|

市场调查报告书

商品编码

1876801

资料中心冷却市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Data Center Cooling Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

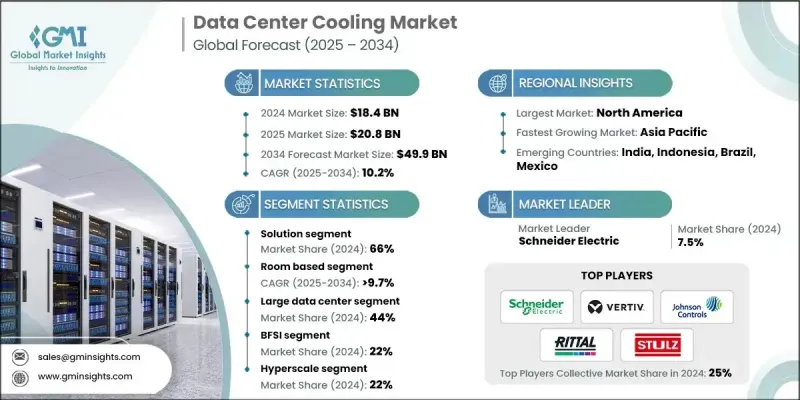

2024 年全球资料中心冷却市场价值为 184 亿美元,预计到 2034 年将以 10.2% 的复合年增长率成长至 499 亿美元。

人工智慧和高效能运算 (HPC) 工作负载的不断增长,正推动着散热方式从传统的风冷转变为先进的液冷解决方案。晶片级直接冷却和浸没式冷却技术正日益应用于 50 至 120 kW 的机架功率密度,使现代资料中心能够应对最新的运算基础设施。边缘资料中心运作于各种不同的环境中,需要灵活的散热管理来确保在紧凑和偏远空间中的可靠性。随着机架功率密度几乎翻倍,从 5 kW 成长到 8-10 kW,传统的风冷系统无法满足需求,促使超大规模资料中心和企业级设施采用液冷解决方案。晶片级直接液冷正成为一种首选方法,它能够确保高功率 CPU 和 GPU 的温度稳定,同时降低能耗并提高系统可靠性。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 184亿美元 |

| 预测值 | 499亿美元 |

| 复合年增长率 | 10.2% |

解决方案领域在 2024 年占据了 66% 的市场份额,预计到 2034 年将以 10.4% 的复合年增长率成长。这一增长得益于对能够支援高密度 AI 和 HPC 工作负载的下一代液冷系统的投资,从而推动了基础设施支出和先进散热管理技术的采用。

2024年,房间冷冻市场占据76.4%的市场份额,预计到2034年将以9.7%的复合年增长率成长。现代房间冷却系统整合了人工智慧辅助优化、变速风扇和密闭解决方案,可实现即时气流调节并提高能源效率。这些创新延长了系统使用寿命,并提高了整体永续性和可靠性。

2024 年,美国资料中心冷却市场占 89% 的份额,创造了 63 亿美元的收入。人工智慧工作负载带来的不断上升的热密度加速了液冷和浸没式冷却的普及,营运商正在升级设施以应对超过 80 kW 的机架密度,尤其是在大型园区环境中。

资料中心冷却市场的主要参与者包括艾默生网路能源、江森自控、Vertiv、施耐德电气、Motivair、Stulz、Degree Controls、Rittal、Airedale International 和 Coolcentric。这些公司正采取多种策略来巩固其市场地位。他们加大研发投入,开发能够应对极端热密度的高效能液体冷却和浸没式冷却技术。与超大规模和企业级资料中心营运商建立合作关係,有助于推广先进冷却解决方案的应用。此外,各公司也持续改进以人工智慧为基础的即时能源管理优化工具。策略性併购则有助于企业拓展技术组合和地理覆盖范围。

