|

市场调查报告书

商品编码

1766341

维生素成分市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Vitamin Ingredients Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

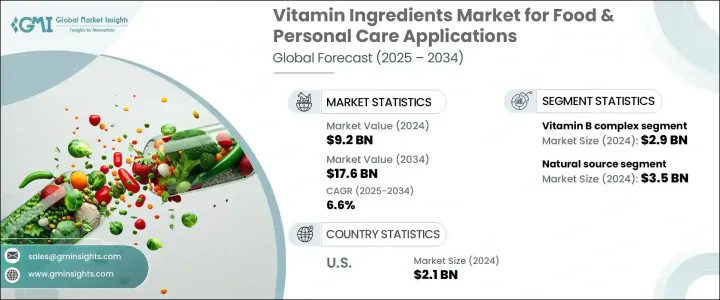

2024年,全球食品和个人护理用维生素成分市场规模达92亿美元,预计到2034年将以6.6%的复合年增长率成长,达到176亿美元。这一增长主要源于消费者对健康、营养和福祉日益增长的关注。随着人们更加积极主动地进行预防性医疗保健和膳食优化,全球范围内正在发生重大转变,这推动了对富含维生素产品的需求。由于微量营养素缺乏症和生活方式相关健康问题的日益普遍,强化食品和饮料以及补充剂和功能性个人护理用品的需求正在增长。

维生素正越来越多地被融入谷物、零食、乳製品和饮料等食品中,而个人护理品牌则将其融入护肤和护髮配方中,以满足消费者对抗衰老、补水和环保等功效的需求。这种跨行业的双重应用正在加速市场对维生素的接受度。在个人护理领域,维生素作为活性成分,具有抗发炎、亮白和修復功效,尤其是在精华液、乳液和洗髮精中。消费者对清洁标籤、植物源成分和功能性健康益处的偏好不断变化,进一步扩大了维生素成分(无论是在口服配方中还是外用配方中)的吸收。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 92亿美元 |

| 预测值 | 176亿美元 |

| 复合年增长率 | 6.6% |

2024年,B群维生素市场规模达29亿美元,预计2034年将以6.4%的复合年增长率成长。 B群维生素因在新陈代谢、能量生成、神经功能和产前护理中的重要作用而闻名,其种类繁多,包括B1、B2、B3、B6、B9和B12等。这些成分广泛用于膳食补充剂、能量饮料和强化食品。在个人护理领域,B3和B5等衍生物因其能够促进皮肤保湿、减少泛红和改善整体肤色而广受欢迎。由于B群维生素用途广泛且经济实惠,其仍是製造商的首选成分。其多功能性和功效使其成为各种营养和化妆品应用的理想选择,从而巩固了其在维生素成分领域的市场地位。

2024年,天然来源细分市场的价值为35亿美元,预计2025年至2034年期间的复合年增长率为6.5%,占38.2%的市场份额。消费者对清洁标章、天然萃取和植物性成分的偏好日益增长,推动品牌在产品配方中使用天然维生素来源。这些从植物、水果和蔬菜中提取的维生素被广泛认为更安全、更有效、更容易吸收。在食品和美容等高端类别中,对天然维生素的需求尤其高,因为这些类别注重透明度和永续性。天然来源,例如用于维生素C的西印度樱桃油和用于维生素E的葵花籽油,因其与有机和低加工配方的兼容性而被广泛采用,从而支持了产品开发向道德和透明化方向发展。

2024年,美国食品和个人护理用维生素成分市场规模达21亿美元,预计到2034年将以6.4%的复合年增长率成长。在美国,消费者对预防性保健的日益关注,加上对清洁标籤产品的认知度不断提升,持续推动市场需求。先进的食品和美容行业,加上强有力的监管支援和产品配方的创新,是推动市场扩张的关键因素。研发能力使企业能够提高生物利用度和功效,而当局发布的营养强化指南则有助于提升消费者的信任。富含维生素的护肤品和功能性食品的使用也促进了市场的成长。

