|

市场调查报告书

商品编码

1885806

人工智慧资料中心市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)AI Data Center Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

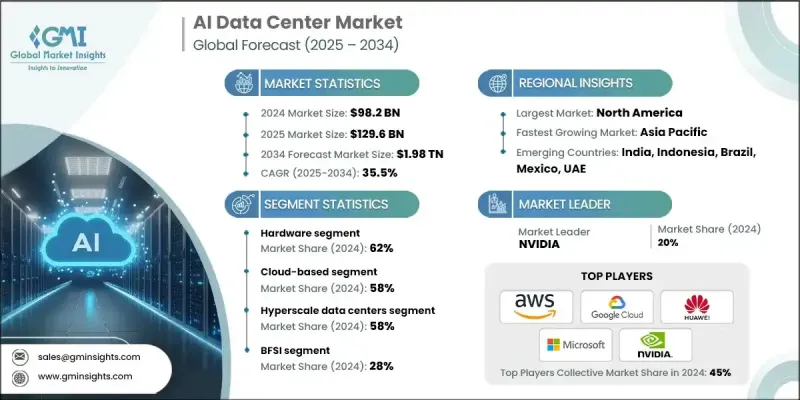

2024 年全球人工智慧资料中心市场价值为 982 亿美元,预计到 2034 年将以 35.5% 的复合年增长率成长至 1.98 兆美元。

生成式人工智慧和机器学习工具的日益普及对处理能力和储存容量提出了极高的要求,因此对专门针对人工智慧工作负载优化的资料中心的依赖性也日益增强。这些环境依赖先进的GPU、可扩展的系统架构和超低延迟网络,以支援金融、医疗保健和零售等行业复杂的模型训练和推理。巨量资料分析也在加速这一需求,因为企业需要处理大量的结构化和非结构化资讯流,必须快速处理这些资讯。专注于人工智慧的设施能够为即时工作负载提供高效能运算,从而巩固其作为全球数位转型关键基础设施的地位。云端运算的快速扩张以及超大规模设施数量的不断增长,持续推动对人工智慧就绪型基础设施的需求。服务供应商正在投资建造先进的人工智慧资料平台,为企业和开发者提供可扩展的服务,进一步增强了市场发展势头。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 982亿美元 |

| 预测值 | 1.98兆美元 |

| 复合年增长率 | 35.5% |

2024年,硬体领域市场规模将达611亿美元。成长主要得益于人工智慧晶片、GPU加速器、先进散热技术、高密度伺服器系统和光网路解决方案的广泛应用。 GPU能耗的不断攀升、机架密度向30-120千瓦的转变,以及领先科技公司推出的大规模部署策略,正在塑造该行业的长期资本配置格局。

2024年,云端运算领域占据了58%的市场份额,预计2025年至2034年将以35.2%的复合年增长率成长。该领域之所以领先,是因为其无与伦比的可扩展性、灵活的消费选项以及无需前期投资即可使用最新的AI加速计算硬体。超大规模服务供应商正投入数十亿美元加强全球AI基础设施建设,从而推动AI驱动型服务的普及,并增加对GPU、TPU和专用处理器的需求。

2024年,美国人工智慧资料中心市场规模预计将达332亿美元。凭藉众多超大规模营运商的支援以及在GPU集群、液冷技术和大规模人工智慧资料中心建设方面的巨额投资,美国在该领域保持领先地位。联邦政府的激励措施、区域税收优惠和基础设施建设资金进一步巩固了美国作为人工智慧运算能力最强地区的地位。

人工智慧资料中心市场的主要参与者包括华为、AWS、英伟达、HPE、Digital Realty、Google、联想、微软、Equinix 和戴尔科技。这些公司正致力于拓展在人工智慧资料中心市场的份额,并专注于基础设施现代化、大规模GPU部署和节能係统设计。许多公司正在投资高密度机架、整合液冷系统和新一代网络,以支援先进的人工智慧工作负载。与晶片製造商、云端服务供应商和託管营运商建立策略合作伙伴关係,有助于加速容量扩张并确保获得尖端人工智慧硬体。服务供应商也正在扩大全球资料中心规模,增强自动化能力,并透过整合再生能源优化电力利用率。与企业签订长期合约、提供人工智慧即服务 (AIaaS) 产品以及建立专用人工智慧集群,进一步巩固了其竞争地位和市场主导地位。