目录

第一章:方法论

- 市场范围和定义

- 研究设计

- 研究方法

- 资料收集方法

- 资料探勘来源

- 全球的

- 地区/国家

- 基准估算和计算

- 基准年计算

- 市场估算的关键趋势

- 初步研究和验证

- 原始资料

- 预测模型

- 研究假设和局限性

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 利润率分析

- 成本结构

- 每个阶段的价值增加

- 影响价值链的因素

- 中断

- 产业影响因素

- 成长驱动因素

- 日益增长的高密度人工智慧和高效能运算工作负载部署

- 人们越来越关注永续性和能源效率

- 新兴地区资料中心容量扩张不断成长

- DCIM与基于AI的冷却优化集成

- 产业陷阱与挑战

- 前期成本高和改造挑战

- 液冷基础设施管理的复杂性

- 日益严格的冷媒环境法规

- 市场机会

- 亚太和中东非地区超大规模和託管设施的成长

- 整合人工智慧驱动的热管理

- 转向模组化、预製资料中心

- 成长驱动因素

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 南美洲

- 中东和非洲

- 波特的分析

- PESTEL 分析

- 技术与创新格局

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 副产品

- 成本細項分析

- 专利分析

- 永续性和环境方面

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

- 市场成熟度与采纳度分析

- 未来趋势与市场动盪

- 人工智慧在冷却系统的应用

- 量子计算冷却需求

- 永续和绿色冷冻技术

- 模组化和预製冷却解决方案

- 废热回收再利用系统

- 先进材料与奈米技术

- 自主冷却系统管理

- 区块链和分散式计算的影响

- 6G基础设施冷却需求

- 资料中心冷却市场动态及差距分析

- 功率密度趋势和冷却需求

- 冷却技术迁移模式

- 市场差距分析

- 能源效率和永续性势在必行

- 资料中心机械系统演化

- 策略研发与市场契合框架

- 暖通空调公司的研发投资重点

- 市场协调策略和框架

- 进阶解决方案开发路径

- 伙伴关係和生态系统发展

- 实施路线图

- 投资分析与市场机会

- 投资环境概览

- 创投与私募股权活动

- 策略投资机会

- 市场进入策略

- 技术授权机会

- 地理扩张策略

- 投资报酬分析

- 未来投资趋势

- 电源使用效率 (PUE) 趋势与分析

- PUE简介及其重要性

- 按资料中心类型分類的平均 PUE 基准测试

- 冷却技术对PUE的影响

- PUE优化策略与人工智慧驱动的控制

- PUE 标准的区域和监管影响

第四章:竞争格局

- 介绍

- 公司市占率分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划和资金

第五章:市场估算与预测:依组件划分,2021-2034年

- 主要趋势

- 解决方案

- 空调

- 空气处理机组

- 分离式空调系统

- 一体式空调机组(PAC)

- 其他的

- 冷却单元

- 空冷式冷水机

- 水冷式冷水机

- 乙二醇冷却式冰水机

- 冷却水塔

- 蒸发冷却

- 干燥

- 其他的

- 控制系统

- 经济器系统

- 冷凝

- 非冷凝式

- 液冷系统

- 直接连接到晶片

- 沉浸式

- 单相

- 两相

- 其他的

- 空调

- 服务

- 咨询

- 维护和支援

- 安装和部署

第六章:市场估算与预测:依冷冻技术划分,2021-2034年

- 主要趋势

- 基于货架/行

- 房间

第七章:市场估算与预测:依资料中心规模划分,2021-2034年

- 主要趋势

- 小型资料中心

- 中型资料中心

- 大型资料中心

第八章:市场估算与预测:依应用领域划分,2021-2034年

- 主要趋势

- 金融服务业

- 託管

- 活力

- 政府

- 卫生保健

- 製造业

- 资讯科技与电信

- 其他的

第九章:市场估算与预测:依资料中心划分,2021-2034年

- 主要趋势

- 超大规模

- 託管

- 企业

- 边缘

- 云

第十章:市场估计与预测:依地区划分,2021-2034年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 北欧

