|

市场调查报告书

商品编码

1913362

电动汽车增程器市场:市场机会、成长驱动因素、产业趋势分析及预测(2026-2035)Electric Vehicle Range Extender Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

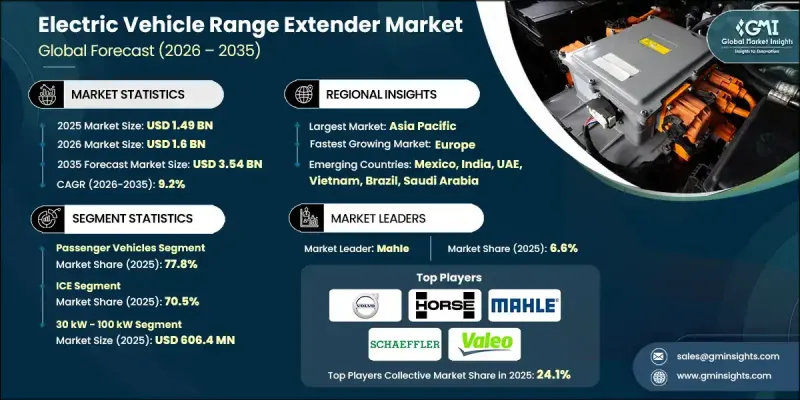

全球电动车增程器市场预计到 2025 年将达到 14.9 亿美元,到 2035 年将达到 35.4 亿美元,年复合成长率为 9.2%。

全球向电动出行的加速转型持续推动市场扩张,电动车销量的成长直接带动了对解决续航里程问题的技术的需求。在公共充电网路不发达的地区,增程器的重要性日益凸显。技术的不断进步提升了现代增程器器的成本效益和性能,增加了其大规模部署的潜力。这些系统有助于提高车辆效率、减少环境影响并延长续航里程,使电动出行对个人和商业用途更具吸引力。同时,电池领域的创新也带来了竞争压力,电池能量密度和快速充电能力的提升降低了对辅助电源系统的依赖。儘管面临这些挑战,增程器透过解决长途旅行难题并促进电动车在各种应用场景中的普及,继续为市场成长提供支援。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 初始市场规模 | 14.9亿美元 |

| 市场规模预测 | 35.4亿美元 |

| 复合年增长率 | 9.2% |

预计到2025年,乘用车市占率将达到77.8%。消费者越来越重视日常都市区和郊区用车的续航里程,因为减少充电频率可以提高电动车的便利性和使用者信心。增程器的应用有助于缓解消费者最初的里程焦虑,从而推动电动乘用车在全球范围内获得强劲增长。

预计到 2025 年,基于内燃机的解决方案市占率将达到 70.5%,2026 年至 2035 年的复合年增长率将达到 9.6%。与新兴的发电替代方案相比,由于这些系统技术成熟、供应链完善且开发和製造成本较低,製造商仍青睐这些系统。

2025年,美国电动车增程器市场价值将达3.097亿美元。各州政府对电动车的奖励、税收减免和监管支持将继续推动国内生产和投资,从而增强美国市场的成长。

目录

第一章:分析方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 成本结构

- 每个阶段的附加价值

- 影响价值链的因素

- 中断

- 产业影响因素

- 司机

- 消费者日益增长的里程焦虑

- 电动商用车和车队车辆的成长

- 新兴市场电动车普及率不断提高

- 农村地区和高速公路沿线缺乏充电基础设施

- 产业潜在风险与挑战

- 快速充电基础设施的快速扩张

- 提高电池能量密度并降低成本

- 市场机会

- 电动卡车和货车的增程器

- 现有电动车平台的改造解决方案

- 基础设施存在缺口的新兴市场

- 氢燃料和电子燃料增程器系统

- 司机

- 成长潜力分析

- 监管环境

- 北美洲

- 加州空气资源委员会(CARB)先进清洁汽车II(ACC II)

- 美国环保署温室气体(GHG)标准

- IRA(通货膨胀削减法案)税额扣抵

- 欧洲

- 欧7标准

- 效用因子(UF)曲线调整

- 欧盟委员会

- 国际清洁交通委员会

- 亚太地区

- 中国的新能源汽车政策

- 印度的FAME-III(草案)

- 双学分制(CAFC 和 NEV)

- 拉丁美洲

- 巴西搬家计划

- CONAMA(Conselho Nacional do Meio Ambiente)

