|

市场调查报告书

商品编码

1871100

先进光刻技术用光阻化学品市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Photoresist Chemicals for Advanced Lithography Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

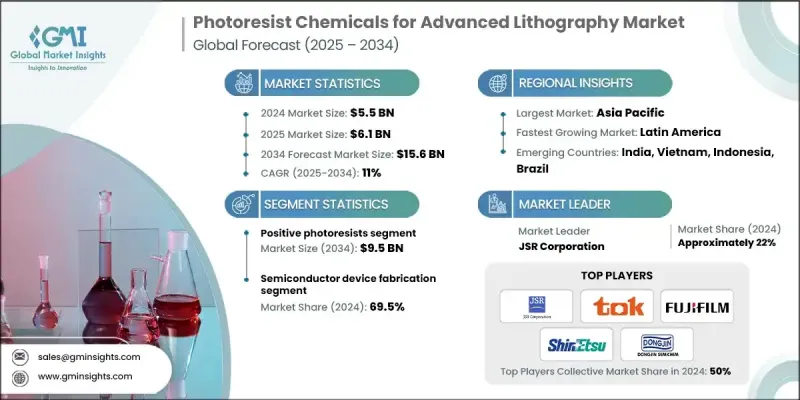

2024 年全球先进光阻化学品市场价值为 55 亿美元,预计到 2034 年将以 11% 的复合年增长率增长至 156 亿美元。

亚太地区投资的成长、高数值孔径极紫外线(High-NA EUV)系统的商业化以及3D封装技术的进步正在推动市场发展。 7奈米和5奈米以下製程节点的采用、极紫外光刻技术的日益普及以及人工智慧、5G和汽车应用领域对高性能晶片不断增长的需求,都在推动着这项变革。波长为13.5奈米的极紫外线(EUV)光刻技术能够实现5奈米线宽的图案化,显着提升了对化学放大光阻(CAR)和金属氧化物基极紫外光阻的需求。向高数值孔径极紫外光刻、结合深紫外线(DUV)和极紫外光(EUV)的混合微影以及定向自组装(DSA)技术的演进,正在重塑光阻的化学系统。像 JSR、TOK、东进半导体和富士胶片这样的行业领导者正在调整产品路线图,以适应 2nm 和 1.4nm 节点的准备情况,这标誌着从传统的 KrF/i 线光阻向 EUV 平台的明显转变。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 55亿美元 |

| 预测值 | 156亿美元 |

| 复合年增长率 | 11% |

2024年,正性光阻市场规模达34亿美元,预计2034年将达95亿美元,年复合成长率达10.7%。化学放大光阻在该领域占据主导地位,其对10奈米以下尺寸的装置具有高灵敏度,并能实现精确的製程控制。该领域的创新主要集中在提高抗蚀刻性、开发模组化光阻方案以及最大限度地减少极紫外光刻中的二次电子模糊,所有这些对于在小尺寸下最大限度地提高良率都至关重要。

由于半导体装置製造领域对用于先进逻辑、记忆体、类比和人工智慧晶片的高纯度、高效能光阻的需求,预计到2024年,该领域将占据69.5%的市场份额。多重曝光复杂性的增加和高数值孔径极紫外光刻(High-NA EUV)技术的普及,使得采用5nm、3nm以及即将推出的2nm製程节点生产的逻辑元件(包括CPU、GPU和SoC)成为光阻材料的最大消耗者。

2024年,美国先进光阻化学品市场规模为8.174亿美元,预计将以10.8%的复合年增长率成长,到2034年达到23亿美元。北美市场的成长主要得益于半导体产业振兴政策,包括鼓励国内晶片生产的立法。随着主要製造商新建製造工厂,这些政策正在推动对本地采购的光阻和先进光刻材料的需求。

先进光刻胶化学品市场的主要参与者包括默克集团(Merck KGaA)、布鲁尔科学公司(Brewer Science, Inc.)、陶氏化学(Dow)、富士胶卷控股株式会社(Fujifilm Holdings Corporation)、Inpria Corporation、东进半导体株式会(Dongjtern Schemy. Ltd.)、信越化学株式会社(Shin-Etsu Chemical Co., Ltd.)、JSR株式会社(JSR Corporation)、化药先进材料株式会社(Kayaku Advanced Materials)、东京樱工业株式会社(Tokyo Ohka Kogyo Co., Ltd.)、Micro Chemist Technology GmbH、起友化学公司(Sucroed Resist Technology Gmbical) Company)、江苏那塔光电材料有限公司(Jiangsu Nata Opto-electronic Material Co., Ltd.)及Irresistible Materials Ltd.。领先企业正大力投资研发,以开发适用于高数值孔径极紫外光刻(High-NA EUV)和5奈米以下製程节点的新一代光阻化学品。与半导体製造商的策略合作有助于将产品创新与商业光刻需求相匹配。各公司正在扩大亚太和北美地区的产能,以满足不断增长的区域需求。一些企业专注于混合光刻解决方案和定向自组装技术,以拓宽产品的应用范围。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 利润率

