|

市场调查报告书

商品编码

1766212

益生菌食品市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Probiotic Food Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

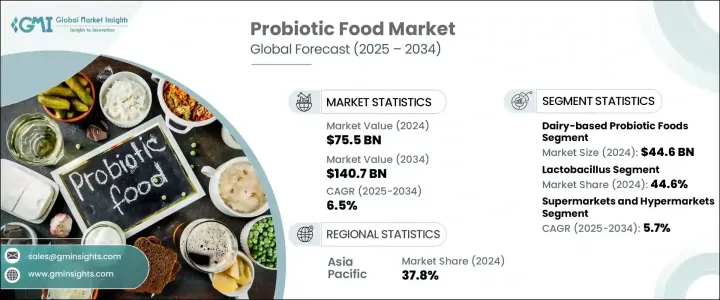

2024年,全球益生菌食品市场价值达755亿美元,预计到2034年将以6.5%的复合年增长率成长至1,407亿美元。这一强劲成长反映了消费者越来越重视预防性保健和功能性营养。大众对消化健康、心理健康和免疫系统支持的意识不断增强,推动了富含益生菌食品的日常消费。消费者也越来越多地寻求符合现代生活方式和健康价值观的功能性食品。植物性和非乳製品配方正吸引着纯素食者和乳糖不耐症人群的关注,而诸如耐储存胶囊和益生菌零食棒等创新产品也正在提高益生菌的可及性。益生菌也正从食品领域扩展到护肤和美容领域,拓展健康和保健运动的版图。

科学研究的进步和有利的监管支持持续为益生菌食品市场带来新的机会,促进创新并加速产品开发。正在进行的临床研究正在加深人们对特定益生菌菌株如何影响肠道健康、免疫力、心理健康、皮肤健康和代谢功能的理解。越来越多的证据鼓励製造商探索新的应用,并针对特定健康目标定製配方,从而为不同年龄和生活方式需求开闢专门的产品类别。各地区的监管机构也发挥关键作用,透过制定更清晰的指导方针、品质标准和安全规程,增强消费者信任,简化新产品的市场准入流程。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 755亿美元 |

| 预测值 | 1407亿美元 |

| 复合年增长率 | 6.5% |

在菌株细分方面,乳酸桿菌在2024年占据44.6%的市场份额,预计在2025-2034年期间的复合年增长率为5.3%。该菌株的吸引力在于其对各种产品类型的高度适应性,以及在多个食品加工阶段的耐受性。双歧桿菌因其对结肠健康的益处以及与儿科和老年营养的相关性而持续广泛应用。嗜热链球菌在益生菌生产中也发挥着至关重要的作用,尤其是在乳製品发酵过程中具有增味作用。同时,干型芽孢桿菌由于其较长的保质期和耐受极端条件的能力而使用量正在上升。

2024年,液体饮料市场占据了53.8%的市场份额,市场规模达到407亿美元。这一主导地位主要归功于功能性饮料的日益普及,它们提供了一种便捷高效的益生菌摄取方式。由于其吸收迅速、便于携带且易于融入日常生活,消费者对这类饮品趋之若鹋,尤其是那些生活方式积极且健康意识增强的消费者。便利营养的兴起进一步推动了即饮益生菌产品的需求,这与年轻都市族群寻求即时健康解决方案的偏好相契合。

2024年,亚太地区益生菌食品市场占37.8%的市占率。市场动态因地区而异,受饮食习惯、医疗保健系统和消费者意识差异的影响。受城镇化进程加快、可支配收入增加以及长期以来对发酵益生菌食品的文化认同的推动,亚太地区正经历着最快的扩张。随着日本、中国和印度等国中产阶级人口的持续成长,人们的健康意识显着增强,这些国家已成为重要的新兴市场。相较之下,儘管拉丁美洲面临负担能力的挑战,但医疗保健通路和零售基础设施的改善正在为市场发展创造有利条件。

