|

市场调查报告书

商品编码

1844558

汽车热交换器:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)Automotive Heat Exchanger - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

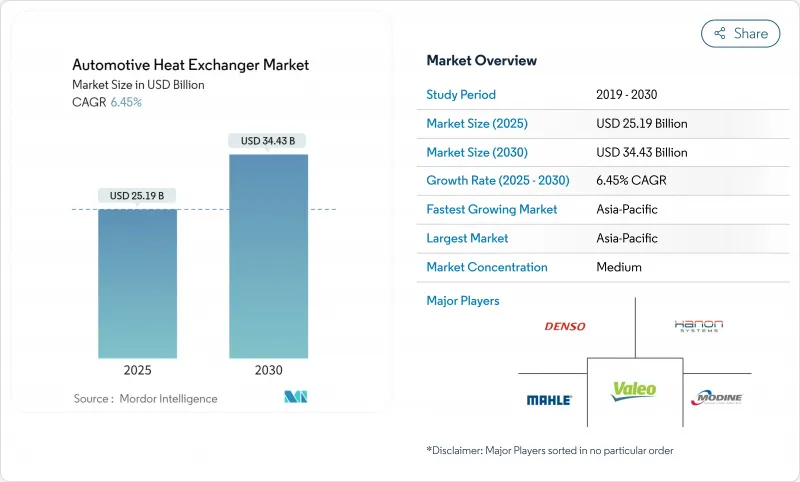

预计2025年汽车热交换器市场规模将达251.9亿美元,2030年将扩大至344.3亿美元,复合年增长率为6.45%。

从内燃机冷却迴路到电池、电力电子和座舱气候控制的多迴路架构的转变,正在推动汽车热交换器市场的扩张。电气化平台需要能够防止电池热失控、管理800V充电负载并延长车辆续航里程的组件。亚太地区电动车的普及、欧7耐久性法规以及热泵整合也提升了汽车热交换器市场的产品复杂性和价值。供应商正在透过微通道设计、耐腐蚀合金和热泵整合模组来应对这项挑战,而铝和铜等材料的波动性则持续对整个汽车热交换器市场的利润率造成压力。

全球汽车热交换器市场趋势与洞察

电动车销售推动先进温度控管需求

电动车所需的铝材比内燃机汽车多出约30%,这迫使散热器以外的热交换器必须重新设计。电池迴路必须将电池温度保持在2°C以内,以避免失控,而碳化硅逆变器会造成局部热峰值,这些峰值由微通道芯体处理。低电导率流体(例如Preston符合GB29743-2标准的冷却液形状和涂层选项)以及直接浸入式冷却技术,为消除电导率风险的介电单元开闢了新的市场。

严格的全球排放法规

将于2024年5月公布的欧7法规将统一废气排放法规,并增加煞车和轮胎颗粒物限值,间接增加了热负荷,同时迫使汽车製造商追求更高的能源效率。该法规将要求电池的耐用性,要求交换器寿命超过10年,并推动使用防腐焊焊板,而机载诊断将实现预测性流量控制。该计画将持续到2026年11月,将缩短检验窗口,并有利于拥有预认证测试台架的供应商。

铝和铜的价格波动

电动车型的铜用量高达80公斤,是内燃机车的四倍。汽车製造商透过多年期封闭式和闭环回收进行对冲,但地区溢价仍然扭曲了筹资策略。合金创新提高了单位重量的导电性,有助于限制对原金属的需求,并在外汇飙升时稳定成本。

細項分析

散热器将成为汽车热交换器市场最大的细分市场,到2024年将占销售额的39.29%。到2030年,电池和电力电子冷却器的复合年增长率将达到13.20%,市场份额将下降,这反映了电气化的优先性。锂离子电池组需要+-2°C的热稳定性才能快速充电,这推动了汽车热交换器市场对整合冷却板和介电浸没模组的需求。增压空气系统正与涡轮增压保持同步发展,而油冷却器将重点转向电桥润滑。座舱蒸发器和冷凝器正在演变为可逆热泵热交换器,而氢燃料电池加湿器正在成为一个新兴的利基市场。

