|

市场调查报告书

商品编码

1876537

自愿性农业碳信用市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Voluntary Agriculture Carbon Credit Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

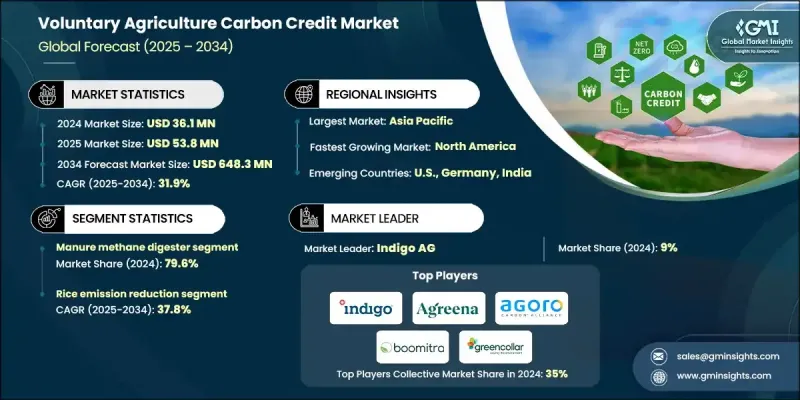

2024 年全球自愿性农业碳信用市场价值为 3,610 万美元,预计到 2034 年将以 31.9% 的复合年增长率增长至 6.483 亿美元。

企业净零排放承诺的激增推动了市场成长,因为企业越来越希望抵消其供应链产生的范围3排放。农业碳信用额提供了一种可衡量的方式来展现企业的环境责任,同时支持永续农业实践。从零星购买碳抵销金额到整合永续发展融资的转变,已将碳信用纳入企业投资策略。由企业主导的经核实的农业碳专案进一步创造了巨大的机会。私部门的参与正在重塑市场格局,企业不仅购买碳信用额,还设计和管理自己的专案。强调高品质、经核实的碳信用有助于规范实践并增强买家信心。数位化平台和第三方验证确保了透明度和可追溯性,而简化的註册流程和稳定的收入来源使碳信用专案对农民越来越有吸引力。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 3610万美元 |

| 预测值 | 6.483亿美元 |

| 复合年增长率 | 31.9% |

2024年,粪便甲烷消化器市占率达到79.6%,预计到2034年将以30.6%的复合年增长率成长。成长的主要驱动力是可再生天然气生产方式的转变,以及与营养物回收和共消化製程的融合。甲烷捕集和转化为燃料的强劲市场诱因进一步加速了这些项目在全球的推广应用。

预计到2034年,水稻减量措施将以37.8%的速度成长,这主要得益于交替干湿灌溉方式的推广以及经核证碳信用计画的扩展。透过在生长季期间控制排水期,农民可以显着降低水稻田的甲烷排放量。这些项目通常整合了高效施肥和永续灌溉技术等措施,从而增强土壤固碳能力并减少一氧化二氮排放,进而扩大碳信用的产生范围。

2024年,美国自愿性农业碳信用市场创造了690万美元的收入。该国的企业气候倡议正将碳信用从可选的抵销手段转变为策略性金融工具。企业正将农业碳信用纳入资本配置和永续发展挂钩的金融机制,尤其针对范围3排放。这一趋势正在推动美国市场对经核实的高品质碳信用的需求不断增长。

全球自愿性农业碳信用市场的主要参与者包括Agoro Carbon Alliance、AgriCapture、Agreena、Boomitra、Carbon Asset Solutions、CarbonSink、CIBO Technologies、Climate Action Reserve、Cultivo、eAgronom、EverCarbon、Green Carbon Inc.、GreenCollar、Indigo Ag、Landkmate、Phak Ag Private Limited。这些公司正采取多种策略来巩固其市场地位并扩大市场份额。他们大力投资于专案开发和验证系统,以确保高品质、可信赖的信用额度。与农民、技术提供者和企业买家建立策略合作伙伴关係,有助于提高专案的普及率和覆盖范围。各公司正在利用数位化平台和可追溯性工具来提高透明度、简化註册流程,并确保参与者获得稳定的收入。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 监管环境