- 中东和非洲

- GSO(海湾标准组织)标准

- 阿拉伯联合大公国(阿联酋)国家电动车政策

- 沙乌地阿拉伯 SASO 法规

- 北美洲

- 波特五力分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 副产品

- 生产统计

- 生产基地

- 消费基础

- 出口和进口

- 永续性和环境影响

- 环境影响评估

- 社会影响力和社区服务

- 公司管治与企业社会责任

- 永续金融与投资趋势

- 对各区域基础设施发展状况进行评估

- 充电基础设施发展状况:依地区划分

- 增程器系统的燃料供应状况

- 都市区和城际基础设施缺口

- 对增程器需求前景的影响

- 成本細項分析

- 发动机/能源产出单元成本

- 发电机及电气电子设备成本

- 燃油系统和排放气体控製成本

- 温度控管和冷却系统成本

- 製造和组装成本

- 案例研究

- 未来前景与机会

第四章 竞争情势

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 主要企业的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 重大进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 企业扩张计画和资金筹措

第五章增程器市场估算与预测(2022-2035)

- 内燃机(ICE)

- 柴油引擎

- 汽油

- 旋转

- 替代燃料电池

- 天然气

- 氢

- 生质燃料

第六章 按产量分類的市场估计与预测(2022-2035 年)

- 小于30千瓦

- 30kW~100kW

- 100千瓦或以上

第七章 按组件分類的市场估计和预测(2022-2035 年)

- 电池组

- 电源转换器

- 电动机

- 发电机

- 其他的

第八章 按车辆类型分類的市场估计和预测(2022-2035 年)

- 搭乘用车

- 轿车

- SUV

- 掀背车

- 商用车辆

- 轻型商用车(LCV)

- 中型商用车(MCV)

- 重型商用车(HCV)

- 两轮车/三轮车

第九章 按应用领域分類的市场估算与预测(2022-2035 年)

- 企业/物流车辆

- 共乘/计程车/租车服务

- 个人车

第十章 依销售管道分類的市场估计与预测(2022-2035 年)

- OEM

- 售后市场

第十一章 各地区市场估计与预测(2022-2035 年)

- 北美洲

- 美国

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 北欧国家

- 比荷卢经济联盟

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲和纽西兰

- 新加坡

- 马来西亚

- 印尼

- 越南

- 泰国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 哥伦比亚

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十二章:公司简介

- 世界公司

- ZF Group

- Stellantis

- Hyundai Motor

- Volvo

- Mazda Motor

- BYD

- Li Auto

- Huawei

- Leapmotor

- Magna

- MAHLE Powertrain

- Ballard

- 本地公司

- AVL

- FEV Group

- Plug Power

- Scout Motors

- Avatr Technologies

- Deepal

- Bosch Engineering

- XPeng Motors

- 新兴企业

- Obrist Powertrain

- Delta Motorsports

- Ceres Power

- Symbio

- EP Tender

The Global Electric Vehicle Range Extender Market was valued at USD 1.49 billion in 2025 and is estimated to grow at a CAGR of 9.2% to reach USD 3.54 billion by 2035.

The accelerating shift toward electric mobility worldwide continues to support market expansion, as rising EV sales directly increase demand for technologies that address driving range concerns. Range extenders are gaining relevance in regions where public charging networks remain underdeveloped. Ongoing technological progress has improved the cost efficiency and performance of modern range extender systems, making them more viable for large-scale adoption. These systems help improve vehicle efficiency, reduce environmental impact, and extend driving distance, which strengthens the appeal of electric mobility for both private and commercial use. At the same time, innovation within the battery sector is creating competitive pressure, as higher battery energy density and faster charging capabilities reduce dependence on auxiliary power systems. Despite these challenges, range extenders continue to support market growth by addressing long-distance travel limitations and enabling wider EV acceptance across diverse use cases.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.49 Billion |

| Forecast Value | $3.54 Billion |

| CAGR | 9.2% |

The passenger vehicles segment accounted for 77.8% share in 2025. Consumers increasingly prioritize extended driving range for everyday urban and suburban usage, as reduced charging frequency improves convenience and confidence in EV ownership. Range extender integration has helped ease earlier adoption barriers related to range anxiety, allowing electric passenger vehicles to gain stronger global traction.

The internal combustion engine-based solutions segment held 70.5% share in 2025 and is forecast to grow at a CAGR of 9.6% from 2026 to 2035. Manufacturers continue to favor these systems due to their technical maturity, established supply chains, and lower development and manufacturing costs compared to newer power generation alternatives.

