|

市场调查报告书

商品编码

1892759

宠物科技市场机会、成长驱动因素、产业趋势分析及预测(2026-2035年)Pet Tech Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

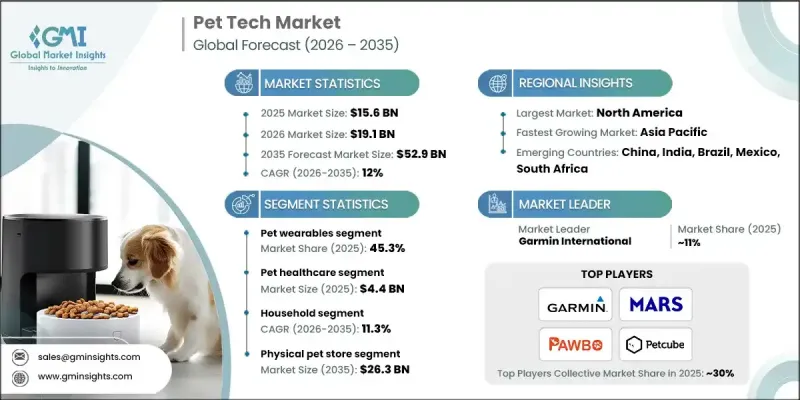

2025年全球宠物科技市场价值156亿美元,预计2035年将以12%的复合年增长率成长至529亿美元。

全球宠物饲养量的快速成长、可支配收入的增加、宠物照护支出的提高以及创新科技宠物解决方案的涌现,共同推动了宠物科技市场的成长。宠物科技专注于智慧型装置和数位平台,旨在监测宠物健康、保障宠物安全,并为主人提供互动和便利。这些解决方案能够实现即时监测,提升宠物整体健康水平,并简化日常护理流程。 Petcube、玛氏公司、Garmin International 和 Pawbo 等行业领导者正透过推出智慧项圈、餵食器、摄影机和健康监测设备来推动市场成长,这些设备能够提供关于宠物健康状况的准确、可操作的资讯。物联网和人工智慧整合设备的应用,使主人能够远端追踪宠物的行为、活动和健康指标,从而在提高护理品质的同时,减少人工监测工作量。

| 市场范围 | |

|---|---|

| 起始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 156亿美元 |

| 预测值 | 529亿美元 |

| 复合年增长率 | 12% |

预计到2025年,宠物穿戴装置市占率将达到45.3%。这些设备,包括智慧项圈、胸背带和背心,能够让主人即时追踪宠物的心率、体温、活动量和位置。与人工智慧和物联网技术的融合,增强了资料收集和远端监控能力,从而能够更好地进行预防性护理和及时干预。

预计到2025年,宠物医疗保健市场规模将达到44亿美元。人们对宠物健康的日益关注以及将宠物视为家庭成员的观念,正在推动对健康科技解决方案的需求。智慧项圈、健身追踪器和配套应用程式可以帮助主人监测宠物的健康指标,并有效地管理它们的日常健康护理。

2025年北美宠物科技市场规模达86亿美元,预计2035年将达297亿美元,复合年增长率(CAGR)为12.2%。宠物拥有率高、先进技术应用广泛以及宠物护理支出不断增长,均推动了市场的强劲增长。现有成熟企业的存在以及创新设备的普及,也进一步促进了区域市场的扩张。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 产业影响因素

