|

市场调查报告书

商品编码

1766198

自动填充分配器市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Automated Void Fill Dispensers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

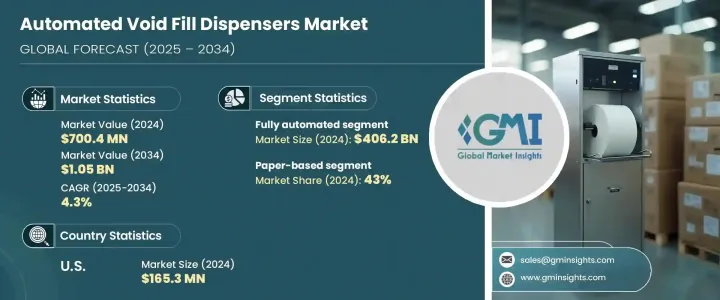

2024年,全球自动填充分配器市场规模达7.004亿美元,预计2034年将以4.3%的复合年增长率成长,达到10.5亿美元。这一成长主要得益于电子商务行业的快速扩张,这增加了对高效可持续包装解决方案的需求。自动填充分配器发挥着至关重要的作用,它使用纸张、泡棉或充气产品等缓衝材料填充包装中的空隙,从而在运输过程中保护物品。这些分配器可协助製造商优化材料使用,降低成本,同时提高包装效率。此外,人们对环保包装的日益重视也加速了这些机器的普及,因为它们能够实现精准分配,最大限度地减少浪费,并有助于遵守全球环保法规。

人工智慧和物联网的融合等技术进步,透过实现即时资料监控、预测性维护以及跨生产线的无缝连接,正在彻底改变机器效能。这些智慧功能不仅提高了效率和准确性,还能减少停机时间和营运成本。因此,这些智慧系统已成为现代自动化包装设施中不可或缺的一部分,因为速度、精确度和适应性对于满足日益增长的需求和保持竞争优势至关重要。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 7.004亿美元 |

| 预测值 | 10.5亿美元 |

| 复合年增长率 | 4.3% |

2024年,全自动包装领域占据市场主导地位,创造了4.062亿美元的收入,预计到2034年将以4.7%的复合年增长率成长。该领域的扩张得益于各行各业寻求节省人力、高效且能够处理大批量的包装解决方案。全自动分配器能够精确控制物料输出,减少浪费并促进永续发展。由于人工智慧和物联网等先进自动化技术的集成,它们在智慧仓库和製造工厂的应用日益广泛,从而提高了整体生产力和营运效率。

2024年,纸本产品占据了43%的市场份额,创造了可观的收入,预计2025-2034年期间的复合年增长率将达到4.5%。纸质填充剂因其可回收特性且符合日益严格的环保标准而备受青睐。随着法规的收紧,电商和包装行业的公司正在逐步淘汰不可回收和有毒材料,转而采用环保替代品,这使得纸质系统成为首选。

美国自动填充分配器市场占79%的市场份额,2024年市场规模达1.653亿美元。美国对永续发展和环保製造的重视,推动了对纸质填充解决方案的强劲需求。此外,向智慧工厂和自动化的转变,也推动了配备人工智慧视觉系统和物联网连接等智慧功能的全自动分配器的普及,从而提高包装作业的效率和产量。

全球自动填充分配器市场的主要参与者包括 EcoEnclose、Ranpak、IPG、Papier Sprick、Storopack Hans Reichenecker、Crawford Packaging、HexcelPack、The Packaging Club、Pregis、Kite Packaging、Ashtonne Packaging、Omni Group、Fromm Packaging Systems、Fromm Packaging Systems。为了巩固市场地位,领先的公司正在大力投资研发,以提高机器的精度、速度和能源效率。他们专注于整合尖端的人工智慧和物联网技术,以实现即时监控、预测性维护以及与其他包装系统的无缝连接。与包装製造商和电商公司建立策略合作伙伴关係,有助于这些公司根据特定客户需求客製化解决方案。此外,不断扩展的产品组合以涵盖可持续和可回收的填充材料,也体现了他们对环保合规的承诺。提供培训、售后支援和灵活的融资方案也有助于公司建立长期客户关係,并扩大其在新兴市场的影响力。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 利润率

