|

市场调查报告书

商品编码

1871096

油气热交换器市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Oil and Gas Heat Exchanger Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

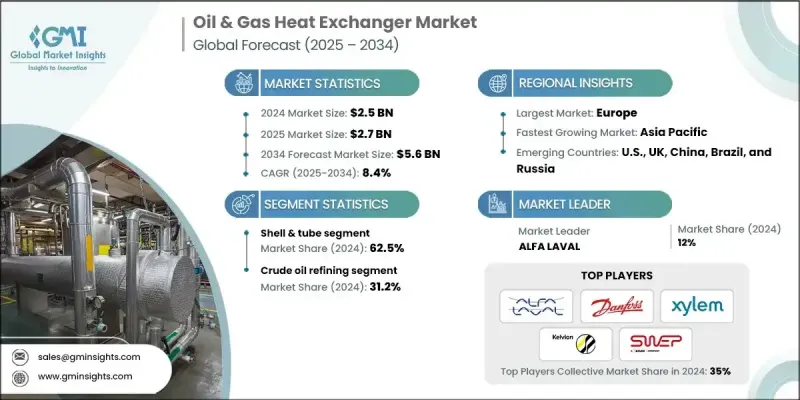

2024 年全球油气热交换器市场价值为 25 亿美元,预计到 2034 年将以 8.4% 的复合年增长率增长至 56 亿美元。

由于对油气基础设施的持续投资以及对高效供暖和製冷系统日益增长的需求,该行业的前景仍然强劲。热交换器在维持油气作业的热平衡方面发挥着至关重要的作用,它确保流体间有效的能量传递,从而提高生产效率并降低营运成本。炼油、加工和勘探活动中对节能热管理的日益重视,以及技术的进步,进一步刺激了市场扩张。专案专用、客製化热交换器的日益普及,确保了精确的温度控制和运作可靠性,也提高了市场渗透率。此外,适用于复杂或空间受限设施的紧凑型和适应性设计越来越受到青睐,这加速了产品的普及。向可持续且经济高效的热力技术转型,旨在提高能源效率和减少排放,正在重新定义产业趋势和竞争力。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 25亿美元 |

| 预测值 | 56亿美元 |

| 复合年增长率 | 8.4% |

2024年,管壳式热泵市占率达到62.5%,预计到2034年将以8%的复合年增长率成长。该细分市场持续成长,主要得益于其在原油炼製和天然气加工领域的广泛应用,这主要归功于其高耐久性以及在极端压力和温度条件下运作的能力。上游和下游基础设施投资的不断增加,以及对可靠高效热性能的持续需求,都推动了这一成长趋势。耐腐蚀材料的引入、用于增强传热的改进型管束结构,以及用于预测性维护和运行优化的先进监控系统的集成,都在提升产品需求和运营效率。

原油炼製应用领域在2024年占据31.2%的市场份额,预计到2034年将以7.5%的复合年增长率成长。全球炼油产能的提升,以及对优化工厂性能日益重视,是推动该领域成长的重要因素。日益严格的环境法规鼓励提高能源利用率和减少排放,进一步塑造了市场格局。数位技术、预测性维护工具以及旨在提高可靠性和延长设备寿命的高效热交换器的日益普及,也推动了这一领域的扩张。

2024年,美国油气热交换器市场占据78%的市场份额,市场规模达4.528亿美元。美国市场的成长得益于其强大的油气基础设施、页岩气开采技术的进步以及炼油和加工能力投资的不断增加。能源基础设施现代化建设的日益重视以及向符合永续发展目标的节能解决方案转型,是推动这一成长的主要因素。不断完善的环境标准和向净零排放目标的推进,进一步促进了先进热交换器系统在该地区得到广泛应用。

全球油气热交换器市场的主要企业包括ALFA LAVAL、API Heat Transfer、BARRIQUAND Heat Exchanger、Bronswerk、Danfoss、Funke Warmeaustauscher Apparatebau GmbH、HFM、HISAKA WORKS LTD.、HRS Heatrs、KAM Thermal Equipmenter、Kmbx、Hexson、Moler、M Group、SPX Flow、SWEP International、Thermofin、TITAN Metal Fabricators、Tranter、Turnbull & Scott Group和Xylem。油气热交换器市场的关键参与者正积极采取多种策略来提升其市场份额和竞争力。各公司致力于扩大全球生产能力并加强供应链,以满足不断增长的需求。策略合作和併购促进了技术共享和产品组合多元化。各公司正大力投资研发,以开发高性能、耐腐蚀且节能的热交换器,从而满足不断变化的产业需求。为提高运作可靠性并减少停机时间,公司正在优先考虑整合数位监控系统和预测性维护技术。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 原物料供应及采购分析

