|

市场调查报告书

商品编码

1936512

电动汽车电池组件市场机会、成长要素、产业趋势分析及2026年至2035年预测Electric Vehicle (EV) Battery Components Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

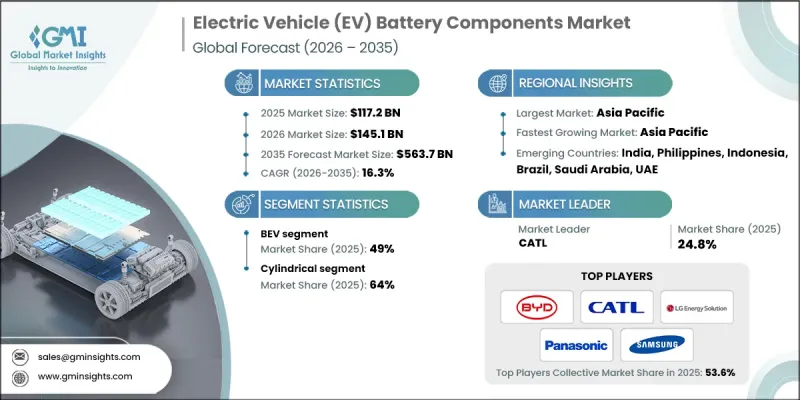

全球电动车电池组件市场预计到 2025 年将达到 1,172 亿美元,到 2035 年将达到 5,637 亿美元,年复合成长率为 16.3%。

全球电动车的快速普及正在改变汽车动力传动系统设计,并重塑供应链。电池单元、模组、正极、阳极、电池管理系统 (BMS) 和温度控管解决方案等组件如今已成为决定车辆续航里程、性能、安全性和成本效益的核心要素。随着汽车製造商从内燃机转向专用电动车架构,电池系统正日益被视为完全整合的平台,而非独立的组件,这影响着营运可行性和全生命週期经济性。汽车製造商、电池製造商、材料供应商和半导体公司之间的大规模投资和策略联盟进一步推动了市场发展。垂直整合策略,例如内部电池组装、本地化电池生产以及正负极材料的合资企业,使原始设备製造商 (OEM) 能够确保供应、降低成本并提高品质。此外,广泛的组件测试、全生命週期优化以及对国际安全标准的遵守,都提高了产品的可靠性、耐久性和热安全性。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 1172亿美元 |

| 预测金额 | 5637亿美元 |

| 复合年增长率 | 16.3% |

预计到2025年,电池式电动车(BEV)市场份额将达到49%,并在2035年之前以17%的复合年增长率成长。纯电动车完全依赖电池动力,因此对高容量电池、模组及相关系统有着强劲的需求,以确保长续航里程、快速充电和稳定的性能。全球范围内支持零排放汽车的政策和奖励正在进一步加速纯电动车的普及,使其成为市场发展的关键驱动力。

预计到2025年,圆柱形电池市占率将达到64%,并在2026年至2035年间以15.7%的复合年增长率成长。这些电池因其性能可靠、能量密度高、温度控管出色以及循环寿命长而备受青睐。其模组化设计和标准化尺寸使其能够无缝整合到电池组中,从而简化组装、维护和回收。此外,圆柱形电池还具有更高的安全性、可靠的散热性能以及在高电流负载下的耐久性,使其成为乘用车和商用电动车应用的首选。

预计到2025年,中国电动车电池零件市场将占据显着份额。中国快速的工业化进程、强劲的国内电动车需求以及高度整合的供应链体系,都为市场的蓬勃发展提供了强力支撑。作为主要的电动车生产中心,中国对电池电芯、正极材料、负极材料、隔膜、电解和外壳等零件的需求持续强劲。中国对上游锂精炼、正极材料製造和石墨负极材料生产的掌控,确保了成本效益、快速规模生产和稳定的供应。此外,透过与生产连结奖励计画和长期产业规划等政策支持,进一步加速了电池零件各领域的技术应用和产能扩张。

