|

市场调查报告书

商品编码

1936509

奈米纤维素在复合材料和涂料领域的市场:机会、成长动力、产业趋势分析和预测(2026-2035年)Nanocellulose in Composites and Coatings Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

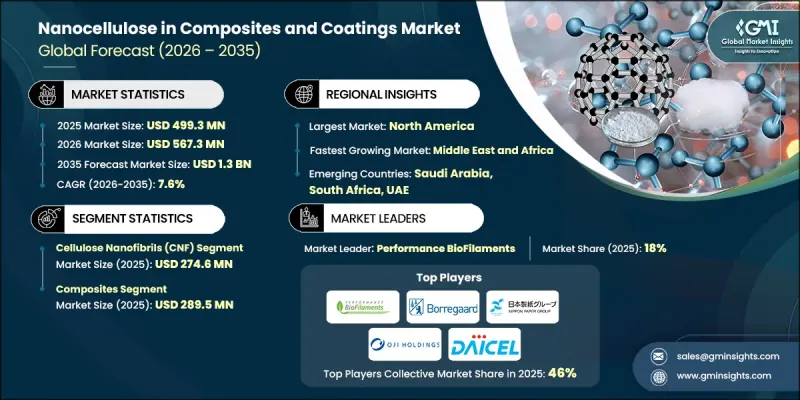

2025 年全球复合材料和涂料用奈米纤维素市场价值为 4.993 亿美元,预计到 2035 年将达到 13 亿美元,年复合成长率为 7.6%。

奈米纤维素是指至少一个维度尺寸为奈米级的纤维素材料,通常提取自植物纤维、细菌和藻类。该材料包括纤维素奈米晶体、纤维素奈米纤维和细菌纤维素,它们在尺寸、结构和结晶质系统中的功能性添加剂。即使在低添加量下,奈米纤维素也能改善材料的机械性能、耐热性和阻隔性能。它能够在增强聚合物基体的同时保持轻质特性,因此在包装、建筑和工业材料应用领域有着广泛的需求。此外,对永续性关注也进一步加速了奈米纤维素的应用,各产业越来越重视可再生和可生物降解的材料解决方案。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始金额 | 4.993亿美元 |

| 预测金额 | 13亿美元 |

| 复合年增长率 | 7.6% |

奈米纤维素在涂料配方中具有显着的性能优势,包括增强成膜性、改善阻隔性能和提高流变控制能力。其对氧气、水分和油的渗透性降低,使其在防护性和功能性涂料应用中日益重要。奈米纤维素与多种涂料系统的相容性使其能够在不影响环境性能的前提下,提高表面均匀性和耐久性。这些效能优势正推动其在多个终端应用领域的需求稳定成长。

预计到2025年,纤维素奈米纤维市场规模将达到2.746亿美元。纤维素奈米纤维和微纤化纤维素因其长而柔韧的纤维网络,能够显着提高增强性能、韧性和黏度控制,因此在复合材料和涂料领域得到广泛应用。这些材料能够高效分散在聚合物和涂料系统中,从而实现均匀的结构形成和表面均匀性的提升。相对简单的加工要求也进一步促进了它们在各种材料配方中的广泛应用。

预计到2025年,复合材料市场规模将达到2.895亿美元。奈米纤维素能够提高复合材料系统的刚度、耐久性和负荷分布,同时保持轻质特性。其天然来源使其能够开发出更永续的复合材料,作为传统合成增强材料的替代方案。奈米纤维素与多种基材的相容性使其在众多产业的结构和半结构复合材料应用中都具有广泛的应用前景。

预计到2025年,北美复合材料和涂料领域的奈米纤维素市场规模将达到2.833亿美元。先进的工业基础设施、永续材料的高普及率以及交通运输、航太和包装行业的稳定需求,都将推动市场成长。持续加大研发投入和材料创新也将进一步增强该地区的市场前景。政府鼓励使用环保材料的奖励正在加速其应用,而美国凭藉其大规模生产能力、先进的製造技术以及消费者对永续产品日益增强的意识,在北美奈米纤维素市场中处于领先地位。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段的附加价值

- 影响价值链的因素

- 中断

- 产业影响因素

- 成长驱动因素

- 对永续材料的需求日益增长

- 生产技术进步

- 增强的机械性质和阻隔性能

- 产业潜在风险与挑战

- 高昂的生产成本

- 分散性和相容性问题

- 市场机会

- 高性能复合材料的开发

- 与智慧材料的集成

- 致力于循环经济

- 成长驱动因素

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特五力分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 依产品类型

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 专利状态

- 贸易统计(HS编码)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续努力

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 考虑到碳足迹

第四章 竞争情势

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 重大进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章 依产品类型分類的市场估算与预测,2022-2035年

