|

市场调查报告书

商品编码

1871164

汽车网路安全硬体市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Automotive Cybersecurity Hardware Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

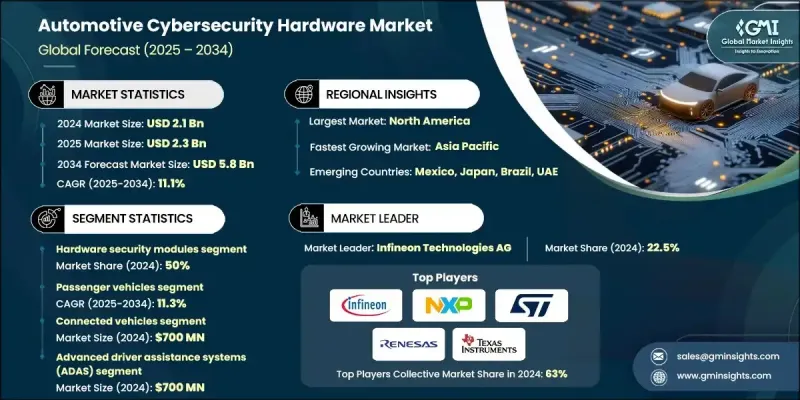

2024 年全球汽车网路安全硬体市场价值为 21 亿美元,预计到 2034 年将以 11.1% 的复合年增长率增长至 58 亿美元。

随着车辆向高度互联的软体定义平台演进,网路威胁情势显着扩大。 ECU、感测器、数位座舱和远端资讯处理系统的日益集成,使得车辆更容易遭受网路威胁。因此,市场对能够保护车辆关键功能并维护运作完整性的硬体级网路安全系统的需求激增。原始设备製造商 (OEM) 和一级供应商正在嵌入安全元件,以防止资料外洩、未经授权的存取和功能中断。集中式车辆架构、OTA 软体更新以及日益严格的汽车网路安全合规法规等趋势正在推动市场加速发展。随着互联互通成为现代出行方式的基石,网路安全硬体在确保安全可靠的驾驶体验方面发挥着至关重要的作用。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 21亿美元 |

| 预测值 | 58亿美元 |

| 复合年增长率 | 11.1% |

2024年,硬体安全模组(HSM)市占率达到50%,预计2025年至2034年将以10.8%的复合年增长率成长。这些模组作为基础安全元件,在车辆核心系统中提供金钥管理、加密处理和防篡改功能。它们部署在电子控制单元(ECU)、网域控制器和连网平台中,支援安全通讯、认证软体功能和即时网路防御能力。汽车製造商越来越依赖HSM来满足监管要求并降低车辆网路中日益增长的网路安全风险。

2024年乘用车市场市占率达82%,预计到2034年将以11.3%的复合年增长率成长。此细分市场的成长主要得益于数位系统在日常车辆(包括电动和混合动力车型)中的广泛应用。安全微控制器、硬体安全模组(HSM)和可信任硬体元件如今已成为资讯娱乐系统、高级驾驶辅助系统(ADAS)、车联网(V2X)和空中下载(OTA)更新框架的标准组件。这些解决方案确保了安全的资料交换、系统完整性,并符合ISO/SAE 21434和UNECE WP.29等国际标准,使其成为下一代汽车平台不可或缺的一部分。

2024年,美国汽车网路安全硬体市场占81.1%的市场份额,市场规模达6.1亿美元。凭藉其先进的汽车生态系统、高电动车普及率以及不断完善的监管体系,美国已成为网路安全硬体的强劲需求中心。汽车製造商正在部署加密模组和先进的ECU(电子控制单元),以应对互联和自动驾驶汽车面临的威胁。美国强劲的监管势头和强大的製造业基础将继续推动嵌入式硬体保护措施在商用和乘用车队中的应用。