- 每个阶段的价值增加

- 影响价值链的因素

- 中断

- 产业影响因素

- 成长驱动因素

- 产业陷阱与挑战

- 市场机会

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL 分析

- 价格趋势

- 按地区

- 按类型

- 未来市场趋势

- 技术与创新格局

- 当前技术趋势

- 新兴技术

- 专利格局

- 贸易统计(註:仅提供重点国家的贸易统计)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估算与预测:依类型划分,2021-2034年

- 主要趋势

- 正性光阻

- 丙烯酸酯类光阻

- 基于酚醛树脂(dnq)的系统

- 聚甲基丙烯酸甲酯(PMMA)

- 负性光阻

- 环氧树脂基

- 含硅光刻胶

- 金属基光阻

第六章:市场估算与预测:依光刻技术划分,2021-2034年

- 主要趋势

- 杜夫光刻

- 248nm krf光刻

- 193nm干法光刻

- 193nm浸没式微影(arfi)

- 极紫外线(EUV)光刻

- 紫外光@13.5 nm

- 高纳 euv

- I线光刻(365奈米)

- 奈米压印光刻(无)

- 电子束光刻

第七章:市场估算与预测:依最终用途划分,2021-2034年

- 主要趋势

- 半导体装置製造

- 逻辑元件

- 储存装置

- 边缘设备

- 影像感测器

- MEMS元件

- 汽车记忆体

- 消费性电子记忆体

- 工业和医疗保健存储器

- 显示电子应用

- LCD製造

- OLED显示器生产

- 下一代显示器

- 先进封装应用

- 3D包装

- 系统级封装(SIP)

- 晶圆级封装(WLP)

- 光掩模製造

- EUV掩模

- DUV 掩模

第八章:市场估算与预测:依地区划分,2021-2034年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

- 中东和非洲其他地区

第九章:公司简介

- Brewer Science, Inc.

- Dongjin Semichem Co., Ltd.

- Dow

- Eternal Materials Co., Ltd.

- Fujifilm Holdings Corporation

- Inpria Corporation

- Irresistible Materials Ltd.

- Jiangsu Nata Opto-electronic Material Co., Ltd.

- JSR Corporation

- Kayaku Advanced Materials

- Merck KGaA

- Micro Resist Technology GmbH

- Shin-Etsu Chemical Co., Ltd.

- Sumitomo Chemical Company

- Tokyo Ohka Kogyo Co., Ltd.

- Others

The Global Photoresist Chemicals for Advanced Lithography Market was valued at USD 5.5 Billion in 2024 and is estimated to grow at a CAGR of 11% to reach USD 15.6 Billion by 2034.

The market is being propelled by rising investments in the Asia-Pacific region, the commercialization of High-NA EUV systems, and advancements in 3D packaging technologies. The adoption of sub-7nm and sub-5nm process nodes, growing use of EUV lithography, and increasing demand for high-performance chips in AI, 5G, and automotive applications are driving this transformation. Extreme Ultraviolet (EUV) lithography at 13.5 nm wavelengths is enabling the patterning of 5nm line widths, significantly boosting demand for chemically amplified resists (CARs) and metal-oxide-based EUV photoresists. The evolution toward High-NA EUV, hybrid lithography combining DUV and EUV, and directed self-assembly (DSA) is reshaping resist chemistries. Industry leaders like JSR, TOK, Dongjin Semichem, and Fujifilm are aligning product roadmaps with 2nm and 1.4nm node readiness, marking a clear shift from traditional KrF/i-line resists to EUV-focused platforms.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.5 Billion |

| Forecast Value | $15.6 Billion |

| CAGR | 11% |

The positive photoresists segment generated USD 3.4 Billion in 2024 and is expected to reach USD 9.5 Billion by 2034, growing at a CAGR of 10.7%. Chemically amplified resists dominate this segment, offering high sensitivity for sub-10nm geometries and enabling precise process control. Innovations in this space focus on improving etch resistance, developing modular photoresist options, and minimizing secondary electron blur in EUV lithography, all critical to maximizing yields at small dimensions.

The semiconductor device fabrication segment held a 69.5% share in 2024 owing to its need for high-purity, high-performance photoresists used in advanced logic, memory, analog, and AI-focused chips. Increasing multi-patterning complexity and High-NA EUV adoption make logic devices, including CPUs, GPUs, and SoCs produced at 5nm, 3nm, and soon 2nm nodes, the largest consumers of photoresist materials.

U.S. Photoresist Chemicals for Advanced Lithography Market generated USD 817.4 million in 2024 and is expected to grow at a CAGR of 10.8% to reach USD 2.3 Billion by 2034. North America's growth is being fueled by semiconductor revitalization policies, including legislation encouraging domestic chip production. These policies are driving the demand for locally sourced photoresist and advanced lithography materials as new fabrication facilities are established by major manufacturers.

