|

市场调查报告书

商品编码

1885869

硅奈米线电池技术市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Silicon Nanowire Battery Technology Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

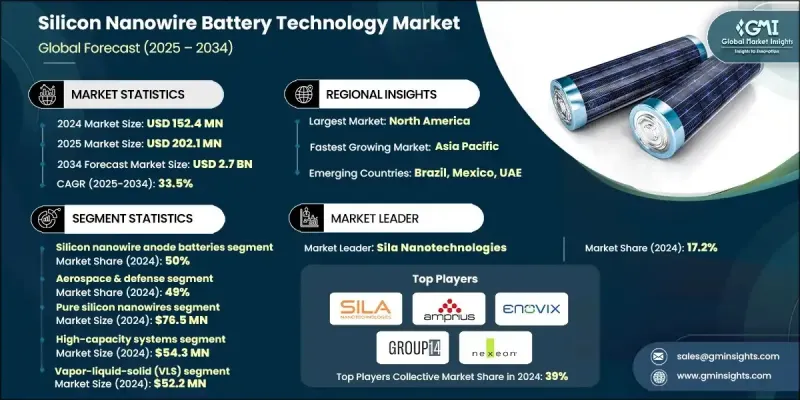

2024 年全球硅奈米线电池技术市场价值为 1.524 亿美元,预计到 2034 年将以 33.5% 的复合年增长率增长至 27 亿美元。

强劲的发展势头源于高能量密度储能係统的普及、电动汽车的蓬勃发展以及先进电池化学技术在消费电子、汽车和固定式储能等主要领域的广泛应用。随着储能需求不断演变,对耐久性、充电速度和循环寿命的要求也日益提高,製造商正日益专注于材料科学的突破、可扩展的製造技术以及数位化增强的开发路径。这些努力旨在确保电池的安全性、实际性能以及商业化部署的准备就绪。此外,先进工程工具的更广泛应用也进一步推动了市场的发展,这些工具简化了开发流程,缩短了原型製作週期,使企业能够更快地将下一代电池推向主流市场。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 1.524亿美元 |

| 预测值 | 27亿美元 |

| 复合年增长率 | 33.5% |

对人工智慧驱动的材料研究、物联网连接的监测平台和基于云端的电池管理系统的日益依赖,正在改变奈米材料电池技术的发展方式。这些解决方案使开发人员能够持续洞察电化学活性,及早预测衰减趋势,并支援研究部门、试点设施和整合合作伙伴之间的同步工作流程管理。数位孪生、机器学习模拟和自动化测试平台的应用有助于加快验证週期、提高能量保持率并降低研发成本,从而支援智慧电池生态系统的转型。

预计到2024年,硅奈米线负极电池市占率将达到50%,并在2025年至2034年间以32.9%的复合年增长率成长。这些负极系统经过精心设计,可显着提升能量密度、导电性和耐久性。其独特的结构能够更好地吸收锂离子,同时克服了传统石墨负极的限制。随着交通运输、电子和航太等产业对更长电池寿命的需求不断增长,纯硅奈米线负极的应用也日益普及,各行业都在寻求更可靠、更高输出功率的储能技术。

2024年,航太与国防领域占据49%的市场份额,预计到2034年将以33.1%的复合年增长率成长。其主导地位源自于对轻量化、高容量、高效能且能在严苛环境下运作的电源解决方案的需求。硅奈米线阳极系统具有高功率重量比、快速充电和超强的运作耐久性,能够满足该领域对先进设备的需求。随着对高可靠性能源系统需求的增长,对奈米结构材料、先进热控制系统和基于人工智慧的建模工具的持续投资进一步巩固了该领域的领先地位。

预计到2024年,美国硅奈米线电池技术市场将占88%的份额,市场规模约4,960万美元。这一领先地位得益于美国成熟的电动车和电池生产体系、强大的研发基础设施以及领先的奈米材料创新企业的积极参与。高容量硅奈米线电池在电动交通、消费性电子产品和电网级储能领域的应用正在加速成长。美国各地的企业正在部署人工智慧诊断技术、物联网连接的监控解决方案和云端管理软体,以提高电池安全性、提升效率并增强营运智慧。

