|

市场调查报告书

商品编码

1822572

逻辑 IC 市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Logic IC Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

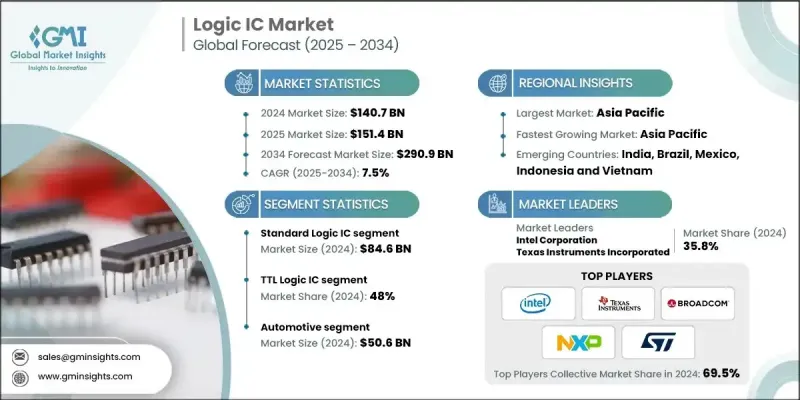

2024 年全球逻辑 IC 市场价值为 1,407 亿美元,预计到 2034 年将以 7.5% 的复合年增长率成长至 2,909 亿美元。

消费性电子产品的爆炸性成长是逻辑积体电路市场最重要的驱动力之一。智慧型手机、平板电脑、笔记型电脑、智慧型电视、游戏机和穿戴式科技等设备已成为全球数十亿用户日常生活中不可或缺的一部分。这些产品严重依赖逻辑积体电路来管理资料处理、讯号路由、电源管理和系统控制等任务。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 1407亿美元 |

| 预测值 | 2909亿美元 |

| 复合年增长率 | 7.5% |

标准逻辑IC将获得发展

标准逻辑IC领域在2024年实现了可观的成长,这得益于其在工业、消费性电子和运算设备中的基本讯号处理、定时和控制应用中的广泛应用。这些IC因其可靠性、相容性以及易于整合到各种电路设计中而备受推崇。虽然标准逻辑IC被认为是成熟的技术,但它在支援嵌入式系统、电源管理单元和周边介面的基础操作方面仍然具有重要意义。

TTL逻辑IC需求不断成长

受高速开关和一致逻辑电平驱动,TTL 逻辑 IC 领域在 2024 年占据了相当大的份额。儘管在较新的应用中 TTL IC 已被 CMOS 替代品所取代,但由于其坚固耐用和简单易用,仍在传统系统、测试设备和某些工业控制中使用。在教育工具和小批量工业应用中,TTL 领域继续发挥其价值,因为这些应用更重视讯号稳定性和速度,而不是功耗。

汽车领域采用率不断上升

2024年,汽车产业收入强劲成长,这得益于先进驾驶辅助系统(ADAS)、资讯娱乐系统、电动动力系统和电池管理系统等电子设备快速融入汽车。汽车製造商越来越依赖逻辑积体电路 (IC) 进行即时资料处理、安全监控和车联网 (V2X) 通讯。随着汽车朝向更高自动化程度迈进,对高可靠性、低延迟逻辑元件的需求持续成长。

区域洞察

亚太地区将崛起为利润丰厚的地区

2024年,亚太地区逻辑IC市场占据了相当大的份额,这得益于其强大的製造业基础、不断增长的消费电子产品需求以及对工业自动化不断增长的投资。中国大陆、韩国、日本和台湾等国家和地区不仅是逻辑IC的主要消费国,也是其重要的生产国,并拥有成熟的半导体生态系统和政府支持的创新政策。

逻辑 IC 市场的主要参与者包括莱迪思半导体公司、意法半导体公司、格罗方德公司、美满电子公司、亚德诺半导体公司、高通公司、英飞凌科技股份公司、三星电子有限公司、博通公司、赛灵思公司 (AMD)、英特尔公司、安升美林半导体公司、升特科技公司、德州仪器公司和电导公司。

