|

市场调查报告书

商品编码

1876536

发酵衍生蛋白配料市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Fermentation-Derived Protein Ingredients Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

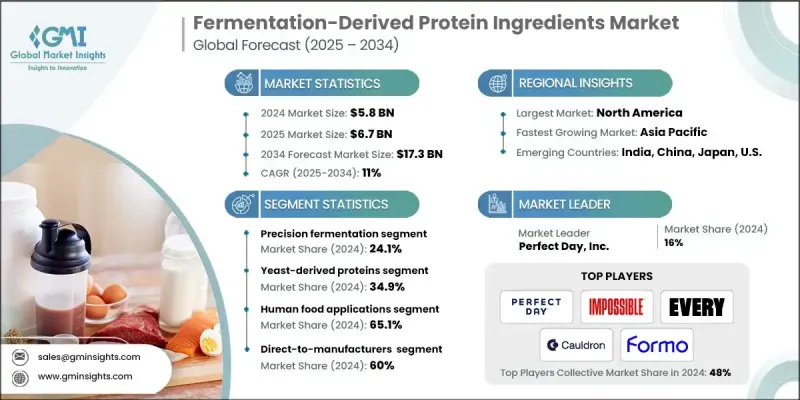

2024 年全球发酵衍生蛋白质配料市场价值为 58 亿美元,预计到 2034 年将以 11% 的复合年增长率增长至 173 亿美元。

消费者对永续、植物性和清洁标籤蛋白解决方案的需求日益增长,推动了市场扩张。发酵蛋白因其可扩展性、营养价值以及与传统动物性蛋白质相比更低的环境影响,正作为替代蛋白来源而备受青睐。这些蛋白质由微生物、真菌或基因工程改造的微生物生产,所需的土地、水和能源资源显着减少,从而降低了整体生态足迹。发酵过程能够确保品质稳定、安全可靠且易于规模化生产,使其对素食主义者和具有道德意识的消费者极具吸引力。其功能特性使其可用于强化各种食品,延长保存期限,并提升风味。包括生物改良、合成製程和人工智慧驱动的自动化在内的製造技术创新,正在进一步优化生产效率,减少浪费,并实现对蛋白质特性和功能特性的精准控制。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 58亿美元 |

| 预测值 | 173亿美元 |

| 复合年增长率 | 11% |

到 2024 年,精准发酵领域占据了 24.1% 的市场份额,预计到 2034 年将以 11.1% 的复合年增长率成长。此方法利用基因工程微生物生产与传统来源蛋白质相似的特定蛋白质,从而可以控制营养成分、功能和感官属性。

细菌蛋白市占率为25.1%,预计到2034年将以11.2%的复合年增长率成长,该细分市场主要由生长速度快、产量高的细菌菌株生产。此细分市场涵盖传统的单细胞蛋白质和精准发酵蛋白,使细菌成为大规模生产高效可靠的蛋白质来源。

北美发酵衍生蛋白配料市场占据43.5%的市场份额,年复合成长率达11.1%,预计到2024年市场规模将达20亿美元。市场成长主要得益于消费者对永续植物蛋白的强劲需求,以及发酵技术的进步。此外,美国和加拿大素食主义和弹性素食主义的兴起,以及监管支持和清洁标籤创新,进一步推动了市场的普及和扩张。

全球发酵蛋白配料市场的主要参与者包括ScaleUp Bio、Formo、TurtleTree Labs、Nature's Fynd、Onego Bio、Solar Foods Oy、Standing Ovation、The Better Meat Co.、Cauldron、The EVERY Company、Perfect Day, Inc.和Impossible Foods Inc.。这些公司正致力于创新、研发和策略合作,以巩固其市场地位。许多公司正在开发新一代发酵技术和基因优化菌株,以提高蛋白质的产量、品质和功能性。此外,各公司也正在投资自动化和人工智慧驱动的生产系统,以提高效率、减少浪费并维持产品标准的一致性。与食品和饮料製造商的策略合作有助于将这些蛋白质整合到面向消费者的产品中。同时,各公司也正在扩大区域生产设施、与供应商建立联盟并寻求授权协议,以扩大其业务范围。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 利润率