活跃于汽车网路安全硬体市场的关键企业包括C2A Security、英飞凌科技(Infineon Technologies AG)、意法半导体(STMicroelectronics NV)、瑞萨电子(Renesas Electronics)、微芯科技(Microchip Technology)、亚德诺半导体(Analog Devices)、NXSduct(Mirctors) Instruments)、GuardKnox和Escrypt。全球汽车网路安全硬体市场的领导者正大力投资于安全硬体IP、晶片级加密技术和可扩展的平台架构,以增强其竞争优势。各公司优先考虑与集中式车辆架构和网域控制器相容的整合就绪型模组,例如HSM和TPM。与OEM厂商和一级供应商的合作有助于确保在早期设计阶段就将相关技术纳入考量,并达成长期供应协议。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 利润率

- 成本结构

- 每个阶段的价值增加

- 影响价值链的因素

- 中断

- 产业影响因素

- 成长驱动因素

- 日益增长的车辆互联

- 电气化和自动驾驶汽车的普及

- 严格的监管框架

- 安全硬体模组的使用日益增多

- 产业陷阱与挑战

- 高昂的实施和整合成本

- 复杂系统集成

- 市场机会

- 采用人工智慧驱动的安全解决方案

- 扩展安全的OTA更新生态系统

- 日益严格的监管合规要求

- 整合云端连线安全解决方案

- 成长驱动因素

- 成长潜力分析

- 监管环境

- ISO 21434 网路安全工程标准

- 联合国R155和R156法规要求

- SAE J3061 网路安全指南

- NIST网路安全框架适应

- 区域合规性和认证要求

- 波特的分析

- PESTEL 分析

- 技术与创新格局

- 加密效能与吞吐量分析

- 安全处理延迟和即时能力

- 威胁侦测准确率和误报率

- 功耗和效率指标

- 防篡改和物理安全评估

- 复杂性与开发时间的整合

- 价格趋势

- 按地区

- 副产品

- 生产统计

- 生产中心

- 消费中心

- 进出口

- 成本細項分析

- 专利分析

- 永续性和环境方面

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

- 风险评估框架

- 最佳情况

- 隐私与资料保护框架分析

- 市场成熟度与采纳分析

- 汽车资料隐私要求

- GDPR 与区域隐私法规合规性

- 数据匿名化与假名化技术

- 同意管理和用户控制

- 跨境资料传输安全

- 威胁情势与攻击向量分析

- 车辆攻击面测绘

- 常见攻击途径与方法

- 新兴威胁趋势及预测

- 产业事件分析及经验教训

- 威胁情报与资讯共享

- 隐私与资料保护框架分析

- 汽车资料隐私要求

- GDPR 与区域隐私法规合规性

- 数据匿名化与假名化技术

- 同意管理和用户控制

- 跨境资料传输安全

第四章:竞争格局

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划和资金

第五章:市场估算与预测:依硬体划分,2021-2034年

- 主要趋势

- 硬体安全模组(HSM)

- 网路安全控制器

- 防火墙和入侵侦测单元

- 安全微控制器

- 加密/解密晶片

第六章:市场估计与预测:依车辆互联程度划分,2021-2034年

- 主要趋势

- 连网汽车

- 半自主

- 全自动驾驶汽车

- 非连网车辆

第七章:市场估价与预测:依车辆类型划分,2021-2034年

- 主要趋势

- 搭乘用车

- SUV

- 轿车

- 掀背车

- 商用车辆

- 轻型商用车(LCV)

- 中型商用车(MCV)

- 重型商用车(HCV)

第八章:市场估算与预测:依应用领域划分,2021-2034年

- 主要趋势

- 高级驾驶辅助系统(ADAS)

- 资讯娱乐和车载资讯系统

- 动力总成和底盘

- 车身电子设备与舒适系统

- 通讯系统(V2X、OTA 更新)