在食品和个人护理用维生素成分市场中营运的主要公司包括巴斯夫、哥兰比亚、蓝星安迪苏、龙沙集团和帝斯曼。这些公司专注于创新、产品开发和扩大其天然成分组合以保持竞争力。为了加强其在食品和个人护理用维生素成分市场的地位,领先公司正在采取多管齐下的策略。这些措施包括扩大使用天然和清洁标籤成分的产品线、在食品和美容领域建立策略合作伙伴关係以及投资研发以提高成分的生物利用度和稳定性。公司还透过提供可追溯的采购和永续性认证来满足消费者对透明度的需求。此外,公司越来越多地瞄准产前护理、皮肤老化和纯素饮食等利基健康领域,以多样化其产品并进入高成长类别。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 利润率

- 每个阶段的增值

- 影响价值链的因素

- 中断

- 产业衝击力

- 成长动力

- 消费者对强化和功能性食品的需求不断增加。

- 提高个人健康和保健意识。

- 扩大维生素在护肤品和化妆品配方中的应用。

- 政府推动营养强化的措施。

- 产业陷阱与挑战

- 跨地区监管的复杂性

- 某些维生素配方的稳定性和保存期限问题

- 市场机会

- 成长动力

- 成长潜力分析

- 监管格局

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- Pestel 分析

- 价格趋势

- 按地区

- 按维生素

- 未来市场趋势

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 专利格局

- 贸易统计(HS编码)(註:仅提供重点国家的贸易统计资料)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续实践

- 减少废弃物的策略

- 生产中的能源效率

- 环保倡议

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:依维生素类型,2021-2034

- 主要趋势

- 维生素A

- 维生素B复合物

- 维生素B1(硫胺素)

- 维生素B2(核黄素)

- 维生素B3(烟碱酸)

- 维生素B5(泛酸)

- 维生素B6(吡哆醇)

- 维生素B7(生物素)

- 维生素B9(叶酸)

- 维生素B12(钴胺素)

- 维生素C(抗坏血酸)

- 维生素D

- 维生素 D2(麦角钙化醇)

- 维生素 D3(胆钙化醇)

- 维生素E

- 维生素K

第六章:市场估计与预测:依来源,2021-2034

- 主要趋势

- 自然的

- 植物基

- 动物性

- 微生物

- 合成的

- 半合成

第七章:市场估计与预测:依形式,2021-2034

- 主要趋势

- 粉末

- 液体

- 珠粒

- 胶囊

- 颗粒

- 其他的

第 8 章:市场估计与预测:按应用,2021 年至 2034 年

- 主要趋势

- 食品和饮料应用

- 功能性食品

- 强化食品

- 乳製品

- 烘焙和糖果

- 早餐麦片

- 婴儿配方奶粉

- 其他的

- 饮料

- 功能性饮料

- 果汁和冰沙

- 能量饮料

- 其他的

- 膳食补充剂

- 动物饲料

- 个人护理应用

- 保养品

- 抗衰老产品

- 保湿霜和乳霜

- 防晒产品

- 脸部精华液

- 其他的

- 护髮

- 洗髮精和护髮素

- 髮油和精华素

- 生髮产品

- 其他的

- 彩妆

- 口腔护理

- 身体护理

- 营养化妆品

- 其他的

- 保养品

第九章:市场估计与预测:按地区,2021-2034

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第十章:公司简介

- Adisseo (Bluestar Adisseo Company)

- Archer Daniels Midland Company (ADM)

- BASF SE

- DSM-Firmenich AG

- Eastman Chemical Company

- Fenchem Biotek Ltd.

- Foodchem International Corporation

- Glanbia plc

- Kappa Bioscience AS

- Koninklijke DSM NV

- Lonza Group

- Lycored

- Nutraceutical Corporation

- Prinova Group LLC

- Sternchemie GmbH & Co. KG

- The Lubrizol Corporation

- Vertellus Holdings LLC

- Vitablend Nederland BV

- Vitalife Biosciences

- Zhejiang NHU Co., Ltd

The Global Vitamin Ingredients Market for Food and Personal Care Applications was valued at USD 9.2 billion in 2024 and is estimated to grow at a CAGR of 6.6% to reach USD 17.6 billion by 2034. This growth is primarily driven by increasing consumer attention toward health, nutrition, and well-being. A significant shift is occurring worldwide as people become more proactive about preventive healthcare and dietary enhancement, fueling the demand for vitamin-enriched products. Fortified foods and beverages, along with supplements and functional personal care items, are gaining momentum due to the rising prevalence of micronutrient deficiencies and lifestyle-related health issues.