硅奈米线电池技术市场的主要参与者包括Amprius Technologies、BTR New Material、Enevate、ENOVIX、Group14 Technologies、Nexeon、OneD Battery Sciences、信越化学、Sila Nanotechnologies和XG Sciences。这些公司正致力于透过多种策略措施来增强自身的竞争力。许多公司正在扩大产能,以支持商业化并确保稳定的供应。研发专案是提升能量密度、改善循环稳定性、优化奈米线结构的关键。与电动车製造商、电子产品品牌和国防承包商的合作有助于加速技术的实际应用。此外,企业也正在整合以人工智慧为基础的分析、数位孪生和自动化测试系统,以缩短开发週期并降低成本。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 利润率

- 成本结构

- 每个阶段的价值增加

- 影响价值链的因素

- 中断

- 产业影响因素

- 成长驱动因素

- 对高能量密度电池的需求不断增长

- 奈米材料工程和基于人工智慧的材料优化方面的进展

- 快速充电基础设施和高功率应用的发展

- 汽车原始设备製造商和电池製造商的投资不断增加

- 产业陷阱与挑战

- 生产成本高且可扩展性挑战

- 机械不稳定性及退化风险

- 市场机会

- 电动车普及率高和车队电气化

- 固定式储能设施的扩建

- 拓展至电网级及再生能源储存系统

- 开发符合循环经济原则的回收技术

- 成长驱动因素

- 成长潜力分析

- 监管环境

- 奈米材料法规及TSCA合规性

- 职业安全要求和 NIOSH 指南

- 环境影响法规与美国环保署标准

- 国际标准与协调努力

- 产品安全与测试要求

- 认证流程和品质保证

- 监管时间表及未来政策变化

- 合规成本分析及实施策略

- 波特的分析

- PESTEL 分析

- 技术与创新格局

- 技术演进时程及里程碑

- 技术性能提升预测

- 成本削减路线图和经济目标

- 生产规模扩大时程和产能规划

- 新兴科技整合与融合

- 市场渗透情景及采纳曲线

- 颠覆性技术威胁及市场影响

- 长期市场机会与策略远见

- 技术转移与商业化途径

- 创新生态系与合作网络

- 价格趋势

- 按地区

- 副产品

- 生产统计

- 生产中心

- 消费中心

- 进出口

- 成本細項分析

- 专利分析

- 永续性和环境方面

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 最佳情况

- 製造规模化和商业化路线图

- 效能比较矩阵与替代技术

- 资本支出与融资环境

- 性能衰减与循环寿命分析

- 电解质和分离器创新趋势

- 电池组整合与系统级设计

第四章:竞争格局

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划和资金

第五章:市场估算与预测:依类型划分,2021-2034年

- 主要趋势

- 硅奈米线阳极电池

- 硅奈米线复合电池

- 混合奈米结构电池

第六章:市场估算与预测:依製造方法划分,2021-2034年

- 主要趋势

- 气液固(VLS)生长

- 金属辅助化学蚀刻(MACE)

- 化学气相沉积(CVD)

- 基于解决方案的成长方法

- 电化学沉积

第七章:市场估算与预测:依绩效类别划分,2021-2034年

- 主要趋势

- 高容量系统

- 快速充电系统

- 长循环寿命系统

- 成本最佳化系统

第八章:市场估算与预测:依材料成分划分,2021-2034年

- 主要趋势

- 纯硅奈米线

- 硅碳复合材料

- 二氧化硅复合材料

- 硅合金奈米线

第九章:市场估计与预测:依应用领域划分,2021-2034年

- 主要趋势

- 航太与国防

- 汽车

- 消费性电子产品

- 固定式储能

第十章:市场估计与预测:依地区划分,2021-2034年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 比利时