全球益生菌食品市场的竞争者正采取多管齐下的策略来巩固其市场地位。 Probi AB、通用磨坊公司、雀巢公司、达能公司和养乐多本社等领先公司正大力投资产品创新,推出多样化的产品形式以适应不断变化的消费者生活方式。他们也透过策略合作、併购等方式扩大全球影响力。许多公司专注于清洁标籤配方和天然发酵成分,以满足日益增长的透明度和最低限度加工的需求。此外,研发投入正在帮助解锁新的菌株和应用,将益生菌从食品扩展到个人护理和补充剂领域。全球参与者也正在调整其行销和分销方式,以进军高成长区域市场。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 利润率

- 每个阶段的增值

- 影响价值链的因素

- 中断

- 产业衝击力

- 成长动力

- 产业陷阱与挑战

- 市场机会

- 成长潜力分析

- 监管格局

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL分析

- 价格趋势

- 按地区

- 按产品

- 未来市场趋势

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 专利态势

- 贸易统计(HS编码)(註:仅提供重点国家的贸易统计资料)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续实践

- 减少废弃物的策略

- 生产中的能源效率

- 环保倡议

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:依产品类型,2021 年至 2034 年

- 主要趋势

- 乳製品益生菌食品

- 优格

- 克菲尔

- 起司

- 酪乳

- 其他的

- 非乳製品益生菌食品

- 植物优格替代品

- 大豆基

- 杏仁基

- 椰子基

- 燕麦基

- 其他植物替代品

- 酸菜

- 泡菜

- 酸菜

- 泡菜

- 其他发酵蔬菜

- 发酵豆製品

- 豆豉

- 味噌

- 纳豆

- 康普茶

- 其他非乳製品

- 植物优格替代品

- 益生菌强化食品

- 谷物和零食

- 麵包店

- 糖果

- 营养棒

- 其他的

第六章:市场估计与预测:按益生菌菌株,2021 年至 2034 年

- 主要趋势

- 乳酸桿菌

- 嗜酸乳桿菌

- 鼠李糖乳桿菌

- 干酪乳桿菌

- 植物乳酸桿菌

- 其他的

- 双歧桿菌

- 双歧桿菌

- 长双歧桿菌

- 乳酸双歧桿菌

- 短双歧桿菌

- 其他的

- 链球菌

- 嗜热链球菌

- 其他的

- 芽孢桿菌

- 凝结芽孢桿菌

- 枯草桿菌

- 其他的

- 酵母菌

- 布拉氏酵母菌

- 其他的

- 多菌株配方

- 其他益生菌菌株

第七章:市场估计与预测:依形式,2021 年至 2034 年

- 主要趋势

- 液体

- 坚硬的

- 半固体

第八章:市场估计与预测:按配销通路,2021 年至 2034 年

- 主要趋势

- 超市和大卖场

- 便利商店

- 专卖店

- 网路零售

- 其他的

第九章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

第十章:公司简介

- Danone SA

- Yakult Honsha Co., Ltd.

- Nestle SA

- General Mills, Inc.

- Probi AB

- Lifeway Foods, Inc.

- BioGaia AB

- Chr. Hansen Holding A/S

- Lallemand Inc.

- Arla Foods amba

- Chobani, LLC

- Fonterra Co-operative Group Limited

- Kerry Group plc

- Kellogg Company

- PepsiCo, Inc.

The Global Probiotic Food Market was valued at USD 75.5 billion in 2024 and is estimated to grow at a CAGR of 6.5% to reach USD 140.7 billion by 2034. This robust growth reflects a broader shift among consumers toward preventive healthcare and functional nutrition. Growing public awareness around digestive health, mental well-being, and immune system support is fueling daily consumption of probiotic-rich food products. Consumers are increasingly seeking functional options that align with modern lifestyles and health values. Plant-based and dairy-free formulations are attracting attention from vegan and lactose-intolerant demographics, while innovations such as shelf-stable capsules and probiotic-infused snack bars are enhancing accessibility. Probiotics are also branching out beyond food into skincare and beauty, expanding the health and wellness movement.