目录

第一章:方法论

- 市场范围和定义

- 研究设计

- 研究方法

- 资料收集方法

- 资料探勘来源

- 全球的

- 地区/国家

- 基准估算和计算

- 基准年计算

- 市场估算的关键趋势

- 初步研究和验证

- 原始资料

- 预测模型

- 研究假设和局限性

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 利润率

- 成本结构

- 每个阶段的价值增加

- 影响价值链的因素

- 中断

- 产业影响因素

- 成长驱动因素

- 采用生成式人工智慧和机器学习

- 巨量资料分析领域的成长

- 云端扩充和超大规模部署

- GPU和晶片技术的进步

- 产业陷阱与挑战

- 高昂的资本和营运成本

- 能源消耗与永续性议题

- 市场机会

- 边缘人工智慧资料中心

- 液冷和绿色技术

- 人工智慧即服务平台

- 新兴市场采用

- 成长驱动因素

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL 分析

- 技术与创新格局

- 当前技术趋势

- GPU 与加速器技术演进

- 液冷技术进步

- 电源分配创新(48V架构、模组化UPS)

- 新兴技术

- 软体定义基础设施

- 边缘运算集成

- 当前技术趋势

- 定价分析

- 託管定价趋势(每千瓦,每机架)

- 云端运算人工智慧运算定价演变

- 能源成本对总拥有成本的影响

- 冷却技术成本比较

- 成本細項分析

- 专利分析

- 冷却技术专利

- 人工智慧晶片架构专利

- 电源管理创新

- 资料中心设计专利

- 永续性和环境方面

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

- 用例

- 最佳情况

- 互联互通及网路基础设施分析

- 资料中心互连架构

- 高速织物要求

- 超大规模企业对海底电缆的投资

- 互联网交换点邻近性与对等互联

- 各区域的光纤回程可用性

- 5G与边缘网路集成

- 软体定义网路采用

- 投资与融资分析

- 超大规模资本支出趋势

- 私募股权和基础设施基金活动

- 政府投资计划

- 人工智慧基础设施新创企业的创投

第四章:竞争格局

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划和资金

- 新增产能及场地公告

- 供应商选择标准

- 产品和服务基准测试

第五章:市场估算与预测:依组件划分,2021-2034年

- 主要趋势

- 硬体

- 伺服器

- GPU

- 贮存

- 网路装置

- 软体

- 人工智慧框架

- 编排工具

- 管理平台

- 服务

- 专业服务

- 部署与集成

- 咨询

- 支援与维护

- 託管服务

- 专业服务

第六章:市场估算与预测:依部署模式划分,2021-2034年

- 主要趋势

- 基于云端的

- 现场

- 杂交种

第七章:市场估算与预测:依资料中心划分,2021-2034年

- 主要趋势

- 超大规模资料中心

- 企业资料中心

- 託管资料中心

- 边缘资料中心

第八章:市场估算与预测:依产业垂直领域划分,2021-2034年

- 主要趋势

- 金融服务业

- 政府

- 卫生保健

- 资讯科技与电信

- 汽车

- 媒体与娱乐

- 其他的

第九章:市场估计与预测:依地区划分,2021-2034年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 北欧

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳新银行

- 越南

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙乌地阿拉伯

- 阿联酋

第十章:公司简介

- Global companies

- AWS

- Dell Technologies

- Digital Realty

- Equinix

- Google Cloud

- HPE

- Huawei

- Lenovo

- Microsoft

- NVIDIA

- 区域玩家

- Ascenty (Digital Realty/Brookfield)

- China Telecom

- Cirion Technologies

- Elea Data Centers

- ST Telemedia Global Data Centres (STT GDC)

- Telehouse (KDDI)

- TierPoint

- 新兴玩家

- Applied Digital

- CoreWeave

- Crusoe Energy

- Lambda Labs

- Nebius AI

The Global AI Data Center Market was valued at USD 98.2 billion in 2024 and is estimated to grow at a CAGR of 35.5% to reach USD 1.98 trillion by 2034.

Growing adoption of generative AI and machine learning tools requires extraordinary processing power and storage capabilities, increasing reliance on data centers specifically optimized for AI workloads. These environments depend on advanced GPUs, scalable system architecture, and ultra-low-latency networking to support complex model training and inference across industries such as finance, healthcare, and retail. Big data analytics is also accelerating demand, as organizations handle massive streams of structured and unstructured information that must be processed rapidly. AI-focused facilities enable high-performance computing for real-time workloads, strengthening their role as essential infrastructure for global digital transformation. The rapid expansion of cloud computing, along with the rising number of hyperscale facilities, continues to amplify the need for AI-ready infrastructures. Providers are investing in advanced AI data platforms that offer scalable services to enterprises and developers, further increasing market momentum.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $98.2 Billion |

| Forecast Value | $1.98 Trillion |

| CAGR | 35.5% |

The hardware segment accounted for USD 61.1 billion in 2024. Growth is driven by expanding use of AI chips, GPU accelerators, advanced cooling technologies, high-density server systems, and optical networking solutions. Rising GPU energy requirements, the shift toward rack densities between 30-120 kW, and large-scale deployment strategies introduced by leading technology companies are shaping long-term capital allocation in the sector.