- 影响价值链的关键因素

- 中断

- 监管环境

- 产业影响因素

- 成长驱动因素

- 产业陷阱与挑战

- 成长潜力分析

- 波特的分析

- PESTEL 分析

- 油气热交换器的成本结构分析

- 新兴机会与趋势

- 利用物联网技术实现数位转型

- 新兴市场渗透

- 投资分析及未来展望

第四章:竞争格局

- 介绍

- 按地区分類的公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 中东和非洲

- 拉丁美洲

- 策略倡议

- 重要伙伴关係与合作

- 主要併购活动

- 产品创新与发布

- 市场扩张策略

- 竞争性标竿分析

- 战略仪錶板

- 创新与永续发展格局

第五章:市场规模及预测:依技术划分,2021-2034年

- 主要趋势

- 壳管

- 盘子

- 风冷

- 其他的

第六章:市场规模及预测:依应用领域划分,2021-2034年

- 主要趋势

- 陆上生产设施

- 原油炼製

- 石油化学加工

- 液化天然气设施

- 管道系统

- 其他的

第七章:市场规模及预测:依地区划分,2021-2034年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 俄罗斯

- 义大利

- 西班牙

- 波兰

- 亚太地区

- 中国

- 日本

- 韩国

- 印度

- 印尼

- 马来西亚

- 泰国

- 越南

- 菲律宾

- 澳洲

- 中东和非洲

- 沙乌地阿拉伯

- 阿联酋

- 埃及

- 南非

- 拉丁美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 智利

第八章:公司简介

- ALFA LAVAL

- API Heat Transfer

- BARRIQUAND Heat Exchanger

- Bronswerk

- Danfoss

- Funke Warmeaustauscher Apparatebau GmbH

- HFM

- HISAKA WORKS LTD.

- HRS Heat Exchangers

- KAM Thermal Equipment, LTD

- Kelvion Holding GmbH

- Mersen

- Metalforms, LLC

- Nexson Group

- SPX Flow

- SWEP International

- Thermofin

- TITAN Metal Fabricators

- Tranter

- Turnbull & Scott Group

- Xylem

The Global Oil & Gas Heat Exchanger Market was valued at USD 2.5 Billion in 2024 and is estimated to grow at a CAGR of 8.4% to reach USD 5.6 Billion by 2034.

The industry's outlook remains strong as continuous investments in oil and gas infrastructure and rising demand for efficient heating and cooling systems continue to drive growth. Heat exchangers play a vital role in maintaining thermal balance across oil and gas operations by ensuring effective energy transfer between fluid streams, which enhances productivity and reduces operational costs. The growing focus on energy-efficient thermal management across refining, processing, and exploration activities, coupled with technological advancements, is further stimulating market expansion. Increasing adoption of project-specific, customized heat exchangers that ensure precise temperature control and operational reliability is also enhancing market penetration. Moreover, the growing preference for compact and adaptable designs suitable for complex or space-constrained facilities is accelerating product adoption. The shift toward sustainable and cost-effective thermal technologies aimed at improving energy performance and reducing emissions is redefining industry trends and competitiveness.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.5 Billion |

| Forecast Value | $5.6 Billion |

| CAGR | 8.4% |

The shell and tube segment held a 62.5% share in 2024 and is forecasted to grow at a CAGR of 8% through 2034. This segment continues to gain traction due to its robust use in both crude oil refining and gas processing applications, primarily driven by its high durability and ability to operate under extreme pressure and temperature conditions. Expanding investments in upstream and downstream infrastructure and the continuous need for reliable and efficient thermal performance are supporting this growth trajectory. The introduction of corrosion-resistant materials, improved tube configurations for enhanced heat transfer, and the integration of advanced monitoring systems designed for predictive maintenance and operational optimization are boosting product demand and efficiency across operations.

The crude oil refining application segment held a 31.2% share in 2024 and is expected to grow at a CAGR of 7.5% through 2034. Rising refining capacities worldwide, coupled with an increasing emphasis on optimizing plant performance, are contributing significantly to the segment's growth. Stricter environmental norms encouraging better energy utilization and reduced emissions are further shaping the market landscape. The growing integration of digital technologies, predictive maintenance tools, and high-efficiency heat exchangers designed to improve reliability and extend equipment life is fueling this expansion.

United States Oil & Gas Heat Exchanger Market held a 78% share in 2024, generating USD 452.8 million. The U.S. market is expanding due to the country's strong oil and gas infrastructure, advancements in shale extraction, and rising investments in refining and processing capacities. Increasing focus on modernizing energy infrastructure and the transition toward energy-efficient solutions in alignment with sustainability goals are major drivers behind this growth. Evolving environmental standards and the push toward net-zero objectives are further supporting widespread adoption of advanced heat exchanger systems across the region.

