|

市场调查报告书

商品编码

1936549

生质燃料市场机会、成长要素、产业趋势分析及2026年至2035年预测Biofuel Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

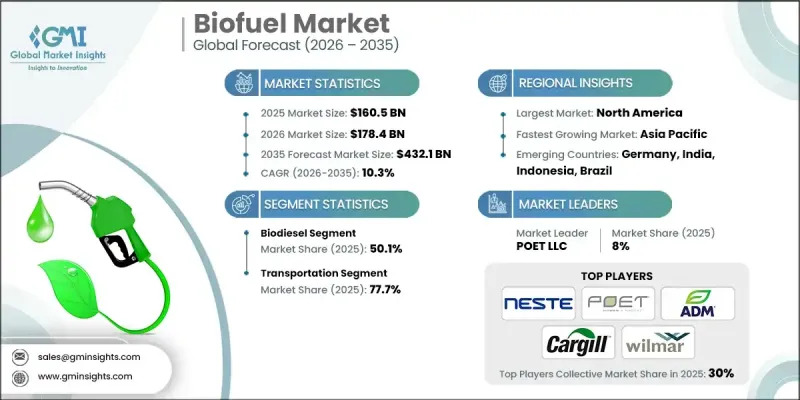

全球生质燃料市场预计到 2025 年将达到 1,605 亿美元,到 2035 年将达到 4,321 亿美元,年复合成长率为 10.3%。

旨在推动交通运输业脱碳的持续监管要求,正在全球范围内推动可预测且可持续的生质燃料需求。各国政府正日益将生命週期碳强度降低纳入燃料政策,并建立合规市场,使低碳燃料生产商能够获得可交易的碳信用额度。这些法规规范了检验和可追溯性,降低了买方风险,并强化了销售合约。因此,公路、航空和海运领域对乙醇、生质柴油、可再生柴油(氢化植物油,HVO)、沼气/压缩生物气(CBG)和永续航空燃料(SAF)的需求正在增长。积极的政策管理,包括合规时间表和豁免机制,维护了市场的确定性,使依赖稳定供应来开展产业计画和资本计划的农民、炼油商和燃料调配商受益。诸如低碳燃料标准(LCFS)等项目持续扩展,鼓励以废弃物和残渣为基础的生质燃料,扩大基础设施和交通运输领域的碳信用额度机会,并支持利用废弃食用油、动物脂肪、垃圾掩埋沼气和有机废弃物进行大规模生产。

| 市场覆盖范围 | |

|---|---|

| 开始年份 | 2025 |

| 预测年份 | 2026-2035 |

| 起始值 | 1605亿美元 |

| 预测金额 | 4321亿美元 |

| 复合年增长率 | 10.3% |

预计到2025年,生质柴油市占率将达到50.1%,并在2035年之前以10.5%的复合年增长率成长。生产商正投资改造碳排放设施,以减少生命週期排放,提高在低碳燃料标准(LCFS)等框架下的碳排放强度(CI)评分,并在国内外合规市场获得更高的经济回报。生质柴油持续受益于严格的碳排放强度政策和不断增加的监管奖励,从而推动了以废弃物和剩余原料为原料的燃料的维修。

预计到2025年,交通运输业将占全球需求的77.7%,并在2035年之前以9.5%的复合年增长率成长。监管要求、合规主导的信贷市场以及可直接可再生燃料的普及,使得交通运输业成为最稳定、最大的需求来源。各国政府正优先考虑在该领域生质燃料,尤其是在重型卡车、市政车辆和长途物流领域,因为生物燃料无需对车辆或基础设施进行重大改造即时减少排放。能源安全问题以及减少对进口石化燃料依赖的需求,进一步推动了已开发经济体和新兴经济体对生质燃料的采用。

预计到2025年,美国生质燃料市场规模将达到546亿美元,占93%的市场。其主导地位得益于成熟的法规环境、完善的原料供应链以及有利于低碳燃料的合规机制。能源安全优先事项、石化燃料价格波动以及企业致力于货运、航空和航运业脱碳的承诺,都在增强政治支持,所有这些因素都在加速生质燃料的消费。

