|

市场调查报告书

商品编码

1876621

电动汽车电池管理晶片市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Electric Vehicle Battery Management Chips Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

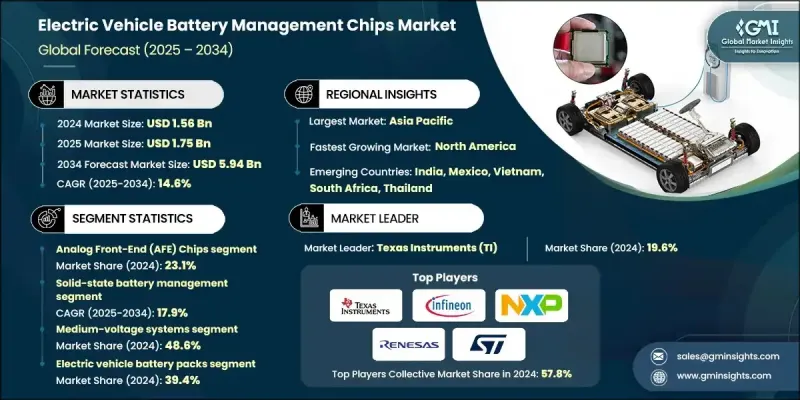

2024 年全球电动车电池管理晶片市场价值为 15.6 亿美元,预计到 2034 年将以 14.6% 的复合年增长率增长至 59.4 亿美元。

随着製造商寻求降低过热、短路和过充等风险,对电池安全性的日益重视持续推动着市场对电池管理晶片的需求。这些晶片持续监测电池组内的电芯状态,确保可靠的性能和运作安全。随着全球安全标准日益严格,汽车公司正大力投资研发新一代管理晶片,以增强保护性能、延长电池寿命并提升消费者信心。除了安全性的提升,受环保理念、政府激励措施和减排指令的推动,电动车需求的快速成长仍然是市场发展的关键催化剂。电池管理晶片在优化电源效率、调节充电週期和预防故障方面发挥着至关重要的作用。先进监控功能和预测性维护系统的集成,正将电池管理转变为高度数据驱动的过程。随着连网汽车和自动驾驶汽车的兴起,製造商正专注于能够提供增强通讯、能量优化和诊断功能的晶片。安全性、效率和数位化这三者的融合,必将推动市场在预测期内持续扩张。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 15.6亿美元 |

| 预测值 | 59.4亿美元 |

| 复合年增长率 | 14.6% |

2024年,类比前端(AFE)晶片市占率为23.1%,预计2034年将以13.4%的复合年增长率成长。 AFE晶片作为电池单元和数位控制器之间的关键接口,能够将电压和温度等类比讯号精确转换为数位资料,从而实现精确的监控和控制。现代AFE组件需要极高的测量精度,以确保在各种电压范围和快速测量视窗内都能达到最佳性能和稳定性。

2025年至2034年,固态电池管理领域将以17.9%的复合年增长率成长。固态电池系统采用不易燃的固体电解质代替液态电解质,在安全性、能量密度、循环寿命和耐温性方面均有显着提升。这些电池的能量密度可超过400 Wh/kg,并拥有更长的使用寿命,因此需要能够处理其独特电气特性的精密电池管理晶片。

预计到2024年,美国电动车电池管理晶片市场份额将达到87.4%。联邦政府的支持性政策、税收优惠以及旨在促进国内生产的各项倡议,显着增强了美国的电动车生态系统。推动清洁能源和製造业创新的立法措施持续推动本地晶片研发,从而降低潜在的供应链中断风险。美国製造商正将人工智慧和预测分析技术整合到电池管理系统中,以提高电池性能、增强即时监控并延长电池寿命,这进一步推动了产业转型为智慧能源系统。

