|

市场调查报告书

商品编码

1928902

金属加工液市场机会、成长要素、产业趋势分析及2026年至2035年预测Metalworking Fluids Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

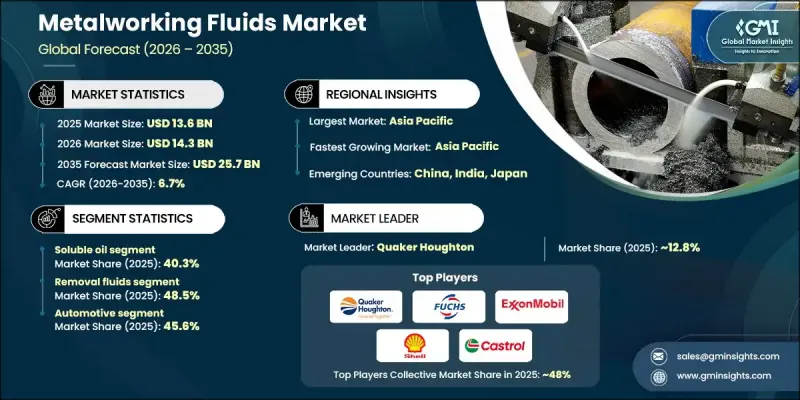

全球金属加工液市场预计到 2025 年将达到 136 亿美元,到 2035 年将达到 257 亿美元,年复合成长率为 6.7%。

金属加工液是指用于机械加工、研磨、成形和表面处理等製程的专用润滑剂和冷却剂。这些产品包括纯油、水溶性油、半合成油和全合成油,它们发挥重要的功能,例如减少摩擦、散热、排屑、防止腐蚀和延长刀具寿命。水溶性加工液因其成本效益高、乳化稳定性好以及适用于各种加工製作流程优点而被广泛采用,因此占据市场主导。汽车和航太製造业的扩张、对高精度零件需求的不断增长以及加工技术的进步是推动市场成长的主要因素。此外,人们对生物基和永续配方的日益关注,以及对高速、复杂金属加工应用性能的改进,也推动了全球市场的需求。在热稳定性、润滑性和表面光洁度方面的持续创新,确保了金属加工液在现代製造业中始终扮演着不可或缺的角色。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 136亿美元 |

| 预测金额 | 257亿美元 |

| 复合年增长率 | 6.7% |

2025年,可溶性油市占率达到40.3%,预计2026年至2035年将以6.5%的复合年增长率成长。可溶性油因其在冷却效率、润滑性能和成本效益方面的均衡表现而备受青睐。这些油液具有优异的乳化稳定性和多功能性,可满足铣削、钻孔、车削和研磨等多种应用需求。水基配方在提供高效散热的同时,也能为中等负载作业提供足够的润滑,因此是通用机械加工的首选。

2025年,切削液市占率占比达48.5%,预计2026年至2035年将以7.2%的复合年增长率成长。其市场主导地位主要源自于汽车、航太和通用工程等产业对切削、研磨、铣削、钻孔和车削等加工操作的根本性需求。切削液在金属去除过程中提供关键的润滑、冷却、切屑管理和刀具保护,确保稳定的生产效率。由于其对各种金属和工况的广泛适用性,切削液将继续作为机械加工的基础发挥至关重要的作用。

预计到2025年,美国金属加工液市场规模将达26亿美元。北美地区,尤其是美国市场的成长,得益于其强大的工业基础,包括汽车製造、航太零件製造和机械生产。引擎、变速箱和结构件製造对精度、效率和可靠性的需求,持续推动高性能加工液(例如切削油、半合成油和成型油)的需求。先进的基础设施、完善的生产设施和严格的品质标准,也持续推动该地区市场对这些产品的采用。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段的附加价值

- 影响价值链的因素

- 中断

- 产业影响因素

- 司机

- 产业潜在风险与挑战

- 市场机会

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 副产品

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 专利状态

- 贸易统计(HS编码)