汽车热交换器市场仍专注于散热器容量。然而,燃料电池客车和卡车的堆迭式加湿模组市场仍有閒置频段,而埃贝赫的排气装置则将水回收与声音阻尼相结合。混合废热回收对于符合欧盟7标准的动力传动系统仍然至关重要,随着纯电池应用的增加,它为供应商提供了过渡产品。

由于模具成熟且成本低廉,管翅芯式热交换器到2024年将占据汽车热交换器市场份额的47.28%。由于原始设备製造商为了在滑板底盘中实现碰撞封装而牺牲了厚度,板条组件的复合年增长率将达到8.84%。微通道和扁管单元是汽车热交换器市场中成长最快的部分。热管和均热板正在高阶电池组中得到应用,随着固体电池降低热负荷并提高对温度均匀性的要求,这一趋势可能会呈现级联式增长。

在高压迴路中,管壳式热交换器已站稳脚跟,主要用于氢燃料电池和废热回收系统,而板棒式设计采用内部偏置翅片来降低流速和噪音,正在加强其在商用车增压空气冷却中的地位。

区域分析

预计到2024年,亚太地区将占据汽车热交换器市场的47.23%,复合年增长率为8.78%。预计到2025年,中国汽车产量将超过3,500万辆,电动车销量年均成长50%,这将有利于能够大规模生产微通道管的垂直整合铝挤型机。日本的燃料电池蓝图和韩国在辐射供暖方面的进步将进一步丰富汽车热交换器市场的技术需求。

北美市场发出的信号喜忧参半:电动车零售需求疲软导致福特削减了F-150 Lightning的产量,而抗击通膨的立法则推动了供应链的区域化。 Gentherm公布2025年第一季销售额为3.54亿美元,新订单累计4亿美元。国内挤压和硬焊投资或能为抵御外部材料衝击提供缓衝。

欧洲的份额将取决于2026年11月欧7标准的合规期限。汽车製造商正在利用76%的回收率,并增加再生铝的使用。安森美半导体在捷克共和国投资20亿美元的碳化硅工厂,由于更高的键结温度,将推动当地散热器需求。此外,国家预算正瞄准氢能卡车市场,使燃料电池加湿器在汽车热交换器市场中保持领先。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场状况

- 市场概况

- 市场驱动因素

- 电动车销售推动先进温度控管需求

- 严格的全球排放法规

- 新兴市场暖通空调渗透率不断上升

- 电动汽车热泵系统的集成

- 800V高压XEV架构

- 燃料电池加湿器的使用

- 市场限制

- 铝和铜的价格波动

- 严格的耐久性和腐蚀检验成本

- 降低固态电池组的热负荷

- 微通道挤压进料瓶颈

- 价值/供应链分析

- 监管状况

- 技术展望

- 五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章市场规模及成长预测

- 按用途

- 散热器

- 增压空气冷却器/中冷器

- 油冷却器

- EGR及废气热回收设备

- 座舱 HVAC(蒸发器和冷凝器)

- 电池/电力电子冷却器

- 燃料电池加湿器

- 其他用途

- 依设计类型

- 管翅式

- 板材棒材

- 微通道扁管

- 壳管式

- 其他的

- 按材质

- 铝

- 铜/黄铜

- 防锈的

- 复合材料和聚合物

- 按车辆类型

- 搭乘用车

- 轻型商用车

- 重型商用车和非公路用车

- 按动力传动系统

- 内燃机(ICE)

- 混合动力电动车(HEV/PHEV)

- 纯电动车(BEV)

- 燃料电池电动车(FCEV)

- 按地区

- 北美洲

- 美国

- 加拿大

- 北美其他地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 俄罗斯

- 其他欧洲国家

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 其他亚太地区

- 中东和非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 土耳其

- 南非

- 其他中东和非洲地区

- 北美洲

第六章 竞争态势

- 市场集中度

- 策略倡议

- 市占率分析

- 公司简介

- DENSO Corporation

- MAHLE GmbH

- Valeo SA

- Hanon Systems

- Modine Manufacturing Company

- Dana Incorporated

- Marelli(Calsonic Kansei)

- Sanden Holdings

- GEA Group

- Kelvion Holdings

- T.RAD Co. Ltd.