- 波兰

- 比荷卢经济联盟

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 东南亚

- 汶莱

- 柬埔寨

- 印尼

- 寮国

- 马来西亚

- 缅甸

- 菲律宾

- 新加坡

- 泰国

- 东帝汶

- 越南

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 智利

- MEA

- 南非

- 沙乌地阿拉伯

- 阿联酋

第十一章:公司简介

- 全球参与者

- Carrier Global

- Daikin Industries

- Emerson Electric

- Honeywell International

- Johnson Controls

- Mitsubishi

- Schneider Electric

- Siemens

- Trane Technologies

- Vertiv

- 区域玩家

- Airedale International

- Asetek

- Coolcentric

- CoolIT Systems

- Green Revolution Cooling (GRC)

- LiquidStack

- Motivair

- Rittal

- STULZ

- Submer Technologies

- 新兴参与者

- Boyd

- Chilldyne

- ExaScaler

- Hardcore Computer

- Iceotope Technologies

- Kaltra

- Midas Green Technologies

- Phononic

- TMGcore

- ZutaCore

The Global Data Center Cooling Market was valued at USD 18.4 billion in 2024 and is estimated to grow at a CAGR of 10.2% to reach USD 49.9 billion by 2034.

Rising AI and high-performance computing (HPC) workloads are driving a transition from traditional air-based cooling to advanced liquid cooling solutions. Direct-to-chip and immersion cooling technologies are increasingly managing rack densities of 50 to 120 kW, allowing modern data centers to handle the latest compute infrastructure. Edge data centers, operating in varied environments, require flexible thermal management to maintain reliability in compact and remote spaces. With rack power densities nearly doubling from 5 kW to 8-10 kW, conventional air-based systems can no longer meet demand, prompting hyperscale and enterprise facilities to adopt liquid-based solutions. Direct-to-chip liquid cooling is emerging as a preferred method, ensuring stable temperatures for high-wattage CPUs and GPUs while reducing energy consumption and enhancing system reliability.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $18.4 Billion |

| Forecast Value | $49.9 Billion |

| CAGR | 10.2% |

The solutions segment held a 66% share in 2024 and is expected to grow at a CAGR of 10.4% through 2034. This growth is fueled by investments in next-generation liquid cooling systems capable of supporting high-density AI and HPC workloads, driving infrastructure expenditure and advanced heat management adoption.

The room-based cooling segment held a 76.4% share in 2024 and is projected to grow at a CAGR of 9.7% through 2034. Modern room-based systems now integrate AI-assisted optimization, variable-speed fans, and containment solutions, enabling real-time airflow adjustments and energy efficiency improvements. These innovations extend system lifespan and improve overall sustainability and reliability.

U.S. Data Center Cooling Market held a 89% share and generated USD 6.3 billion in 2024. Rising heat densities from AI workloads have accelerated the adoption of liquid and immersion cooling, as operators upgrade facilities to manage rack densities above 80 kW, particularly in large-scale campus environments.

Key players in the Data Center Cooling Market include Emerson Network Power, Johnson Controls, Vertiv, Schneider Electric, Motivair, Stulz, Degree Controls, Rittal, Airedale International, and Coolcentric. Companies in the Data Center Cooling Market are employing multiple strategies to strengthen their market presence. They are investing in R&D to develop high-efficiency liquid and immersion cooling technologies capable of handling extreme heat densities. Partnerships with hyperscale and enterprise data center operators help expand the adoption of advanced cooling solutions. Firms are also enhancing AI-based optimization tools for real-time energy management. Strategic mergers and acquisitions allow players to broaden their technology portfolios and geographic footprint.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Cooling technique

- 2.2.4 Data center size

- 2.2.5 Application

- 2.2.6 Data center

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing deployment of high-density AI and HPC workloads

- 3.2.1.2 Growing focus on sustainability and energy efficiency

- 3.2.1.3 Rising data center capacity expansions in emerging regions

- 3.2.1.4 Integration of DCIM and AI-based cooling optimization

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High upfront cost and retrofit challenges

- 3.2.2.2 Complexity in managing liquid cooling infrastructure

- 3.2.2.3 Rising environmental regulations on refrigerants

- 3.2.3 Market opportunities

- 3.2.3.1 Growth of hyperscale and colocation facilities in APAC and MEA

- 3.2.3.2 Integration of AI-driven thermal management

- 3.2.3.3 Shift toward modular, prefabricated data centers

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 South America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By Products