- 荷兰

- 瑞典

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 新加坡

- 韩国

- 越南

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 阿联酋

- 南非

- 沙乌地阿拉伯

第十一章:公司简介

- Global Player

- Amprius Technologies

- BTR New Material

- Group14 Technologies

- LG Energy Solution

- Nexeon

- OneD Material

- Panasonic Energy

- Samsung SDI

- Shanshan Technology

- Sila Nanotechnologies

- Regional Player

- DAEJOO Electronic Materials

- Enevate

- Gotion High-tech

- GUIBAO Science & Technology

- IOPSILION

- KINGi New Materials

- LeydenJar Technologies

- NanoGraf

- NEO Battery Materials

- StoreDot

- 新兴参与者

11.3.1. 电池

- 阿德瓦诺

- 香港能源

- 奈米陶瓷实验室

- 固态动力

The Global Silicon Nanowire Battery Technology Market was valued at USD 152.4 million in 2024 and is estimated to grow at a CAGR of 33.5% to reach USD 2.7 billion by 2034.

Strong momentum comes from the shift toward high-energy-density storage systems, surging electric mobility, and broader use of advanced battery chemistries across major sectors such as consumer electronics, automotive, and stationary energy storage. As energy storage requirements evolve to demand higher durability, faster charging, and longer life cycles, manufacturers are increasingly focusing on breakthroughs in material science, scalable fabrication techniques, and digitally enhanced development pathways. These efforts are aimed at ensuring safety, real-world performance, and readiness for commercial deployment. The market's progress is also reinforced by greater integration of sophisticated engineering tools that streamline development and reduce prototyping timelines, enabling companies to push next-generation batteries toward mainstream adoption.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $152.4 Million |

| Forecast Value | $2.7 Billion |

| CAGR | 33.5% |

Growing reliance on AI-driven material research, IoT-linked monitoring platforms, and cloud-based battery management systems is transforming how nanomaterial battery technologies evolve. These solutions give developers continuous insight into electrochemical activity, allow early prediction of degradation trends, and support synchronized workflow management across research units, pilot facilities, and integration partners. The use of digital twins, machine-learning simulations, and automated testing platforms helps accelerate validation cycles, enhance energy retention, and cut down development expenditures, supporting the transition toward intelligent battery ecosystems.

The silicon nanowire anode batteries segment captured a 50% share in 2024 and is estimated to grow at a CAGR of 32.9% between 2025 and 2034. These anode systems are engineered to deliver substantial improvements in energy density, conductivity, and durability. Their structure enables greater lithium-ion intake while addressing limitations found in conventional graphite. Rising demand for extended battery life in transportation, electronics, and aerospace applications continues to strengthen the adoption of pure silicon nanowire anodes as industries pursue more reliable and high-output storage technologies.

The aerospace and defense segment held a 49% share in 2024 and is expected to grow at a CAGR of 33.1% through 2034. Its dominance is driven by the need for lightweight, high-capacity, and high-performance power solutions capable of functioning in harsh operating environments. Silicon nanowire anode systems offer high power-to-weight ratios, rapid charging, and strong operational endurance, which support the sector's advanced equipment needs. Continuous investments in nanostructured materials, advanced thermal-control systems, and AI-based modeling tools strengthen the segment's leadership as demand for resilient energy systems grows.

United States Silicon Nanowire Battery Technology Market held an 88% share in 2024, generating approximately USD 49.6 million. This position is supported by a well-established EV and battery production landscape, strong R&D infrastructure, and significant involvement from leading nanomaterials innovators. Adoption of high-capacity silicon nanowire batteries has accelerated across electric transportation, consumer devices, and grid-level storage. Companies across the U.S. are deploying AI-enabled diagnostics, IoT-connected monitoring solutions, and cloud-supported management software to increase battery safety, improve efficiency, and enhance operational intelligence.