- 产业影响因素

- 成长驱动因素

- 产业陷阱与挑战

- 成长潜力分析

- 波特的分析

- PESTEL 分析

- 新兴机会与趋势

- 数位化和物联网集成

- 新兴市场渗透

第四章:竞争格局

- 介绍

- 公司市占率分析

- 策略倡议

- 竞争性标竿分析

- 战略仪錶板

- 创新与技术格局

第五章:市场规模及预测:依专案类型划分,2021-2034年

- 主要趋势

- 粪便甲烷消化器

- 水稻减量

- 永续农业

- 改进的灌溉管理

- 其他的

第六章:市场规模及预测:依地区划分,2021-2034年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 瑞士

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 台湾

- 世界其他地区

第七章:公司简介

- AgriCapture

- Agoro Carbon Alliance

- Agreena

- Boomitra

- Carbon Asset Solutions

- CarbonSink

- CIBO Technologies

- Climate Action Reserve

- Cultivo

- eAgronom

- EverCarbon

- Green Carbon Inc.

- GreenCollar

- Indigo Ag

- Landbanking Group

- Loam Bio

- Nori

- Pachama

- South Pole

- TerraCarbon

- Varaha ClimateAg Private Limited

The Global Voluntary Agriculture Carbon Credit Market was valued at USD 36.1 million in 2024 and is estimated to grow at a CAGR of 31.9% to reach USD 648.3 million by 2034.

The market's growth is driven by the surge in corporate net-zero commitments, as companies increasingly look to offset their Scope 3 emissions originating from their supply chains. Agriculture-based carbon credits provide a measurable way to showcase environmental responsibility while supporting sustainable farming practices. The transition from occasional carbon offset purchases to integrated sustainability financing has embedded carbon credits into corporate investment strategies. Verified agriculture carbon projects led by companies are further creating significant opportunities. Private sector participation is reshaping the landscape, with organizations not only buying credits but also designing and managing their own programs. Emphasizing high-quality, verified credits standardizes practices and builds buyer confidence. Digital platforms and third-party verification ensure transparency and traceability, while streamlined enrollment and consistent revenue streams make carbon credit programs increasingly attractive to farmers.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $36.1 Million |

| Forecast Value | $648.3 Million |

| CAGR | 31.9% |

The manure methane digester segment held 79.6% share in 2024 and is expected to grow at a CAGR of 30.6% through 2034. Growth is driven by the shift toward renewable natural gas production and integration with nutrient recovery and codigestion processes. Strong market incentives for methane capture and conversion into fuel further accelerate the adoption of these projects worldwide.

The rice emission reduction initiatives are anticipated to grow at a rate of 37.8% through 2034, fueled by the adoption of alternate wetting and drying practices combined with the expansion of verified carbon credit programs. By incorporating controlled drainage periods during the growing season, farmers can significantly lower methane emissions from flooded fields. These projects often integrate practices such as efficient fertilizer use and sustainable irrigation techniques, enhancing soil carbon sequestration and reducing nitrous oxide emissions, thereby broadening the scope of carbon credit generation.

U.S. Voluntary Agriculture Carbon Credit Market generated USD 6.9 million in 2024. Corporate climate initiatives in the country are transforming carbon credits from optional offsets into strategic financial instruments. Companies are embedding agriculture-based credits into capital allocation and sustainability-linked financial mechanisms, particularly targeting Scope 3 emissions. This trend is driving heightened demand for verified and high-quality credits in the U.S. market.

Key players in the Global Voluntary Agriculture Carbon Credit Market include Agoro Carbon Alliance, AgriCapture, Agreena, Boomitra, Carbon Asset Solutions, CarbonSink, CIBO Technologies, Climate Action Reserve, Cultivo, eAgronom, EverCarbon, Green Carbon Inc., GreenCollar, Indigo Ag, Landbanking Group, Loam Bio, Nori, Pachama, South Pole, TerraCarbon, and Varaha ClimateAg Private Limited. Companies in the Global Voluntary Agriculture Carbon Credit Market are employing several strategies to strengthen their market presence and expand their foothold. They are investing heavily in project development and verification systems to ensure high-quality, credible credits. Strategic partnerships with farmers, technology providers, and corporate buyers enhance program adoption and reach. Firms are leveraging digital platforms and traceability tools to provide transparency, simplify enrollment, and ensure consistent revenue for participants.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