目录

第一章调查方法

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率分析

- 成本结构

- 每个阶段的附加价值

- 影响价值链的因素

- 中断

- 产业影响因素

- 司机

- 全球电动乘用车和商用车的普及率不断提高

- 政府加大奖励、补助和电动车基础设施投资

- 电池超级工厂扩建及区域产能扩张

- 物流、公共运输和车队车辆电气化进展

- 产业潜在风险与挑战

- 关键电池原物料高成本且价格波动大

- 缺乏大规模电池回收和废弃电池处理基础设施

- 市场机会

- 扩大新一代电池化学技术和固态电池组件的应用

- 电动车和电池国产化政策推动国内製造业成长。

- 对先进电池管理系统和电力电子产品的需求激增

- 二次利用和回收电池组件应用领域的成长

- 司机

- 成长潜力分析

- 监管环境

- 北美洲

- 美国:NHTSA自动驾驶系统引导与自动驾驶车辆测试倡议

- 欧洲

- 欧盟电池法规(欧盟法规 2023/1542)

- 德国:电池法(Batteriegesetz-BattG)

- 英国:电池和蓄电池法规

- 法国:电池生产者延伸责任制(EPR)

- 亚太地区

- 中国:新能源汽车动力电池安全与回收管理条例

- 日本:经济产业省锂离子电池安全与回收指南

- 韩国:《电气电子设备与车辆资源化回收法》

- 新加坡:环境保护与管理(电池废弃物)条例

- 拉丁美洲

- 巴西:国家固态废弃物政策(电力逆向物流法规)

- 墨西哥:官方标准 NOM-212-SEMARNAT(电池废弃物管理)

- 智利:生产者延伸责任法(第20920号法律)

- 中东和非洲

- 阿联酋:联邦综合废弃物管理法(电池相关条款)

- 沙乌地阿拉伯:环境法和SASO电动车电池技术法规

- 南非:《国家环境管理法》-《废弃物法》(电池合规性)

- 北美洲

- 波特五力分析

- PESTEL 分析

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 专利分析

- 永续性和环境影响分析

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

- 未来前景与机会

- OEM实施框架

- 垂直整合趋势

- 长期供应合约及其对零件价格的影响

- 优选供应商模式和公开采购

- 共同开发和合资模式

- 使用案例和应用场景

- 全球产能与运转率分析

- 运作能与公布产能对比

- 各区域的运转率

- 面临产能过剩及供不应求风险的地区

- 识别组件中的瓶颈

第四章 竞争情势

- 介绍

- 公司市占率分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 重大进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 企业扩张计画和资金筹措

第五章 依电池类型分類的市场估计与预测,2022-2035年

- 圆柱形

- 袋式

- 棱镜电池

6. 2022-2035年按推进方式分類的市场估计与预测

- 电池式电动车(BEV)

- PHEV

- HEV

第七章 依车辆类型分類的市场估计与预测,2022-2035年

- 搭乘用车

- 轿车

- 掀背车

- SUV

- 商用车辆

- 轻型商用车(LCV)

- MCV

- 重型商用车(HCV)

- 两轮车和三轮车

8. 2022-2035年按电池化学类型分類的市场估算与预测

- 磷酸锂铁

- 镍钴铝合金

- 镍、锰、钴

- 锰酸锂

- 其他的

第九章 按组件分類的市场估算与预测,2022-2035年

- 细胞成分

- 阴极

- 阳极

- 电解质

- 其他的

- 包装零件

- 电池管理系统

- 温度控管系统

- 外壳和围护结构

- 其他的

第十章 2022-2035年各地区市场估计与预测

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 比利时

- 荷兰

- 瑞典

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 菲律宾

- 印尼

- 新加坡

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

第十一章:公司简介

- 世界公司

- BASF SE

- BYD

- Contemporary Amperex Technology Co. Limited(CATL)

- Johnson

- LG Energy Solution

- Panasonic

- Samsung

- Umicore

- Arkema

- 当地公司

- Asahi Kasei

- BTR New Energy Materials

- Celgard

- EVE Energy

- Ganfeng Lithium

- Gotion High-Tech

- Huayou Cobalt

- JFE Chemical

- Mitsubishi Chemical

- SK Innovation

- Sumitomo Metal Mining

- Toray Industries

- 新兴企业

- Amprius Technologies

- Anovion Technologies

- Ascend Elements

- FREYR Battery

- QuantumScape

- Redwood Materials

The Global Electric Vehicle Battery Components Market was valued at USD 117.2 billion in 2025 and is estimated to grow at a CAGR of 16.3% to reach USD 563.7 billion by 2035.