Key companies active in the Silicon Nanowire Battery Technology Market include Amprius Technologies, BTR New Material, Enevate, ENOVIX, Group14 Technologies, Nexeon, OneD Battery Sciences, ShinEtsu Chemical, Sila Nanotechnologies, and XG Sciences. Companies involved in the Silicon Nanowire Battery Technology Market are focusing on several strategic approaches to strengthen their competitive standing. Many firms are expanding their manufacturing capacities to support commercialization and ensure a consistent supply. Heavy emphasis is placed on R&D programs that enhance energy density, improve cycle stability, and optimize nanowire structures. Collaborations with EV makers, electronics brands, and defense contractors help accelerate real-world adoption. Businesses are also integrating AI-based analytics, digital twins, and automated testing systems to shorten development cycles and reduce costs.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Fabrication Method

- 2.2.4 Performance Category

- 2.2.5 Material Composition

- 2.2.6 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for high-energy-density batteries

- 3.2.1.2 Advancements in nanomaterial engineering and ai-based material optimization

- 3.2.1.3 Growth of fast-charging infrastructure and high-power applications

- 3.2.1.4 Increasing investments from automotive OEMs and battery manufacturers

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production costs and scalability challenges

- 3.2.2.2 Mechanical instability and degradation risks

- 3.2.3 Market opportunities

- 3.2.3.1 High EV adoption and fleet electrification

- 3.2.3.2 Expansion of stationary energy storage

- 3.2.3.3 Expansion into grid-scale and renewable energy storage systems

- 3.2.3.4 Development of circular-economy-aligned recycling technologies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 Nanomaterial regulations & TSCA compliance

- 3.4.2 Occupational safety requirements & NIOSH guidelines

- 3.4.3 Environmental impact regulations & EPA standards

- 3.4.4 International standards & harmonization efforts

- 3.4.5 Product safety & testing requirements

- 3.4.6 Certification processes & quality assurance

- 3.4.7 Regulatory timeline & future policy changes

- 3.4.8 Compliance cost analysis & implementation strategies

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation Landscape

- 3.7.1 Technology evolution timeline & milestones

- 3.7.2 Performance improvement projections by technology

- 3.7.3 Cost reduction roadmap & economic targets

- 3.7.4 Manufacturing scale-up timeline & capacity planning

- 3.7.5 Emerging technology integration & convergence

- 3.7.6 Market penetration scenarios & adoption curves

- 3.7.7 Disruptive technology threats & market impact

- 3.7.8 Long-term market opportunities & strategic vision

- 3.7.9 Technology transfer & commercialization pathways

- 3.7.10 Innovation ecosystem & collaboration networks

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Best case scenarios

- 3.14 Manufacturing Scalability & Commercialization Roadmap

- 3.15 Performance Comparison Matrix vs. Alternative Technologies

- 3.16 Capital Expenditure & Funding Landscape

- 3.17 Performance Degradation & Cycle Life Analysis

- 3.18 Electrolyte & Separator Innovation Trends

- 3.19 Battery Pack Integration & System-Level Design

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Type, 2021 - 2034 ($ Mn, Units)

- 5.1 Key trends

- 5.2 Silicon nanowire anode batteries

- 5.3 Silicon nanowire composite batteries

- 5.4 Hybrid nanostructure batteries

Chapter 6 Market Estimates & Forecast, By Fabrication Method, 2021 - 2034 ($ Mn, Units)

- 6.1 Key trends

- 6.2 Vapor-liquid-solid (VLS) growth

- 6.3 Metal-assisted chemical etching (MACE)

- 6.4 Chemical vapor deposition (CVD)

- 6.5 Solution-based growth methods

- 6.6 Electrochemical deposition

Chapter 7 Market Estimates & Forecast, By Performance Category, 2021 - 2034 ($ Mn, Units)

- 7.1 Key trends

- 7.2 High-capacity systems

- 7.3 Fast charging systems

- 7.4 Long-cycle life systems

- 7.5 Cost-optimized systems

Chapter 8 Market Estimates & Forecast, By Material Composition, 2021 - 2034 ($ Mn, Units)

