|

市场调查报告书

商品编码

1871238

自修復防水材料市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Self-healing Waterproofing Materials Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

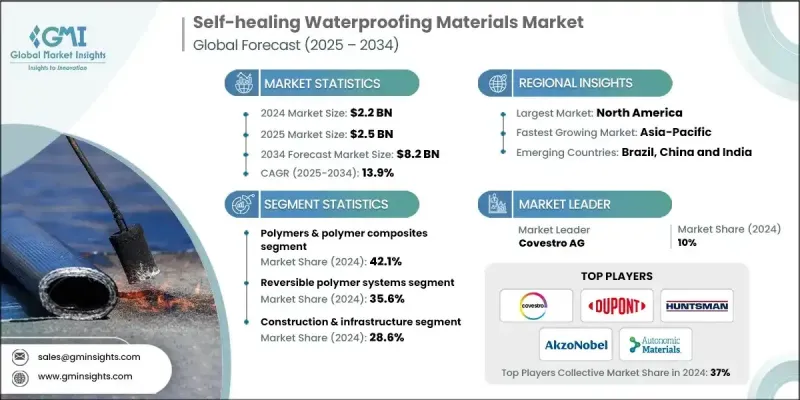

2024 年全球自修復防水材料市场价值为 22 亿美元,预计到 2034 年将以 13.9% 的复合年增长率增长至 82 亿美元。

随着各行业日益关注长期耐久性和降低维护成本,市场正经历强劲成长。这些先进材料在建筑、汽车和电子应用领域正获得广泛认可,因为在这些领域,潮湿和恶劣的环境条件往往会影响材料的性能和使用寿命。在建筑领域,自修復涂料和混凝土正被应用于提高结构韧性并最大限度地降低生命週期成本。汽车产业正在采用耐腐蚀和损伤修復表面来增强耐久性。微胶囊化、血管系统和形状记忆聚合物等技术的进步正在推动更高效的自修復机制的发展。此外,用于即时损伤检测和自主修復激活的传感器系统的整合正在塑造下一代防水解决方案。儘管取得了这些进展,但市场仍面临着成本效益和可扩展性方面的挑战,尤其是在发展中经济体。然而,对永续材料的监管支持力度不断加大以及全球在标准化方面所做的努力有望促进其商业化。亚太地区基础设施的快速发展,在城市化进程和对持久耐用建筑材料日益增长的需求的推动下,进一步促进了市场扩张。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 22亿美元 |

| 预测值 | 82亿美元 |

| 复合年增长率 | 13.9% |

2024年,聚合物及聚合物复合材料市占率达到42.1%,预计2034年将以13.6%的复合年增长率成长。其市场主导地位归功于其高度的适应性、成熟的製造流程以及在多个行业多样化应用领域的适用性。这些材料可采用多种自修復机制,使其成为建筑、汽车和电子应用的理想选择。永续和生物基聚合物技术的不断进步,以及研发投入的不断成长,正在进一步提升全球环保市场对这类材料的需求。

2024年,可逆聚合物体系市占率达到35.6%,预计2025年至2034年间将以13.7%的复合年增长率成长。这些系统因其能够在多次自癒循环中保持良好的机械性能而备受青睐。基于动态共价键和非共价键,它们能够在受到应力或损伤时自主恢復结构。其与现有製造流程的兼容性以及商业化规模化生产的特性,使其非常适合建筑、电子和交通运输等行业的大规模应用。其自癒机制的可靠性和可重复性也促进了其在工业领域的广泛应用。

2024年,北美自修復防水材料市占率达38.2%。该地区受益于政府的大力支持、世界一流的研究设施以及先进材料的早期商业化。航太、国防和基础设施领域的高性能应用正在推动市场需求,而私营和公共机构对创新的巨额投资也为此提供了有力支撑。致力于材料科学的研究合作和机构的资助持续巩固北美的领先地位。众多知名大学、新创企业和成熟的化学企业的存在,推动了产品的持续开发和技术进步,确保了该地区创新自修復解决方案的稳定供应。

全球自修復防水材料市场的主要参与者包括:Autonomic Materials Inc.、杜邦公司、PPG工业公司、Avecom NV、科思创股份公司、Critical Materials SA、Tnemec Company Inc.、Devan Chemicals NV、阿克苏诺贝尔公司、亨斯迈公司、Applied Thin Films Inc.、Acciona Ltd SA 和 Som。为了巩固市场地位,领先企业正致力于技术创新、产品多元化和永续发展。许多企业正在加大研发投入,以提高自修復系统的效率、反应速度和成本效益。他们正与研究机构和工业企业建立策略合作伙伴关係,以加速产品测试和商业化进程。製造商正在扩大产能,并开发环保配方,以满足全球永续发展标准。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 利润率