全球电动车电池管理晶片市场的主要参与者包括意法半导体(ST)、恩智浦半导体(NXP Semiconductors)、德州仪器(TI)、微芯科技(Microchip Technology)、英飞凌科技(Infineon Technologies)、ABLIC Inc.、罗姆株式会社(Rohm Co. Ltd)、日清纺电子(Recess)。这些领导企业正致力于产品创新、合作和策略扩张,以巩固其市场地位。各公司正加大研发投入,设计高效率、低功耗的晶片,以提升能源管理水准并提高安全标准。与汽车OEM厂商和电池生产商的合作,使得下一代电动车的客製化晶片整合成为可能。许多企业正在采用人工智慧驱动的监控解决方案,以实现预测性诊断和即时优化。拓展区域製造中心和供应链垂直整合是确保可靠性和成本效益的关键策略。永续性和智慧能源管理是企业旨在增强竞争力并支持全球向电动出行转型的重要倡议。

目录

第一章:方法论

- 市场范围和定义

- 研究设计

- 研究方法

- 资料收集方法

- 资料探勘来源

- 全球的

- 地区/国家

- 基准估算和计算

- 基准年计算

- 市场估算的关键趋势

- 初步研究和验证

- 原始资料

- 预报

- 研究假设和局限性

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 价值链分析与产业结构

- 原料与晶圆製造

- BMS IC设计与开发

- 半导体製造与测试

- BMS模组组装与集成

- 电池组整合与验证

- OEM车辆整合与部署

- 售后市场及服务生态系统

- 报废回收与永续性

- 价值链分析与产业结构

- 供应商格局

- 原物料供应商

- 零件製造商

- 电池製造商

- 系统整合商

- OEM

- 最终用途

- 产业影响因素

- 成长驱动因素

- 电动车市场蓬勃发展

- 电池安全与监管要求

- 能量密度与效能优化需求

- 快速充电基础设施建设

- 电网储能市场成长

- 产业陷阱与挑战

- 高昂的开发和资格认证成本

- 复杂的多细胞监测挑战

- 市场机会

- 固态电池技术集成

- 无线电池管理系统

- 人工智慧增强型电池优化

- 二次电池应用

- 成长驱动因素

- 成长潜力分析

- 监管环境

- 波特的分析

- PESTEL 分析

- 技术与创新格局

- 目前技术

- 新兴技术

- 专利分析

- 价格趋势分析

- 副产品

- 按地区

- 成本分解分析

- 生产统计数据

- 生产中心

- 消费中心

- 进出口

- 永续性和环境方面

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

- 市场成熟度与采纳度分析

- 技术准备程度评估

- 区域采用成熟度比较

- 应用领域成熟度分析

- 生产准备度和规模评估

- 商业部署时程

- 总拥有成本 (TCO) 分析

- BMS晶片组件成本

- 系统整合与开发费用

- 汽车认证和测试成本

- 製造和部署费用

- 维护和更换生命週期成本

- 按技术类型分類的总拥有成本比较

- 整合复杂性与实施挑战

- 多单元架构设计挑战

- 高压隔离和安全要求

- 通讯协定集成

- 热管理与散热

- 软体整合与演算法开发

- 製造流程及品质控制分析

- 半导体製造及良率优化

- 汽车级测试与认证

- 品质保证与可靠性测试

- 供应链管理与采购

- 成本降低与流程优化

- 安全与功能安全框架分析

- ISO 26262 ASIL 合规性要求

- 电池安全标准与法规

- 失效模式分析与预防

- 冗余与容错设计

- 网路安全与资料保护

第四章:竞争格局

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 重要新闻和倡议

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划和资金

第五章:市场估计与预测:依技术划分,2021-2034年

- 主要趋势

- 模拟前端 (AFE) 晶片

- 细胞监测积体电路

- 电池平衡电路

- 保护积体电路

- 电池管理控制器

- 电流检测积体电路

第六章:市场估计与预测:依电池类型划分,2021-2034年

- 主要趋势

- 锂离子电池管理

- 磷酸铁锂管理

- 固态电池管理

- 镍氢化物管理

- 高级化学支持

第七章:市场估算与预测:依电压范围划分,2021-2034年

- 主要趋势

- 低电压系统

- 中压系统

- 高压系统

- 超高压系统

第八章:市场估算与预测:以一体化程度划分,2021-2034年

- 主要趋势

- 离散元件

- 整合解决方案

- 系统单晶片 (SoC)