- 纤维素奈米晶体(CNC)

- 纤维素奈米纤维(CNF)

- 细菌奈米纤维素(BNC)

- 微纤化纤维素(MFC/CMF)

第六章 按应用领域分類的市场估算与预测,2022-2035年

- 复合材料

- 高分子复合材料

- 汽车复合材料

- 建材

- 用于包装的复合材料

- 电子设备/先进材料

- 涂层

- 纸张和包装用阻隔涂层

- 纤维涂层/表面处理

- 功能性和保护性涂层

- 农业薄膜和智慧涂层

第七章 2022-2035年各地区市场估算与预测

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿拉伯聯合大公国

- 其他中东和非洲地区

第八章 公司简介

- Anomera Inc.

- Blue Goose Biorefineries Inc.

- Borregaard AS

- CelluComp Ltd.

- Daicel Corporation

- GranBio Technologies

- Kao Corporation

- Kruger Inc.

- Melodea Ltd.

- Nippon Paper Industries Co., Ltd.

- Oji Holdings Corporation

- Performance BioFilaments

- Seiko PMC Corporation

The Global Nanocellulose in Composites and Coatings Market was valued at USD 499.3 million in 2025 and is estimated to grow at a CAGR of 7.6% to reach USD 1.3 billion by 2035.

Nanocellulose refers to cellulose materials that feature at least one dimension at the nanometer scale and are commonly sourced from plant fibers, bacteria, or algae. The material portfolio includes cellulose nanocrystals, cellulose nanofibrils, and bacterial cellulose, each defined by variations in size, structure, and crystallinity. Nanocellulose offers a unique combination of high mechanical strength, low density, large surface area, biodegradability, and adaptable surface chemistry. These characteristics position it as a valuable reinforcement agent in advanced composites and as a functional additive in coating systems. Even at low loadings, nanocellulose enhances mechanical, thermal, and barrier performance. Its ability to strengthen polymer matrices while preserving lightweight characteristics supports demand across packaging, construction, and industrial material applications. Sustainability considerations further accelerate adoption as industries increasingly favor renewable and biodegradable material solutions.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $499.3 Million |

| Forecast Value | $1.3 Billion |

| CAGR | 7.6% |

Nanocellulose also delivers strong performance benefits within coating formulations by supporting film formation, improving barrier efficiency, and enhancing rheological control. The material reduces permeability to oxygen, moisture, and oils, expanding its relevance in protective and functional coating applications. Its compatibility with various coating systems allows manufacturers to achieve improved surface uniformity and durability without compromising environmental performance. These functional advantages continue to support consistent demand growth across multiple end-use sectors.

The cellulose nanofibrils segment reached USD 274.6 million in 2025. Cellulose nanofibrils and microfibrillated cellulose remain widely adopted due to their long, flexible fiber networks that significantly improve reinforcement, toughness, and viscosity control in composites and coatings. These materials disperse efficiently within polymer and coating systems, enabling uniform structure formation and enhanced surface consistency. Their relatively straightforward processing requirements further support their broad adoption across diverse material formulations.

The composites segment generated USD 289.5 million in 2025. Nanocellulose strengthens composite systems by improving stiffness, durability, and load distribution while maintaining low material weight. Its natural origin enables the development of more sustainable composite alternatives to traditional synthetic reinforcements. Compatibility with multiple matrix types allows nanocellulose to support both structural and semi-structural composite applications across a wide range of industries.

North America Nanocellulose in Composites and Coatings Market captured USD 283.3 million in 2025. Growth is supported by advanced industrial infrastructure, high adoption of sustainable materials, and consistent demand from transportation, aerospace, and packaging sectors. Continued investment in research and material innovation further strengthens the regional outlook. Government incentives encouraging environmentally responsible materials accelerate adoption, while the US leads the region through scaled production capabilities, advanced manufacturing technologies, and growing consumer awareness regarding sustainable products.

Key companies active in the Global Nanocellulose in Composites and Coatings Market include Borregaard AS, Anomera Inc., Nippon Paper Industries Co., Ltd., Melodea Ltd., Kruger Inc., Kao Corporation, Performance BioFilaments, Daicel Corporation, CelluComp Ltd., Blue Goose Biorefineries Inc., Seiko PMC Corporation, Oji Holdings Corporation, and GranBio Technologies. Companies operating in the market focus on expanding production capacity and improving material consistency to strengthen their competitive position. Strategic investments in process optimization help reduce costs and enable large-scale commercialization. Many players prioritize partnerships with composite and coating manufacturers to accelerate application development and market penetration. Continuous research into surface modification and performance enhancement supports product differentiation.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product Type

