to reach USD 9.8 billion by 2034, driven by the shift toward plant-based foods and changes in consumer preferences, increasing environmental awareness, and greater access to healthier alternatives compared to traditional animal-based options. As people become more conscious of their food choices and ethical treatment of animals, vegan ingredients have become a key focus in food innovation. The growing interest in plant-based nutrition has led to increased demand for plant proteins, including soy, pea, rice, and lentils, which are not only more sustainable but also offer functional benefits in a variety of food applications. This has sparked a transformation in how food is produced, distributed, and consumed.

A major driving force behind this trend is the growing adoption of plant-based diets, which has led to an explosion of vegan food products across multiple categories, such as ready-to-eat meals, snacks, beverages, and even dietary supplements. The environmental benefits of plant-based ingredients-requiring fewer resources to produce than animal products-have also spurred the shift. Government initiatives supporting sustainable agriculture and the promotion of alternative protein sources are further boosting the market's expansion. As demand for these products rises, innovation continues to play a significant role, with new ingredients such as fermented mycoprotein entering the market to enhance the texture and nutritional profile of plant-based foods.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.8 Billion |

| Forecast Value | $9.8 Billion |

| CAGR | 5.5% |

The plant-based proteins segment held a 30.2% share and was valued at USD 1.7 billion in 2024. These proteins, sourced from crops like soy, peas, and lentils, are becoming increasingly popular as consumers seek alternatives to meat. The growing focus on plant proteins has led to a diversification of protein sources, as governments also promote legumes and pulses as vital crops in sustainable agriculture. These plant-based proteins are being used not only in meat substitutes but also in other food items, such as baked goods, snacks, and convenience meals, where their protein content is marketed as a health benefit.

The food products segment, valued at USD 3.7 billion in 2024, holds a dominant position in the vegan ingredients market, representing 64.2% share through 2034. This category encompasses a wide range of offerings, including plant-based dairy and meat alternatives, ready-to-bake items, snacks, and sweets. The significant demand for vegan ingredients within this sector is largely driven by increasing consumer awareness regarding health benefits, ethical concerns about animal farming, and the environmental impact of traditional animal-based food production.

United States Vegan Ingredients Market was valued at USD 1.8 billion in 2024 and is expected to continue growing at a robust CAGR of 6.3% through 2034. The U.S. leads both in terms of consumption and innovation, serving as a key driver of the global market. Factors contributing to this surge include rising awareness about personal health, a growing concern over the ethical implications of factory farming, and a shift towards plant-based diets. The American market is not only responding to the demand for healthier and more sustainable food options but also driving forward innovation in vegan food products.

Key companies in the Global Vegan Ingredients Market include Cargill, ADM, Evonik, BASF, and Beyond Meat. These companies have been focusing on expanding their portfolios and improving product offerings by adopting innovative technologies. They are also enhancing their sustainability efforts by investing in eco-friendly production processes and forging partnerships to promote the adoption of plant-based ingredients across various industries. By diversifying their product ranges and exploring new applications for vegan ingredients, these firms aim to solidify their positions in the rapidly growing market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Demand-side impact (selling price)

- 3.2.3.1 Price transmission to end markets

- 3.2.3.2 Market share dynamics

- 3.2.3.3 Consumer response patterns

- 3.2.4 Key companies impacted

- 3.2.5 Strategic industry responses

- 3.2.5.1 Supply chain reconfiguration

- 3.2.5.2 Pricing and product strategies

- 3.2.5.3 Policy engagement

- 3.2.6 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS code)

- 3.3.1 Major exporting countries, 2021-2024 (kilo tons)

- 3.3.2 Major importing countries, 2021-2024 (kilo tons)

- 3.4 Supplier landscape

- 3.5 Profit margin analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.7.1 Global regulatory framework overview

- 3.7.2 FDA regulations

- 3.7.3 EU cosmetics regulation

- 3.7.4 China's CSAR (cosmetic supervision and administration regulation)

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Rising health consciousness

- 3.8.1.2 Environmental sustainability

- 3.8.1.3 Technological advancements in plant-based foods

- 3.8.1.4 Government support and policy initiatives

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 High production costs

- 3.8.2.2 Limited consumer awareness and acceptance

- 3.8.1 Growth drivers

- 3.9 Market opportunities

- 3.9.1 Expansion into developing economies

- 3.9.2 Innovation in functional vegan ingredients for nutraceuticals and cosmetics