- 模组化系统

第九章:市场估计与预测:依应用领域划分,2021-2034年

- 主要趋势

- 电动车电池组

- 油电混合车系统

- 储能係统

- 充电基础设施

- 辅助电池系统

- 手提储能

第十章:市场估价与预测:依车辆类型划分,2021-2034年

- 主要趋势

- 乘用电动车

- 纯电动车

- 插电式混合动力汽车

- 燃料电池电动车

- 商用电动车

- 范斯

- 纯电动车

- 插电式混合动力汽车

- 公车

- 纯电动车

- 燃料电池电动车

- 卡车

- 纯电动车

- 燃料电池电动车

- 范斯

第十一章:市场估计与预测:按地区划分,2021-2034年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 北欧

- 荷兰

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 新加坡

- 越南

- 印尼

- 拉丁美洲

- 巴西

- 哥伦比亚

- 哥斯大黎加

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙乌地阿拉伯

- 阿联酋

第十二章:公司简介

- 全球参与者

- Texas Instruments Incorporated

- Analog Devices

- Infineon Technologies

- NXP Semiconductors

- STMicroelectronics

- Renesas Electronics

- Maxim Integrated Products (Analog Devices)

- ON Semiconductor Corporation

- Microchip Technology

- Regional Champions

- Tesla

- General Motors

- Ford Motor

- BYD

- Contemporary Amperex Technology (CATL)

- LG

- Panasonic

- Samsung

- 新兴参与者和专家

- Monolithic Power Systems

- Linear Technology (Analog Devices)

- Intersil Corporation (Renesas)

- Richtek Technology Corporation

- Diodes Incorporated

- ROHM Semiconductor

- Cypress Semiconductor (Infineon)

- Semtech Corporation

The Global Electric Vehicle Battery Management Chips Market was valued at USD 1.56 billion in 2024 and is estimated to grow at a CAGR of 14.6% to reach USD 5.94 billion by 2034.

Growing emphasis on battery safety continues to fuel market adoption as manufacturers seek to reduce the risks associated with overheating, short-circuiting, and overcharging. These chips continuously monitor cell conditions within the battery pack, ensuring reliable performance and operational safety. As global safety standards become increasingly strict, automotive companies are investing heavily in next-generation management chips to enhance protection, extend battery life, and boost consumer confidence. In addition to safety improvements, the rapid surge in electric vehicle demand-driven by environmental priorities, government incentives, and emission reduction mandates-remains a crucial market catalyst. Battery management chips play a vital role in optimizing power efficiency, regulating charge cycles, and preventing failures. The integration of advanced monitoring capabilities and predictive maintenance systems is transforming battery management into a highly data-driven process. With the rise of connected and autonomous vehicles, manufacturers are focusing on chips that can deliver enhanced communication, energy optimization, and diagnostic features. This convergence of safety, efficiency, and digitalization is set to propel sustained market expansion throughout the forecast period.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.56 Billion |

| Forecast Value | $5.94 Billion |

| CAGR | 14.6% |

The Analog Front-End (AFE) chips segment held a 23.1% share in 2024 and is expected to witness a CAGR of 13.4% through 2034. AFE chips serve as critical interfaces between battery cells and the digital controller, accurately converting analog signals such as voltage and temperature into digital data for precise monitoring and control. Modern AFE components demand high measurement accuracy, ensuring optimal performance and stability across voltage ranges and rapid measurement windows.