- 其他的

第九章:市场估算与预测:依销售管道划分,2021-2034年

- 主要趋势

- OEM

- 售后市场

第十章:市场估计与预测:依地区划分,2021-2034年

- 主要趋势

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 比利时

- 荷兰

- 瑞典

- 亚太地区

- 中国

- 中国

- 印度

- 日本

- 澳洲

- 新加坡

- 韩国

- 越南

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 阿联酋

- 南非

- 沙乌地阿拉伯

第十一章:公司简介

- 全球参与者

- Analog Devices

- Blackberry

- Infineon Technologies AG

- Maxim Integrated Products

- Microchip Technology

- NXP Semiconductors

- Qualcomm Technologies

- Renesas Electronics Corporation

- STMicroelectronics NV

- Texas Instruments Incorporated

- 区域玩家

- Aptiv PLC

- BMW

- Continental AG

- Denso

- Harman International

- Mercedes-Benz

- Robert Bosch

- Tesla

- 新兴玩家

- Argus Cyber Security

11.3.2. C2 A 安全

- Escrypt

- GuardKnox

- 卡兰巴安保

- 上游

The Global Automotive Cybersecurity Hardware Market was valued at USD 2.1 Billion in 2024 and is estimated to grow at a CAGR of 11.1% to reach USD 5.8 Billion by 2034.

As vehicles evolve into highly connected, software-defined platforms, the threat landscape has expanded significantly. Increasing integration of ECUs, sensors, digital cockpits, and telematics systems has created greater vulnerabilities to cyber threats. In response, demand is surging for hardware-based cybersecurity systems that can secure critical vehicle functions and maintain operational integrity. OEMs and Tier-1 suppliers are embedding secure elements to prevent data breaches, unauthorized access, and functional disruptions. The market is accelerating due to trends like centralized vehicle architectures, OTA software updates, and tighter regulations around automotive cybersecurity compliance. As connectivity becomes a cornerstone of modern mobility, cybersecurity hardware is playing a pivotal role in ensuring safe and trusted driving experiences.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.1 Billion |

| Forecast Value | $5.8 Billion |

| CAGR | 11.1% |

In 2024, the hardware security modules segment held a 50% share and is projected to grow at a CAGR of 10.8% from 2025 to 2034. These modules act as foundational security components, delivering key management, cryptographic processing, and tamper resistance within core vehicle systems. Their deployment in ECUs, domain controllers, and connected platforms supports secure communication, authenticated software functions, and real-time cyber defense capabilities. Automakers increasingly rely on HSMs to meet regulatory mandates and mitigate rising cybersecurity risks in vehicle networks.

The passenger vehicles segment held an 82% share in 2024 and is expected to grow at a 11.3% CAGR through 2034. Growth in this segment is fueled by widespread integration of digital systems in everyday vehicles, including electric and hybrid models. Secure microcontrollers, HSMs, and trusted hardware elements are now standard components in infotainment systems, ADAS, V2X connectivity, and OTA update frameworks. These solutions ensure secure data exchange, system integrity, and alignment with international standards like ISO/SAE 21434 and UNECE WP.29, making them essential for next-gen automotive platforms.

US Automotive Cybersecurity Hardware Market held an 81.1% share and generated USD 610 million in 2024. With its advanced automotive ecosystem, high EV adoption rate, and evolving regulations, the US represents a strong demand center for cybersecurity hardware. Automakers are deploying cryptographic modules and advanced ECUs to address threats in connected and autonomous vehicles. The country's regulatory momentum and robust manufacturing base continue to support the rollout of embedded hardware protections across commercial and passenger fleets.