- 2.1.1 Business trends

- 2.1.2 Project type trends

- 2.1.3 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technology factors

- 3.6.5 Environmental factors

- 3.6.6 Legal factors

- 3.7 Emerging opportunities & trends

- 3.7.1 Digitalization and IoT integration

- 3.7.2 Emerging market penetration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, 2024

- 4.3 Strategic initiatives

- 4.4 Competitive benchmarking

- 4.5 Strategic dashboard

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Project Type, 2021 - 2034 (USD Million, Million Credit)

- 5.1 Key trends

- 5.2 Manure methane digester

- 5.3 Rice emission reduction

- 5.4 Sustainable agriculture

- 5.5 Improved irrigation management

- 5.6 Others

Chapter 6 Market Size and Forecast, By Region, 2021 - 2034 (USD Million, Million Credit)

- 6.1 Key trends

- 6.2 North America

- 6.2.1 U.S.

- 6.2.2 Canada

- 6.3 Europe

- 6.3.1 UK

- 6.3.2 Germany

- 6.3.3 Switzerland

- 6.3.4 Netherlands

- 6.4 Asia Pacific

- 6.4.1 China

- 6.4.2 Japan

- 6.4.3 India

- 6.4.4 Taiwan

- 6.5 Rest of World

Chapter 7 Company Profiles

- 7.1 AgriCapture

- 7.2 Agoro Carbon Alliance

- 7.3 Agreena

- 7.4 Boomitra

- 7.5 Carbon Asset Solutions

- 7.6 CarbonSink

- 7.7 CIBO Technologies

- 7.8 Climate Action Reserve

- 7.9 Cultivo

- 7.10 eAgronom

- 7.11 EverCarbon

- 7.12 Green Carbon Inc.

- 7.13 GreenCollar

- 7.14 Indigo Ag

- 7.15 Landbanking Group

- 7.16 Loam Bio

- 7.17 Nori

- 7.18 Pachama

- 7.19 South Pole

- 7.20 TerraCarbon

- 7.21 Varaha ClimateAg Private Limited

2026-2030年全球排碳权市场

2026-2030年全球排碳权市场 智慧碳交易平台市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户、解决方案和模式划分

智慧碳交易平台市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户、解决方案和模式划分 全球排碳权检验、验证和认证市场(按类型、应用和地区划分)-预测至2030年

全球排碳权检验、验证和认证市场(按类型、应用和地区划分)-预测至2030年 日本排碳权市场规模、份额、趋势及预测(按类型、计划类型、最终用途行业和地区划分,2026-2034年)

日本排碳权市场规模、份额、趋势及预测(按类型、计划类型、最终用途行业和地区划分,2026-2034年) 排碳权市场机会、成长要素、产业趋势分析及2026年至2035年预测

排碳权市场机会、成长要素、产业趋势分析及2026年至2035年预测 农业碳封存市场-全球产业规模、份额、趋势、机会、预测:按原料、应用、地区和竞争对手划分,2021-2031年

农业碳封存市场-全球产业规模、份额、趋势、机会、预测:按原料、应用、地区和竞争对手划分,2021-2031年 全球碳农业和农业排碳权市场预测至2032年:按类型、排碳权类型、机制、部署模式、最终用户和地区划分

全球碳农业和农业排碳权市场预测至2032年:按类型、排碳权类型、机制、部署模式、最终用户和地区划分 排碳权市场规模、份额和趋势分析报告:按类型、计划类型、最终用途、地区和细分市场预测(2026-2033 年)

排碳权市场规模、份额和趋势分析报告:按类型、计划类型、最终用途、地区和细分市场预测(2026-2033 年) 排碳权市场规模、份额和成长分析(按类型、计划类型、最终用途和地区划分)-2026-2033年产业预测

排碳权市场规模、份额和成长分析(按类型、计划类型、最终用途和地区划分)-2026-2033年产业预测 全球排碳权市场机会与策略(至2034年)

全球排碳权市场机会与策略(至2034年)