The cloud-based category held a 58% share in 2024 and is projected to grow at a CAGR of 35.2% from 2025 through 2034. This segment leads due to its unmatched scalability, flexible consumption options, and access to the latest AI-accelerated computing hardware without upfront investment. Hyperscale providers are making multi-billion-dollar commitments to strengthen global AI infrastructures, propelling adoption of AI-driven services and increasing demand for GPUs, TPUs, and specialized processors.

US AI Data Center Market generated USD 33.2 billion in 2024. The country maintains a leading position supported by prominent hyperscale operators and substantial investments in GPU clusters, liquid cooling, and large-scale AI-aligned builds. Federal incentives, regional tax advantages, and infrastructure funding have further solidified the United States as the most capacity-rich region for AI computing.

Key participants in the AI Data Center Market include Huawei, AWS, NVIDIA, HPE, Digital Realty, Google, Lenovo, Microsoft, Equinix, and Dell Technologies. Companies expanding their foothold in the AI data center market are focusing on infrastructure modernization, large-scale GPU deployments, and energy-efficient system design. Many firms are investing in high-density racks, integrated liquid cooling, and next-generation networking to support advanced AI workloads. Strategic partnerships with chipmakers, cloud providers, and colocation operators help accelerate capacity expansion and ensure access to cutting-edge AI hardware. Providers are also scaling global data center footprints, enhancing automation capabilities, and optimizing power utilization through renewable-energy integration. Long-term contracts with enterprises, AI-as-a-service offerings, and the buildout of specialized AI clusters further reinforce competitive positioning and market dominance.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Deployment mode

- 2.2.4 Data center

- 2.2.5 Industry vertical

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook

- 2.6 Strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Adoption of generative AI & machine learning

- 3.2.1.2 Growth in big data analytics

- 3.2.1.3 Cloud expansion & hyperscale deployments

- 3.2.1.4 Advancements in GPU & chip technologies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High capital & operational costs

- 3.2.2.2 Energy consumption & sustainability issues

- 3.2.3 Market opportunities

- 3.2.3.1 Edge AI data centers

- 3.2.3.2 Liquid cooling & green technologies

- 3.2.3.3 AI-as-a-service platforms

- 3.2.3.4 Emerging markets adoption

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.1.1 GPU & accelerator technology evolution

- 3.7.1.2 Liquid cooling technology advancement

- 3.7.1.3 Power distribution innovation (48V Architecture, Modular UPS)

- 3.7.2 Emerging technologies

- 3.7.2.1 Software-defined infrastructure

- 3.7.2.2 Edge computing integration

- 3.7.1 Current technological trends

- 3.8 Pricing analysis

- 3.8.1 Colocation pricing trends (per kw, per rack)

- 3.8.2 Cloud AI compute pricing evolution

- 3.8.3 Energy cost impact on total cost of ownership

- 3.8.4 Cooling technology cost comparison

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis

- 3.10.1 Cooling technology patents

- 3.10.2 AI chip architecture patents

- 3.10.3 Power management innovations

- 3.10.4 Data center design patents

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.12 Carbon footprint considerations

- 3.13 Use cases

- 3.14 Best case scenario

- 3.15 Interconnection & network infrastructure analysis

- 3.15.1 Data center interconnection architecture

- 3.15.2 High-speed fabric requirements

- 3.15.3 Submarine cable investments by hyperscalers

- 3.15.4 Internet exchange point proximity & peering

- 3.15.5 Fiber backhaul availability by region

- 3.15.6. 5 g & edge network integration

- 3.15.7 Software-defined networking adoption

- 3.16 Investment & funding analysis

- 3.16.1 Hyperscale capital expenditure trends

- 3.16.2 Private equity & infrastructure fund activity

- 3.16.3 Government investment programs

- 3.16.4 Venture capital in AI infrastructure startups

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

- 4.7 New capacity & site announcements

- 4.8 Vendor selection criteria

- 4.9 Product & service benchmarking

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Servers

- 5.2.2 GPUs

- 5.2.3 Storage

- 5.2.4 Networking equipment

- 5.3 Software

- 5.3.1 AI frameworks

- 5.3.2 Orchestration tools

- 5.3.3 Management platforms

- 5.4 Services

- 5.4.1 Professional services

- 5.4.1.1 Deployment & Integration

- 5.4.1.2 Consulting

- 5.4.1.3 Support & maintenance

- 5.4.2 Managed services

- 5.4.1 Professional services

Chapter 6 Market Estimates & Forecast, By Deployment Mode, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Cloud-based