The rapid adoption of electric vehicles worldwide is transforming automotive powertrain design and reshaping supply chains. Components such as battery cells, modules, cathodes, anodes, battery management systems (BMS), and thermal management solutions are now central to determining vehicle range, performance, safety, and cost efficiency. As automakers shift from internal combustion engines to dedicated EV architectures, battery systems are increasingly treated as fully integrated platforms rather than individual parts, influencing both operational viability and lifecycle economics. The market is further boosted by large-scale investments and strategic collaborations among automakers, battery manufacturers, material suppliers, and semiconductor firms. Vertical integration strategies, including in-house battery assembly, localized cell production, and joint ventures for cathode and anode materials, are enabling OEMs to secure supplies, lower costs, and improve quality. Additionally, extensive component testing, lifecycle optimization, and adherence to global safety standards are enhancing product reliability, durability, and thermal safety.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $117.2 Billion |

| Forecast Value | $563.7 Billion |

| CAGR | 16.3% |

The battery electric vehicle (BEV) segment held 49% share in 2025 and is expected to grow at a CAGR of 17% through 2035. BEVs rely entirely on battery power, driving strong demand for high-capacity cells, modules, and associated systems to ensure long driving ranges, rapid charging, and consistent performance. Global policies and incentives supporting zero-emission vehicles further accelerate BEV adoption, positioning this segment as the primary growth driver for the market.

The cylindrical cells segment held 64% share in 2025, with projected growth at a CAGR of 15.7% from 2026 to 2035. These cells are favored for their proven performance, high energy density, superior thermal management, and long lifecycle. Their modular design and standardized sizes allow seamless integration into battery packs, simplifying assembly, maintenance, and recycling. Cylindrical cells also provide enhanced safety, reliable heat dissipation, and durability under high current loads, making them a preferred choice for both passenger and commercial EV applications.

China Electric Vehicle (EV) Battery Components Market reached a significant share in 2025. The country's rapid industrialization, strong domestic EV demand, and extensive supply chain integration support robust market expansion. China's dominant EV production base drives ongoing demand for battery cells, cathodes, anodes, separators, electrolytes, and casings. Control over upstream lithium refining, cathode manufacturing, and graphite anode production ensures cost efficiency, rapid scaling, and stable supply. Policy support through production-linked incentives and long-term industrial planning further accelerates technology adoption and capacity expansion across battery component segments.

Key players shaping the Global Electric Vehicle Battery Components Market include CATL, BYD, Panasonic, Blue Line Battery, Johnson Matthey, Mitsubishi Chemical, LG Energy Solution, Samsung SDI, Sumitomo Metal Mining, and Umicore. Leading companies in the Electric Vehicle Battery Components Market are adopting multiple strategies to strengthen their market presence and competitive position. These include forming strategic alliances with automakers and material suppliers to secure raw material access, investing in localized manufacturing to reduce costs and improve supply chain resilience, and expanding R&D efforts to develop next-generation high-capacity, fast-charging, and longer-lasting battery systems. Companies are also enhancing production scalability, integrating advanced thermal management and battery management technologies, and pursuing mergers or joint ventures to enter new geographic markets. Focused testing, lifecycle optimization, and adherence to global safety and environmental standards further improve product reliability, building trust among OEMs and fleet operators and solidifying long-term market foothold.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Battery Form

- 2.2.3 Propulsion

- 2.2.4 Vehicle

- 2.2.5 Battery Chemistry

- 2.2.6 Component

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global adoption of electric passenger and commercial vehicles

- 3.2.1.2 Increase in government incentives, subsidies, and EV infrastructure investments

- 3.2.1.3 Expansion of battery giga factories and localized manufacturing capacity

- 3.2.1.4 Growing electrification of logistics, public transport, and fleet vehicles

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost and price volatility of critical battery raw materials

- 3.2.2.2 Limited large-scale battery recycling and end-of-life infrastructure

- 3.2.3 Market opportunities

- 3.2.3.1 Rise in adoption of next-generation battery chemistries and solid-state components

- 3.2.3.2 Increase in domestic manufacturing supported by EV and battery localization policies

- 3.2.3.3 Surge in demand for advanced battery management systems and power electronics

- 3.2.3.4 Growth in second life and recycling-based battery component applications

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 United States: NHTSA ADS Guidance & AV TEST Initiative.