- 每个阶段的价值增加

- 影响价值链的因素

- 中断

- 产业影响因素

- 成长驱动因素

- 基础设施维护成本不断增长,以及降低维修频率的需求日益迫切。

- 航太工业需要轻质、自修復复合材料

- 汽车产业力推耐刮擦和自我修復涂层

- 产业陷阱与挑战

- 高昂的初始材料成本和复杂的製造工艺

- 标准化测试方案和效能验证有限

- 市场机会

- 再生能源系统中的新兴应用

- 医疗器材整合及生物相容性自修復材料

- 成长驱动因素

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL 分析

- 价格趋势

- 按地区

- 依材料类型

- 未来市场趋势

- 技术与创新格局

- 当前技术趋势

- 新兴技术

- 专利格局

- 贸易统计(HS编码)(註:仅提供重点国家的贸易统计资料)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估算与预测:依材料类型划分,2021-2034年

- 主要趋势

- 聚合物及聚合物复合材料

- 金属及金属合金

- 陶瓷和玻璃材料

- 混凝土及水泥材料

- 复合材料

第六章:市场估计与预测:依技术划分,2021-2034年

- 主要趋势

- 可逆聚合物体系

- 形状记忆材料

- 微胶囊化技术

- 血管网路系统

- 生物材料系统

第七章:市场估算与预测:依最终用途划分,2021-2034年

- 主要趋势

- 建筑与基础设施

- 汽车与运输

- 航太与国防

- 医疗保健和生物医学

- 电子与半导体

- 能源与电力系统

第八章:市场估算与预测:依地区划分,2021-2034年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

- 中东和非洲其他地区

第九章:公司简介

- Covestro AG

- DuPont de Nemours Inc.

- Huntsman Corporation

- Akzo Nobel NV

- Autonomic Materials Inc.

- Acciona SA

- PPG Industries Inc.

- Applied Thin Films Inc.

- Avecom NV

- Critical Materials SA

- Devan Chemicals NV

- Sensor Coating Systems Ltd.

- Tnemec Company, Inc.

The Global Self-healing Waterproofing Materials Market was valued at USD 2.2 Billion in 2024 and is estimated to grow at a CAGR of 13.9% to reach USD 8.2 Billion by 2034.

The market is experiencing strong growth as industries increasingly focus on long-term durability and reduced maintenance costs. These advanced materials are gaining traction in construction, automotive, and electronics applications, where exposure to moisture and harsh environmental conditions often affects performance and lifespan. In the construction sector, self-healing coatings and concretes are being incorporated to improve structural resilience and minimize lifecycle expenses. The automotive industry is adopting corrosion-resistant and damage-repairing surfaces to enhance durability. Technological progress in microencapsulation, vascular systems, and shape-memory polymers is driving the evolution of more efficient self-repair mechanisms. In addition, the integration of sensor-based systems for real-time damage detection and autonomous healing activation is shaping the next generation of waterproofing solutions. Despite these advancements, the market faces challenges related to cost-effectiveness and scalability, especially in developing economies. However, growing regulatory support for sustainable materials and global efforts toward standardization are expected to foster commercialization. Rapid infrastructure development across the Asia-Pacific region further contributes to market expansion, driven by urbanization and the rising need for long-lasting construction materials.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.2 Billion |

| Forecast Value | $8.2 Billion |

| CAGR | 13.9% |

The polymers and polymer composites segment held a 42.1% share in 2024 and is projected to grow at a CAGR of 13.6% through 2034. Their dominance is attributed to high adaptability, mature manufacturing capabilities, and suitability for diverse applications across multiple industries. These materials can employ a range of self-healing mechanisms, making them ideal for construction, automotive, and electronic applications. Continuous advancements in sustainable and bio-based polymer technologies, combined with growing research investments, are reinforcing their demand in environmentally conscious markets worldwide.

The reversible polymer systems segment held 35.6% share in 2024 and is expected to grow at a CAGR of 13.7% during 2025-2034. These systems are favored for their ability to undergo multiple healing cycles without significant loss in mechanical performance. Based on dynamic covalent and non-covalent bonding, they can autonomously restore their structure when exposed to stress or damage. Their compatibility with existing manufacturing processes and commercial scalability make them highly suitable for large-scale applications in sectors such as construction, electronics, and transportation. The reliability and repeatability of their healing mechanisms contribute to their widespread industrial adoption.

North America Self-healing Waterproofing Materials Market held 38.2% share in 2024. The region benefits from strong government funding, world-class research facilities, and early commercialization of advanced materials. High-performance applications in aerospace, defense, and infrastructure are driving demand, supported by significant investments in innovation from both private and public institutions. Research collaborations and funding from agencies dedicated to material science continue to strengthen North America's leadership position. The presence of major universities, startups, and established chemical companies fuels continuous product development and technological advancement, ensuring a steady supply of innovative self-healing solutions across the region.