U.S. Electric Vehicle Range Extender Market garnered USD 309.7 million in 2025. State-level incentives, tax benefits, and regulatory support for electric vehicles continue to encourage domestic production and investment, strengthening market growth across the country.

Key companies active in the Global Electric Vehicle Range Extender Market include ZF Group, Hyundai Mobis, Mahle, Mazda, AVL, Li Auto, Schaeffler, AB Volvo, Valeo, and Horse Powertrain. Companies operating in the Electric Vehicle Range Extender Market focus on technology optimization, cost reduction, and strategic partnerships to reinforce their market position. Many players invest heavily in research and development to improve efficiency, durability, and system integration. Collaboration with vehicle manufacturers allows suppliers to align product design with evolving EV platforms. Firms also prioritize scalable manufacturing to meet rising demand while maintaining competitive pricing. Geographic expansion remains a key strategy, with companies strengthening regional production and distribution networks. In addition, players emphasize compliance with emission regulations and alignment with government incentive programs.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Range extender

- 2.2.3 Power Output

- 2.2.4 Component

- 2.2.5 Vehicle

- 2.2.6 Application

- 2.2.7 Sales Channel

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising consumer range anxiety

- 3.2.1.2 Growth in electric commercial and fleet vehicles

- 3.2.1.3 Expansion of EV adoption in emerging markets

- 3.2.1.4 Limited charging infrastructure in rural and highway areas

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Rapid expansion of fast-charging infrastructure

- 3.2.2.2 Increasing battery energy density and cost decline

- 3.2.3 Market opportunities

- 3.2.3.1 Range extenders for electric trucks and vans

- 3.2.3.2 Retrofitting solutions for existing EV platforms

- 3.2.3.3 Emerging markets with infrastructure gaps

- 3.2.3.4 Hydrogen and e-fuel-based range extender systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 CARB Advanced Clean Cars II (ACC II)

- 3.4.1.2 EPA Greenhouse Gas (GHG) Standards

- 3.4.1.3 IRA (Inflation Reduction Act) Tax Credits

- 3.4.2 Europe

- 3.4.2.1 Euro 7 Standards

- 3.4.2.2 Utility Factor (UF) Curve Adjustments

- 3.4.2.3 European Commission

- 3.4.2.4 International Council on Clean Transportation

- 3.4.3 Asia Pacific

- 3.4.3.1 China’s New Energy Vehicle Policy

- 3.4.3.2 India’s FAME-III (Draft)

- 3.4.3.3 Dual Credit System (CAFC & NEV)

- 3.4.4 Latin America

- 3.4.4.1 Brazil’s Mover Program

- 3.4.4.2 CONAMA (Conselho Nacional do Meio Ambiente)

- 3.4.5 Middle East & Africa

- 3.4.5.1 GSO (Gulf Standardization Organization) Standards

- 3.4.5.2 UAE National EV Policy

- 3.4.5.3 Saudi SASO Regulations

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Sustainability and environmental impact

- 3.10.1 Environmental impact assessment

- 3.10.2 Social impact & community benefits

- 3.10.3 Governance & corporate responsibility

- 3.10.4 Sustainable finance & investment trends

- 3.11 Regional infrastructure readiness assessment

- 3.11.1 Charging infrastructure maturity by region

- 3.11.2 Fuel availability for range extender systems

- 3.11.3 Urban versus intercity infrastructure gaps

- 3.11.4 Impact on range extender demand outlook

- 3.12 Cost breakdown analysis

- 3.12.1 Engine or energy generation unit cost

- 3.12.2 Generator and power electronics cost

- 3.12.3 Fuel system and emissions control cost

- 3.12.4 Thermal management and cooling system cost

- 3.12.5 Manufacturing and assembly cost

- 3.13 Case studies

- 3.14 Future outlook & opportunities

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Range Extender, 2022 - 2035 ($Mn, Units)

- 5.1 Key trends

- 5.2 ICE

- 5.2.1 Diesel

- 5.2.2 Gasoline

- 5.2.3 Rotary

- 5.3 Alternate fuel cell

- 5.3.1 Natural gas

- 5.3.2 Hydrogen

- 5.3.3 Biofuel

Chapter 6 Market Estimates & Forecast, By Power Output, 2022 - 2035 ($Mn, Units)

- 6.1 Key trends

- 6.2 Less than 30 kW

- 6.3 30 kW - 100 kW

- 6.4 Above 100 kW

Chapter 7 Market Estimates & Forecast, By Component, 2022 - 2035 ($Mn, Units)