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

- 3.11.6 Market Maturity & Adoption Analysis

- 3.12 Future trends & market disruptions

- 3.12.1 Artificial intelligence integration in cooling

- 3.12.2 Quantum computing cooling requirements

- 3.12.3 Sustainable & green cooling technologies

- 3.12.4 Modular & prefabricated cooling solutions

- 3.12.5 Waste heat recovery & reuse systems

- 3.12.6 Advanced materials & nanotechnology

- 3.12.7 Autonomous cooling system management

- 3.12.8 Blockchain & distributed computing impact

- 3.12.9. 6 G infrastructure cooling requirements

- 3.13 Data center cooling market dynamics & gap analysis

- 3.13.1 Power density trends and cooling requirements

- 3.13.2 Cooling technology migration patterns

- 3.13.3 Market gap analysis

- 3.13.4 Energy efficiency and sustainability imperatives

- 3.13.5 Mechanical systems evolution in data centers

- 3.14 Strategic R&D & market alignment framework

- 3.14.1 R&D investment priorities for HVAC companies

- 3.14.2 Market alignment strategies and frameworks

- 3.14.3 Advanced solutions development pathway

- 3.14.4 Partnership and ecosystem development

- 3.14.5 Implementation roadmap

- 3.15 Investment analysis & market opportunities

- 3.15.1 Investment landscape overview

- 3.15.2 Venture capital & private equity activity

- 3.15.3 Strategic investment opportunities

- 3.15.4 Market entry strategies

- 3.15.5 Technology licensing opportunities

- 3.15.6 Geographic expansion strategies

- 3.15.7 Investment return analysis

- 3.15.8 Future investment trends

- 3.16 Power Usage Effectiveness (PUE) trends and analysis

- 3.16.1 Introduction to PUE and its importance

- 3.16.2 Average PUE benchmarks by data center type

- 3.16.3 Impact of cooling technologies on PUE

- 3.16.4 PUE optimization strategies and ai-driven controls

- 3.16.5 Regional and regulatory implications for PUE standards

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 South America

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021-2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Solution

- 5.2.1 Air conditioner

- 5.2.1.1 Air handling units

- 5.2.1.2 Split air conditioning systems

- 5.2.1.3 Packaged air conditioning units (PAC)

- 5.2.1.4 Others

- 5.2.2 Chilling unit

- 5.2.2.1 Air-cooled chillers

- 5.2.2.2 Water-cooled chillers

- 5.2.2.3 Glycol-cooled chillers

- 5.2.3 Cooling tower

- 5.2.3.1 Evaporative cooling

- 5.2.3.2 Dry

- 5.2.3.3 Others

- 5.2.4 Control system

- 5.2.4.1 Economizer system

- 5.2.4.2 Condensing

- 5.2.4.3 Non-condensing

- 5.2.5 Liquid cooling system

- 5.2.5.1 Direct to chip

- 5.2.5.2 Immersive

- 5.2.5.2.1 Single phase

- 5.2.5.2.2 Two phase

- 5.2.5.3 Others

- 5.2.1 Air conditioner

- 5.3 Service

- 5.3.1 Consulting

- 5.3.2 Maintenance and support

- 5.3.3 Installation and deployment

Chapter 6 Market Estimates & Forecast, By Cooling Technique, 2021-2034 ($Bn)

- 6.1 Key trends

- 6.2 Rack/row based

- 6.3 Room based

Chapter 7 Market Estimates & Forecast, By Data Center Size, 2021-2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Small data center

- 7.3 Medium data center

- 7.4 Large data center

Chapter 8 Market Estimates & Forecast, By Application, 2021-2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 BFSI

- 8.3 Colocation

- 8.4 Energy

- 8.5 Government

- 8.6 Healthcare

- 8.7 Manufacturing

- 8.8 IT & Telecom

- 8.9 Others

Chapter 9 Market Estimates & Forecast, By Data Center, 2021-2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 Hyperscale

