|

市场调查报告书

商品编码

1755334

汽车语音辨识市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Automotive Voice Recognition Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

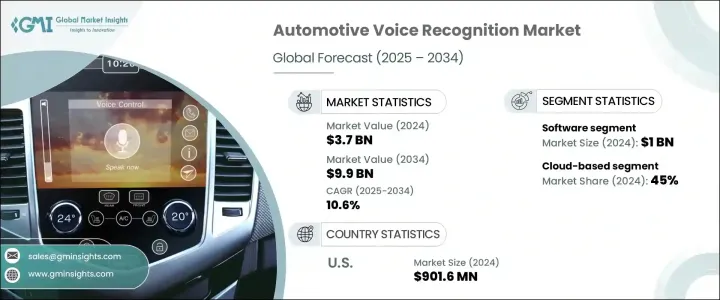

2024年,全球汽车语音辨识市场规模达37亿美元,预计2034年将以10.6%的复合年增长率成长,达到99亿美元。这得归功于先进语音控制系统的快速普及,因为越来越多的汽车采用旨在提升驾驶安全性和便利性的智慧技术。这些系统减少了驾驶员分心,提高了道路安全合规性。随着越来越多的汽车製造商致力于提供连网汽车,对语音辨识技术的需求持续成长。将这些系统与Google Assistant和Alexa等热门数位助理集成,可以显着提升汽车的吸引力和功能性,使用户能够控制各种汽车功能,例如资讯娱乐、空调设置,甚至车辆诊断。

5G 和云端运算技术的发展进一步推动了更复杂语音辨识功能的需求。借助 5G 低延迟和高频宽支援的即时音讯处理,车载语音助理如今能够即时响应,带来更丰富的用户体验。这些进步为汽车带来了新的功能和服务,增强了汽车的数位介面,并扩展了其功能。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 37亿美元 |

| 预测值 | 99亿美元 |

| 复合年增长率 | 10.6% |

2024年,软体市场价值达10亿美元。这个市场的重要性在于软体在语音辨识系统中的核心作用,尤其是在语音转文字、自然语言处理和命令处理等领域。人工智慧和机器学习的软体开发能够持续提升系统的准确性和个人化,使这些系统更能适应各种语言、驾驶偏好和车辆平台。

2024年,云端系统占据了45%的市场。云端系统能够无缝更新语音辨识程序,无需召回实体车辆,从而确保技术始终保持最新和竞争力。这些系统还可以与其他数位助理和智慧型装置集成,为用户提供跨平台、更互联的体验。云端系统支援即时学习,并可在全球范围内运行,从而提升了其在汽车语音识别市场的可扩展性和多功能性。

2024年,美国汽车语音辨识市场规模达9.016亿美元。美国在整合先进语音辨识系统的豪华高端汽车普及率方面处于领先地位。美国消费者高度重视人身安全和便利,进一步推动了对这些系统的需求。此外,凭藉成熟完善的汽车市场,美国持续在连网汽车技术方面投入巨资,确保其在语音辨识领域保持领先地位。

全球汽车语音辨识市场的主要参与者包括爱信精机、阿里巴巴集团、亚马逊、百度、博世、Cerence、大陆集团、Google、哈曼国际和微软。为了保持竞争优势,汽车语音辨识市场的公司越来越注重开发融合人工智慧和机器学习的先进软体,以实现更出色的语音命令识别和更个性化的用户体验。与汽车製造商和科技巨头的合作也正成为一种常见策略,因为各公司都希望将其语音辨识系统与数位助理和其他车载技术结合。各公司正大力投资研发,以突破即时处理的界限,减少延迟并改善语音控制系统的功能。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 汽车製造商

- 一级供应商

- 语音AI/软体供应商

- 云端基础设施供应商

- 硬体提供者

- 最终用途

- 利润率分析

- 专利分析

- 重要新闻和倡议

- 监管格局

- 语音辨识统计

- 采用率

- 使用模式

- 顾客偏好

- 成本細項分析

- 价格趋势

- 地区

- 硬体

- 衝击力

- 成长动力

- 连网汽车需求不断成长

- 消费者对车载资讯娱乐的偏好

- 云端运算和5G的成长

- 加强驾驶员安全法规

- 产业陷阱与挑战

- 实施成本高

- 与遗留系统的复杂集成

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第五章:市场估计与预测:按组件,2021 - 2034 年

- 主要趋势

- 硬体

- 麦克风

- 电子控制单元(ECU)

- 资讯娱乐主机/(HMI)

- 连接硬体

- 其他的

- 软体

- 自动语音辨识(ASR)

- 自然语言理解(NLU)

- 文字转语音 (TTS)

- 语音助理平台(定製或第三方)

- 其他的

- 服务

- OTA 更新(无线)

- 第三方应用程式集成

- 多语言支援服务

- 其他的

第六章:市场估计与预测:依部署模型,2021 - 2034 年

- 主要趋势

- 嵌入式

- 基于云端

- 杂交种

第七章:市场估计与预测:依车型,2021 - 2034 年

- 主要趋势

- 冰

- 电的

第八章:市场估计与预测:按应用,2021 - 2034 年

- 主要趋势

- 导航

- 气候控制

- 资讯娱乐

- 车辆管理

- 安全功能

- 其他的

第九章:市场估计与预测:依销售管道,2021 - 2034 年

- 主要趋势

- 原始设备製造商

- 售后市场

第十章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 北欧人

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 东南亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 阿联酋

- 南非

- 沙乌地阿拉伯

第 11 章:公司简介

- Aisin Seiki

- Alibaba Group

- Amazon

- Baidu Inc.