- 成长驱动因素

- 宠物饲养和人性化程度的提高

- 人们越来越关注宠物健康和福祉

- 宠物护理的便利性和物联网、人工智慧和资料分析等技术进步

- 政府透过资金和监管支持技术进步。

- 产业陷阱与挑战

- 设备可靠性和故障

- 前期成本高

- 市场机会

- 人工智慧驱动的宠物行为和训练解决方案

- 远端兽医和远端诊断平台

- 成长驱动因素

- 成长潜力分析

- 监管环境

- 北美洲

- 我们

- 加拿大

- 欧洲

- 亚太地区

- 北美洲

- 技术与创新格局

- 目前技术

- 新兴技术

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估算与预测:依产品划分,2022-2035年

- 宠物穿戴装置

- 智慧项圈

- 智慧背心

- 智慧线束

- 智慧型相机

- 智慧宠物笼和床

- 智慧宠物门

- 智慧宠物餵食器和食盆

- 智慧宠物围栏

- 智慧宠物饮水器

- 智慧宠物玩具

第六章:市场估算与预测:依应用领域划分,2022-2035年

- 宠物医疗保健

- 宠物主人便利

- 通讯与娱乐

- 宠物安全

第七章:市场估算与预测:依最终用途划分,2022-2035年

- 家庭

- 商业的

第八章:市场估算与预测:依配销通路划分,2022-2035年

- 实体宠物店

- 仅限线上销售的零售商

- 实体大型零售商

第九章:市场估计与预测:依地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第十章:公司简介

- Actijoy

- CleverPet

- Dogtra

- Felcana

- Fitbark

- Furbo

- Garmin International

- Halo Collar

- Link My Pet

- Loc8tor

- Mars Incorporated

- Pawbo

- Pawscout

- Petcube

- Pet Huhou

- PETKIT

- PetPace

- Qpets

- Tianjin Smart Pets Technology

- Tractive

The Global Pet Tech Market was valued at USD 15.6 billion in 2025 and is estimated to grow at a CAGR of 12% to reach USD 52.9 billion by 2035.

The market growth is fueled by the rapid rise in pet ownership worldwide, increasing disposable incomes, higher spending on pet care, and the availability of innovative, technology-driven solutions for pets. Pet tech focuses on smart devices and digital platforms designed to monitor pets' health, ensure their safety, and provide engagement and convenience for owners. These solutions enable real-time monitoring, enhance overall pet wellness, and simplify care routines. Key players such as Petcube, Mars, Inc., Garmin International, and Pawbo are driving growth by launching smart collars, feeders, cameras, and health-monitoring devices that provide accurate, actionable insights on pets' wellbeing. Adoption of IoT-enabled and AI-integrated devices allows owners to remotely track behavior, activity, and health metrics, improving care quality while reducing manual monitoring efforts.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $15.6 Billion |

| Forecast Value | $52.9 Billion |

| CAGR | 12% |

The pet wearables segment held a 45.3% share in 2025. These devices, including smart collars, harnesses, and vests, enable owners to track heart rate, body temperature, activity levels, and location in real time. Integration with AI and IoT technologies enhances data collection and remote monitoring, allowing for improved preventive care and timely interventions.

The pet healthcare segment reached USD 4.4 billion in 2025. Growing awareness about pet wellness and the perception of pets as family members are driving demand for health-focused tech solutions. Smart collars, fitness trackers, and companion apps help owners monitor pets' health parameters and manage wellness routines effectively.

North America Pet Tech Market generated USD 8.6 billion in 2025 and is projected to reach USD 29.7 billion by 2035, at a CAGR of 12.2%. High pet ownership rates, advanced technological adoption, and growing expenditure on pet care contribute to strong market growth. The presence of established players and the widespread availability of innovative devices further support regional expansion.

Key players operating in the Global Pet Tech Market include Furbo, Actijoy, CleverPet, Dogtra, Felcana, Fitbark, Garmin International, Halo Collar, Link My Pet, Loc8tor, Mars, Inc., Pawbo, Pawscout, Petcube, Pet Huhou, PETKIT, PetPace, Qpets, Tianjin Smart Pets Technology, and Tractive. Companies in the Pet Tech Market are strengthening their presence through continuous innovation, launching new wearable devices, health trackers, and AI-integrated solutions that enhance pet monitoring capabilities. Strategic partnerships with veterinarians, pet retailers, and technology firms expand distribution channels and customer outreach. Firms are also focusing on user-friendly mobile apps and cloud-based platforms to improve real-time monitoring and data management. Expanding into emerging markets and offering customized solutions for different pet species helps capture a wider audience. Marketing campaigns emphasizing pet wellness, safety, and convenience further enhance brand recognition and consumer trust, supporting long-term market growth and competitive positioning.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Application trends

- 2.2.4 End use trends

- 2.2.5 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increased pet ownership and humanization

- 3.2.1.2 Growing awareness of pet health and wellness

- 3.2.1.3 Convenience and technological advancements like IoT, AI and data analytics for pet care

- 3.2.1.4 Governments supporting tech advancements through funding and regulations

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Device reliability and malfunctioning

- 3.2.2.2 High upfront cost

- 3.2.3 Market opportunities

- 3.2.3.1 AI-driven pet behavior and training solutions

- 3.2.3.2 Tele-veterinary and remote diagnostics platforms

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S.