为了巩固其在逻辑积体电路市场的地位,各大公司正在采取一系列措施,包括技术领先、供应链敏捷性和以应用为中心的创新。许多公司正在大力投入研发,以更小的製程节点和先进的封装技术开发逻辑积体电路,以满足速度、功率效率和整合度的需求。与代工厂和无晶圆厂设计公司的策略性收购和合作,正在帮助公司加快产品上市时间并取得新技术。

目录

第一章:方法论与范围

第 2 章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 利润率

- 成本结构

- 每个阶段的增值

- 影响价值链的因素

- 中断

- 衝击力

- 成长动力

- 工业自动化和智慧製造的需求不断增长

- 16 位元和 BiCMOS 逻辑 IC 技术的进步

- 汽车电子和ADAS中的逻辑IC集成

- 逻辑积体电路在消费性电子产品和边缘运算设备的应用

- 电信和资料中心基础架构中逻辑积体电路部署的扩展

- 产业陷阱与挑战

- 实施和升级成本高

- 来自替代处理和整合技术的竞争

- 成长动力

- 成长潜力分析

- 监管格局

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL分析

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 新兴商业模式

- 合规性要求

- 消费者情绪分析

- 专利和智慧财产权分析

- 地缘政治与贸易动态

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 市场集中度分析

- 关键参与者的竞争基准

- 财务绩效比较

- 收入

- 利润率

- 研发

- 产品组合比较

- 产品范围广度

- 科技

- 创新

- 地理位置比较

- 全球足迹分析

- 服务网路覆盖

- 各地区市场渗透率

- 竞争定位矩阵

- 领导者

- 挑战者

- 追踪者

- 利基市场参与者

- 战略展望矩阵

- 财务绩效比较

- 2021-2024 年关键发展

- 併购

- 伙伴关係与合作

- 技术进步

- 扩张和投资策略

- 数位转型计划

- 新兴/新创企业竞争对手格局

第五章:市场估计与预测:依类型,2021-2034

- 主要趋势

- 标准逻辑IC

- CMOS逻辑积体电路

- TTL逻辑IC

- BiCMOS逻辑积体电路

- 可程式逻辑装置(PLD)

- 可程式逻辑阵列(PLA)

- 可程式阵列逻辑(PAL)

- 复杂可程式逻辑装置(CPLD)

- 现场可程式闸阵列(FPGA)

第六章:市场估计与预测:依技术,2021-2034

- 主要趋势

- CMOS逻辑积体电路

- TTL逻辑IC

- BiCMOS逻辑积体电路

第七章:市场估计与预测:依最终用途产业,2021-2034

- 主要趋势

- 汽车

- 消费性电子产品

- 工业的

- 卫生保健

- 航太与国防

第八章:市场估计与预测:按地区,2021-2034

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 多边环境协定

- 南非

- 沙乌地阿拉伯

- 阿联酋

第九章:公司简介

- PNY Technologies Inc.

- Intel Corporation

- Texas Instruments Incorporated

- Broadcom Inc.

- NXP Semiconductors NV

- ON Semiconductor Corporation

- STMicroelectronics NV

- Microchip Technology Inc.

- Analog Devices, Inc.

- Infineon Technologies AG

- Renesas Electronics Corporation

- Xilinx, Inc. (AMD)

- Lattice Semiconductor Corporation

- Marvell Technology, Inc.

- Qualcomm Incorporated

- Semtech Corporation

- GlobalFoundries Inc.

- Samsung Electronics Co., Ltd.

The Global Logic IC Market was valued at USD 140.7 billion in 2024 and is estimated to grow at a CAGR of 7.5% to reach USD 290.9 billion by 2034.