The solid-state battery management segment will grow at a CAGR of 17.9% from 2025 to 2034. Solid-state battery systems utilize non-flammable solid electrolytes instead of liquid ones, offering significant improvements in safety, energy density, cycle life, and temperature tolerance. These batteries can achieve energy densities exceeding 400 Wh/kg and provide longer operational lifespans, driving the need for sophisticated battery management chips capable of handling their unique electrical characteristics.

United States Electric Vehicle Battery Management Chips Market held an 87.4% share in 2024. Supportive federal policies, tax incentives, and initiatives aimed at advancing domestic production have significantly strengthened the country's EV ecosystem. Legislative measures promoting clean energy and manufacturing innovation continue to bolster local chip development, mitigating potential supply chain disruptions. U.S. manufacturers are integrating artificial intelligence and predictive analytics into their battery management systems to improve performance, enhance real-time monitoring, and extend the overall lifespan of batteries, which further supports the industry's evolution toward intelligent energy systems.

Major companies operating in the Global Electric Vehicle Battery Management Chips Market include STMicroelectronics (ST), NXP Semiconductors, Texas Instruments (TI), Microchip Technology, Infineon Technologies, ABLIC Inc., Rohm Co. Ltd, Nisshinbo Micro Devices, and Renesas Electronics. Leading companies in the Electric Vehicle Battery Management Chips Market are focusing on product innovation, collaboration, and strategic expansion to reinforce their market presence. Firms are investing in research and development to design high-efficiency, low-power chips that enhance energy management and improve safety standards. Partnerships with automotive OEMs and battery producers are enabling customized chip integration for next-generation electric vehicles. Many players are adopting AI-powered monitoring solutions to enable predictive diagnostics and real-time optimization. Expansion into regional manufacturing hubs and vertical integration within the supply chain are key strategies to ensure reliability and cost efficiency. Sustainability and smart energy management are central to corporate initiatives aimed at strengthening competitiveness and supporting the global transition toward electrified mobility.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Technology

- 2.2.2 Battery

- 2.2.3 Voltage range

- 2.2.4 Integration level

- 2.2.5 Application

- 2.2.6 Vehicle

- 2.2.7 Regional

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Value Chain Analysis & Industry Structure

- 3.1.1.1 Raw Materials & Wafer Fabrication

- 3.1.1.2 BMS IC Design & Development

- 3.1.1.3 Semiconductor Manufacturing & Testing

- 3.1.1.4 BMS Module Assembly & Integration

- 3.1.1.5 Battery Pack Integration & Validation

- 3.1.1.6 OEM Vehicle Integration & Deployment

- 3.1.1.7 Aftermarket & Service Ecosystem

- 3.1.1.8 End-of-Life Recycling & Sustainability

- 3.1.1 Value Chain Analysis & Industry Structure

- 3.2 Supplier landscape

- 3.2.1 Raw material suppliers

- 3.2.2 Component manufacturers

- 3.2.3 Battery manufacturers

- 3.2.4 System integrators

- 3.2.5 OEM

- 3.2.6 End use

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Electric Vehicle Market Proliferation

- 3.3.1.2 Battery Safety & Regulatory Requirements

- 3.3.1.3 Energy Density & Performance Optimization Demand

- 3.3.1.4 Fast Charging Infrastructure Development

- 3.3.1.5 Grid Energy Storage Market Growth

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 High Development & Qualification Costs

- 3.3.2.2 Complex Multi-Cell Monitoring Challenges

- 3.3.3 Market opportunities

- 3.3.3.1 Solid-State Battery Technology Integration

- 3.3.3.2 Wireless Battery Management Systems

- 3.3.3.3 AI-Enhanced Battery Optimization

- 3.3.3.4 Second-Life Battery Applications

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.2 Europe

- 3.5.3 Asia Pacific

- 3.5.4 Latin America

- 3.5.5 Middle East and Africa

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Technology and Innovation landscape