- 8.1 Key trends

- 8.2 Pure silicon nanowires

- 8.3 Silicon-carbon composites

- 8.4 Silicon-oxide composites

- 8.5 Silicon alloy nanowires

Chapter 9 Market Estimates & Forecast, By Application, 2021 - 2034 ($ Mn, Units)

- 9.1 Key trends

- 9.2 Aerospace & defense

- 9.3 Automotive

- 9.4 Consumer electronics

- 9.5 Stationary energy storage

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($ Mn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Belgium

- 10.3.7 Netherlands

- 10.3.8 Sweden

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 Singapore

- 10.4.6 South Korea

- 10.4.7 Vietnam

- 10.4.8 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Global Player

- 11.1.1 Amprius Technologies

- 11.1.2 BTR New Material

- 11.1.3 Group14 Technologies

- 11.1.4 LG Energy Solution

- 11.1.5 Nexeon

- 11.1.6 OneD Material

- 11.1.7 Panasonic Energy

- 11.1.8 Samsung SDI

- 11.1.9 Shanshan Technology

- 11.1.10 Sila Nanotechnologies

- 11.2 Regional Player

- 11.2.1 DAEJOO Electronic Materials

- 11.2.2 Enevate

- 11.2.3 Gotion High-tech

- 11.2.4 GUIBAO Science & Technology

- 11.2.5 IOPSILION

- 11.2.6 KINGi New Materials

- 11.2.7 LeydenJar Technologies

- 11.2.8 NanoGraf

- 11.2.9 NEO Battery Materials

- 11.2.10 StoreDot

- 11.3 Emerging Players

11.3.1. DBattery

- 11.3.2 Advano

- 11.3.3 HKG Energy

- 11.3.4 Nanoramic Laboratories

- 11.3.5 Solid Power

先进电池市场:按化学成分、电芯形式、电池类型、应用和最终用户划分-2026-2032年全球市场预测

先进电池市场:按化学成分、电芯形式、电池类型、应用和最终用户划分-2026-2032年全球市场预测 先进电池材料市场预测至2034年—全球材料类型、电池类型、形状、技术、应用、最终用户和区域分析

先进电池材料市场预测至2034年—全球材料类型、电池类型、形状、技术、应用、最终用户和区域分析 全球先进电池市场规模、份额、趋势和成长分析报告(2026-2034年)

全球先进电池市场规模、份额、趋势和成长分析报告(2026-2034年) 智慧型运输收费系统市场机会、成长驱动因素、产业趋势分析及预测(2026-2035年)大型圆柱形电池雷射焊接市场:按雷射源类型、电池化学成分、电池容量、功率输出、焊接技术和应用划分-全球预测,2026-2032年

智慧型运输收费系统市场机会、成长驱动因素、产业趋势分析及预测(2026-2035年)大型圆柱形电池雷射焊接市场:按雷射源类型、电池化学成分、电池容量、功率输出、焊接技术和应用划分-全球预测,2026-2032年 全球资料中心电池市场:市场规模、份额和趋势分析(按电池类型、资料中心、应用和地区划分),细分市场预测(2026-2033 年)

全球资料中心电池市场:市场规模、份额和趋势分析(按电池类型、资料中心、应用和地区划分),细分市场预测(2026-2033 年) 2026年全球先进电池技术市场报告2026年全球大型圆柱形电池市场报告

2026年全球先进电池技术市场报告2026年全球大型圆柱形电池市场报告 先进电池技术市场-全球产业规模、份额、趋势、机会与预测:按技术、最终用户、地区和竞争对手划分,2021-2031年浸没式液冷电池系统市场按应用、化学成分、模组类型、冷却液类型和电压划分-2026-2032年全球预测

先进电池技术市场-全球产业规模、份额、趋势、机会与预测:按技术、最终用户、地区和竞争对手划分,2021-2031年浸没式液冷电池系统市场按应用、化学成分、模组类型、冷却液类型和电压划分-2026-2032年全球预测