- 每个阶段的价值增加

- 影响价值链的因素

- 中断

- 产业影响因素

- 成长驱动因素

- 产业陷阱与挑战

- 市场机会

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL 分析

- 价格趋势

- 按地区

- 来源

- 未来市场趋势

- 技术与创新格局

- 当前技术趋势

- 新兴技术

- 专利格局

- 贸易统计(HS编码)(註:仅提供重点国家的贸易统计资料)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估算与预测:依生产技术划分,2021-2034年

- 主要趋势

- 精准发酵

- 生物质发酵

- 其他的

第六章:市场估算与预测:依来源划分,2021-2034年

- 主要趋势

- 细菌来源的蛋白质

- 酵母来源的蛋白质

- 丝状真菌来源的蛋白质

- 微藻来源的蛋白质

第七章:市场估计与预测:依应用领域划分,2021-2034年

- 关键趋势

- 人类食品应用

- 乳製品替代蛋白

- 肉类替代品及增强剂

- 鸡蛋替代蛋白

- 功能性食品和饮料

- 营养补充品

- 动物饲料应用

- 牲畜饲料添加剂

- 水产养殖蛋白

- 宠物食品原料

- 特种动物营养

- 药物应用

- 治疗性蛋白质的生产

- 营养保健品与医疗营养

- 化妆品和个人护理应用

- 功能蛋白

- 抗老与护肤

- 护髮产品

- 其他的

第八章:市场估算与预测:依配销通路划分,2021-2034年

- 主要趋势

- 直接向製造商供货

- 特种原料分销商

- 合约製造组织(CMOS)

- 线上平台

- 其他的

第九章:市场估计与预测:依地区划分,2021-2034年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

- 中东和非洲其他地区

第十章:公司简介

- Cauldron

- Formo

- Impossible Foods Inc.

- Nature's Fynd

- Onego Bio

- Perfect Day, Inc.

- ScaleUp Bio

- Solar Foods Oy

- Standing Ovation

- The Better Meat Co.

- The EVERY Company

- TurtleTree Labs

The Global Fermentation-Derived Protein Ingredients Market was valued at USD 5.8 billion in 2024 and is estimated to grow at a CAGR of 11% to reach USD 17.3 billion by 2034.

Market expansion is fueled by increasing consumer preference for sustainable, plant-based, and clean-label protein solutions. Fermentation-derived proteins are gaining traction as alternative protein sources due to their scalability, nutritional value, and reduced environmental impact compared to conventional animal proteins. Produced from microbes, fungi, or engineered microorganisms, these proteins require significantly fewer land, water, and energy resources, lowering the overall ecological footprint. Fermentation processes offer consistent quality, safety, and scalability, making these ingredients attractive to vegan and ethically conscious consumers. Their functional properties allow for fortification, improved shelf life, and enhanced flavor profiles in various food products. Innovations in manufacturing, including biological improvements, synthetic processes, and AI-driven automation, are further optimizing production efficiency, reducing waste, and enabling precise control over protein characteristics and functional properties.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.8 Billion |

| Forecast Value | $17.3 Billion |

| CAGR | 11% |

The precision fermentation segment held a 24.1% share in 2024, with a projected CAGR of 11.1% through 2034. This method uses genetically engineered microorganisms to produce specific proteins that mirror those from conventional sources, allowing control over nutritional content, functionality, and sensory attributes.

The bacterial-derived proteins segment held a 25.1% share, growing at 11.2% CAGR through 2034, generated from bacterial species with high growth rates and yields. This segment includes both traditional single-cell proteins and precision fermentation-derived proteins, making bacteria an efficient and reliable protein source for large-scale production.