- 每个阶段的增值

- 影响价值链的因素

- 产业衝击力

- 成长动力

- 电子商务产业的扩张

- 永续性和环境合规性

- 与智慧仓储和工业4.0的融合

- 产业陷阱与挑战

- 初始资本投入高

- 与现有仓储系统的整合挑战

- 永续性和过度包装问题

- 机会

- 成长动力

- 成长潜力分析

- 未来市场趋势

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 按产品

- 监管格局

- 标准和合规要求

- 区域监理框架

- 认证标准

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 中东和非洲

- 拉丁美洲

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:按类型,2021 - 2034 年

- 主要趋势

- 半自动化

- 全自动

第六章:市场估计与预测:按包装材料类型,2021 - 2034 年

- 主要趋势

- 纸本

- 泡沫基

- 其他的

第七章:市场估计与预测:按运营,2021 - 2034 年

- 主要趋势

- 融合的

- 独立

第八章:市场估计与预测:按产量,2021 - 2034 年

- 主要趋势

- 高达100公尺/分钟

- 100公尺/分钟 - 200公尺/分钟

- 200公尺/分钟以上

第九章:市场估计与预测:按最终用途产业,2021 - 2034 年

- 主要趋势

- 包装

- 电子商务

- 电子产品

- 製药

- 消费品

- 汽车

- 其他(家具和家居用品、化妆品和个人护理等)

第 10 章:市场估计与预测:按配销通路,2021 年至 2034 年

- 主要趋势

- 直销

- 间接销售

第 11 章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第十二章:公司简介

- Ashtonne Packaging

- Crawford Packaging

- EcoEnclose

- Fromm Packaging Systems

- HexcelPack

- IPG

- Kite Packaging

- Omni Group

- Papier Sprick

- Pregis

- Ranpak

- Sealed Air

- Storopack Hans Reichenecker

- The Packaging Club

- Zepak

The Global Automated Void Fill Dispensers Market was valued at USD 700.4 million in 2024 and is estimated to grow at a CAGR of 4.3% to reach USD 1.05 billion by 2034. This growth is primarily driven by the rapid expansion of the e-commerce sector, which has heightened the demand for efficient and sustainable packaging solutions. Automated void fill dispensers play a crucial role by filling empty spaces in packages with cushioning materials such as paper, foam, or air-based products to protect items during shipping. These dispensers help manufacturers optimize material usage, reducing costs while improving packaging efficiency. Furthermore, the growing emphasis on eco-friendly packaging has accelerated the adoption of these machines, as they allow for precise dispensing that minimizes waste and supports compliance with environmental regulations globally

Technological advancements, such as the integration of AI and IoT, are revolutionizing machine performance by enabling real-time data monitoring, predictive maintenance, and seamless connectivity across production lines. These smart capabilities not only boost efficiency and accuracy but also reduce downtime and operational costs. As a result, these intelligent systems have become indispensable in modern, automated packaging facilities, where speed, precision, and adaptability are critical to meeting ever-growing demands and maintaining competitive advantage.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $700.4 Million |

| Forecast Value | $1.05 Billion |

| CAGR | 4.3% |

In 2024, the fully automated segment dominated the market, generating USD 406.2 million in revenue and is expected to grow at a CAGR of 4.7% through 2034. This segment's expansion is fueled by industries seeking labor-saving, efficient packaging solutions capable of handling high volumes. Fully automated dispensers precisely control material output, reducing waste and boosting sustainability efforts. Their growing adoption in smart warehouses and manufacturing plants is propelled by the integration of advanced automation technologies like AI and IoT, which improve overall productivity and operational efficiency.

The paper-based segment held a 43% share in 2024, generating significant revenue and is anticipated to grow at a CAGR of 4.5% during 2025-2034. Paper-based void fill dispensers are favored due to their recyclable nature and alignment with increasingly strict environmental standards. As regulations tighten, companies across the e-commerce and packaging industries are phasing out non-recyclable and toxic materials in favor of eco-friendly alternatives, making paper-based systems the preferred choice.

