|

市场调查报告书

商品编码

1773356

宠物治疗饮食市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Pet Therapeutic Diet Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

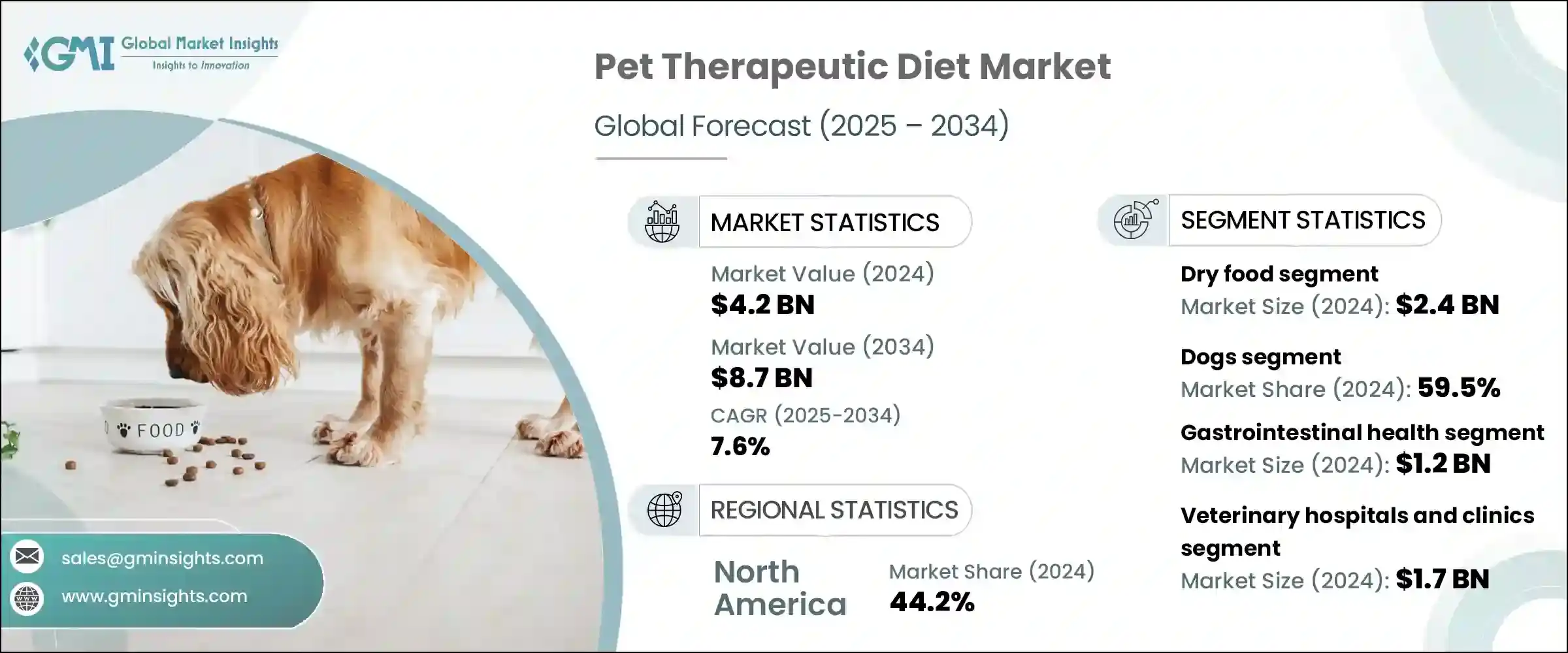

2024年,全球宠物治疗性饮食市场规模达42亿美元,预计到2034年将以7.6%的复合年增长率成长,达到87亿美元。伴侣动物日益增多的慢性健康问题(例如肥胖、糖尿病、肾臟病和胃肠道疾病)正在推动对有针对性的营养解决方案的需求。随着宠物主人越来越多地采用以家庭为中心的宠物护理方式,他们更愿意投资兼具预防和治疗功效的专用饮食。人们对负责任的宠物饲养意识的不断提高以及向主动健康管理的转变,正在强化这一趋势。

兽医指导的不断增长以及对更全面护理方案的需求进一步推动了治疗性营养的广泛应用。如今,许多宠物主人将营养视为管理宠物状况和确保长期健康的重要工具。宠物人性化趋势提高了人们对宠物食品品质和临床功效的期望。因此,越来越多的消费者选择针对特定疾病的饮食来支持康復和持续健康,这使得治疗性饮食成为新兴市场和已开发市场伴侣动物保健策略的核心组成部分。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 42亿美元 |

| 预测值 | 87亿美元 |

| 复合年增长率 | 7.6% |

宠物治疗性饮食是动物营养领域的一个专业领域,旨在帮助治疗、控製或预防宠物的特定疾病。这些配方在兽医护理中发挥关键作用,提供营养益处,以促进康復、减轻症状并促进整体健康。