Leading companies operating in the Global Oil & Gas Heat Exchanger Market include ALFA LAVAL, API Heat Transfer, BARRIQUAND Heat Exchanger, Bronswerk, Danfoss, Funke Warmeaustauscher Apparatebau GmbH, HFM, HISAKA WORKS LTD., HRS Heat Exchangers, KAM Thermal Equipment LTD, Kelvion Holding GmbH, Mersen, Metalforms LLC, Nexson Group, SPX Flow, SWEP International, Thermofin, TITAN Metal Fabricators, Tranter, Turnbull & Scott Group, and Xylem. Key players in the Oil & Gas Heat Exchanger Market are actively adopting several strategies to enhance their market presence and competitiveness. Companies are focusing on expanding their global production capabilities and strengthening their supply chains to meet increasing demand. Strategic collaborations and mergers are enabling technology sharing and portfolio diversification. Firms are heavily investing in R&D to develop high-performance, corrosion-resistant, and energy-efficient heat exchangers tailored to evolving industry requirements. Integration of digital monitoring systems and predictive maintenance technologies is being prioritized to enhance operational reliability and reduce downtime.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

- 2.2 Business trends

- 2.3 Technology trends

- 2.4 Application trends

- 2.5 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Key factors affecting the value chain

- 3.1.3 Disruptions

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 Cost structure analysis of oil & gas heat exchangers

- 3.8 Emerging opportunities & trends

- 3.8.1 Digital transformation with IoT technologies

- 3.8.2 Emerging market penetration

- 3.9 Investment analysis & future outlook

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2024

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic initiatives

- 4.3.1 Key partnerships & collaborations

- 4.3.2 Major M&A activities

- 4.3.3 Product innovations & launches

- 4.3.4 Market expansion strategies

- 4.4 Competitive benchmarking

- 4.5 Strategic dashboard

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Technology, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 Shell & tube

- 5.3 Plate

- 5.4 Air cooled

- 5.5 Others

Chapter 6 Market Size and Forecast, By Application, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Onshore production facilities

- 6.3 Crude oil refining

- 6.4 Petrochemical processing

- 6.5 LNG facilities

- 6.6 Pipeline systems

- 6.7 Others

Chapter 7 Market Size and Forecast, By Region, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Russia

- 7.3.5 Italy

- 7.3.6 Spain

- 7.3.7 Poland

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 South Korea

- 7.4.4 India

- 7.4.5 Indonesia

- 7.4.6 Malaysia

- 7.4.7 Thailand

- 7.4.8 Vietnam

- 7.4.9 Philippines

- 7.4.10 Australia

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 Egypt

- 7.5.4 South Africa

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

- 7.6.3 Colombia

- 7.6.4 Chile

Chapter 8 Company Profiles

- 8.1 ALFA LAVAL

- 8.2 API Heat Transfer

- 8.3 BARRIQUAND Heat Exchanger

- 8.4 Bronswerk

- 8.5 Danfoss

- 8.6 Funke Warmeaustauscher Apparatebau GmbH

- 8.7 HFM

- 8.8 HISAKA WORKS LTD.

- 8.9 HRS Heat Exchangers

- 8.10 KAM Thermal Equipment, LTD

- 8.11 Kelvion Holding GmbH

- 8.12 Mersen

- 8.13 Metalforms, LLC

- 8.14 Nexson Group

- 8.15 SPX Flow

- 8.16 SWEP International

- 8.17 Thermofin

- 8.18 TITAN Metal Fabricators

- 8.19 Tranter

- 8.20 Turnbull & Scott Group

- 8.21 Xylem

动力传动系统热交换器市场规模、份额和成长分析:按热交换器类型、应用、材质、设计类型和地区划分-产业预测(2026-2033 年)

动力传动系统热交换器市场规模、份额和成长分析:按热交换器类型、应用、材质、设计类型和地区划分-产业预测(2026-2033 年) 汽车热交换器全球市场规模、份额、趋势和成长分析报告(2026-2034)

汽车热交换器全球市场规模、份额、趋势和成长分析报告(2026-2034) 汽车热交换器市场 - 全球产业规模、份额、趋势、机会及预测(按应用、设计类型、车辆类型、动力系统、地区和竞争格局划分,2021-2031年)

汽车热交换器市场 - 全球产业规模、份额、趋势、机会及预测(按应用、设计类型、车辆类型、动力系统、地区和竞争格局划分,2021-2031年) 汽车热交换器:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)

汽车热交换器:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年) 全球汽车热交换器市场(按推进系统和零件、设计、车辆类型、电动车类型、非公路用车辆类型、地区划分)- 预测至 2032 年

全球汽车热交换器市场(按推进系统和零件、设计、车辆类型、电动车类型、非公路用车辆类型、地区划分)- 预测至 2032 年 汽车热交换器市场分析及预测(至2034年):类型、产品、技术、组件、应用、材料类型、最终用户、功能、安装类型、设备

汽车热交换器市场分析及预测(至2034年):类型、产品、技术、组件、应用、材料类型、最终用户、功能、安装类型、设备 汽车热交换器市场规模、份额和成长分析(按设计类型、车辆类型、电动车、应用和地区)- 2025-2032 年产业预测

汽车热交换器市场规模、份额和成长分析(按设计类型、车辆类型、电动车、应用和地区)- 2025-2032 年产业预测 汽车热交换器市场机会、成长动力、产业趋势分析及 2025-2034 年预测汽车热交换器市场(按设计类型、车辆类型、电动车、非公路车辆类型、应用和地区划分)2024 年至 2031 年

汽车热交换器市场机会、成长动力、产业趋势分析及 2025-2034 年预测汽车热交换器市场(按设计类型、车辆类型、电动车、非公路车辆类型、应用和地区划分)2024 年至 2031 年 2024-2028年全球汽车热交换器市场

2024-2028年全球汽车热交换器市场