- 6.3 On-premises

- 6.4 Hybrid

Chapter 7 Market Estimates & Forecast, By Data Center, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Hyperscale data centers

- 7.3 Enterprise data centers

- 7.4 Colocation data centers

- 7.5 Edge data centers

Chapter 8 Market Estimates & Forecast, By Industry Vertical, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 BFSI

- 8.3 Government

- 8.4 Healthcare

- 8.5 IT & telecom

- 8.6 Automotive

- 8.7 Media & entertainment

- 8.8 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Vietnam

- 9.4.7 Indonesia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global companies

- 10.1.1 AWS

- 10.1.2 Dell Technologies

- 10.1.3 Digital Realty

- 10.1.4 Equinix

- 10.1.5 Google Cloud

- 10.1.6 HPE

- 10.1.7 Huawei

- 10.1.8 Lenovo

- 10.1.9 Microsoft

- 10.1.10 NVIDIA

- 10.2 Regional players

- 10.2.1 Ascenty (Digital Realty/Brookfield)

- 10.2.2 China Telecom

- 10.2.3 Cirion Technologies

- 10.2.4 Elea Data Centers

- 10.2.5 ST Telemedia Global Data Centres (STT GDC)

- 10.2.6 Telehouse (KDDI)

- 10.2.7 TierPoint

- 10.3 Emerging players

- 10.3.1 Applied Digital

- 10.3.2 CoreWeave

- 10.3.3 Crusoe Energy

- 10.3.4 Lambda Labs

- 10.3.5 Nebius AI

人工智慧资料中心市场规模、份额、成长率和全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测

人工智慧资料中心市场规模、份额、成长率和全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测 全球人工智慧资料中心基础设施市场:预测(至2034年)-按组件、部署方式、人工智慧工作负载、技术、电力和冷却基础设施、最终用户和地区进行分析全球人工智慧资料中心风险管理市场:预测(至 2034 年)—按解决方案类型、风险管理类型、部署方式、资料中心类型、人工智慧技术、最终用户和地区进行分析全球人工智慧驱动型资料中心永续性优化市场:预测(至 2034 年)—按组件、部署方式、资料中心类别、人工智慧技术类型、永续性优化重点领域、最终用户和地区进行分析全球人工智慧驱动资料中心营运市场预测(至2034年):按部署类型、资料中心类型、应用程式和地区划分全球资料中心人工智慧优化网路基础设施市场:预测(至2034年)-按产品、网路、部署方式、资料中心类别、人工智慧应用、最终使用者和地区进行分析

全球人工智慧资料中心基础设施市场:预测(至2034年)-按组件、部署方式、人工智慧工作负载、技术、电力和冷却基础设施、最终用户和地区进行分析全球人工智慧资料中心风险管理市场:预测(至 2034 年)—按解决方案类型、风险管理类型、部署方式、资料中心类型、人工智慧技术、最终用户和地区进行分析全球人工智慧驱动型资料中心永续性优化市场:预测(至 2034 年)—按组件、部署方式、资料中心类别、人工智慧技术类型、永续性优化重点领域、最终用户和地区进行分析全球人工智慧驱动资料中心营运市场预测(至2034年):按部署类型、资料中心类型、应用程式和地区划分全球资料中心人工智慧优化网路基础设施市场:预测(至2034年)-按产品、网路、部署方式、资料中心类别、人工智慧应用、最终使用者和地区进行分析 人工智慧互联的转折点:物理层面的生态系统转型与价值创造。

人工智慧互联的转折点:物理层面的生态系统转型与价值创造。 全球人工智慧资料中心互连趋势(2025)

全球人工智慧资料中心互连趋势(2025) 全球和中国的AI资料中心市场(2025年):展开及预测

全球和中国的AI资料中心市场(2025年):展开及预测 逆渗透空调市场报告:2031 年趋势、预测与竞争分析

逆渗透空调市场报告:2031 年趋势、预测与竞争分析