The explosive growth in consumer electronics is one of the most significant drivers of the logic IC market. Devices such as smartphones, tablets, laptops, smart TVs, gaming consoles, and wearable technology have become essential parts of daily life for billions of users around the world. These products rely heavily on logic integrated circuits to manage tasks like data processing, signal routing, power management, and system control.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $140.7 billion |

| Forecast Value | $290.9 billion |

| CAGR | 7.5% |

Standard Logic IC to Gain Traction

The standard logic IC segment held sizable growth in 2024 owing to its widespread use in basic signal processing, timing, and control applications across industrial, consumer, and computing devices. These ICs are valued for their reliability, compatibility, and ease of integration into a variety of circuit designs. While considered mature technology, standard logic ICs remain relevant in supporting foundational operations in embedded systems, power management units, and peripheral interfaces.

Rising Demand for TTL Logic IC

The TTL logic IC segment held a significant share in 2024, driven by high-speed switching and consistent logic levels. Though replaced by CMOS alternatives in newer applications, TTL ICs are still used in legacy systems, test equipment, and certain industrial controls due to their robustness and simplicity. The segment continues to find value in educational tools and low-volume industrial applications where signal stability and speed are prioritized over consumption.

Rising Adoption in the Automotive Segment

The automotive segment generated robust revenues in 2024, driven by the rapid integration of electronics into vehicles for advanced driver assistance systems (ADAS), infotainment, electric powertrains, and battery management systems. Automakers are increasingly relying on logic ICs for real-time data processing, safety monitoring, and vehicle-to-everything (V2X) communications. As vehicles transition toward higher automation levels, the demand for high-reliability, low-latency logic components continues to rise.

Regional Insights

Asia Pacific to Emerge as a Lucrative Region

Asia Pacific logic IC market held a significant share in 2024, fueled by its strong manufacturing base, rising demand for consumer electronics, and growing investments in industrial automation. Countries like China, South Korea, Japan, and Taiwan are not only major consumers but are key producers of logic ICs, supported by mature semiconductor ecosystems and government-backed innovation policies.

Major players in the logic IC market are Lattice Semiconductor Corporation, STMicroelectronics N.V., GlobalFoundries Inc., Marvell Technology, Inc., Analog Devices, Inc., Qualcomm Incorporated, Infineon Technologies AG, Samsung Electronics Co., Ltd., Broadcom Inc., Xilinx, Inc. (AMD), Intel Corporation, ON Semiconductor Corporation, Semtech Corporation, Texas Instruments Incorporated, Renesas Electronics Corporation, Microchip Technology Inc., and NXP Semiconductors N.V.

To strengthen their presence in the logic IC market, companies are adopting a mix of technology leadership, supply chain agility, and application-focused innovation. Many are investing heavily in R&D to develop logic ICs using smaller process nodes and advanced packaging techniques to meet demands for speed, power efficiency, and integration. Strategic acquisitions and collaborations with foundries and fabless design firms are helping companies accelerate time-to-market and access new technologies.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Offering trends

- 2.2.2 Operating trends

- 2.2.3 Application trends

- 2.2.4 End use industry trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2025-2034 (USD Billion)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand from industrial automation and smart manufacturing

- 3.2.1.2 Advancements in 16-bit and BiCMOS logic IC technologies

- 3.2.1.3 Integration of logic ICs in automotive electronics and ADAS

- 3.2.1.4 Use of logic ICs in consumer electronics and edge computing devices

- 3.2.1.5 Expansion of logic IC deployment in telecommunications and data center infrastructure

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High implementation and upgrade costs

- 3.2.2.2 Competition from alternative processing and integration technologies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging business models

- 3.9 Compliance requirements

- 3.10 Consumer sentiment analysis

- 3.11 Patent and IP analysis

- 3.12 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 MEA

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital Transformation Initiatives

- 4.5 Emerging/ Startup Competitors Landscape

Chapter 5 Market Estimates & Forecast, By Type, 2021-2034 (USD Billion and Units)