- 3.9.3 Customized B2B solutions for food service and private label

- 3.9.4 Sustainable packaging and clean label positioning

- 3.10 Market entry and expansion strategies

- 3.10.1 Market entry barriers and challenges

- 3.10.1.1 Regulatory hurdles and compliance costs

- 3.10.1.2 Intellectual property constraints

- 3.10.1.3 Established player dominance

- 3.10.1.4 Technical expertise requirements

- 3.10.2 Market entry strategies

- 3.10.2.1 Joint ventures and strategic alliances

- 3.10.2.2 Licensing and technology transfer

- 3.10.2.3 Acquisition and brownfield entry

- 3.10.2.4 Greenfield investment and organic growth

- 3.10.3 Geographic expansion opportunities

- 3.10.3.1 High-growth regional markets

- 3.10.3.2 Untapped market potential assessment

- 3.10.3.3 Cultural and regulatory considerations

- 3.10.3.4 Localization and adaptation strategies

- 3.10.4 Product portfolio expansion strategies

- 3.10.4.1 Line extensions and product variants

- 3.10.4.2 Cross-category expansion

- 3.10.4.3 Premium and value segment targeting

- 3.10.4.4 Customization and personalization approaches

- 3.10.1 Market entry barriers and challenges

- 3.11 Risk assessment and mitigation strategies

- 3.11.1 Market risks

- 3.11.1.1 Demand volatility and cyclicality

- 3.11.1.2 Competitive intensity and price pressure

- 3.11.1.3 Substitute products and technologies

- 3.11.1.4 Consumer preference shifts

- 3.11.2 Operational risks

- 3.11.2.1 Supply chain disruptions

- 3.11.2.2 Quality control and product safety

- 3.11.2.3 Manufacturing and formulation challenges

- 3.11.2.4 Workforce and talent management

- 3.11.3 Regulatory and compliance risks

- 3.11.3.1 Changing regulatory landscape

- 3.11.3.2 Ingredient restrictions and bans

- 3.11.3.3 Labeling and marketing claim risks

- 3.11.1 Market risks

- 3.12 Future outlook and market projections

- 3.12.1 Short-term market outlook (1-2 years)

- 3.12.1.1 Immediate growth opportunities

- 3.12.1.2 Near-term challenges

- 3.12.1.3 Competitive landscape evolution

- 3.12.2 Medium-term market outlook (3-5 years)

- 3.12.2.1 Emerging market segments

- 3.12.2.2 Technology adoption curves

- 3.12.2.3 Supply-demand balance projections

- 3.12.3 Long-term market outlook (5-10 years)

- 3.12.3.1 Disruptive technologies and innovations

- 3.12.3.2 Sustainability-driven market transformation

- 3.12.3.3 Consumer behavior evolution

- 3.12.3.4 Industry consolidation and restructuring scenarios

- 3.12.4 Scenario analysis and contingency planning

- 3.12.4.1 Best-case growth scenario

- 3.12.4.2 Base-case market evolution

- 3.12.4.3 Worst-case market contraction

- 3.12.4.4 Disruptive scenario analysis

- 3.12.1 Short-term market outlook (1-2 years)

- 3.13 Investment opportunities and strategic recommendations

- 3.13.1 Investment attractiveness assessment

- 3.13.1.1 High-growth market segments

- 3.13.1.2 Technology investment opportunities

- 3.13.1.3 Geographic investment hotspots

- 3.13.1.4 M&A and partnership opportunities

- 3.13.2 Strategic recommendations for ingredient manufacturers

- 3.13.2.1 Product development and innovation focus areas

- 3.13.2.2 Market positioning and differentiation strategies

- 3.13.2.3 Sustainability and compliance roadmap

- 3.13.2.4 Partnership and collaboration opportunities

- 3.13.2.5 Strategic recommendations for end-product manufacturers

- 3.13.2.6 Formulation and product development priorities

- 3.13.2.7 Consumer engagement and marketing strategies

- 3.13.2.8 Distribution and channel optimization

- 3.13.2.9 Sustainability and brand positioning

- 3.13.3 Strategic recommendations for investors and financial stakeholders

- 3.13.3.1 High-potential investment targets

- 3.13.3.2 Risk assessment and mitigation approaches

- 3.13.3.3 Portfolio diversification strategies

- 3.13.3.4 Exit strategy considerations

- 3.13.1 Investment attractiveness assessment

- 3.14 Growth potential analysis

- 3.15 Porter’s analysis

- 3.16 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product, 2021 - 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Plant-based proteins