Key companies active in the Automotive Cybersecurity Hardware Market include C2A Security, Infineon Technologies AG, STMicroelectronics N.V., Renesas Electronics, Microchip Technology, Analog Devices, NXP Semiconductors N.V., Texas Instruments, GuardKnox, and Escrypt. Leading players in the Global Automotive Cybersecurity Hardware Market are heavily investing in secure hardware IP, chip-level cryptography, and scalable platform architectures to strengthen their competitive edge. Companies are prioritizing integration-ready modules such as HSMs and TPMs that are compatible with centralized vehicle architectures and domain controllers. Collaborations with OEMs and Tier-1 suppliers help ensure early design-phase inclusion and long-term supply agreements.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Hardware

- 2.2.3 Vehicle connectivity level

- 2.2.4 Vehicle

- 2.2.5 Application

- 2.2.6 Sales Channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing vehicle connectivity

- 3.2.1.2 Electrification and autonomous vehicle adoption

- 3.2.1.3 Stringent regulatory frameworks

- 3.2.1.4 Increasing use of secure hardware modules

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High implementation and integration costs

- 3.2.2.2 Complex system integration

- 3.2.3 Market opportunities

- 3.2.3.1 Adoption of AI-driven security solutions

- 3.2.3.2 Expansion of secure OTA update ecosystems

- 3.2.3.3 Increasing regulatory compliance requirements

- 3.2.3.4 Integration of cloud-connected security solutions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 ISO 21434 cybersecurity engineering standard

- 3.4.2 UN-R155 & UN-R156 regulatory requirements

- 3.4.3 SAE J3061 cybersecurity guidebook

- 3.4.4 NIST cybersecurity framework adaptation

- 3.4.5 Regional compliance & certification requirements

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation Landscape

- 3.7.1 Cryptographic performance & throughput analysis

- 3.7.2 Security processing latency & real-time capability

- 3.7.3 Threat detection accuracy & false positive rates

- 3.7.4 Power consumption & efficiency metrics

- 3.7.5 Tamper resistance & physical security assessment

- 3.7.6 Integration of complexity & development time

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Risk assessment framework

- 3.14 Best case scenarios

- 3.15 Privacy & Data Protection Framework Analysis

- 3.16 Market maturity & adoption analysis

- 3.16.1 Automotive data privacy requirements

- 3.16.2 GDPR & regional privacy regulation compliance

- 3.16.3 Data anonymization & pseudonymization techniques

- 3.16.4 Consent management & user control

- 3.16.5 Cross-border data transfer security

- 3.17 Threat landscape & attack vector analysis

- 3.17.1 Vehicle attack surface mapping

- 3.17.2 Common attack vectors & methodologies

- 3.17.3 Emerging threat trends & predictions

- 3.17.4 Industry incident analysis & lessons learned

- 3.17.5 Threat intelligence & information sharing

- 3.18 Privacy & data protection framework analysis

- 3.18.1 Automotive data privacy requirements

- 3.18.2 GDPR & regional privacy regulation compliance

- 3.18.3 Data anonymization & pseudonymization techniques

- 3.18.4 Consent management & user control

- 3.18.5 Cross-border data transfer security

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Hardware, 2021 - 2034 ($ Bn, Units)

- 5.1 Key trends

- 5.2 Hardware security module (HSM)

- 5.3 Network security controllers

- 5.4 Firewalls and intrusion detection units

- 5.5 Secure microcontrollers

- 5.6 Encryption/decryption chips

Chapter 6 Market Estimates & Forecast, By Vehicle Connectivity Level, 2021 - 2034 ($ Bn, Units)

- 6.1 Key trends

- 6.2 Connected vehicles

- 6.3 Semi-autonomous

- 6.4 Fully autonomous vehicles

- 6.5 Non-connected vehicles

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Passenger Vehicles

- 7.2.1 SUV

- 7.2.2 Sedan

- 7.2.3 Hatchback

- 7.3 Commercial Vehicles

- 7.3.1 Light commercial vehicles (LCV)

- 7.3.2 Medium commercial vehicles (MCV)

- 7.3.3 Heavy commercial vehicles (HCV)

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Advanced driver assistance systems (ADAS)

- 8.3 Infotainment & telematics

- 8.4 Powertrain & chassis

- 8.5 Body electronics & comfort systems

- 8.6 Communication systems (V2X, OTA updates)