(註:贸易统计数据仅涵盖主要国家。)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续努力

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 考虑到碳足迹

第四章 竞争情势

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 重大进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章 2022-2035年按产品分類的市场估算与预测

- 纯油

- 可溶性油

- 半合成流体

- 合成流体

第六章 按应用领域分類的市场估算与预测,2022-2035年

- 液体

- 成型液

- 保护液

- 加工液

7. 依最终用途分類的市场估计与预测,2022-2035 年

- 车

- 航太

- 建造

- 电

- 农业

- 船

- 卫生保健

- 其他的

第八章 2022-2035年各地区市场估算与预测

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

- 其他中东和非洲地区

第九章:公司简介

- Quaker Houghton

- FUCHS Petrolub SE

- ExxonMobil

- Shell(Shell Lubricants)

- BP Castrol

- Chevron(Caltex)

- TotalEnergies

- Idemitsu Kosan

- Yushiro Chemical

- Blaser Swisslube

- Master Fluid Solutions

- Milacron(Cimcool)

- Oemeta Chemische Werke

- Petron Corporation

- Phoenix Petroleum Philippines

The Global Metalworking Fluids Market was valued at USD 13.6 billion in 2025 and is estimated to grow at a CAGR of 6.7% to reach USD 25.7 billion by 2035.

Metalworking fluids are described as specialized lubricants and coolants essential for machining, grinding, forming, and surface treatment processes. These products, available as neat oils, soluble oils, semi-synthetic, and fully synthetic fluids, provide vital functions such as friction reduction, heat dissipation, chip removal, corrosion protection, and tool life enhancement. Soluble oils dominate the market with broad adoption due to their cost-effectiveness, emulsion stability, and suitability across diverse machining operations. Market growth is propelled by expanding automotive and aerospace manufacturing, rising demand for high-precision components, and advances in machining technologies. Increasing focus on bio-based and sustainable formulations, along with enhanced performance characteristics for high-speed and complex metalworking, is further driving global demand. Continuous innovation in thermal stability, lubricity, and surface finish quality ensures that metalworking fluids remain indispensable in modern manufacturing.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $13.6 billion |

| Forecast Value | $25.7 billion |

| CAGR | 6.7% |

The soluble oil segment accounted for 40.3% share in 2025 and is expected to grow at a CAGR of 6.5% from 2026 to 2035. Soluble oils are favored due to their ability to provide a balanced combination of cooling efficiency, lubrication performance, and cost-effectiveness. These fluids offer excellent emulsion stability and versatility, supporting applications like milling, drilling, turning, and grinding. Their water-based formulation ensures efficient heat dissipation while maintaining sufficient lubrication for moderate-duty operations, making them a preferred choice for general machining requirements.

The removal fluids segment held a 48.5% share in 2025 and is projected to grow at a CAGR of 7.2% from 2026 to 2035. Their dominance is driven by the fundamental need for cutting, grinding, milling, drilling, and turning operations across automotive, aerospace, and general engineering sectors. Removal fluids provide critical lubrication, cooling, chip management, and tool protection, ensuring consistent productivity in metal removal processes. They remain the backbone of machining operations due to their wide applicability across various metals and operational conditions.

U.S. Metalworking Fluids Market generated USD 2.6 billion in 2025. Growth in North America, particularly in the United States, is supported by a strong industrial base encompassing automotive manufacturing, aerospace component fabrication, and machinery production. The demand for high-performance fluids, including removal, semi-synthetic, and forming fluids, is sustained by the requirement for precision, efficiency, and reliability in engine, transmission, and structural component manufacturing. Advanced infrastructure, established production facilities, and stringent quality standards continue to drive regional market adoption.