- 7.1 Key trends

- 7.2 Battery pack

- 7.3 Power converter

- 7.4 Electric motor

- 7.5 Generator

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn, Units)

- 8.1 Key trends

- 8.2 Passenger vehicles

- 8.2.1 Sedan

- 8.2.2 SUV

- 8.2.3 Hatchback

- 8.3 Commercial vehicles

- 8.3.1 LCV

- 8.3.2 MCV

- 8.3.3 HCV

- 8.4 Two-Wheelers & Three-Wheelers

Chapter 9 Market Estimates & Forecast, By Application, 2022 - 2035 ($Mn, Units)

- 9.1 Key trends

- 9.2 Corporate/logistics fleet

- 9.3 Ridesharing/taxi/rental services

- 9.4 Personal vehicles

Chapter 10 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Mn, Units)

- 10.1 Key trends

- 10.2 OEM

- 10.3 Aftermarket

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Nordics

- 11.3.8 Benelux

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 ANZ

- 11.4.6 Singapore

- 11.4.7 Malaysia

- 11.4.8 Indonesia

- 11.4.9 Vietnam

- 11.4.10 Thailand

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.5.4 Colombia

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global companies

- 12.1.1 ZF Group

- 12.1.2 Stellantis

- 12.1.3 Hyundai Motor

- 12.1.4 Volvo

- 12.1.5 Mazda Motor

- 12.1.6 BYD

- 12.1.7 Li Auto

- 12.1.8 Huawei

- 12.1.9 Leapmotor

- 12.1.10 Magna

- 12.1.11 MAHLE Powertrain

- 12.1.12 Ballard

- 12.2 Regional companies

- 12.2.1 AVL

- 12.2.2 FEV Group

- 12.2.3 Plug Power

- 12.2.4 Scout Motors

- 12.2.5 Avatr Technologies

- 12.2.6 Deepal

- 12.2.7 Bosch Engineering

- 12.2.8 XPeng Motors

- 12.3 Emerging companies

- 12.3.1 Obrist Powertrain

- 12.3.2 Delta Motorsports

- 12.3.3 Ceres Power

- 12.3.4 Symbio

- 12.3.5 EP Tender

电动车增程器市场:按增程器类型、燃料类型、功率范围、车辆类型、应用和销售管道划分-2026-2032年全球预测

电动车增程器市场:按增程器类型、燃料类型、功率范围、车辆类型、应用和销售管道划分-2026-2032年全球预测 全球及中国增程器车(REEV)及插电式混合动力汽车(PHEV)市场(2026 年)

全球及中国增程器车(REEV)及插电式混合动力汽车(PHEV)市场(2026 年) 增程型电动车(EREV)市场规模、份额和成长分析:按产品类型、推进系统、电池类型、最终用户和地区划分-2026-2033年产业预测

增程型电动车(EREV)市场规模、份额和成长分析:按产品类型、推进系统、电池类型、最终用户和地区划分-2026-2033年产业预测 增程器电动车市场展望:欧洲、美国、中国,2024-2040年全球电动汽车增程器市场规模、份额、趋势和成长分析报告(2026-2034年)

增程器电动车市场展望:欧洲、美国、中国,2024-2040年全球电动汽车增程器市场规模、份额、趋势和成长分析报告(2026-2034年) 电动车增程器市场-全球产业规模、份额、趋势、机会与预测:按类型、组件类型、车辆类型、地区和竞争格局划分,2021-2031年

电动车增程器市场-全球产业规模、份额、趋势、机会与预测:按类型、组件类型、车辆类型、地区和竞争格局划分,2021-2031年 增程型电动车市场:依车辆类型、增程器类型、电池容量、应用和地区划分 - 全球市场分析(2025-2035)

增程型电动车市场:依车辆类型、增程器类型、电池容量、应用和地区划分 - 全球市场分析(2025-2035) 全球电动车增程器市场:依产品、车辆、组件和地区划分 - 市场规模、行业趋势、机会分析和预测(2026-2035 年)电动车增程器的全球市场:技术·车辆类型·用途·各地区 (~2034年)

全球电动车增程器市场:依产品、车辆、组件和地区划分 - 市场规模、行业趋势、机会分析和预测(2026-2035 年)电动车增程器的全球市场:技术·车辆类型·用途·各地区 (~2034年) 2025 年至 2033 年电动车增程器市场报告(按类型、组件、车辆类型和地区)

2025 年至 2033 年电动车增程器市场报告(按类型、组件、车辆类型和地区)