- Behr Hella Service

- AKG Thermal Systems

- American Industrial Heat Transfer

- Banco Products(India)Ltd.

- Climetal SL

- Constellium SE

- GandM Radiator

- Nippon Light Metal Holdings

- Valeo SA(Thermal Systems)

第七章 市场机会与未来展望

The automotive heat exchanger market reached USD 25.19 billion in 2025 and is projected to rise to USD 34.43 billion by 2030, advancing at a 6.45% CAGR.

The shift from internal-combustion cooling loops to multi-loop architectures for battery, power electronics, and cabin climate control underpins this expansion across the automotive heat exchanger market. Electrified platforms demand components that prevent battery thermal runaway, manage 800-V charging loads, and conserve vehicle range. Strong electric-vehicle adoption in Asia-Pacific, Euro 7 durability rules, and heat-pump integration also elevate product complexity and value content in the automotive heat exchanger market. Suppliers are responding with micro-channel designs, corrosion-resistant alloys, and integrated heat-pump modules, while materials volatility in aluminum and copper continues to pressure margins across the automotive heat exchanger market.

Global Automotive Heat Exchanger Market Trends and Insights

EV Sales-Driven Demand for Advanced Thermal Management

Electric vehicles require roughly 30% more aluminum than combustion cars, forcing the redesign of exchangers beyond radiator duty. Battery loops must keep cell temperatures within a 2 °C band to avoid runaway, while silicon-carbide inverters impose localized heat spikes handled by micro-channel cores. Low-conductivity fluids, such as Prestone's GB29743-2-compliant coolant shape alloy and coating choices, and direct-immersion cooling, open a niche for dielectric units that eliminate conductivity risk.

Stringent Global Emission Regulations

Euro 7 rules published in May 2024 unify tailpipe limits and add brake- and tire-particulate caps, indirectly raising thermal loads as automakers chase efficiency gains. Required battery durability pushes exchanger life targets beyond a decade, spurring corrosion-proof brazing sheets while onboard diagnostics enable predictive flow control. Program timelines to November 2026 tighten validation windows, favoring suppliers with pre-certified test benches.

Aluminum and Copper Price Volatility

Electric models can contain up to 80 kg copper-four times that of combustion cars-making exchanger cost highly sensitive to spot prices. Automakers hedge with multiyear contracts and closed-loop recycling, yet regional premiums still skew sourcing strategies. Alloy innovation that lifts conductivity per unit weight helps limit primary metal demand, stabilizing costs when exchange rates spike.

Other drivers and restraints analyzed in the detailed report include:

- Heat-pump System Integration in Electric Vehicles

- Rising HVAC Penetration in Emerging Markets

- Micro-channel Extrusion Supply Bottlenecks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Radiators accounted for the largest slice of the automotive heat exchanger market size, holding 39.29% revenue in 2024. Their share slips as battery and power-electronics coolers record a 13.20% CAGR to 2030, reflecting electrification priorities. Lithium-ion packs demand +-2 °C thermal stability for fast charging, prompting integrated chill plates and dielectric immersion modules in the automotive heat exchanger market. Charge-air systems keep pace with turbocharging, while oil coolers pivot toward e-axle lubrication. Cabin evaporators and condensers evolve into reversible heat-pump exchangers, and hydrogen fuel-cell humidifiers surface as a nascent niche.

The automotive heat exchanger market continues to prize radiator volumes. Yet, white-space lies in stack humidification modules for fuel-cell buses and trucks, where Eberspacher's exhaust-air unit blends water recovery with acoustic damping. Hybrid exhaust-heat recovery remains relevant in Euro-7-compliant powertrains, giving suppliers a bridge product as pure battery adoption climbs.

