|

市场调查报告书

商品编码

1928878

胶原肠衣市场机会、成长要素、产业趋势分析及预测(2026年至2035年)Collagen Casings Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

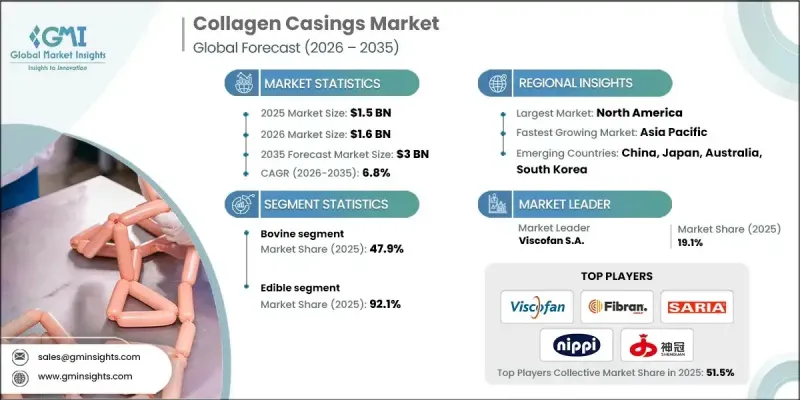

全球胶原肠衣市场预计到 2025 年将达到 15 亿美元,到 2035 年将达到 30 亿美元,年复合成长率为 6.8%。

胶原肠衣是一种可食用的高蛋白香肠肠衣,由牛或猪胶原蛋白製成,是传统动物肠衣的天然永续替代品。胶原蛋白肠衣主要由牛皮製成,因其均匀性、便利性和与高速自动化机械的兼容性而被广泛应用于香肠生产,显着提高了肉类加工商的营运效率。全球肉品消费量的持续增长推动了对胶原肠衣的需求,与天然肠衣相比,扩充性且经济高效的解决方案。根据联合国粮食及农业组织(粮农组织)预测,2023年全球肉类产量预计将达到约3.64亿吨,并有望持续成长,尤其是新兴市场。胶原肠衣因其能够维持直径一致、承受生产过程中的各种压力、降低污染风险并符合严格的食品安全法规而备受青睐。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 15亿美元 |

| 预测金额 | 30亿美元 |

| 复合年增长率 | 6.8% |

预计到2025年,牛胶原蛋白市占率将达到47.9%,并在2035年之前以6.6%的复合年增长率成长。其强度高、稳定性好,且能无缝整合到自动化生产线中,使其成为大型香肠加工商的首选。来自牛肉产业的稳定供应确保了成本效益和可靠的性能。

到2025年,可食用胶原肠衣的市占率将达到92.1%。无论是生肠衣、熟肠衣或烟熏肠衣,都广泛应用于香肠的大规模生产製造。它们在食用时仍能与产品保持连接,尺寸均匀,并且与自动化填充系统兼容,因此成为全球各种规模肉类加工企业的首选。

预计到2025年,北美胶原肠衣市场规模将达到4.462亿美元,2026年至2035年的复合年增长率(CAGR)为6.6%。消费者对天然、洁净标示和无过敏原食品的需求不断增长,推动了胶原肠衣在加工肉品肉製品、蒸馏食品和零食中的应用。为了满足消费者对健康、透明度和产品品质的期望,各公司越来越注重永续采购和环境友善的生产流程。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段的附加价值

- 影响价值链的因素

- 中断

- 产业影响因素

- 司机

- 全球肉类消费和加工量不断增长

- 与天然肠衣相比的优势

- 永续性和循环经济的发展趋势

- 产业潜在风险与挑战

- 原物料价格波动

- 与替代外壳产品的竞争

- 市场机会

- 有效利用製革废弃物

- 高级认证市场

- 司机

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特分析

- PESTEL 分析

- 价格趋势

- 按地区

- 按来源

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 专利状态

- 贸易统计(HS编码)(註:仅提供主要国家的贸易统计)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 考虑到碳足迹

第四章 竞争情势

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 重大进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划

5. 2022-2035年按来源分類的市场估计与预测

- 牛

- 猪肉

- 家禽

- 渔业

- 绵羊和山羊

第六章 2022-2035年按产品分類的市场估算与预测

- 食用

- 不可食用

第七章 依口径分類的市场估计与预测,2022-2035年

- 小直径(14-32毫米)

- 中等直径(33-50毫米)

- 大直径(超过50毫米)

第八章 按应用领域分類的市场估算与预测,2022-2035年

- 生香肠

- 熟香肠

- 干式熟成香肠

- 熏香肠

- 肉类零食

- 其他的

第九章 2022-2035年各地区市场估算与预测

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

- 其他中东和非洲地区

第十章:公司简介

- Belkozin

- FABIOS SA

- Fibran Group

- Foodchem International Corporation

- Nippi Inc.