- 5.2.1 Soy protein

- 5.2.1.1 Soy protein isolates

- 5.2.1.2 Soy protein concentrates

- 5.2.1.3 Textured soy protein

- 5.2.1.4 Soy flour

- 5.2.1.5 Others

- 5.2.2 Pea protein

- 5.2.2.1 Pea protein isolates

- 5.2.2.2 Pea protein concentrates

- 5.2.2.3 Textured pea protein

- 5.2.3 Wheat protein

- 5.2.3.1 Vital wheat gluten

- 5.2.3.2 Wheat protein isolates

- 5.2.3.3 Textured wheat protein

- 5.2.4 Rice protein

- 5.2.4.1 Rice protein isolates

- 5.2.4.2 Rice protein concentrates

- 5.2.4.3 Others

- 5.2.5 Potato protein

- 5.2.6 Algae protein

- 5.2.6.1 Spirulina

- 5.2.6.2 Chlorella

- 5.2.6.3 Others

- 5.2.1 Soy protein

- 5.3 Plant-based dairy alternatives

- 5.3.1 Plant milks

- 5.3.1.1 Almond milk ingredients

- 5.3.1.2 Soymilk ingredients

- 5.3.1.3 Oat milk ingredients

- 5.3.1.4 Coconut milk ingredients

- 5.3.1.5 Rice milk ingredients

- 5.3.1.6 Others

- 5.3.2 Plant-based cheese ingredients

- 5.3.2.1 Protein bases

- 5.3.2.2 Oils and fats

- 5.3.2.3 Flavoring agents

- 5.3.2.4 Functional ingredients

- 5.3.3 Plant-based yogurt ingredients

- 5.3.3.1 Protein bases

- 5.3.3.2 Cultures and fermentation agents

- 5.3.3.3 Texturizing agents

- 5.3.3.4 Flavoring ingredients

- 5.3.4 Plant-based butter and spreads ingredients

- 5.3.4.1 Plant oils and fats

- 5.3.4.2 Emulsifiers

- 5.3.4.3 Flavoring agents

- 5.3.4.4 Coloring agents

- 5.3.5 Plant-based ice cream ingredients

- 5.3.5.1 Plant milk bases

- 5.3.5.2 Fats and oils

- 5.3.5.3 Sweeteners

- 5.3.5.4 Stabilizers and emulsifiers

- 5.3.1 Plant milks

- 5.4 Egg replacers

- 5.4.1 Starch-based egg replacers

- 5.4.2 Protein-based egg replacers

- 5.4.3 Fiber-based egg replacers

- 5.4.4 Legume-based egg replacers

- 5.4.5 Fruit-based egg replacers

- 5.4.6 Aquafaba

- 5.5 Plant-based fats and oils

- 5.5.1 Coconut oil

- 5.5.2 Palm oil

- 5.5.3 Olive oil

- 5.5.4 Avocado oil

- 5.5.5 Sunflower oil

- 5.5.6 Canola oil

- 5.5.7 Specialty plant oils

- 5.5.8 Structured plant lipids

- 5.6 Natural flavors and enhancers

- 5.6.1 Plant-based savory flavors

- 5.6.2 Plant-based sweet flavors

- 5.6.3 Umami enhancers

- 5.6.4 Smoke flavors

- 5.6.5 Spice extracts

- 5.6.6 Herb extracts

- 5.7 Natural colors

- 5.7.1 Anthocyanins

- 5.7.2 Carotenoids

- 5.7.3 Chlorophyll

- 5.7.4 Curcumin

- 5.7.5 Beetroot

- 5.7.6 Others

- 5.8 Hydrocolloids and texturizers

- 5.8.1 Agar-agar

- 5.8.2 Carrageenan

- 5.8.3 Guar gum

- 5.8.4 Locust bean gum

- 5.8.5 Pectin

- 5.8.6 Xanthan gum

- 5.8.7 Konjac gum

- 5.8.8 Modified starches

- 5.9 Vegan sweeteners

- 5.9.1 Cane sugar

- 5.9.2 Beet sugar

- 5.9.3 Coconut sugar

- 5.9.4 Maple syrup

- 5.9.5 Agave nectar

- 5.9.6 Date syrup

- 5.9.7 Stevia

- 5.9.8 Monk fruit extract

- 5.10 Vegan emulsifiers

- 5.10.1 Lecithin (soy, sunflower)

- 5.10.2 Mono- and diglycerides (plant-derived)