2024年,干粮类别引领市场,估值达24亿美元。宠物主人和兽医青睐干粮,因为它经济实惠、保质期长、易于储存。这些产品能够可靠地控制饮食量,是需要持续治疗性营养的宠物的理想选择,尤其是那些正在管理慢性疾病的宠物。干粮配方旨在解决肥胖、肾臟疾病或胃肠道失衡等健康问题,使日常餵食更加轻鬆,同时确保宠物获得持续护理所需的营养。

2024年,犬类食品占了59.5%的市场。越来越多的犬类健康问题——尤其是肥胖——因缺乏运动的生活方式和富含人工成分的饮食而加剧——正在推动对治疗性食品的需求。犬隻频繁进食的天性使得为它们提供均衡、健康的饮食显得尤为重要。它们的饮食习惯和营养需求正日益影响宠物食品的选择,促使主人选择专门的治疗性食品来维持长期健康。

2024年,美国宠物治疗性饮食市场规模达17亿美元。宠物收养率的上升和老龄化动物数量的增加是市场扩张的主要推动因素。如今,许多宠物需要特殊饮食来控制心血管疾病、关节问题和其他慢性疾病。人们对宠物预防性保健措施的日益重视也推动了对治疗性饮食的需求。美国高度发达的兽医网络将这些饮食纳入长期治疗计划,使其成为疾病管理和常规动物护理的标准组成部分。宠物保险意识的提高和普及也使更多宠物主人能够探索更优质的饮食解决方案。

引领全球市场的公司包括兽医营养集团 (Veterinary Nutrition Group)、JustFoodForDogs、Open Farm、Diamond Pet Foods、Mars Petcare、Hill's Pet Nutrition、EmerAid、Stella and Chewy's、United PetFood、Eden Holistic Pet、Blue Buffalo (General Mills)、Virb、Ziwi、Iden Holistic Petacy Foods、Blue Buffalo (General.wi为了加强市场影响力,宠物治疗性饮食领域的公司正大力投资研发,以研发有科学根据、针对特定疾病的膳食。许多公司正在扩大产品线,以涵盖更广泛的健康问题,包括肾臟支持、消化系统护理、代谢健康和关节健康。与兽医和兽医诊所的合作正在提高产品的可信度和影响力。策略性行销工作强调临床疗效和优质成分,以建立消费者的信任。参与者还采用透明标籤和清洁配方,以满足注重健康的宠物主人的期望。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 每个阶段的增值

- 影响价值链的因素

- 产业衝击力

- 成长动力

- 宠物人口老化

- 宠物拥有量和宠物人性化程度的提高

- 伴侣动物慢性病盛行率不断上升

- 产品创新与客製化

- 产业陷阱与挑战

- 监管挑战和可靠性问题

- 认识和教育有限

- 市场机会

- 发展中地区宠物拥有量和都市化进程不断成长

- 对清洁标籤、有机和植物性治疗性饮食的需求不断增长

- 成长动力

- 成长潜力分析

- 监管格局

- 北美洲

- 欧洲

- 亚太地区

- 技术格局

- 定价分析

- 未来市场趋势

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 重点发展

- 併购

- 伙伴关係与协作

- 新产品发布

第五章:市场估计与预测:依产品类型,2021 年至 2034 年

- 主要趋势

- 干粮

- 湿食/罐头食品

- 其他产品类型

第六章:市场估计与预测:依动物类型,2021 年至 2034 年

- 主要趋势

- 猫

- 狗

- 其他动物

第七章:市场估计与预测:依健康状况,2021 年至 2034 年

- 主要趋势

- 肾臟健康

- 胃肠道健康

- 心血管健康

- 体重管理

- 关节护理

- 其他健康状况

第八章:市场估计与预测:按配销通路,2021 年至 2034 年

- 主要趋势

- 兽医医院和诊所

- 电子商务

- 零售药局

- 其他分销管道

第九章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第十章:公司简介

- Blue Buffalo (General Mills)

- Diamond Pet Foods

- Eden Holistic Pet Foods

- EmerAid

- Hill's Pet Nutrition

- iVet.com

- JustFoodForDogs

- Mars Petcare

- Nestle

- Open Farm

- Stella and Chewy's

- United PetFood

- Veterinary Nutrition Group

- Virbac

- Ziwi

The Global Pet Therapeutic Diet Market was valued at USD 4.2 billion in 2024 and is estimated to grow at a CAGR of 7.6% to reach USD 8.7 billion by 2034. Increasing chronic health issues in companion animals-such as obesity, diabetes, kidney disease, and gastrointestinal disorders-are driving the demand for targeted nutritional solutions. As pet owners increasingly adopt a family-centric approach to pet care, they're more willing to invest in specialized diets that offer both preventive and therapeutic benefits. Rising awareness about responsible pet ownership and a shift toward proactive health management are reinforcing this trend.