- Bosch

- Cerence

- Continental

- Emagine

- Harman International

- iNAGO

- Kardome

- Microsoft

- Nextgen Technologies

- Nissan

- Qualcomm Technologies

- Sensory

- SoundHound

- Speak With Me

- Visteon

The Global Automotive Voice Recognition Market was valued at USD 3.7 billion in 2024 and is estimated to grow at a CAGR of 10.6% to reach USD 9.9 billion by 2034, driven by the rapid adoption of advanced voice-controlled systems as more vehicles incorporate smart technology designed to enhance driving safety and convenience. These systems reduce driver distractions, improving safety compliance on the road. As more automakers strive to offer connected vehicles, the demand for voice recognition technology continues to rise. Integrating these systems with popular digital assistants, such as Google Assistant and Alexa, adds significant appeal and functionality, enabling users to control various car features, such as infotainment, climate settings, and even vehicle diagnostics.

The growth of 5G and cloud computing technologies has further propelled the demand for more sophisticated voice recognition capabilities. With real-time audio processing powered by 5G's low latency and high bandwidth, voice assistants in cars can now respond instantly, enabling a richer user experience. These advancements provide cars with new features and services, enhancing their digital interfaces and expanding their functions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.7 Billion |

| Forecast Value | $9.9 Billion |

| CAGR | 10.6% |

The software segment was valued at USD 1 billion in 2024. This segment's importance lies in the core role of software in voice recognition systems, particularly in areas like speech-to-text, natural language processing, and command processing. Software development, enhanced by AI and machine learning, allows for continuous improvements in system accuracy and personalization, making these systems more adaptable to various languages, driver preferences, and vehicle platforms.

The cloud-based segment held a 45% share in 2024. Cloud-based systems enable seamless updates to voice recognition programs without the need for physical vehicle recalls, ensuring that the technology remains up-to-date and competitive. These systems can also integrate with other digital assistants and smart devices, offering users a more connected experience across multiple platforms. Cloud systems support real-time learning and can operate globally, boosting their scalability and versatility in the automotive voice recognition market.

United States Automotive Voice Recognition Market reached USD 901.6 million in 2024. The U.S. leads in adopting luxury and high-end vehicles integrated with advanced voice recognition systems. Consumers in the U.S. place significant value on personal safety and convenience, further driving demand for these systems. Moreover, with an established and well-developed automotive market, the U.S. continues to make substantial investments in connected car technology, ensuring that the country remains a leading player in the voice recognition space.

Key players in the Global Automotive Voice Recognition Market include Aisin Seiki, Alibaba Group, Amazon, Baidu, Bosch, Cerence, Continental, Google, Harman International, and Microsoft. To maintain a competitive edge, companies in the automotive voice recognition market are increasingly focusing on developing advanced software that incorporates artificial intelligence and machine learning, allowing for better voice command recognition and more personalized user experiences. Partnerships with automakers and tech giants are also becoming a common strategy, as companies look to integrate their voice recognition systems with digital assistants and other in-car technologies. Companies are investing heavily in research and development to push the boundaries of real-time processing, reducing latency and improving the functionality of voice-controlled systems.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Automotive manufacturers

- 3.2.2 Tier 1 suppliers

- 3.2.3 Voice AI/software providers

- 3.2.4 Cloud infrastructure providers

- 3.2.5 Hardware providers

- 3.2.6 End use

- 3.3 Profit margin analysis

- 3.4 Patent analysis

- 3.5 Key news & initiatives

- 3.6 Regulatory landscape

- 3.7 Voice recognition statistics

- 3.7.1 Adoption rates

- 3.7.2 Usage patterns

- 3.7.3 Customer preferences

- 3.8 Cost breakdown analysis

- 3.9 Price trend

- 3.9.1 Region

- 3.9.2 Hardware

- 3.10 Impact forces

- 3.10.1 Growth drivers

- 3.10.1.1 Increasing demand for connected cars

- 3.10.1.2 Consumer preference for in-car infotainment

- 3.10.1.3 Growth in cloud computing and 5G

- 3.10.1.4 Enhanced driver safety regulations

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 High implementation costs

- 3.10.2.2 Complex integration with legacy systems

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Microphones

- 5.2.2 Electronic control units (ECUs)

- 5.2.3 Infotainment head unit / (HMI)

- 5.2.4 Connectivity hardware

- 5.2.5 Others

- 5.3 Software

- 5.3.1 Automatic speech recognition (ASR)

- 5.3.2 Natural language understanding (NLU)

- 5.3.3 Text-to-speech (TTS)

- 5.3.4 Voice assistant platforms (custom or third-party)

- 5.3.5 Others

- 5.4 Services

- 5.4.1 OTA updates (Over-the-Air)

- 5.4.2 Third-party app integrations

- 5.4.3 Multilingual support services

- 5.4.4 Others

Chapter 6 Market Estimates & Forecast, By Deployment Model, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Embedded

- 6.3 Cloud-based

- 6.4 Hybrid

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 ICE

- 7.3 Electric

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Navigation

- 8.3 Climate control

- 8.4 Infotainment

- 8.5 Vehicle management

- 8.6 Safety features

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 OEMs

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Aisin Seiki

- 11.2 Alibaba Group

- 11.3 Amazon

- 11.4 Baidu Inc.

- 11.5 Bosch

- 11.6 Cerence

- 11.7 Continental

- 11.8 Emagine

- 11.9 Google

- 11.10 Harman International

- 11.11 iNAGO

- 11.12 Kardome

- 11.13 Microsoft

- 11.14 Nextgen Technologies

- 11.15 Nissan

- 11.16 Qualcomm Technologies

- 11.17 Sensory

- 11.18 SoundHound

- 11.19 Speak With Me

- 11.20 Visteon