United States Automated Void Fill Dispensers Market held 79% share and generated USD 165.3 million in 2024. The country's focus on sustainability and eco-conscious manufacturing has driven strong demand for paper-based void fill solutions. Additionally, the shift toward smart factories and automation supports the uptake of fully automated dispensers equipped with smart features like AI-powered vision systems and IoT connectivity to boost efficiency and throughput in packaging operations.

Key players competing in the Global Automated Void Fill Dispensers Market include EcoEnclose, Ranpak, IPG, Papier Sprick, Storopack Hans Reichenecker, Crawford Packaging, HexcelPack, The Packaging Club, Pregis, Kite Packaging, Ashtonne Packaging, Omni Group, Fromm Packaging Systems, Zepak, and Sealed Air. To strengthen their market presence, leading companies are investing heavily in R&D to enhance machine accuracy, speed, and energy efficiency. They are focusing on integrating cutting-edge AI and IoT technologies to enable real-time monitoring, predictive maintenance, and seamless connectivity with other packaging systems. Strategic partnerships with packaging manufacturers and e-commerce companies help these players customize solutions for specific client needs. Furthermore, expanding product portfolios to include sustainable and recyclable void fill materials supports their commitment to environmental compliance. Offering training, after-sales support, and flexible financing options also helps companies build long-term client relationships and expand their footprint in emerging markets.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Packaging material type

- 2.2.4 Operation

- 2.2.5 Output capacity

- 2.2.6 End use industry

- 2.2.7 Distribution channel

- 2.3 CXO prospectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expansion of e-commerce industry

- 3.2.1.2 Sustainability and environmental compliance

- 3.2.1.3 Integration with smart warehousing and industry 4.0

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial capital investment

- 3.2.2.2 Integration challenges with existing warehousing systems

- 3.2.2.3 Sustainability and over-packaging concerns

- 3.2.3 Opportunities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and Innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product

- 3.7 Regulatory landscape

- 3.7.1 standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Middle East and Africa

- 4.2.1.5 Latin America

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates & Forecast, By Type, 2021 - 2034 ($Million, Thousand Units)

- 5.1 Key trends

- 5.2 Semi-automated

- 5.3 Fully automated

Chapter 6 Market Estimates & Forecast, By Packaging Material Type, 2021 - 2034 ($Million, Thousand Units)

- 6.1 Key trends

- 6.2 Paper based

- 6.3 Foam based

- 6.4 Others

Chapter 7 Market Estimates & Forecast, By Operation, 2021 - 2034 ($Million, Thousand Units)

- 7.1 Key trends

- 7.2 Integrated

- 7.3 Standalone

Chapter 8 Market Estimates & Forecast, By Output Capacity, 2021 - 2034 ($Million, Thousand Units)

- 8.1 Key trends

- 8.2 Up to 100 m/min

- 8.3 100 m/min - 200 m/min

- 8.4 Above 200 m/min

Chapter 9 Market Estimates & Forecast, By End Use Industry, 2021 - 2034 ($Million, Thousand Units)

- 9.1 Key trends

- 9.2 Packaging

- 9.3 E-commerce

- 9.4 Electronics

- 9.5 Pharmaceutical

- 9.6 Consumer goods

- 9.7 Automotive

- 9.8 Others(furnishing and home goods, cosmetic and personal care, etc.)

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034 ($Million, Thousand Units)

- 10.1 Key trends

- 10.2 Direct sales

- 10.3 Indirect sales

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034 ($Million, Thousand Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Ashtonne Packaging

- 12.2 Crawford Packaging

- 12.3 EcoEnclose

- 12.4 Fromm Packaging Systems

- 12.5 HexcelPack

- 12.6 IPG

- 12.7 Kite Packaging

- 12.8 Omni Group

- 12.9 Papier Sprick

- 12.10 Pregis

- 12.11 Ranpak

- 12.12 Sealed Air

- 12.13 Storopack Hans Reichenecker

- 12.14 The Packaging Club

- 12.15 Zepak