Key companies active in the Global Self-healing Waterproofing Materials Market include Autonomic Materials Inc., DuPont de Nemours Inc., PPG Industries Inc., Avecom N.V., Covestro AG, Critical Materials S.A., Tnemec Company Inc., Devan Chemicals NV, Akzo Nobel N.V., Huntsman Corporation, Applied Thin Films Inc., Acciona S.A., and Sensor Coating Systems Ltd. To strengthen their position, leading companies are focusing on technological innovation, product diversification, and sustainable development. Many are increasing R&D investments to improve the efficiency, responsiveness, and cost-effectiveness of self-healing systems. Strategic partnerships with research organizations and industrial players are being established to accelerate product testing and commercialization. Manufacturers are expanding production capacities and developing eco-friendly formulations to meet global sustainability standards.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Material type

- 2.2.3 Technology type

- 2.2.4 End use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing infrastructure maintenance costs & repair frequency reduction needs

- 3.2.1.2 Aerospace industry demands lightweight, self-repairing composites

- 3.2.1.3 Automotive industry push for scratch-resistant & self-healing coatings

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial material costs & manufacturing complexity

- 3.2.2.2 Limited standardized testing protocols & performance validation

- 3.2.3 Market opportunities

- 3.2.3.1 Emerging applications in renewable energy systems

- 3.2.3.2 Medical device integration & biocompatible self-healing materials

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By material type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) ( Note: the trade statistics will be provided for key countries only )

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Material Type, 2021-2034 (USD Billion) (Kilo tons)

- 5.1 Key trends

- 5.2 Polymers & polymer composites

- 5.3 Metals & metal alloys

- 5.4 Ceramics & glass materials

- 5.5 Concrete & cementitious materials

- 5.6 Composite materials

Chapter 6 Market Estimates and Forecast, By Technology, 2021-2034 (USD Billion) (Kilo tons)

- 6.1 Key trends

- 6.2 Reversible polymer systems

- 6.3 Shape memory materials

- 6.4 Microencapsulation technologies

- 6.5 Vascular network systems

- 6.6 Biological material systems

Chapter 7 Market Estimates and Forecast, By End Use, 2021-2034 (USD Billion) (Kilo tons)

- 7.1 Key trends

- 7.2 Construction & infrastructure

- 7.3 Automotive & transportation

- 7.4 Aerospace & defense

- 7.5 Healthcare & biomedical

- 7.6 Electronics & semiconductors

- 7.7 Energy & power systems

Chapter 8 Market Estimates and Forecast, By Region, 2021-2034 (USD Billion) (Kilo tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Covestro AG

- 9.2 DuPont de Nemours Inc.

- 9.3 Huntsman Corporation

- 9.4 Akzo Nobel N.V.

- 9.5 Autonomic Materials Inc.

- 9.6 Acciona S.A.

- 9.7 PPG Industries Inc.

- 9.8 Applied Thin Films Inc.

- 9.9 Avecom N.V.

- 9.10 Critical Materials S.A.

- 9.11 Devan Chemicals NV

- 9.12 Sensor Coating Systems Ltd.

- 9.13 Tnemec Company, Inc.

生物降解自组装材料市场分析及预测(至2035年):类型、产品、应用、技术、材料类型、最终用户、功能、安装类型自癒式电子电路市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、材料类型、装置、功能及最终用户划分自组装奈米电路市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、材料类型、製程、最终用户、功能划分

生物降解自组装材料市场分析及预测(至2035年):类型、产品、应用、技术、材料类型、最终用户、功能、安装类型自癒式电子电路市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、材料类型、装置、功能及最终用户划分自组装奈米电路市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、材料类型、製程、最终用户、功能划分 全球自修復材料市场规模、份额、趋势和成长分析报告(2026-2034年)

全球自修復材料市场规模、份额、趋势和成长分析报告(2026-2034年) 自修復聚合物市场机会、成长要素、产业趋势分析及2026年至2035年预测。

自修復聚合物市场机会、成长要素、产业趋势分析及2026年至2035年预测。 自修復材料市场规模、份额和成长分析(按类型、产品、技术、应用和地区划分)-2026-2033年产业预测

自修復材料市场规模、份额和成长分析(按类型、产品、技术、应用和地区划分)-2026-2033年产业预测 自修復聚合物市场规模、份额和趋势分析报告:按材料、应用、地区和细分市场预测(2025-2033 年)

自修復聚合物市场规模、份额和趋势分析报告:按材料、应用、地区和细分市场预测(2025-2033 年) 自修復材料市场-全球产业规模、份额、趋势、机会和预测,按形态、材料类型、最终用途、地区和竞争格局划分,2020-2030年预测

自修復材料市场-全球产业规模、份额、趋势、机会和预测,按形态、材料类型、最终用途、地区和竞争格局划分,2020-2030年预测 全球基础设施用自修復材料市场:预测至2032年-按材料类型、修復机制、技术、应用、最终用户和地区分類的分析自癒地板材料市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)

全球基础设施用自修復材料市场:预测至2032年-按材料类型、修復机制、技术、应用、最终用户和地区分類的分析自癒地板材料市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)