- PS Seasoning

- SARIA SE &Co. KG

- Shenguan Holdings(Group)Limited

- Viscofan SA

- Viskoteepak

The Global Collagen Casings Market was valued at USD 1.5 billion in 2025 and is estimated to grow at a CAGR of 6.8% to reach USD 3 billion by 2035.

Collagen casings are edible, protein-rich sausage casings made from bovine or porcine collagen, offering a natural and sustainable alternative to traditional casings derived from animal intestines. They are primarily produced from bovine hides and are widely used in sausage manufacturing because they provide uniformity, convenience, and compatibility with high-speed automated machinery, which significantly boosts operational efficiency for meat processors. The steady rise in global meat consumption is fueling demand for collagen casings, as they provide scalable and cost-effective solutions compared to natural alternatives. According to the Food and Agriculture Organization, global meat production reached nearly 364 million metric tons in 2023, with expectations of continuous growth, particularly in emerging markets. Collagen casings are favored because they maintain consistent diameters, withstand production forces, and reduce contamination risks while meeting stringent food safety regulations.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.5 Billion |

| Forecast Value | $3 Billion |

| CAGR | 6.8% |

The bovine collagen segment held a 47.9% share in 2025 and is expected to grow at a CAGR of 6.6% through 2035. Its strength, stability, and seamless integration into automated production lines make it a preferred choice for major sausage processors. Availability from the beef industry ensures cost-effective sourcing and reliable performance.

The edible collagen casings segment held 92.1% share in 2025. Fresh, cooked, and smoked edible casings are widely used in high-volume sausage production. Their ability to remain on the product during consumption, uniform sizing, and compatibility with automated stuffing systems make them the go-to option for meat processors of all scales worldwide.

North America Collagen Casings Market captured USD 446.2 million in 2025 and is projected grow at a CAGR of 6.6% from 2026 to 2035. Rising consumer demand for natural, clean-label, and allergen-free foods is driving the adoption of collagen casings in processed meat, ready-to-eat meals, and snacks. Companies are increasingly focusing on sustainable sourcing and environmentally friendly manufacturing processes to meet consumer expectations regarding health, transparency, and product quality.

Key players in the Global Collagen Casings Market include FABIOS S.A., Belkozin, Nippi Inc., PS Seasoning, Fibran Group, Viscofan S.A., Shenguan Holdings (Group) Limited, Viskoteepak, Foodchem International Corporation, and SARIA SE & Co. KG. Market participants are strengthening their position by investing in R&D to develop high-performance, consistent, and clean-label casings. Collaborations with meat processors and food manufacturers allow them to customize solutions for automated production lines. Geographic expansion into emerging markets with growing meat consumption enhances market penetration. Companies also focus on sustainable sourcing and eco-friendly manufacturing processes to meet regulatory standards and consumer demand. Offering technical support, training, and innovation in casing design further solidifies brand loyalty and increases competitive advantage.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Source

- 2.2.3 Product

- 2.2.4 Caliber

- 2.2.5 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global meat consumption & processing

- 3.2.1.2 Advantages over natural casings

- 3.2.1.3 Sustainability & circular economy trends

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Raw material price volatility

- 3.2.2.2 Competition from alternative casings

- 3.2.3 Market opportunities

- 3.2.3.1 Tannery waste valorization

- 3.2.3.2 Premium certification markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter';s analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By source

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) ( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Source, 2022-2035 (USD Billion) (Million Metres)

- 5.1 Key trends

- 5.2 Bovine

- 5.3 Porcine

- 5.4 Poultry

- 5.5 Marine

- 5.6 Ovine & caprine

Chapter 6 Market Estimates and Forecast, By Product, 2022-2035 (USD Billion) (Million Meters)

- 6.1 Key trends

- 6.2 Edible

- 6.3 Non-edible

Chapter 7 Market Estimates and Forecast, By Caliber, 2022-2035 (USD Billion) (Million Meters)

- 7.1 Key trends

- 7.2 Small diameter (14-32 mm)

- 7.3 Medium diameter (33-50 mm)

- 7.4 Large diameter (>50 mm)

Chapter 8 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Million Meters)

- 8.1 Key trends

- 8.2 Fresh sausages

- 8.3 Cooked sausages

- 8.4 Dry-cured sausages

- 8.5 Smoked sausages

- 8.6 Meat-based snacks

- 8.7 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Million Meters)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Belkozin

- 10.2 FABIOS S.A.

- 10.3 Fibran Group

- 10.4 Foodchem International Corporation

- 10.5 Nippi Inc.

- 10.6 PS Seasoning

- 10.7 SARIA SE & Co. KG

- 10.8 Shenguan Holdings (Group) Limited

- 10.9 Viscofan S.A.

- 10.10 Viskoteepak