- 3.4.1.2 Canada

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.1 North America

- 3.5 Technology and innovation landscape

- 3.5.1 Current technologies

- 3.5.2 Emerging technologies

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2023

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn and Units)

- 5.1 Key trends

- 5.2 Pet wearables

- 5.2.1 Smart collar

- 5.2.2 Smart vest

- 5.2.3 Smart harness

- 5.2.4 Smart camera

- 5.3 Smart pet crates and beds

- 5.4 Smart pet doors

- 5.5 Smart pet feeders and bowls

- 5.6 Smart pet fence

- 5.7 Smart pet water dispenser

- 5.8 Smart pet toys

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Pet healthcare

- 6.3 Pet owner convenience

- 6.4 Communication and entertainment

- 6.5 Pet safety

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Household

- 7.3 Commercial

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 Physical pet store

- 8.3 Online-only retailer

- 8.4 Physical mass merchant store

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn and Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Actijoy

- 10.2 CleverPet

- 10.3 Dogtra

- 10.4 Felcana

- 10.5 Fitbark

- 10.6 Furbo

- 10.7 Garmin International

- 10.8 Halo Collar

- 10.9 Link My Pet

- 10.10 Loc8tor

- 10.11 Mars Incorporated

- 10.12 Pawbo

- 10.13 Pawscout

- 10.14 Petcube

- 10.15 Pet Huhou

- 10.16 PETKIT

- 10.17 PetPace

- 10.18 Qpets

- 10.19 Tianjin Smart Pets Technology

- 10.20 Tractive

2026-2030年全球宠物科技及健康产品市场

2026-2030年全球宠物科技及健康产品市场 宠物护理机器人市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、功能、最终用户和安装类型划分

宠物护理机器人市场分析及预测(至2035年):按类型、产品类型、服务、技术、组件、应用、功能、最终用户和安装类型划分 宠物健康保险平台市场预测至2032年:全球按类型、保险范围、动物类型、平台类型、分销管道、最终用户和地区分類的分析

宠物健康保险平台市场预测至2032年:全球按类型、保险范围、动物类型、平台类型、分销管道、最终用户和地区分類的分析 宠物科技市场-全球产业规模、份额、趋势、机会及预测(按类型、产品、应用、地区及竞争格局划分,2020-2030年预测)宠物保险技术平台市场预测(至 2032 年):按组件、保险类型、部署模式、分销管道、技术、最终用户和地区进行分析2032 年宠物科技市场预测:按产品类型、动物类型、通路、技术、最终用户和地区进行的全球分析

宠物科技市场-全球产业规模、份额、趋势、机会及预测(按类型、产品、应用、地区及竞争格局划分,2020-2030年预测)宠物保险技术平台市场预测(至 2032 年):按组件、保险类型、部署模式、分销管道、技术、最终用户和地区进行分析2032 年宠物科技市场预测:按产品类型、动物类型、通路、技术、最终用户和地区进行的全球分析 全球宠物科技市场

全球宠物科技市场 宠物科技市场规模与预测

宠物科技市场规模与预测 Pettech 市场规模、份额、成长分析、按产品类型、按应用、按最终用途、按分销管道、按地区 - 行业预测,2024-2031 年

Pettech 市场规模、份额、成长分析、按产品类型、按应用、按最终用途、按分销管道、按地区 - 行业预测,2024-2031 年 全球宠物技术市场规模研究,按类型、产品、应用、最终用户、配销通路和区域预测 2022-2032

全球宠物技术市场规模研究,按类型、产品、应用、最终用户、配销通路和区域预测 2022-2032