The broader adoption of therapeutic nutrition is further fueled by growing veterinary guidance and a demand for more holistic care options. Many pet parents now view nutrition as an essential tool for managing conditions and ensuring the long-term wellness of their animals. The trend toward pet humanization has elevated expectations for quality and clinical efficacy in pet food. As a result, more consumers are turning to condition-specific diets to support recovery and ongoing health, positioning therapeutic diets as a core component of companion animal healthcare strategies in both emerging and developed markets.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.2 Billion |

| Forecast Value | $8.7 Billion |

| CAGR | 7.6% |

Pet therapeutic diets represent a specialized segment within the animal nutrition sector, tailored to help treat, manage, or prevent specific medical conditions in pets. These formulations play a key role in veterinary care, delivering nutritional benefits designed to support recovery, reduce symptoms, and promote overall well-being.

The dry food category segment led the market in 2024, reaching a valuation of USD 2.4 billion. Pet owners and veterinarians prefer dry food due to its cost-effectiveness, long shelf life, and ease of storage. These products offer reliable portion control and are ideal for pets requiring consistent therapeutic nutrition, especially those managing chronic conditions. Designed to address health issues like obesity, kidney disease, or gastrointestinal imbalances, dry formulations make daily feeding routines easier while ensuring pets receive the necessary nutrients for ongoing care.

The dogs segment held a 59.5% share in 2024. A growing number of health concerns in dogs-particularly obesity, which is exacerbated by inactive lifestyles and diets high in artificial ingredients-are fueling demand for therapeutic food products. The natural tendency of dogs to consume food frequently increases the importance of feeding them balanced, health-oriented diets. Their dietary habits and nutritional needs are increasingly influencing pet food choices, encouraging owners to turn to specialized therapeutic options to maintain long-term health.

United States Pet Therapeutic Diet Market reached USD 1.7 billion in 2024. Rising pet adoption and the growing population of aging animals are major contributors to market expansion. Many pets now require specialized diets to manage cardiovascular conditions, joint problems, and other chronic illnesses. An increased focus on preventive health measures for pets is also boosting demand for therapeutic diets. The highly developed veterinary network in the U.S. incorporates these diets into long-term treatment plans, making them a standard part of disease management and routine animal care. Greater awareness and access to pet insurance are also enabling more owners to explore premium dietary solutions.

Companies leading the global market include Veterinary Nutrition Group, JustFoodForDogs, Open Farm, Diamond Pet Foods, Mars Petcare, Hill's Pet Nutrition, EmerAid, Stella and Chewy's, United PetFood, Eden Holistic Pet Foods, Blue Buffalo (General Mills), Virbac, Ziwi, Nestle, and iVet.com. To strengthen their market presence, companies in the pet therapeutic diet space are investing heavily in research and development to formulate science-backed, condition-specific diets. Many firms are expanding product lines to cover a wider range of health issues, including renal support, digestive care, metabolic health, and joint wellness. Collaborations with veterinarians and veterinary clinics are enhancing product credibility and reach. Strategic marketing efforts emphasize clinical efficacy and quality ingredients to build trust among consumers. Players are also adopting transparent labeling and clean formulations to align with the expectations of health-conscious pet owners.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Animal type

- 2.2.4 Health condition

- 2.2.5 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Aging pet population

- 3.2.1.2 Rising pet ownership and pet humanization

- 3.2.1.3 Growing prevalence of chronic disease in companion animals

- 3.2.1.4 Product innovation and customization

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Regulatory challenges and reliability concerns

- 3.2.2.2 Limited awareness and education

- 3.2.3 Market opportunities

- 3.2.3.1 Rising pet ownership and urbanization in developing regions

- 3.2.3.2 Growing demand for clean-label, organic and plant-based therapeutic diets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technological landscape

- 3.6 Pricing analysis

- 3.7 Future market trends

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key development

- 4.6.1 Mergers and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Dry food

- 5.3 Wet/ canned food

- 5.4 Other product types

Chapter 6 Market Estimates and Forecast, By Animal Type, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Cats

- 6.3 Dogs

- 6.4 Other animals

Chapter 7 Market Estimates and Forecast, By Health Condition, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Renal health

- 7.3 Gastrointestinal health

- 7.4 Cardiovascular health

- 7.5 Weight management

- 7.6 Joint care

- 7.7 Other health conditions

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Veterinary hospitals and clinics

- 8.3 E-commerce

- 8.4 Retail pharmacies

- 8.5 Other distribution channels

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Blue Buffalo (General Mills)

- 10.2 Diamond Pet Foods

- 10.3 Eden Holistic Pet Foods

- 10.4 EmerAid

- 10.5 Hill's Pet Nutrition

- 10.6 iVet.com

- 10.7 JustFoodForDogs

- 10.8 Mars Petcare

- 10.9 Nestle

- 10.10 Open Farm

- 10.11 Stella and Chewy's

- 10.12 United PetFood

- 10.13 Veterinary Nutrition Group

- 10.14 Virbac

- 10.15 Ziwi