Advancements in scientific research and favorable regulatory support continue to unlock new opportunities across the probiotic food market, fostering innovation and accelerating product development. Ongoing clinical studies are expanding the understanding of how specific probiotic strains impact not only gut health but also immunity, mental wellness, skin health, and metabolic function. This growing body of evidence is encouraging manufacturers to explore new applications and tailor formulations for targeted health outcomes, opening specialized product categories for different age groups and lifestyle needs. Regulatory bodies across various regions are also playing a critical role by establishing clearer guidelines, quality standards, and safety protocols, which are boosting consumer trust and streamlining market entry for new products.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $75.5 Billion |

| Forecast Value | $140.7 Billion |

| CAGR | 6.5% |

In terms of strain segmentation, the lactobacillus segment held a 44.6% share in 2024 and is forecasted to grow at a CAGR of 5.3% during 2025-2034. This strain's appeal lies in its high adaptability across various product types and its ability to survive numerous food processing stages. Bifidobacterium continues to see consistent use due to its benefits for colon health and its relevance in both pediatric and elderly nutrition. Streptococcus thermophilus also plays a vital role in probiotic production, particularly for its flavor-enhancing attributes in dairy fermentation. Meanwhile, the use of dry-form Bacillus species is rising due to their superior shelf life and ability to withstand extreme conditions.

The liquid segment captured a 53.8% share and generated USD 40.7 billion in 2024. This dominance is largely attributed to the growing popularity of functional beverages, which offer a convenient and efficient method of probiotic intake. Consumers are gravitating toward these options due to their quick absorption, portability, and ease of integration into daily routines, especially for those with active lifestyles and heightened health awareness. The rise of on-the-go nutrition has further propelled the demand for ready-to-drink probiotic products, aligning with the preferences of younger, urban populations seeking instant wellness solutions.

Asia Pacific Probiotic Food Market held a 37.8% share in 2024. Market dynamics vary by region, influenced by differences in dietary habits, healthcare systems, and consumer awareness. The Asia-Pacific region is witnessing the fastest expansion, driven by growing urbanization, rising disposable incomes, and a long-standing cultural familiarity with fermented probiotic foods. As the middle-class population continues to grow across countries like Japan, China, and India, there is a noticeable increase in health consciousness, positioning these nations as key emerging markets. In contrast, while Latin America faces affordability challenges, improvements in healthcare access and retail infrastructure are creating favorable conditions for market development.

Companies competing in the Global Probiotic Food Market are adopting multi-faceted strategies to strengthen their market presence. Leading firms such as Probi AB, General Mills, Inc., Nestle S.A., Danone S.A., and Yakult Honsha Co., Ltd. are investing significantly in product innovation, introducing diverse formats to suit changing consumer lifestyles. They are also expanding their global reach through strategic partnerships, mergers, and acquisitions. Many are focused on clean-label formulations and naturally fermented ingredients to align with the rising demand for transparency and minimal processing. Further, R&D investments are helping to unlock new strains and applications, extending probiotics beyond food into personal care and supplements. Global players are also tailoring their marketing and distribution approaches to tap into high-growth regional markets.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 End Use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 – 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Dairy-based probiotic foods

- 5.2.1 Yogurt

- 5.2.2 Kefir

- 5.2.3 Cheese

- 5.2.4 Buttermilk

- 5.2.5 Others

- 5.3 Non-dairy probiotic foods

- 5.3.1 Plant-based yogurt alternatives

- 5.3.1.1 Soy-based

- 5.3.1.2 Almond-based

- 5.3.1.3 Coconut-based

- 5.3.1.4 Oat-based

- 5.3.1.5 Other plant-based alternatives

- 5.3.2 Fermented vegetables

- 5.3.2.1 Kimchi

- 5.3.2.2 Sauerkraut

- 5.3.2.3 Pickles

- 5.3.2.4 Other fermented vegetables

- 5.3.3 Fermented soy products

- 5.3.3.1 Tempeh

- 5.3.3.2 Miso

- 5.3.3.3 Natto

- 5.3.4 Kombucha

- 5.3.5 Other non-dairy products

- 5.3.1 Plant-based yogurt alternatives

- 5.4 Probiotic-fortified foods

- 5.4.1 Cereals & snacks

- 5.4.2 Bakery

- 5.4.3 Confectionery

- 5.4.4 Nutrition bars

- 5.4.5 Others

Chapter 6 Market Estimates and Forecast, By Probiotic Strain, 2021 – 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.1.1 Lactobacillus