North America Fermentation-Derived Protein Ingredients Market held 43.5% share, with a CAGR of 11.1% and generated USD 2 billion in 2024. Growth is driven by strong consumer demand for sustainable and plant-based proteins, supported by technological advancements in fermentation. The rise of vegan and flexitarian diets across the U.S. and Canada, along with regulatory support and clean-label innovations, is further fueling market adoption and expansion.

Key players in the Global Fermentation-Derived Protein Ingredients Market include ScaleUp Bio, Formo, TurtleTree Labs, Nature's Fynd, Onego Bio, Solar Foods Oy, Standing Ovation, The Better Meat Co., Cauldron, The EVERY Company, Perfect Day, Inc., and Impossible Foods Inc. Companies in the Global Fermentation-Derived Protein Ingredients Market are focusing on innovation, R&D, and strategic partnerships to strengthen their market presence. Many are developing next-generation fermentation techniques and genetically optimized strains to enhance protein yield, quality, and functionality. Firms are also investing in automated and AI-driven production systems to increase efficiency, reduce waste, and maintain consistent product standards. Strategic collaborations with food and beverage manufacturers enable integration of these proteins into consumer-ready products. Additionally, companies are expanding regional production facilities, forming alliances with suppliers, and pursuing licensing agreements to broaden their reach.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Production technology

- 2.2.3 Sources

- 2.2.4 Application

- 2.2.5 Distribution channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By source

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Production Technology, 2021-2034 (USD Billion & Kilo Tons)

- 5.1 Key trends

- 5.2 Precision fermentation

- 5.3 Biomass fermentation

- 5.4 Others

Chapter 6 Market Estimates and Forecast, By Sources, 2021-2034 (USD Billion & Kilo Tons)

- 6.1 Key trends

- 6.2 Bacterial-derived proteins

- 6.3 Yeast-derived proteins

- 6.4 Filamentous fungi-derived proteins

- 6.5 Microalgae-derived proteins

Chapter 7 Market Estimates and Forecast, By Application, 2021-2034 (USD Billion & Kilo Tons)

- 7.1 Key trend

- 7.2 Human food applications

- 7.2.1 Dairy alternative proteins

- 7.2.2 Meat alternative & enhancement

- 7.2.3 Egg alternative protein

- 7.2.4 Functional food & beverage

- 7.2.5 Nutritional supplement

- 7.3 Animal feed applications

- 7.3.1 Livestock feed supplement

- 7.3.2 Aquaculture protein

- 7.3.3 Pet food ingredient

- 7.3.4 Specialty animal nutrition

- 7.4 Pharmaceutical applications

- 7.4.1 Therapeutic protein production

- 7.4.2 Nutraceutical & medical nutrition

- 7.5 Cosmetic & personal care applications

- 7.5.1 Functional protein

- 7.5.2 Anti-aging & skin care

- 7.5.3 Hair care product

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021-2034 (USD Billion & Kilo Tons)

- 8.1 Key trends

- 8.2 Direct-to-manufacturer

- 8.3 Specialty ingredient distributors

- 8.4 Contract manufacturing organizations (CMOS)

- 8.5 Online platforms

- 8.6 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021-2034 (USD Billion & Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Cauldron

- 10.2 Formo

- 10.3 Impossible Foods Inc.

- 10.4 Nature's Fynd

- 10.5 Onego Bio

- 10.6 Perfect Day, Inc.

- 10.7 ScaleUp Bio

- 10.8 Solar Foods Oy

- 10.9 Standing Ovation

- 10.10 The Better Meat Co.

- 10.11 The EVERY Company

- 10.12 TurtleTree Labs

发酵原料市场规模、份额及成长分析(按应用、类型、原料来源、形态及地区划分)-2026-2033年产业预测

发酵原料市场规模、份额及成长分析(按应用、类型、原料来源、形态及地区划分)-2026-2033年产业预测 发酵衍生蛋白市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)

发酵衍生蛋白市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年) 人类和动物营养产业的永续发展倡议和成长机会

人类和动物营养产业的永续发展倡议和成长机会