- 2.2.2 Application

- 2.2.3 Regional

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for sustainable materials

- 3.2.1.2 Technological advancements in production

- 3.2.1.3 Enhanced mechanical and barrier properties

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production costs

- 3.2.2.2 Dispersion and compatibility issues

- 3.2.3 Market opportunities

- 3.2.3.1 Development of high-performance composites

- 3.2.3.2 Integration with smart materials

- 3.2.3.3 Circular economy initiatives

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product type

- 3.9 Future market trends

- 3.10 Technology and innovation landscape

- 3.10.1 Current technological trends

- 3.10.2 Emerging technologies

- 3.11 Patent landscape

- 3.12 Trade statistics (HS code)

- 3.12.1 Major importing countries

- 3.12.2 Major exporting countries

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.14 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Cellulose nanocrystals (CNC)

- 5.3 Cellulose nanofibrils (CNF)

- 5.4 Bacterial nanocellulose (BNC)

- 5.5 Microfibrillated cellulose (MFC/CMF)

Chapter 6 Market Estimates and Forecast, By Application, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Composites

- 6.2.1 Polymer matrix composites

- 6.2.2 Automotive composites

- 6.2.3 Construction & building materials

- 6.2.4 Packaging composites

- 6.2.5 Electronics & advanced materials

- 6.3 Coatings

- 6.3.1 Paper & packaging barrier coatings

- 6.3.2 Textile coatings & surface treatments

- 6.3.3 Functional & protective coatings

- 6.3.4 Agricultural films & smart coatings

Chapter 7 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Rest of Europe

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.4.6 Rest of Asia Pacific

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.5.4 Rest of Latin America

- 7.6 Middle East and Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

- 7.6.4 Rest of Middle East and Africa

Chapter 8 Company Profiles

- 8.1 Anomera Inc.

- 8.2 Blue Goose Biorefineries Inc.

- 8.3 Borregaard AS

- 8.4 CelluComp Ltd.

- 8.5 Daicel Corporation

- 8.6 GranBio Technologies

- 8.7 Kao Corporation

- 8.8 Kruger Inc.

- 8.9 Melodea Ltd.

- 8.10 Nippon Paper Industries Co., Ltd.

- 8.11 Oji Holdings Corporation

- 8.12 Performance BioFilaments

- 8.13 Seiko PMC Corporation

奈米纤维素市场:按类型、原料、形态、应用和最终用途产业划分-2026-2032年全球市场预测纤维素奈米晶体市场:按类型、原料、形态、製造流程、应用、终端用户产业划分,全球预测(2026-2032年)

奈米纤维素市场:按类型、原料、形态、应用和最终用途产业划分-2026-2032年全球市场预测纤维素奈米晶体市场:按类型、原料、形态、製造流程、应用、终端用户产业划分,全球预测(2026-2032年) 日本奈米纤维素市场报告(按产品类型(奈米原纤化纤维素、奈米晶纤维素、细菌纤维素、微纤化纤维素及其他)、应用和地区划分,2026-2034年)

日本奈米纤维素市场报告(按产品类型(奈米原纤化纤维素、奈米晶纤维素、细菌纤维素、微纤化纤维素及其他)、应用和地区划分,2026-2034年) 奈米纤维素市场机会、成长要素、产业趋势分析及2026年至2035年预测

奈米纤维素市场机会、成长要素、产业趋势分析及2026年至2035年预测 全球奈米纤维素市场(至 2035 年):依奈米纤维素、应用、分销管道、地区、产业趋势和预测

全球奈米纤维素市场(至 2035 年):依奈米纤维素、应用、分销管道、地区、产业趋势和预测 纤维素奈米晶体增强生物聚合物市场规模、份额和趋势分析报告:按产品、应用、地区和细分市场预测(2025-2033 年)用于包装应用的纤维素奈米晶体市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)

纤维素奈米晶体增强生物聚合物市场规模、份额和趋势分析报告:按产品、应用、地区和细分市场预测(2025-2033 年)用于包装应用的纤维素奈米晶体市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年) 芴:全球市场占有率和排名、总收入和需求预测(2025-2031年)微纤化纤维素(MFC):全球市场份额和排名、总收入和需求预测(2025-2031年)

芴:全球市场占有率和排名、总收入和需求预测(2025-2031年)微纤化纤维素(MFC):全球市场份额和排名、总收入和需求预测(2025-2031年) 奈米纤维素市场-全球产业规模、份额、趋势、机会与预测,按类型(CNF、细菌纤维素、CNC)、按应用、按地区和竞争细分,2020-2030 年预测

奈米纤维素市场-全球产业规模、份额、趋势、机会与预测,按类型(CNF、细菌纤维素、CNC)、按应用、按地区和竞争细分,2020-2030 年预测