- 6.1.2 L. acidophilus

- 6.1.3 L. rhamnosus

- 6.1.4 L. casei

- 6.1.5 L. plantarum

- 6.1.6 Others

- 6.2 Bifidobacterium

- 6.2.1 B. bifidum

- 6.2.2 B. longum

- 6.2.3 B. lactis

- 6.2.4 B. breve

- 6.2.5 Others

- 6.3 Streptococcus

- 6.3.1 S. thermophilus

- 6.3.2 Others

- 6.4 Bacillus

- 6.4.1 B. coagulans

- 6.4.2 B. subtilis

- 6.4.3 Others

- 6.5 Saccharomyces

- 6.5.1 S. boulardii

- 6.5.2 Others

- 6.6 Multi-strain formulations

- 6.7 Other probiotic strains

Chapter 7 Market Estimates and Forecast, By Form, 2021 – 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Liquid

- 7.3 Solid

- 7.4 Semi-solid

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Supermarkets & Hypermarkets

- 8.3 Convenience stores

- 8.4 Specialty stores

- 8.5 Online retail

- 8.6 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Danone S.A.

- 10.2 Yakult Honsha Co., Ltd.

- 10.3 Nestle S.A.

- 10.4 General Mills, Inc.

- 10.5 Probi AB

- 10.6 Lifeway Foods, Inc.

- 10.7 BioGaia AB

- 10.8 Chr. Hansen Holding A/S

- 10.9 Lallemand Inc.

- 10.10 Arla Foods amba

- 10.11 Chobani, LLC

- 10.12 Fonterra Co-operative Group Limited

- 10.13 Kerry Group plc

- 10.14 Kellogg Company

- 10.15 PepsiCo, Inc.

全球益生菌市场规模、份额、趋势和成长分析报告(2026-2034年)

全球益生菌市场规模、份额、趋势和成长分析报告(2026-2034年) 肠道健康和益生菌食品市场预测至2032年:按产品类型、益生菌菌株、剂型、分销管道、最终用户和地区分類的全球分析

肠道健康和益生菌食品市场预测至2032年:按产品类型、益生菌菌株、剂型、分销管道、最终用户和地区分類的全球分析 益生菌在人类营养中的市场规模、份额和成长分析(按类型、应用和地区划分)—2026-2033年产业预测

益生菌在人类营养中的市场规模、份额和成长分析(按类型、应用和地区划分)—2026-2033年产业预测 全球宠物益生菌市场(至2030年):按类型(益生菌、益生元、后生元)、用途(干粮、湿粮、营养补充剂、零食)、宠物(犬、猫、其他)、剂型、功能、生产技术和地区划分全球卡夫发酵食品和益生菌食品市场:预测至2032年-按产品类型、成分、形态、包装、分销管道、最终用户和地区进行分析

全球宠物益生菌市场(至2030年):按类型(益生菌、益生元、后生元)、用途(干粮、湿粮、营养补充剂、零食)、宠物(犬、猫、其他)、剂型、功能、生产技术和地区划分全球卡夫发酵食品和益生菌食品市场:预测至2032年-按产品类型、成分、形态、包装、分销管道、最终用户和地区进行分析 益生菌市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)益生菌运动营养市场规模、占有率、成长及全球产业分析:依类型、应用和地区划分的洞察与预测(2024-2032 年)

益生菌市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)益生菌运动营养市场规模、占有率、成长及全球产业分析:依类型、应用和地区划分的洞察与预测(2024-2032 年) 益生菌:全球市场占有率和排名、总收入和需求预测(2025-2031年)

益生菌:全球市场占有率和排名、总收入和需求预测(2025-2031年) 益生菌的全球市场的评估:各产品类型,各成分,各流通管道,各地区,机会,预测(2018年~2032年)2032 年益生菌食品市场预测:按产品、成分类型、分销管道、最终用户和地区进行的全球分析

益生菌的全球市场的评估:各产品类型,各成分,各流通管道,各地区,机会,预测(2018年~2032年)2032 年益生菌食品市场预测:按产品、成分类型、分销管道、最终用户和地区进行的全球分析