- 3.8.1 Current technology

- 3.8.2 Emerging technology

- 3.9 Patent analysis

- 3.10 Price Trends Analysis

- 3.10.1 By product

- 3.10.2 By region

- 3.11 Cost Breakdown Analysis

- 3.12 Production staistics

- 3.12.1 Production hubs

- 3.12.2 Consumption hubs

- 3.12.3 Export and import

- 3.13 Sustainability and Environmental Aspects

- 3.13.1 Sustainable Practices

- 3.13.2 Waste Reduction Strategies

- 3.13.3 Energy Efficiency in Production

- 3.13.4 Eco-friendly Initiatives

- 3.13.5 Carbon Footprint Considerations

- 3.14 Market Maturity & Adoption Analysis

- 3.14.1 Technology Readiness Level Assessment

- 3.14.2 Regional Adoption Maturity Comparison

- 3.14.3 Application Domain Maturity Analysis

- 3.14.4 Manufacturing Readiness & Scale Assessment

- 3.14.5 Commercial Deployment Timeline

- 3.15 Total Cost of Ownership (TCO) Analysis

- 3.15.1 BMS Chip Component Costs

- 3.15.2 System Integration & Development Expenses

- 3.15.3 Automotive Qualification & Testing Costs

- 3.15.4 Manufacturing & Deployment Expenses

- 3.15.5 Maintenance & Replacement Lifecycle Costs

- 3.15.6 TCO Comparison by Technology Type

- 3.16 Integration Complexity & Implementation Challenges

- 3.16.1 Multi-Cell Architecture Design Challenges

- 3.16.2 High-Voltage Isolation & Safety Requirements

- 3.16.3 Communication Protocol Integration

- 3.16.4 Thermal Management & Heat Dissipation

- 3.16.5 Software Integration & Algorithm Development

- 3.17 Manufacturing Process & Quality Control Analysis

- 3.17.1 Semiconductor Fabrication & Yield Optimization

- 3.17.2 Automotive-Grade Testing & Qualification

- 3.17.3 Quality Assurance & Reliability Testing

- 3.17.4 Supply Chain Management & Sourcing

- 3.17.5 Cost Reduction & Process Optimization

- 3.18 Safety & Functional Safety Framework Analysis

- 3.18.1 ISO 26262 ASIL Compliance Requirements

- 3.18.2 Battery Safety Standards & Regulations

- 3.18.3 Failure Mode Analysis & Prevention

- 3.18.4 Redundancy & Fault Tolerance Design

- 3.18.5 Cybersecurity & Data Protection

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key news and initiatives

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Analog Front-End (AFE) chips

- 5.3 Cell Monitoring ICs

- 5.4 Battery balancing circuits

- 5.5 Protection ICs

- 5.6 Battery management controllers

- 5.7 Current sensing ICs

Chapter 6 Market Estimates & Forecast, By Battery, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Lithium-ion battery management

- 6.3 Lithium iron phosphate management

- 6.4 Solid-state battery management

- 6.5 Nickel-metal hydride management

- 6.6 Advanced chemistry support

Chapter 7 Market Estimates & Forecast, By Voltage Range, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Low-voltage system

- 7.3 Medium-voltage system

- 7.4 High-voltage system

- 7.5 Ultra-high voltage system

Chapter 8 Market Estimates & Forecast, By Integration level, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Discrete component

- 8.3 Integrated solution

- 8.4 System-on-Chip (SoC)

- 8.5 Modular system

Chapter 9 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 Electric vehicle battery packs