- 9.3 Colocation

- 9.4 Enterprise

- 9.5 Edge

- 9.6 Cloud

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.2.3 Mexico

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.3.8 Poland

- 10.3.9 Benelux

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.4.6.1 Brunei

- 10.4.6.2 Cambodia

- 10.4.6.3 Indonesia

- 10.4.6.4 Laos

- 10.4.6.5 Malaysia

- 10.4.6.6 Myanmar

- 10.4.6.7 Philippines

- 10.4.6.8 Singapore

- 10.4.6.9 Thailand

- 10.4.6.10 Timor-Leste

- 10.4.6.11 Vietnam

- 10.5 South America

- 10.5.1 Brazil

- 10.5.2 Argentina

- 10.5.3 Colombia

- 10.5.4 Chile

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 Carrier Global

- 11.1.2 Daikin Industries

- 11.1.3 Emerson Electric

- 11.1.4 Honeywell International

- 11.1.5 Johnson Controls

- 11.1.6 Mitsubishi

- 11.1.7 Schneider Electric

- 11.1.8 Siemens

- 11.1.9 Trane Technologies

- 11.1.10 Vertiv

- 11.2 Regional Players

- 11.2.1 Airedale International

- 11.2.2 Asetek

- 11.2.3 Coolcentric

- 11.2.4 CoolIT Systems

- 11.2.5 Green Revolution Cooling (GRC)

- 11.2.6 LiquidStack

- 11.2.7 Motivair

- 11.2.8 Rittal

- 11.2.9 STULZ

- 11.2.10 Submer Technologies

- 11.3 Emerging Players

- 11.3.1 Boyd

- 11.3.2 Chilldyne

- 11.3.3 ExaScaler

- 11.3.4 Hardcore Computer

- 11.3.5 Iceotope Technologies

- 11.3.6 Kaltra

- 11.3.7 Midas Green Technologies

- 11.3.8 Phononic

- 11.3.9 TMGcore

- 11.3.10 ZutaCore

英洛冷冻市场:依产品类型、冷冻方式、安装方式、冷气量和最终用户划分-2026-2032年全球预测

英洛冷冻市场:依产品类型、冷冻方式、安装方式、冷气量和最终用户划分-2026-2032年全球预测 资料中心冷却市场分析及预测(至2035年):按类型、产品、服务、技术、组件、应用、部署、最终用户、设备及解决方案划分整合式机架安装单元 (CDU) 市场:按阶段、容量、应用和最终用户分類的全球预测,2026-2032 年资料中心CDU市场:按类型、组件、冷却方式、容量、应用工作负载、最终用途、企业规模、安装方式、分销管道划分,全球预测,2026-2032年

资料中心冷却市场分析及预测(至2035年):按类型、产品、服务、技术、组件、应用、部署、最终用户、设备及解决方案划分整合式机架安装单元 (CDU) 市场:按阶段、容量、应用和最终用户分類的全球预测,2026-2032 年资料中心CDU市场:按类型、组件、冷却方式、容量、应用工作负载、最终用途、企业规模、安装方式、分销管道划分,全球预测,2026-2032年 资料中心冷却市场:依组件、冷却技术、资料中心类型和行业划分 - 全球预测至2036年

资料中心冷却市场:依组件、冷却技术、资料中心类型和行业划分 - 全球预测至2036年 资料中心冷却:市场占有率分析、产业趋势与统计、成长预测(2026-2032)

资料中心冷却:市场占有率分析、产业趋势与统计、成长预测(2026-2032) 全球资料中心冷却市场规模、份额、趋势和成长分析报告(2026-2034年)

全球资料中心冷却市场规模、份额、趋势和成长分析报告(2026-2034年) 节水型资料中心技术市场,全球预测至2034年:依冷却技术、水源、水处理方法、所有权模式及地区划分

节水型资料中心技术市场,全球预测至2034年:依冷却技术、水源、水处理方法、所有权模式及地区划分 2026年全球资料中心冷却市场报告全球资料中心冷却市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的分析以及未来预测(2026-2034)

2026年全球资料中心冷却市场报告全球资料中心冷却市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的分析以及未来预测(2026-2034)