Vitamins are increasingly being integrated into food products like cereals, snacks, dairy, and beverages, while personal care brands are embedding them in skincare and haircare formulations to cater to demands for anti-aging, hydration, and environmental protection benefits. This dual application across sectors is accelerating market adoption. In personal care, vitamins serve as active ingredients offering anti-inflammatory, brightening, and restorative properties, particularly in serums, lotions, and shampoos. Evolving consumer preferences toward clean labels, plant-derived ingredients, and functional health benefits further amplify the uptake of vitamin ingredients, both in ingestible and topical formulations.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $9.2 Billion |

| Forecast Value | $17.6 Billion |

| CAGR | 6.6% |

The vitamin B complex segment accounted for USD 2.9 billion in 2024 and is expected to grow at a CAGR of 6.4% through 2034. Known for its essential role in metabolism, energy production, neurological function, and prenatal care, this category includes various forms like B1, B2, B3, B6, B9, and B12. These ingredients are widely formulated in dietary supplements, energy drinks, and fortified foods. In personal care, derivatives such as B3 and B5 are popular for their ability to support skin hydration, reduce redness, and enhance overall skin tone. Due to their wide applicability and cost-effectiveness, B complex vitamins remain a preferred ingredient for manufacturers. Their versatility and efficacy make them ideal for a range of both nutritional and cosmetic applications, strengthening their footprint in the vitamin ingredients space.

The natural source segment was valued at USD 3.5 billion in 2024 and is projected to grow at a CAGR of 6.5% between 2025 and 2034, holding a 38.2% market share. A growing consumer preference for clean-label, naturally derived, and plant-based ingredients is pushing brands to use natural vitamin sources in product formulations. These vitamins, extracted from botanicals, fruits, and vegetables, are widely perceived as safer, more effective, and better absorbed. Demand is especially high in premium categories across food and beauty, where transparency and sustainability are top priorities. Natural sources such as acerola for vitamin C or sunflower oil for vitamin E are widely adopted for their compatibility with organic and minimally processed formulations, supporting the push toward ethical and transparent product development.

U.S. Vitamin Ingredients Market for Food & Personal Care Applications was valued at USD 2.1 billion in 2024 and is anticipated to grow at a 6.4% CAGR through 2034. In the U.S., increasing consumer focus on preventive health, coupled with rising awareness of clean-label products, continues to fuel demand. The advanced food and beauty industries, combined with strong regulatory support and innovation in product formulation, are key factors driving market expansion. R&D capabilities allow companies to improve bioavailability and efficacy, while nutrient fortification guidelines issued by authorities foster consumer trust. The use of vitamin-infused skincare and functional foods also contributes to market traction.

Key companies operating in this Vitamin Ingredients Market for Food & Personal Care Applications include BASF, Glanbia, Bluestar Adisseo, Lonza Group, and DSM N.V. These players are focusing on innovation, product development, and expanding their natural ingredient portfolios to stay competitive. To strengthen their presence in the vitamin ingredients market for food and personal care, leading companies are adopting multi-pronged strategies. These include expanding product lines with natural and clean-label ingredients, forming strategic partnerships across food and beauty sectors, and investing in R&D to enhance ingredient bioavailability and stability. Firms are also leveraging consumer demand for transparency by offering traceable sourcing and sustainability certifications. In addition, companies are increasingly targeting niche health segments like prenatal care, aging skin, and vegan diets to diversify their offerings and tap into high-growth categories.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1.1 Regional

- 2.2.1.2 Vitamin type

- 2.2.1.3 Source

- 2.2.1.4 Form

- 2.2.1.5 Application

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: strategic imperatives

- 2.5 Executive decision points

- 2.6 Critical success factors

- 2.7 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising consumer demand for fortified and functional food products.