- 3.4.2 Europe

- 3.4.2.1 EU Battery Regulation (Regulation (EU) 2023/1542)

- 3.4.2.2 Germany: Battery Act (Batteriegesetz - BattG)

- 3.4.2.3 United Kingdom: Batteries and Accumulators Regulations

- 3.4.2.4 France: Extended Producer Responsibility (EPR) for Batteries

- 3.4.3 Asia Pacific

- 3.4.3.1 China: New Energy Vehicle Power Battery Safety & Recycling Regulations

- 3.4.3.2 Japan: METI Lithium-Ion Battery Safety & Recycling Guidelines

- 3.4.3.3 South Korea: Act on Resource Circulation of Electrical & Electronic Equipment and Vehicles

- 3.4.3.4 Singapore: Environmental Protection and Management (Battery Waste) Regulations

- 3.4.4 Latin America

- 3.4.4.1 Brazil: National Solid Waste Policy (Battery Reverse Logistics Rules)

- 3.4.4.2 Mexico: Official Standard NOM-212-SEMARNAT (Battery Waste Management)

- 3.4.4.3 Chile: Extended Producer Responsibility Law (Law No. 20,920)

- 3.4.5 MEA

- 3.4.5.1 United Arab Emirates: Federal Integrated Waste Management Law (Battery Provisions)

- 3.4.5.2 Saudi Arabia: Environmental Law & SASO EV Battery Technical Regulations

- 3.4.5.3 South Africa: National Environmental Management - Waste Act (Battery Compliance)

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Patent analysis

- 3.9 Sustainability and environmental impact analysis

- 3.9.1 Sustainable practices

- 3.9.2 Waste reduction strategies

- 3.9.3 Energy efficiency in production

- 3.9.4 Eco-friendly initiatives

- 3.9.5 Carbon footprint considerations

- 3.10 Future outlook & opportunities

- 3.11 OEM implementation framework

- 3.11.1 Vertical integration trends

- 3.11.2 Long-term offtake agreements & their impact on component pricing

- 3.11.3 Preferred supplier models vs open procurement

- 3.11.4 Co-development & joint venture models

- 3.12 Use Cases & application scenarios

- 3.13 Global capacity & utilization analysis

- 3.13.1 Installed vs announced component capacity

- 3.13.2 Regional utilization rates

- 3.13.3 Overcapacity & under-supply risk zones

- 3.13.4 Component bottleneck identification

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Battery Form, 2022 - 2035 ($Bn, Units)

- 5.1 Key trends

- 5.2 Cylindrical

- 5.3 Pouch

- 5.4 Prismatic

Chapter 6 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Bn, Units)

- 6.1 Key trends

- 6.2 BEV

- 6.3 PHEV

- 6.4 HEV

Chapter 7 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Bn, Units)

- 7.1 Key trends

- 7.2 Passenger Cars

- 7.2.1 Sedan

- 7.2.2 Hatchback

- 7.2.3 SUV

- 7.3 Commercial vehicle

- 7.3.1 LCV

- 7.3.2 MCV

- 7.3.3 HCV

- 7.4 Two- & Three-Wheelers

Chapter 8 Market Estimates & Forecast, By Battery Chemistry, 2022 - 2035 ($Bn, Units)

- 8.1 Key trends

- 8.2 Lithium iron phosphate

- 8.3 Nickel cobalt aluminum

- 8.4 Nickel manganese cobalt

- 8.5 Lithium manganese oxide

- 8.6 Others

Chapter 9 Market Estimates & Forecast, By Component, 2022 - 2035 ($Bn, Units)