- 5.1 Key trends

- 5.2 Standard Logic ICs

- 5.2.1 CMOS Logic ICs

- 5.2.2 TTL Logic ICs

- 5.2.3 BiCMOS Logic ICs

- 5.3 Programmable Logic Devices (PLDs)

- 5.3.1 Programmable Logic Arrays (PLAs)

- 5.3.2 Programmable Array Logic (PAL)

- 5.3.3 Complex Programmable Logic Devices (CPLDs)

- 5.3.4 Field Programmable Gate Arrays (FPGAs)

Chapter 6 Market Estimates & Forecast, By Technology, 2021-2034 (USD Billion and Units)

- 6.1 Key trends

- 6.2 CMOS Logic ICs

- 6.3 TTL Logic ICs

- 6.4 BiCMOS Logic ICs

Chapter 7 Market Estimates & Forecast, By End Use Industry, 2021-2034 (USD Billion and Units)

- 7.1 Key trends

- 7.2 Automotive

- 7.3 Consumer Electronics

- 7.4 Industrial

- 7.5 Healthcare

- 7.6 Aerospace & Defense

Chapter 8 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion and Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 PNY Technologies Inc.

- 9.2 Intel Corporation

- 9.3 Texas Instruments Incorporated

- 9.4 Broadcom Inc.

- 9.5 NXP Semiconductors N.V.

- 9.6 ON Semiconductor Corporation

- 9.7 STMicroelectronics N.V.

- 9.8 Microchip Technology Inc.

- 9.9 Analog Devices, Inc.

- 9.10 Infineon Technologies AG

- 9.11 Renesas Electronics Corporation

- 9.12 Xilinx, Inc. (AMD)

- 9.13 Lattice Semiconductor Corporation

- 9.14 Marvell Technology, Inc.

- 9.15 Qualcomm Incorporated

- 9.16 Semtech Corporation

- 9.17 GlobalFoundries Inc.

- 9.18 Samsung Electronics Co., Ltd.

全球逻辑积体电路市场:按类型、技术、应用、国家和地区划分-产业分析、市场规模、份额及未来预测(2025-2032年)

全球逻辑积体电路市场:按类型、技术、应用、国家和地区划分-产业分析、市场规模、份额及未来预测(2025-2032年) 全球逻辑积体电路市场规模、份额、产业分析报告:按类型、通用逻辑积体电路类型、按技术、按应用、按地区划分,展望与预测(2025-2032年)

全球逻辑积体电路市场规模、份额、产业分析报告:按类型、通用逻辑积体电路类型、按技术、按应用、按地区划分,展望与预测(2025-2032年) 标准逻辑积体电路的全球市场

标准逻辑积体电路的全球市场 2025-2029年全球标准逻辑IC市场

2025-2029年全球标准逻辑IC市场 逻辑 IC 市场规模、份额和趋势分析报告:按类型、技术、应用、地区和细分市场预测,2025 年至 2033 年

逻辑 IC 市场规模、份额和趋势分析报告:按类型、技术、应用、地区和细分市场预测,2025 年至 2033 年 逻辑IC(积体电路) -市场占有率分析、产业趋势与统计、成长预测(2025-2030)全球消费标准逻辑IC-市场占有率分析、产业趋势与统计、成长预测(2025-2030)标准逻辑 IC:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)消费性专用逻辑IC:市场占有率分析、产业趋势与统计、成长预测(2025-2030)用于电脑和周边设备的标准逻辑 IC -市场占有率分析、行业趋势和统计、成长预测 (2025-2030)

逻辑IC(积体电路) -市场占有率分析、产业趋势与统计、成长预测(2025-2030)全球消费标准逻辑IC-市场占有率分析、产业趋势与统计、成长预测(2025-2030)标准逻辑 IC:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)消费性专用逻辑IC:市场占有率分析、产业趋势与统计、成长预测(2025-2030)用于电脑和周边设备的标准逻辑 IC -市场占有率分析、行业趋势和统计、成长预测 (2025-2030)