- 3.2.1.2 Increasing awareness of personal health and wellness.

- 3.2.1.3 Expanding application of vitamins in skincare and cosmetic formulations.

- 3.2.1.4 Government initiatives promoting nutrient fortification.

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Regulatory complexities across regions

- 3.2.2.2 Stability and shelf-life issues in certain vitamin formulations

- 3.2.3 Market opportunities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia pacific

- 3.4.4 Latin America

- 3.4.5 Middle east & Africa

- 3.5 Porter's analysis

- 3.6 Pestel analysis

- 3.6.1 Technology and innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By vitamin

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Vitamin Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Vitamin A

- 5.3 Vitamin B Complex

- 5.3.1 Vitamin B1 (Thiamine)

- 5.3.2 Vitamin B2 (Riboflavin)

- 5.3.3 Vitamin B3 (Niacin)

- 5.3.4 Vitamin B5 (Pantothenic Acid)

- 5.3.5 Vitamin B6 (Pyridoxine)

- 5.3.6 Vitamin B7 (Biotin)

- 5.3.7 Vitamin B9 (Folic Acid)

- 5.3.8 Vitamin B12 (Cobalamin)

- 5.4 Vitamin C (Ascorbic Acid)

- 5.5 Vitamin D

- 5.5.1 Vitamin D2 (Ergocalciferol)

- 5.5.2 Vitamin D3 (Cholecalciferol)

- 5.6 Vitamin E

- 5.7 Vitamin K

Chapter 6 Market Estimates & Forecast, By Source, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Natural

- 6.2.1 Plant-based

- 6.2.2 Animal-based

- 6.2.3 Microbial

- 6.3 Synthetic

- 6.4 Semi-synthetic

Chapter 7 Market Estimates & Forecast, By Form, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Powder

- 7.3 Liquid

- 7.4 Beadlets

- 7.5 Encapsulated

- 7.6 Granules

- 7.7 Others

Chapter 8 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Food & beverage applications

- 8.2.1 Functional foods

- 8.2.2 Fortified foods

- 8.2.2.1 Dairy products

- 8.2.2.2 Bakery & confectionery

- 8.2.2.3 Breakfast cereals

- 8.2.2.4 Infant formula

- 8.2.2.5 Others

- 8.2.3 Beverages

- 8.2.3.1 Functional drinks

- 8.2.3.2 Juices & smoothies

- 8.2.3.3 Energy drinks

- 8.2.3.4 Others

- 8.2.4 Dietary supplements

- 8.2.5 Animal feed

- 8.3 Personal care applications

- 8.3.1 Skincare

- 8.3.1.1 Anti-aging products

- 8.3.1.2 Moisturizers & creams

- 8.3.1.3 Sun care products

- 8.3.1.4 Facial serums

- 8.3.1.5 Others

- 8.3.2 Haircare

- 8.3.2.1 Shampoos & conditioners

- 8.3.2.2 Hair oils & serums

- 8.3.2.3 Hair growth products

- 8.3.2.4 Others

- 8.3.3 Color cosmetics

- 8.3.4 Oral care

- 8.3.5 Body care

- 8.3.6 Nutricosmetics

- 8.3.7 Others

- 8.3.1 Skincare

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Adisseo (Bluestar Adisseo Company)

- 10.2 Archer Daniels Midland Company (ADM)

- 10.3 BASF SE

- 10.4 DSM-Firmenich AG

- 10.5 Eastman Chemical Company

- 10.6 Fenchem Biotek Ltd.

- 10.7 Foodchem International Corporation

- 10.8 Glanbia plc

- 10.9 Kappa Bioscience AS

- 10.10 Koninklijke DSM N.V.

- 10.11 Lonza Group

- 10.12 Lycored

- 10.13 Nutraceutical Corporation

- 10.14 Prinova Group LLC

- 10.15 Sternchemie GmbH & Co. KG

- 10.16 The Lubrizol Corporation

- 10.17 Vertellus Holdings LLC

- 10.18 Vitablend Nederland B.V.

- 10.19 Vitalife Biosciences

- 10.20 Zhejiang NHU Co., Ltd