- 9.1 Key trends

- 9.2 Cell Components

- 9.2.1 Cathode

- 9.2.2 Anode

- 9.2.3 Electrolyte

- 9.2.4 Others

- 9.3 Pack Components

- 9.3.1 Battery Management System

- 9.3.2 Thermal Management System

- 9.3.3 Housing & Enclosure

- 9.3.4 Others

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Belgium

- 10.3.8 Netherlands

- 10.3.9 Sweden

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Philippines

- 10.4.7 Indonesia

- 10.4.8 Singapore

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 BASF SE

- 11.1.2 BYD

- 11.1.3 Contemporary Amperex Technology Co. Limited (CATL)

- 11.1.4 Johnson

- 11.1.5 LG Energy Solution

- 11.1.6 Panasonic

- 11.1.7 Samsung

- 11.1.8 Umicore

- 11.1.9 Arkema

- 11.2 Regional Players

- 11.2.1 Asahi Kasei

- 11.2.2 BTR New Energy Materials

- 11.2.3 Celgard

- 11.2.4 EVE Energy

- 11.2.5 Ganfeng Lithium

- 11.2.6 Gotion High-Tech

- 11.2.7 Huayou Cobalt

- 11.2.8 JFE Chemical

- 11.2.9 Mitsubishi Chemical

- 11.2.10 SK Innovation

- 11.2.11 Sumitomo Metal Mining

- 11.2.12 Toray Industries

- 11.3 Emerging Players

- 11.3.1 Amprius Technologies

- 11.3.2 Anovion Technologies

- 11.3.3 Ascend Elements

- 11.3.4 FREYR Battery

- 11.3.5 QuantumScape

- 11.3.6 Redwood Materials

电动车电力电子市场预测至2034年-按组件、半导体材料、功率元件类型、车辆类型、电压架构、整合度和地区分類的全球分析

电动车电力电子市场预测至2034年-按组件、半导体材料、功率元件类型、车辆类型、电压架构、整合度和地区分類的全球分析 汽车金属化薄膜电容器市场报告:趋势、预测与竞争分析(至2035年)

汽车金属化薄膜电容器市场报告:趋势、预测与竞争分析(至2035年) 2026年全球电动车(EV)包装运输箱市场监测报告

2026年全球电动车(EV)包装运输箱市场监测报告 新能源诊断设备市场:按类型、技术、应用、最终用户和分销管道划分,全球预测,2026-2032年

新能源诊断设备市场:按类型、技术、应用、最终用户和分销管道划分,全球预测,2026-2032年 电动车保险桿市场规模、份额和成长分析:按材质、车辆类型、製造流程分析、通路和地区划分-2026-2033年产业预测

电动车保险桿市场规模、份额和成长分析:按材质、车辆类型、製造流程分析、通路和地区划分-2026-2033年产业预测 2026-2034年全球电动车工程塑胶市场规模、份额、趋势及成长分析全球自我调整交通底盘市场预测(至2034年):按底盘类型、材料、车辆类型、技术、最终用户和地区划分

2026-2034年全球电动车工程塑胶市场规模、份额、趋势及成长分析全球自我调整交通底盘市场预测(至2034年):按底盘类型、材料、车辆类型、技术、最终用户和地区划分 日本电动汽车零件市场规模、份额、趋势及预测(按零件、分销管道和地区划分),2026-2034年日本电动车电池组件市场:规模、份额、趋势和预测:按组件类型、电池类型、车辆类型、推进系统、最终用户和地区划分(2026-2034 年)

日本电动汽车零件市场规模、份额、趋势及预测(按零件、分销管道和地区划分),2026-2034年日本电动车电池组件市场:规模、份额、趋势和预测:按组件类型、电池类型、车辆类型、推进系统、最终用户和地区划分(2026-2034 年) 电动车零件市场-全球产业规模、份额、趋势、机会及预测(按车辆类型、动力类型、零件类型、地区和竞争格局划分,2021-2031年)

电动车零件市场-全球产业规模、份额、趋势、机会及预测(按车辆类型、动力类型、零件类型、地区和竞争格局划分,2021-2031年)