目录

第一章调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 监管环境

- 产业影响因素

- 司机

- 产业潜在风险与挑战

- 成长潜力分析

- 波特五力分析

- PESTEL 分析

- 新的机会与趋势

- 数位化和物联网集成

- 拓展新兴市场

第四章 竞争情势

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 中东和非洲

- 拉丁美洲

- 策略倡议

- 竞争标竿分析

- 战略仪錶板

- 创新与科技趋势

第五章 依燃料类型分類的市场规模及预测(2022-2035年)

- 生质柴油

- 乙醇

- 其他的

第六章 依原料分類的市场规模及预测(2022-2035年)

- 粗粒颗粒

- 糖料作物

- 植物油

- 其他的

第七章 依应用领域分類的市场规模及预测(2022-2035年)

- 运输

- 航空领域

- 其他的

第八章 2022-2035年各地区市场规模及预测

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 法国

- 西班牙

- 英国

- 义大利

- 亚太地区

- 中国

- 印度

- 印尼

- 澳洲

- 韩国

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 拉丁美洲

- 巴西

- 阿根廷

第九章:公司简介

- ADM

- Borregaard

- BTG Bioliquids

- Cargill

- Chevron Corporation

- Clariant

- COFCO

- CropEnergies

- FutureFuel

- Munzer Bioindustrie

- My Eco Energy

- Neste Corporation

- POET

- Praj Industries

- The Andersons

- TotalEnergies

- UPM

- Verbio

- Wilmar International

- Zilor

The Global Biofuel Market was valued at USD 160.5 billion in 2025 and is estimated to grow at a CAGR of 10.3% to reach USD 432.1 billion by 2035.

Continuous regulatory mandates aimed at decarbonizing transportation are driving predictable and durable demand for biofuels worldwide. Governments are increasingly embedding lifecycle carbon intensity reductions into fuel policies, creating compliance markets where producers can earn tradable credits for supplying lower-carbon fuels. These regulations standardize verification and traceability, reducing buyer risk and strengthening offtake agreements, which in turn boosts demand for ethanol, biodiesel, renewable diesel (HVO), biogas/CBG, and sustainable aviation fuels across road, aviation, and marine segments. Active policy management, including compliance timelines and waiver mechanisms, maintains market certainty, benefiting farmers, refiners, and fuel blenders who rely on consistent volumes for operational and capital planning. Programs such as Low Carbon Fuel Standards (LCFS) are expanding, incentivizing waste- and residue-based biofuels and broadening credit opportunities for infrastructure and transit, supporting large-scale production from used cooking oil, animal fats, landfill gas, and organic waste streams.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $160.5 Billion |

| Forecast Value | $432.1 billion |

| CAGR | 10.3% |

The biodiesel segment accounted for 50.1% share in 2025 and is projected to grow at a CAGR of 10.5% through 2035. Producers are investing in carbon capture retrofits to reduce lifecycle emissions, improve CI scores under LCFS-like frameworks, and qualify for higher economic returns in both domestic and export compliance markets. Biodiesel continues to benefit from stringent carbon-intensity policies and increasing regulatory incentives, encouraging fleets to adopt fuels derived from waste and residue feedstocks.

The transportation sector represented 77.7% share in 2025 and is expected to grow at a CAGR of 9.5% by 2035. Transport remains the most stable and largest demand center due to regulatory mandates, compliance-driven credit markets, and availability of drop-in renewable fuels. Governments prioritize biofuels in this sector because they achieve immediate emissions reductions without major vehicle or infrastructure modifications, especially in heavy-duty trucking, municipal fleets, and long-haul logistics. Energy security concerns and the need to reduce dependence on imported fossil fuels further reinforce biofuel adoption in developed and emerging economies.

U.S. Biofuel Market held 93% share, generating USD 54.6 billion in 2025. Leadership is driven by a mature regulatory ecosystem, well-developed feedstock supply chains, and compliance mechanisms that reward lower-carbon fuels. Political support is reinforced by energy security priorities, fossil fuel price volatility, and corporate decarbonization commitments from freight, aviation, and maritime industries, which collectively accelerate biofuel consumption.