Tube-fin cores represented 47.28% of automotive heat exchanger market share in 2024 owing to mature tooling and low cost. Plate-bar assemblies grow 8.84% CAGR as OEMs trade off thickness for crash packaging in skateboard chassis. The automotive heat exchanger market size for micro-channel flat tube units is scaling fastest because superior transfer coefficients enable slim modules around crowded battery trays. Heat pipes and vapor chambers appear in premium battery packs, a trend likely to cascade as solid-state cells lower heat loads but tighten temperature uniformity needs.

In high-pressure loops, shell-and-tube exchangers preserve a foothold, mainly in hydrogen fuel-cell and waste-heat recovery systems where robustness outweighs weight penalties. Concurrently, plate-bar variants adopt internal offset fins to temper flow velocity and noise, reinforcing their position in commercial-vehicle charge-air cooling.

The Automotive Heat Exchanger Market Report is Segmented by Application (Radiator, Charge-Air Coolers / Intercoolers, and More), Design Type (Tube-Fin, Plate-Bar, and More), Material (Aluminum, Copper / Brass, and More) Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Powertrain Type (Internal Combustion Engine Vehicles, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific dominated the automotive heat exchanger market with 47.23% share in 2024 and is forecast to expand 8.78% CAGR. China exceeded 35 million vehicle builds in 2025, with EV sales up 50% yearly, benefiting vertically integrated aluminum extruders that produce micro-channel tubes at scale. Japan's fuel-cell roadmap and South Korea's radiant heating breakthroughs further diversify technical demand across the automotive heat exchanger market.

North America confronts mixed signals: softer retail EV demand led Ford to trim F-150 Lightning volumes, yet the Inflation Reduction Act spurs localized supply chains. Gentherm booked USD 400 million in new awards while achieving USD 354 million Q1 2025 revenue, reflecting resilience in climate-comfort niches. Domestic extrusion and brazing investment could cushion against foreign material shocks.

Europe's share is shaped by Euro 7's November 2026 compliance deadline. Automakers are boosting recycled aluminum use, leveraging a 76% collection rate. Onsemi's USD 2 billion SiC facility in Czechia elevates regional heat-sink demand owing to higher junction temperatures. National funding also targets hydrogen truck corridors, keeping fuel-cell humidifier lines viable within the automotive heat exchanger market

- DENSO Corporation

- MAHLE GmbH

- Valeo SA

- Hanon Systems

- Modine Manufacturing Company

- Dana Incorporated

- Marelli (Calsonic Kansei)

- Sanden Holdings

- GEA Group

- Kelvion Holdings

- T.RAD Co. Ltd.

- Behr Hella Service

- AKG Thermal Systems

- American Industrial Heat Transfer

- Banco Products (India) Ltd.

- Climetal SL

- Constellium SE

- GandM Radiator

- Nippon Light Metal Holdings

- Valeo SA (Thermal Systems)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EV Sales-Driven Demand For Advanced Thermal Management

- 4.2.2 Stringent Global Emission Regulations

- 4.2.3 Rising HVAC Penetration In Emerging Markets

- 4.2.4 Heat-Pump System Integration In Electric Vehicles

- 4.2.5 800-V High-Voltage XEV Architectures

- 4.2.6 Fuel-Cell Humidifier Exchanger Adoption

- 4.3 Market Restraints

- 4.3.1 Aluminum and Copper Price Volatility

- 4.3.2 Stringent Durability and Corrosion Validation Costs

- 4.3.3 Declining Heat-Load In Solid-State Battery Packs

- 4.3.4 Micro-Channel Extrusion Supply Bottlenecks

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value (USD))

- 5.1 By Application

- 5.1.1 Radiators

- 5.1.2 Charge-Air Coolers / Intercoolers

- 5.1.3 Oil Coolers

- 5.1.4 EGR and Exhaust Gas Heat Recovery

- 5.1.5 Cabin HVAC (Evaporator and Condenser)