Key players in the Photoresist Chemicals for Advanced Lithography Market include Merck KGaA, Brewer Science, Inc., Dow, Fujifilm Holdings Corporation, Inpria Corporation, Dongjin Semichem Co., Ltd., Eternal Materials Co., Ltd., Shin-Etsu Chemical Co., Ltd., JSR Corporation, Kayaku Advanced Materials, Tokyo Ohka Kogyo Co., Ltd., Micro Resist Technology GmbH, Sumitomo Chemical Company, Jiangsu Nata Opto-electronic Material Co., Ltd., and Irresistible Materials Ltd. Leading companies are investing heavily in R&D to develop next-generation resist chemistries suitable for High-NA EUV and sub-5nm process nodes. Strategic collaborations with semiconductor manufacturers help align product innovations with commercial lithography requirements. Firms are expanding production capacities in Asia-Pacific and North America to meet rising regional demand. Some players focus on hybrid lithography solutions and directed self-assembly technologies to broaden product applicability.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Lithography technology

- 2.2.4 End use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics ( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.7 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 (USD Million) (Tons)

- 5.1 Key trends

- 5.2 Positive photoresists

- 5.2.1 Acrylate-based photoresists

- 5.2.2 Novolac-based (dnq) systems

- 5.2.3 Poly (methyl methacrylate) (PMMA)

- 5.3 Negative photoresists

- 5.3.1 Epoxy-based

- 5.3.2 Silicon-containing resists

- 5.3.3 Metal-based resists

Chapter 6 Market Estimates and Forecast, By Lithography Technology, 2021 - 2034 (USD Million) (Tons)

- 6.1 Key trends

- 6.2 Duv lithography

- 6.2.1 248nm krf lithography

- 6.2.2 193nm dry lithography

- 6.2.3 193nm immersion lithography (arfi)

- 6.3 Extreme ultraviolet (euv) lithography

- 6.3.1 Euv @ 13.5 nm

- 6.3.2 High-na euv

- 6.4 I-line lithography (365 nm)

- 6.5 Nanoimprint lithography (nil)

- 6.6 E-beam lithography

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Million) (Tons)

- 7.1 Key trends

- 7.2 Semiconductor device fabrication

- 7.2.1 Logic devices

- 7.2.2 Memory devices

- 7.2.3 Edge devices

- 7.2.4 Image sensors

- 7.3 Mems devices

- 7.3.1 Automotive mems

- 7.3.2 Consumer electronics mems

- 7.3.3 Industrial & healthcare mems

- 7.4 Display electronics applications

- 7.4.1 LCD manufacturing

- 7.4.2 OLED display production

- 7.4.3 Next-generation displays

- 7.5 Advanced packaging applications

- 7.5.1 3d packaging

- 7.5.2 System-in-package (SIP)

- 7.5.3 Wafer-level packaging (WLP)

- 7.6 Photomask manufacturing

- 7.6.1 EUV mask

- 7.6.2 DUV mask

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million) (Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Brewer Science, Inc.

- 9.2 Dongjin Semichem Co., Ltd.

- 9.3 Dow

- 9.4 Eternal Materials Co., Ltd.

- 9.5 Fujifilm Holdings Corporation

- 9.6 Inpria Corporation

- 9.7 Irresistible Materials Ltd.

- 9.8 Jiangsu Nata Opto-electronic Material Co., Ltd.

- 9.9 JSR Corporation

- 9.10 Kayaku Advanced Materials

- 9.11 Merck KGaA

- 9.12 Micro Resist Technology GmbH

- 9.13 Shin-Etsu Chemical Co., Ltd.

- 9.14 Sumitomo Chemical Company

- 9.15 Tokyo Ohka Kogyo Co., Ltd.

- 9.16 Others

2026年光阻剂电子化学品全球市场报告

2026年光阻剂电子化学品全球市场报告 光阻剂原料市场按应用、抗蚀剂类型、材料类型、技术和最终用户划分-2026-2032年全球预测光阻剂电子化学品市场按类型、形态、技术、应用和最终用户划分 - 全球预测 2026-2032半导体光阻剂材料市场:按类型、曝光技术、晶圆尺寸和应用划分-2026-2032年全球预测

光阻剂原料市场按应用、抗蚀剂类型、材料类型、技术和最终用户划分-2026-2032年全球预测光阻剂电子化学品市场按类型、形态、技术、应用和最终用户划分 - 全球预测 2026-2032半导体光阻剂材料市场:按类型、曝光技术、晶圆尺寸和应用划分-2026-2032年全球预测 光阻剂化学品市场-2025-2030年预测

光阻剂化学品市场-2025-2030年预测 全球液态光阻剂市场

全球液态光阻剂市场 2030 年光致变色材料市场预测:按产品、类型、材料、技术、应用、最终用户和地区进行的全球分析ArF干式及ArF浸液抗蚀剂材料的全球市场规模:各类型,各用途,各地区,范围及预测负性光阻剂化学品的全球市场:分析 - 按类型、按药物、按应用、按地区、预测(至 2030 年)

2030 年光致变色材料市场预测:按产品、类型、材料、技术、应用、最终用户和地区进行的全球分析ArF干式及ArF浸液抗蚀剂材料的全球市场规模:各类型,各用途,各地区,范围及预测负性光阻剂化学品的全球市场:分析 - 按类型、按药物、按应用、按地区、预测(至 2030 年) 光阻电子化学品市场,按类型、形式、应用、国家和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测

光阻电子化学品市场,按类型、形式、应用、国家和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测