Key players in the Global Biofuel Market include ADM, Borregaard, BTG Bioliquids, Cargill, Chevron Corporation, Clariant, COFCO, CropEnergies, FutureFuel, Munzer Bioindustrie, My Eco Energy, Neste Corporation, POET, Praj Industries, The Andersons, TotalEnergies, UPM, Verbio, Wilmar International, and Zilor. Companies in the biofuel industry are deploying several strategies to strengthen their market presence. They are investing in R&D to develop low-carbon and waste-based feedstocks, improving efficiency and compliance with regulatory frameworks. Strategic partnerships with local feedstock suppliers and transportation firms expand supply chains and market reach. Businesses are also investing in advanced production infrastructure, including carbon capture retrofits and scale-up of renewable diesel and sustainable aviation fuel capacity. Market penetration is further reinforced through government engagement, lobbying for favorable policies, and participation in compliance credit programs.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitment

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

- 1.9 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Fuel trends

- 2.1.3 Feedstock trends

- 2.1.4 Application trends

- 2.1.5 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technology factors

- 3.6.5 environmental factors

- 3.6.6 Legal factors

- 3.7 Emerging opportunities & trends

- 3.7.1 Digitalization and IoT integration

- 3.7.2 Emerging market penetration

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic initiatives

- 4.4 Competitive benchmarking

- 4.5 Strategic dashboard

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Fuel, 2022 - 2035 (USD Million, Mtoe)

- 5.1 Key trends

- 5.2 Biodiesel

- 5.3 Ethanol

- 5.4 Others

Chapter 6 Market Size and Forecast, By Feedstock, 2022 - 2035 (USD Million, Mtoe)

- 6.1 Key trends

- 6.2 Coarse grain

- 6.3 Sugar crop

- 6.4 Vegetable oil

- 6.5 Others

Chapter 7 Market Size and Forecast, By Application, 2022 - 2035 (USD Million, Mtoe)

- 7.1 Key trends

- 7.2 Transportation

- 7.3 Aviation

- 7.4 Others

Chapter 8 Market Size and Forecast, By Region, 2022 - 2035 (USD Million, Mtoe)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 France

- 8.3.3 Spain

- 8.3.4 UK

- 8.3.5 Italy

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Indonesia

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 South Africa

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

Chapter 9 Company Profiles

- 9.1 ADM

- 9.2 Borregaard

- 9.3 BTG Bioliquids

- 9.4 Cargill

- 9.5 Chevron Corporation

- 9.6 Clariant

- 9.7 COFCO

- 9.8 CropEnergies

- 9.9 FutureFuel

- 9.10 Munzer Bioindustrie

- 9.11 My Eco Energy

- 9.12 Neste Corporation

- 9.13 POET

- 9.14 Praj Industries

- 9.15 The Andersons

- 9.16 TotalEnergies

- 9.17 UPM

- 9.18 Verbio

- 9.19 Wilmar International

- 9.20 Zilor

乳化燃料市场:2026-2032年全球市场预测(按燃料类型、混合比例、分销管道、应用和最终用户划分)

乳化燃料市场:2026-2032年全球市场预测(按燃料类型、混合比例、分销管道、应用和最终用户划分) 燃油品质感测器-全球市场份额和排名、总销售量和需求预测(2026-2032 年)

燃油品质感测器-全球市场份额和排名、总销售量和需求预测(2026-2032 年) 2026年全球生质燃料催化剂市场研究报告

2026年全球生质燃料催化剂市场研究报告 交通运输用生质燃料的市场机会、成长要素、产业趋势分析及 2026-2035 年预测。

交通运输用生质燃料的市场机会、成长要素、产业趋势分析及 2026-2035 年预测。 生质燃料:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

生质燃料:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 全球交通运输用生质燃料市场:规模、份额、趋势和成长分析报告(2026-2034年)全球生物氢市场规模、份额、趋势和成长分析报告(2026-2034年)全球生质燃料市场规模、份额、趋势和成长分析报告(2026-2034年)

全球交通运输用生质燃料市场:规模、份额、趋势和成长分析报告(2026-2034年)全球生物氢市场规模、份额、趋势和成长分析报告(2026-2034年)全球生质燃料市场规模、份额、趋势和成长分析报告(2026-2034年) 日本生质燃料市场规模、份额、趋势和预测:按类型、原材料和地区划分,2026-2034年

日本生质燃料市场规模、份额、趋势和预测:按类型、原材料和地区划分,2026-2034年 2026年全球单细胞油市场报告

2026年全球单细胞油市场报告