- 5.1.6 Battery / Power-electronics Coolers

- 5.1.7 Fuel-cell Humidifiers

- 5.1.8 Other Applications

- 5.2 By Design Type

- 5.2.1 Tube-Fin

- 5.2.2 Plate-Bar

- 5.2.3 Micro-channel Flat Tube

- 5.2.4 Shell-and-Tube

- 5.2.5 Others

- 5.3 By Material

- 5.3.1 Aluminum

- 5.3.2 Copper / Brass

- 5.3.3 Stainless Steel

- 5.3.4 Composites and Polymers

- 5.4 By Vehicle Type

- 5.4.1 Passenger Cars

- 5.4.2 Light Commercial Vehicles

- 5.4.3 Heavy Commercial and Off-Highway Vehicles

- 5.5 By Powertrain Type

- 5.5.1 Internal Combustion Engine (ICE)

- 5.5.2 Hybrid Electric Vehicles (HEV/PHEV)

- 5.5.3 Battery Electric Vehicles (BEV)

- 5.5.4 Fuel-Cell Electric Vehicles (FCEV)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Russia

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 Turkey

- 5.6.5.4 South Africa

- 5.6.5.5 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 DENSO Corporation

- 6.4.2 MAHLE GmbH

- 6.4.3 Valeo SA

- 6.4.4 Hanon Systems

- 6.4.5 Modine Manufacturing Company

- 6.4.6 Dana Incorporated

- 6.4.7 Marelli (Calsonic Kansei)

- 6.4.8 Sanden Holdings

- 6.4.9 GEA Group

- 6.4.10 Kelvion Holdings

- 6.4.11 T.RAD Co. Ltd.

- 6.4.12 Behr Hella Service

- 6.4.13 AKG Thermal Systems

- 6.4.14 American Industrial Heat Transfer

- 6.4.15 Banco Products (India) Ltd.

- 6.4.16 Climetal SL

- 6.4.17 Constellium SE

- 6.4.18 GandM Radiator

- 6.4.19 Nippon Light Metal Holdings

- 6.4.20 Valeo SA (Thermal Systems)

7 Market Opportunities and Future Outlook

动力传动系统热交换器市场规模、份额和成长分析:按热交换器类型、应用、材质、设计类型和地区划分-产业预测(2026-2033 年)

动力传动系统热交换器市场规模、份额和成长分析:按热交换器类型、应用、材质、设计类型和地区划分-产业预测(2026-2033 年) 汽车热交换器全球市场规模、份额、趋势和成长分析报告(2026-2034)

汽车热交换器全球市场规模、份额、趋势和成长分析报告(2026-2034) 汽车热交换器市场 - 全球产业规模、份额、趋势、机会及预测(按应用、设计类型、车辆类型、动力系统、地区和竞争格局划分,2021-2031年)

汽车热交换器市场 - 全球产业规模、份额、趋势、机会及预测(按应用、设计类型、车辆类型、动力系统、地区和竞争格局划分,2021-2031年) 油气热交换器市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)

油气热交换器市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年) 全球汽车热交换器市场(按推进系统和零件、设计、车辆类型、电动车类型、非公路用车辆类型、地区划分)- 预测至 2032 年

全球汽车热交换器市场(按推进系统和零件、设计、车辆类型、电动车类型、非公路用车辆类型、地区划分)- 预测至 2032 年 汽车热交换器市场分析及预测(至2034年):类型、产品、技术、组件、应用、材料类型、最终用户、功能、安装类型、设备

汽车热交换器市场分析及预测(至2034年):类型、产品、技术、组件、应用、材料类型、最终用户、功能、安装类型、设备 汽车热交换器市场规模、份额和成长分析(按设计类型、车辆类型、电动车、应用和地区)- 2025-2032 年产业预测汽车热交换器市场机会、成长动力、产业趋势分析及 2025-2034 年预测汽车热交换器市场(按设计类型、车辆类型、电动车、非公路车辆类型、应用和地区划分)2024 年至 2031 年

汽车热交换器市场规模、份额和成长分析(按设计类型、车辆类型、电动车、应用和地区)- 2025-2032 年产业预测汽车热交换器市场机会、成长动力、产业趋势分析及 2025-2034 年预测汽车热交换器市场(按设计类型、车辆类型、电动车、非公路车辆类型、应用和地区划分)2024 年至 2031 年 2024-2028年全球汽车热交换器市场

2024-2028年全球汽车热交换器市场