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 Key trends

- 10.3 North America

- 10.3.1 US

- 10.3.2 Canada

- 10.4 Europe

- 10.4.1 UK

- 10.4.2 Germany

- 10.4.3 France

- 10.4.4 Italy

- 10.4.5 Spain

- 10.4.6 Belgium

- 10.4.7 Netherlands

- 10.4.8 Sweden

- 10.5 Asia Pacific

- 10.5.1 China

- 10.5.2 China

- 10.5.3 India

- 10.5.4 Japan

- 10.5.5 Australia

- 10.5.6 Singapore

- 10.5.7 South Korea

- 10.5.8 Vietnam

- 10.5.9 Indonesia

- 10.6 Latin America

- 10.6.1 Brazil

- 10.6.2 Mexico

- 10.6.3 Argentina

- 10.7 MEA

- 10.7.1 UAE

- 10.7.2 South Africa

- 10.7.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Global players

- 11.1.1 Analog Devices

- 11.1.2 Blackberry

- 11.1.3 Infineon Technologies AG

- 11.1.4 Maxim Integrated Products

- 11.1.5 Microchip Technology

- 11.1.6 NXP Semiconductors

- 11.1.7 Qualcomm Technologies

- 11.1.8 Renesas Electronics Corporation

- 11.1.9 STMicroelectronics N.V.

- 11.1.10 Texas Instruments Incorporated

- 11.2 Regional players

- 11.2.1 Aptiv PLC

- 11.2.2 BMW

- 11.2.3 Continental AG

- 11.2.4 Denso

- 11.2.5 Harman International

- 11.2.6 Mercedes-Benz

- 11.2.7 Robert Bosch

- 11.2.8 Tesla

- 11.3 Emerging players

- 11.3.1 Argus Cyber Security

11.3.2. C2 A Security

- 11.3.3 Escrypt

- 11.3.4 GuardKnox

- 11.3.5 Karamba Security

- 11.3.6 Upstream

互联行动安全解决方案市场预测至2034年:按产品类型、连接类型、技术、应用、最终用户和地区分類的全球分析

互联行动安全解决方案市场预测至2034年:按产品类型、连接类型、技术、应用、最终用户和地区分類的全球分析 2026年全球外部云端汽车保全服务市场报告

2026年全球外部云端汽车保全服务市场报告 汽车软体开发与安全解决方案

汽车软体开发与安全解决方案 汽车网路安全市场(至 2040 年):依组件、形式、安全类型、车辆类型、应用、地区和主要参与者划分的行业趋势和全球预测

汽车网路安全市场(至 2040 年):依组件、形式、安全类型、车辆类型、应用、地区和主要参与者划分的行业趋势和全球预测 联网汽车安全市场机会、成长要素、产业趋势分析及2026年至2035年预测

联网汽车安全市场机会、成长要素、产业趋势分析及2026年至2035年预测 汽车网路安全市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户和解决方案划分

汽车网路安全市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户和解决方案划分 2026-2034年全球汽车网路安全市场规模、份额、趋势和成长分析报告人工智慧在汽车网路安全领域的市场机会、成长驱动因素、产业趋势分析及预测(2026-2035年)

2026-2034年全球汽车网路安全市场规模、份额、趋势和成长分析报告人工智慧在汽车网路安全领域的市场机会、成长驱动因素、产业趋势分析及预测(2026-2035年) 乘用车网路安全市场-全球产业规模、份额、趋势、机会、预测:按安全类型、应用类型、地区和竞争格局划分,2021-2031年商用车网路安全市场-全球产业规模、份额、趋势、机会、预测:按安全类型、应用、地区和竞争格局划分,2021-2031年

乘用车网路安全市场-全球产业规模、份额、趋势、机会、预测:按安全类型、应用类型、地区和竞争格局划分,2021-2031年商用车网路安全市场-全球产业规模、份额、趋势、机会、预测:按安全类型、应用、地区和竞争格局划分,2021-2031年