Key players operating in the Global Metalworking Fluids Market include Quaker Houghton, ExxonMobil, FUCHS Petrolub SE, Blaser Swisslube, Chevron (Caltex), TotalEnergies, Idemitsu Kosan, Shell (Shell Lubricants), Milacron (Cimcool), Master Fluid Solutions, Yushiro Chemical, Petron Corporation, Oemeta Chemische Werke, Phoenix Petroleum Philippines, and BP Castrol. Companies in the Global Metalworking Fluids Market are strengthening their positions by focusing on product innovation, sustainability, and technical support. Leading manufacturers are developing high-performance synthetic and semi-synthetic fluids with improved thermal stability, lubricity, and emulsion life to meet the demands of modern machining operations. Strategic collaborations with OEMs and industrial partners enable customized solutions tailored to specific metalworking processes. Expansion into emerging regions, coupled with efficient supply chain management, allows companies to widen their global footprint.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product

- 2.2.2 Application

- 2.2.3 End Use

- 2.2.4 Regional

- 2.3 TAM Analysis, 2025-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter';s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Future market trends

- 3.10 Technology and innovation landscape

- 3.10.1 Current technological trends

- 3.10.2 Emerging technologies

- 3.11 Patent landscape

- 3.12 Trade statistics (HS code)

( Note: the trade statistics will be provided for key countries only)

- 3.12.1 Major importing countries

- 3.12.2 Major exporting countries

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.14 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Neat oil

- 5.3 Soluble oil

- 5.4 Semi-synthetic fluid

- 5.5 Synthetic fluid

Chapter 6 Market Estimates and Forecast, By Application, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Removal fluids

- 6.3 Forming fluids

- 6.4 Protecting fluids

- 6.5 Treating fluids

Chapter 7 Market Estimates and Forecast, By End Use, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Automotive

- 7.3 Aerospace

- 7.4 Construction

- 7.5 Electrical & power

- 7.6 Agriculture

- 7.7 Marine

- 7.8 Healthcare

- 7.9 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Quaker Houghton

- 9.2 FUCHS Petrolub SE

- 9.3 ExxonMobil

- 9.4 Shell (Shell Lubricants)

- 9.5 BP Castrol

- 9.6 Chevron (Caltex)

- 9.7 TotalEnergies

- 9.8 Idemitsu Kosan

- 9.9 Yushiro Chemical

- 9.10 Blaser Swisslube

- 9.11 Master Fluid Solutions

- 9.12 Milacron (Cimcool)

- 9.13 Oemeta Chemische Werke

- 9.14 Petron Corporation

- 9.15 Phoenix Petroleum Philippines

金属加工液市场:2026-2032年全球市场预测(依产品类型、最终用途产业、製程、原料及销售管道)

金属加工液市场:2026-2032年全球市场预测(依产品类型、最终用途产业、製程、原料及销售管道) 金属加工液全球市场报告(2026 年)

金属加工液全球市场报告(2026 年) 2026-2030年全球金属加工液市场

2026-2030年全球金属加工液市场 日本金属加工液市场报告:按产品类型、原料、最终用途、流体类型、产业和地区划分(2026-2034年)

日本金属加工液市场报告:按产品类型、原料、最终用途、流体类型、产业和地区划分(2026-2034年) 全球金属加工液市场(至 2030 年):按类型(直馏油、水溶性油、半合成油、合成油)、产品类型(除油、防銹油、成型油、加工油)、最终用户产业和地区划分2025 年至 2033 年金属加工液市场报告(按产品类型、来源、最终用途、液体类型、产业和地区)

全球金属加工液市场(至 2030 年):按类型(直馏油、水溶性油、半合成油、合成油)、产品类型(除油、防銹油、成型油、加工油)、最终用户产业和地区划分2025 年至 2033 年金属加工液市场报告(按产品类型、来源、最终用途、液体类型、产业和地区) 全球金属加工液市场预测(截至 2030 年):按产品、功能、最终用户和地区进行分析

全球金属加工液市场预测(截至 2030 年):按产品、功能、最终用户和地区进行分析 全球金属加工液市场规模、产品类型、最终用户产业、地区、范围和预测

全球金属加工液市场规模、产品类型、最终用户产业、地区、范围和预测