- 9.3 Hybrid electric vehicle systems

- 9.4 Energy storage systems

- 9.5 Charging infrastructure

- 9.6 Auxiliary battery systems

- 9.7 Portable energy storage

Chapter 10 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 Passenger EVs

- 10.2.1 BEV

- 10.2.2 PHEV

- 10.2.3 FCEV

- 10.3 Commercial EV

- 10.3.1 Vans

- 10.3.1.1 BEV

- 10.3.1.2 PHEV

- 10.3.2 Buses

- 10.3.2.1 BEV

- 10.3.2.2 FCEV

- 10.3.3 Trucks

- 10.3.3.1 BEV

- 10.3.3.2 FCEV

- 10.3.1 Vans

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Nordics

- 11.3.7 Netherlands

- 11.3.8 Russia

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Singapore

- 11.4.7 Vietnam

- 11.4.8 Indonesia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Colombia

- 11.5.3 Costa Rica

- 11.5.4 Mexico

- 11.5.5 Argentina

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global Players

- 12.1.1 Texas Instruments Incorporated

- 12.1.2 Analog Devices

- 12.1.3 Infineon Technologies

- 12.1.4 NXP Semiconductors

- 12.1.5 STMicroelectronics

- 12.1.6 Renesas Electronics

- 12.1.7 Maxim Integrated Products (Analog Devices)

- 12.1.8 ON Semiconductor Corporation

- 12.1.9 Microchip Technology

- 12.2 Regional Champions

- 12.2.1 Tesla

- 12.2.2 General Motors

- 12.2.3 Ford Motor

- 12.2.4 BYD

- 12.2.5 Contemporary Amperex Technology (CATL)

- 12.2.6 LG

- 12.2.7 Panasonic

- 12.2.8 Samsung

- 12.3 Emerging Players & Specialists

- 12.3.1 Monolithic Power Systems

- 12.3.2 Linear Technology (Analog Devices)

- 12.3.3 Intersil Corporation (Renesas)

- 12.3.4 Richtek Technology Corporation

- 12.3.5 Diodes Incorporated

- 12.3.6 ROHM Semiconductor

- 12.3.7 Cypress Semiconductor (Infineon)

- 12.3.8 Semtech Corporation

电动汽车电池管理系统市场规模、占有率、成长及全球产业分析:依类型、应用和地区划分的洞察与预测(2026-2034)

电动汽车电池管理系统市场规模、占有率、成长及全球产业分析:依类型、应用和地区划分的洞察与预测(2026-2034) 全球电池性能保障市场报告(2026 年)

全球电池性能保障市场报告(2026 年) 商用车电池管理系统市场 - 全球产业规模、份额、趋势、机会及预测(按电池类型、车辆类型、类型、地区和竞争格局划分),2021-2031年电动车电池管理市场 - 全球产业规模、份额、趋势、机会及预测(按组件、动力类型、车辆类型、地区和竞争格局划分,2021-2031年)

商用车电池管理系统市场 - 全球产业规模、份额、趋势、机会及预测(按电池类型、车辆类型、类型、地区和竞争格局划分),2021-2031年电动车电池管理市场 - 全球产业规模、份额、趋势、机会及预测(按组件、动力类型、车辆类型、地区和竞争格局划分,2021-2031年) 电动车电池管理系统(BMS)讯号变压器市场按车辆类型、额定电压、拓朴结构、相数、应用和最终用途划分-2026-2032年全球预测铅酸电池充电管理晶片市场:按充电方式、稳压器类型、电压范围、应用和分销管道分類的全球预测(2026-2032年)

电动车电池管理系统(BMS)讯号变压器市场按车辆类型、额定电压、拓朴结构、相数、应用和最终用途划分-2026-2032年全球预测铅酸电池充电管理晶片市场:按充电方式、稳压器类型、电压范围、应用和分销管道分類的全球预测(2026-2032年) 电动汽车电池管理系统:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

电动汽车电池管理系统:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 电动车电池自动化市场预测至2032年:按组件、工艺、电池类型、应用、最终用户和地区分類的全球分析2032 年电动车电池回收再利用市场预测:按电池化学成分、回收流程、应用、最终用户和地区进行的全球分析

电动车电池自动化市场预测至2032年:按组件、工艺、电池类型、应用、最终用户和地区分類的全球分析2032 年电动车电池回收再利用市场预测:按电池化学成分、回收流程、应用、最终用户和地区进行的全球分析 全球电动汽车电池测试市场

全球电动汽车电池测试市场