- 5.10.3 Citrus fiber

- 5.10.4 Others

- 5.11 Vegan preservatives

- 5.11.1 Rosemary extract

- 5.11.2 Tocopherols

- 5.11.3 Ascorbic acid

- 5.11.4 Others

- 5.12 Specialty vegan ingredients

- 5.12.1 Nutritional yeast

- 5.12.2 Seaweed and algae derivatives

- 5.12.3 Fermented ingredients

- 5.12.4 Others

Chapter 6 Market Estimates & Forecast, By Application, 2021 - 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Food products

- 6.2.1 Plant-based meat alternatives

- 6.2.1.1 Burgers and patties

- 6.2.1.2 Sausages and hot dogs

- 6.2.1.3 Nuggets and strips

- 6.2.1.4 Ground meat alternatives

- 6.2.1.5 Deli slices

- 6.2.2 Plant-based dairy alternatives

- 6.2.2.1 Milk alternatives

- 6.2.2.2 Cheese alternatives

- 6.2.2.3 Yogurt alternatives

- 6.2.2.4 Butter and spread alternatives

- 6.2.2.5 Ice cream alternatives

- 6.2.3 Bakery products

- 6.2.3.1 Breads and rolls

- 6.2.3.2 Cakes and pastries

- 6.2.3.3 Cookies and biscuits

- 6.2.4 Confectionery

- 6.2.5 Snacks

- 6.2.5.1 Savory snacks

- 6.2.5.2 Energy bars

- 6.2.6 Soups and broths

- 6.2.6.1 Sauces and gravies

- 6.2.6.2 Dressings and mayonnaise alternatives

- 6.2.7 Ready meals

- 6.2.8 Frozen meals

- 6.2.9 Infant formula and baby food

- 6.2.1 Plant-based meat alternatives

- 6.3 Beverages

- 6.3.1 Plant-based milk

- 6.3.2 Plant-based protein drinks

- 6.3.3 Smoothies and juices

- 6.3.4 Coffee and tea additives

- 6.3.5 Alcoholic beverages

- 6.4 Personal care and cosmetics

- 6.4.1 Skincare products

- 6.4.2 Haircare products

- 6.4.3 Color cosmetics

- 6.4.4 Oral care products

- 6.5 Dietary supplements

- 6.6 Animal feed alternatives

- 6.7 Pet food

- 6.7.1 Livestock feed

- 6.7.2 Aquaculture feed

- 6.7.3 Others

Chapter 7 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 UK

- 7.3.2 Germany

- 7.3.3 France

- 7.3.4 Italy

- 7.3.5 Spain

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 South Korea

- 7.4.5 Australia

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 MEA

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Aadhunik Ayurveda

- 8.2 ADM

- 8.3 BASF

- 8.4 Beyond Meat

- 8.5 Cargill

- 8.6 Evonik

- 8.7 Schouten

- 8.8 Symega

- 8.9 Tofurky

- 8.10 Trader Joe’s

全球纯素牛排市场规模、份额、趋势和成长分析报告(2026-2034)

全球纯素牛排市场规模、份额、趋势和成长分析报告(2026-2034) 纯素麵粉市场-全球产业规模、份额、趋势、机会及预测(依产品、类型、通路、地区及竞争格局划分,2021-2031年)

纯素麵粉市场-全球产业规模、份额、趋势、机会及预测(依产品、类型、通路、地区及竞争格局划分,2021-2031年) 纯素人造奶油市场规模、份额和成长分析(按产品类型、应用、销售管道、最终用户和地区划分)—2026-2033年产业预测

纯素人造奶油市场规模、份额和成长分析(按产品类型、应用、销售管道、最终用户和地区划分)—2026-2033年产业预测 纯素冷冻食品:全球市场份额和排名、总收入和需求预测(2025-2031 年)

纯素冷冻食品:全球市场份额和排名、总收入和需求预测(2025-2031 年) 全球素食鲔鱼市场全球素食快餐市场按产品类型、分销管道、消费者偏好和地区划分:未来预测

全球素食鲔鱼市场全球素食快餐市场按产品类型、分销管道、消费者偏好和地区划分:未来预测 全球素食鲔鱼市场按成分、用途、分销管道和地区划分

全球素食鲔鱼市场按成分、用途、分销管道和地区划分 素食冷冻食品市场:全球市场分析与预测(2030 年)

素食冷冻食品市场:全球市场分析与预测(2030 年) 纯素混合饮料市场、机会、成长动力、产业趋势分析与预测,2024-2032

纯素混合饮料市场、机会、成长动力、产业趋势分析与预测,2024-2032 到 2030 年全球纯素牛排市场预测:按原产地、分销管道、最终用户、地区划分

到 2030 年全球纯素牛排市场预测:按原产地、分销管道、最终用户、地区划分